Are severance pay subject to insurance contributions in the event of a layoff? Every employer should know the answer to this question. After all, when an employee is dismissed due to the liquidation of an enterprise or a reduction in staff, he must be guaranteed to be paid not only wages for the period worked, but also compensation for unused vacation days. The employer is required to pay tax and insurance contributions on each payment. In addition, the employee must be paid severance pay, which is also subject to personal income tax and other contributions, but under certain conditions. How does this happen? Let's look at it in more detail.

The main mistakes when calculating severance pay to an employee laid off from work

The process of laying off employees entails large costs for the employer, so most organizations that dismiss their subordinates from service due to a reduction in the number of staff try by hook or by crook to avoid unnecessary expenses. Most often, they insist that the employee write a letter of resignation of his own free will or offer a transfer to another position. However, this cannot be done. The current legislation clearly defines the sequence of the staff reduction procedure, as well as information regarding all payments and their taxation. Therefore, every employer is obliged to adhere to the correct dismissal “scheme” in order to avoid problems with the law.

Answer

6-NDFL

In 6-NDFL, do not reflect severance benefits paid within three average earnings.

The fact is that severance pay that does not exceed three times the average earnings is not subject to personal income tax (clause 3 of Article 217 of the Tax Code of the Russian Federation). And there is no need to reflect non-taxable payments in form 6-NDFL (letters of the Federal Tax Service of Russia dated March 24, 2016 No. BS-4-11/5106, dated March 23, 2016 No. BS-4-11/4901, dated March 23, 2016 No. BS-4- 11/ [email protected] ).

Accordingly, if you did not record payments in 6-NDFL, no adjustment is needed.

If you wrote it down, please submit updated calculations. Incorrect indicators in 6-NDFL are subject to a fine of 500 rubles. (Article 126.1 of the Tax Code of the Russian Federation).

ERSV

In the calculation of insurance premiums, you should have recorded severance payments in the lines with the total amount of payments and with non-taxable amounts. Let's explain in more detail.

In the calculation of insurance premiums, you record all payments in favor of employees accrued under employment contracts and civil contracts for work or services (clauses 1 and 2 of Article 420 of the Tax Code of the Russian Federation and clause 7.5 of the procedure for filling out the calculation, approved by order of the Federal Tax Service of Russia dated 10.10.2016 No. ММВ-7-11/ [email protected] ).

Thus, in subsections 1.1 and 1.2 you will include amounts in severance payments within three average earnings in the indicators on lines 030 and 040. In Appendix 2 you will record severance payments on lines 020 and 030.

If you did not reflect severance payments in your contribution calculations, submit updated calculations. True, if you don’t file, you won’t face a fine. Tax authorities fine for errors in the calculation of contributions, which led to underpayment of contributions (Article 120 of the Tax Code of the Russian Federation). And if you did not show non-taxable payments in the calculation, this error did not lead to an underpayment. But in order to avoid unnecessary questions from inspectors, we still advise you to submit clarifications.

- When filling out the RSV-1 form for the first quarter, check whether there were any payments to those fired. As a general rule, Section 6 does not need to be filled out for dismissed employees. But the situation is different if the former employee received payments subject to insurance premiums in the reporting quarter

- When filling out section 6 of the RSV-1 form, use the example and sample

- If a dismissed employee brought sick leave, this is not a reason to include it in RSV-1

How is severance pay calculated upon dismissal due to staff reduction?

Judging by the Labor Code of the Russian Federation, upon termination of an employment relationship due to the liquidation of an enterprise or a reduction in the number of staff, the employer is obliged to pay a severance pay to the dismissed employee, the amount of which is formed from the amount of average earnings for 1 calendar month. In addition, the employee is entitled to an average monthly salary and compensation payments for vacation days not taken off.

It is also worth noting that if, during employment at this enterprise, a clause was specified in the contract containing information about the amount of compensation in the event of dismissal at the initiative of the employer, then in such a situation the law allows for increased payments to the employee. However, its size cannot be increased more than 6 times.

What taxes are levied on compensation for staff reduction?

Today, not every organization can talk about its stability; against the backdrop of the current economic situation, many enterprises, including state-owned ones, have to take measures such as reducing the number of their employees.

Since in such situations the employee is the most vulnerable party, the legislator in the labor code has established certain guarantees and compensations that the laid-off worker can count on.

In order to avoid labor disputes and problems with the tax service in the event of a reduction procedure, the organization should know what compensation an employee is entitled to in the event of a reduction in staff, and what taxes it is subject to.

According to articles 84.1, 140 of the Labor Code of the Russian Federation

on the day of dismissal, the employer is obliged to pay the laid-off employee all amounts due to him from the employer.

This should include the following payments:

Wages for time actually worked before dismissal.

Compensation for unused vacation days

Severance pay in the amount of average monthly earnings in case of dismissal due to reduction. From part one and part two of Art. 178 of the Labor Code of the Russian Federation it follows that a laid-off employee has the right to receive:

on the day of dismissal - severance pay in the amount of average earnings;

if during the second month from the date of dismissal the employee does not find a job - the average earnings for that month;

If within two weeks from the date of dismissal the employee applied to the employment service and was not employed by him within three months from the date of dismissal, then in exceptional cases, by decision of the employment agency, the employee is paid the average salary for this third month.

Additional compensation in the amount of average earnings, calculated in proportion to the time remaining before the expiration of the notice period for dismissal, if the employment contract is terminated with the written consent of the employee before the expiration of the two-month notice period for staff reduction. The fact is that according to the general rule enshrined in part two of Art. 180 of the Labor Code of the Russian Federation, the employee must be warned by the employer personally and against signature of the upcoming dismissal due to staff reduction at least two months before the dismissal. The notice must indicate the specific date of dismissal. At the same time, by virtue of part three of Art. 180 of the Labor Code of the Russian Federation, the employer, with the written consent of the employee, has the right to terminate the employment contract with him before the expiration of the period specified in part two of the same article of the Labor Code of the Russian Federation, paying him additional compensation in the amount of the employee’s average earnings, calculated in proportion to the time remaining before the expiration of the notice period for dismissal .

Taxation of compensation.

In the first part of the article, we determined what kind of compensation an employee is entitled to when staffing is reduced, now let’s figure out what taxes it is subject to.

Within the meaning of paragraph 1 of Art. 210 of the Tax Code of the Russian Federation, the taxpayer’s tax base includes:

- income expressed in monetary form;

— income expressed in kind;

-material benefit in the context of Article 212 of the Tax Code of the Russian Federation.

In addition, for tax purposes, income received from sources in the Russian Federation, clause 6, clause 1, article 208 of the Tax Code, includes payment for such actions performed in the Russian Federation as:

— fulfillment of labor duties;

- completed work;

— service provided;

Based on the content of the two above articles, the correct conclusion is that the salary that the employee received for the month of work preceding the moment of dismissal, like all previous payments for labor, is the employee’s income. As a result, the tax agent must withhold personal income tax in the amount of 13% from this salary.

Regarding the question of what taxes are levied on compensation for staff reduction , then according to clause 3 of Art. 217 Tax Code of the Russian Federation

All types of compensation payments established by the legislation of the Russian Federation, legislative acts of the constituent entities of the Russian Federation, decisions of representative bodies of local self-government compensation, including compensation payments related to the dismissal of an employee, are not subject to personal income tax.

The position of the Ministry of Finance of the Russian Federation was expressed on this same topic in a Letter dated February 17, 2006. No. 03-05-01-03/18 and Letter dated February 9, 2006 No. 03-05-01-04/22.

The Department of the Federal Tax Service for the city of Moscow outlined its attitude to the issue:

- in Letter dated June 18, 2009 No. 20-14/3/061778,

— In Letter dated August 21, 2006 No. 28-10/73963,

- in Letter dated August 29, 2005 No. 28-11/61080.

They, in particular, contain instructions that compensation payments related to the dismissal of an employee and paid in accordance with Art. 178 Labor Code of the Russian Federation.

Compensation payments should include:

— severance pay in the amount of average monthly earnings;

— average monthly earnings for the period of employment.

In practice, situations arise when the amount of severance pay payable in connection with a reduction in the number of workers exceeds the norms established by the Tax Code (Article 178). The reasons for this are provisions that improve the rights of the worker, either prescribed in his employment contract, or adopted by a local act of the organization in which he works.

In such situations, the tax should still be withheld, but with the following features:

So, according to Art. 255 Tax Code of the Russian Federation

severance pay, which is paid to employees upon dismissal in excess of the norm established in Art. 178 of the Labor Code of the Russian Federation, refers to accruals for employees released due to reorganization or liquidation of the taxpayer, reduction in the number (staff) of employees, and, accordingly, reduces the tax base for the income tax of taxpayers-organizations.

At the same time, from that part of the benefits due to the laid-off employee that exceeds those specified in Art. 178 of the Labor Code of the Russian Federation, the size of the tax must be withheld on personal income. (Confirmation of this conclusion was reflected in Letters of the Ministry of Finance No. 03-03-06/2/168, 03-03-06/1/546).

We will also touch upon the issue of taxation of compensation that the employer pays to the employee if the latter gives his consent to the early termination of the employment contract (before the end of the notice period).

In the above case, the person being laid off is entitled to compensation, the amount of which is calculated in proportion to the time that remains until dismissal based on the Warning, and is paid based on average earnings.

Regarding the taxation of this compensation, the Russian Ministry of Finance expressed its position in letter dated March 11, 2009 No. 03-04-06-01/54. According to the Ministry of Finance, the above payment is subject to the rules established by clause 3 of Art. 217 Tax Code of the Russian Federation.

Now, regarding compensation for unused vacation days.

From para. 6 clause 3 art. 217 of the Tax Code of the Russian Federation it follows that

compensation for unused vacations is not included in the list of those compensations paid to an employee upon dismissal, which are not taxed.

Simply put, payments due to a redundant employee as compensation for unused vacation days are subject to personal income tax in the generally accepted manner.

There are corresponding letters on this topic: Federal Tax Service of Russia for Moscow dated May 7, 2008 No. 28-10/044275, Federal Tax Service of Russia dated March 13, 2006 No. 04-1-03/133.

When is severance pay due?

Upon receipt of written notice of dismissal due to staff reduction, the employee is not required to write a letter of resignation of his own free will, because then he will not be able to receive severance pay. To reduce the number of employees, the company must have a reason for this. As a rule, the reason for reducing staff is most often the closure of one of the company’s branches, liquidation of production, financial problems, etc.

Immediately after making a decision to reduce staff, the manager issues an order, which must be correctly executed and registered. The document specifies a list of positions subject to reduction and the dates of their planned dismissal. Then a commission is assembled that checks the correctness of the reduction process and the timing of the execution of the order. All workers subject to dismissal with subsequent receipt of severance pay must be familiarized with the order.

According to Articles 178, 180 and 140 of the Labor Code of the Russian Federation, the employer is obliged to transfer severance pay and all other payments upon dismissal due to reduction on the employee’s last working day.

In case of termination of the employment relationship, regardless of the reason, the calculation of benefits is carried out on the form T61. It takes into account the hours actually worked and calculates the salary and other payments due to the resigning employee.

What you need to know about severance pay?

Severance pay is a type of financial assistance for a dismissed employee until he finds a new job.

Since in this case we mean termination of the employment contract through the fault of the employer (and on the grounds established by Article 178 of the Labor Code of the Russian Federation), the company is obliged to pay the employee the amount of compensation.

Upon dismissal by agreement of the parties

The existence of an agreement between the parties indicates that management and the employee agreed on the need to dismiss the latter. In this regard, benefits under the Labor Code of the Russian Federation are not paid to the employee. But, as part 4 of Article 178 of the Labor Code of the Russian Federation states, the employer can include the provision on severance pay in the list of employee rights in other cases, including by agreement of the parties. It is fixed in an employment or collective agreement.

When staffing is reduced

Staff reduction is a reduction in the number of employees in an organization. In this regard, employees dismissed on this basis are entitled to compensation in the form of severance pay.

The payment amount is:

- average monthly earnings;

- the average salary retained by the employee for the period of employment, but not more than 2 months from the date of termination of the employment contract.

The benefit is calculated in accordance with Article 139 of the Labor Code of the Russian Federation and the government act. Equal to several average monthly salaries (usually two).

The average salary is calculated based on the amount of money actually accrued to the employee and data on how much time he worked in the twelve previous calendar months (by these we mean the period from the 1st to the 30th/31st inclusive, and in February - to the 28th/29th). All other forms of payments, regardless of their sources, used by a particular employer are also taken into account.

The law lists payments that cannot be used when calculating average earnings. For example, these include bonuses, sick leave, maternity benefits and other paid days away from work.

The average salary of an employee cannot be less than the minimum subsistence level established by law. Also, this amount does not depend on the age, length of service or qualification level of the citizen.

If an employee has worked for an organization for less than 1 year, to calculate the average salary and benefits, the time during which he was officially on the staff is taken into account. In a situation where a citizen worked for less than a month before the reduction of staff, the tariff rate or salary is used for calculation.

Liquidation of the enterprise

Russian legislation understands liquidation as a forced or voluntary, complete cessation of the activities of any organization (manufacturing enterprise or company).

With this form of closure of a legal entity, its rights and obligations are not transferred to another organization, therefore all employees with whom it has an employment contract are subject to dismissal with the payment of appropriate compensation. One of them is also a benefit.

The most important obligation of the employer during liquidation is to promptly notify the employee of dismissal in writing, 2 months before the upcoming termination of activity.

Severance pay during liquidation is calculated in the same way as in the case of staff reduction. Also, the average monthly earnings for 2 months are taken as a basis, which is the total amount of the benefit. It is assumed that during this period the employee will be looking for work.

Funds are disbursed on the day the employment relationship ends, when full payment is ready. Funds to employees are paid from the employer's budget, which includes a certain amount to be spent in the event of liquidation of the company.

Payment of the total amount of severance pay is carried out in the following order:

- benefits on the day of dismissal;

- compensation payment after the expiration of the first month following dismissal;

- refund for the second month, which is final.

However, according to labor legislation, cases arise when an employee can receive payment even after two months have passed from the date of dismissal. If he is registered with the employment center within 2 weeks of losing his job, he can extend the period of detention for another 1 month.

This is possible if no suitable position has been found for the employee within 2 months. Severance pay due to liquidation does not affect the assignment of unemployment benefits.

Sometimes it is possible to reduce the amount of compensation. For example, this applies to those employees who are employed in seasonal jobs. They are given severance pay equal to two weeks' average earnings.

Conscription

If the cancellation of an employee’s employment contract is related to his conscription into military or alternative civilian service, he is entitled to severance pay in the amount of the average salary for 2 weeks. To be eligible for this payment, the conscript must present at his place of work a summons to appear at the military registration and enlistment office to be sent to serve.

Based on this document, an order is issued to terminate the employment contract under clause 1 of part 1 of Article 83 of the Labor Code of the Russian Federation. By analogy with the situations described above, the future serviceman receives the severance pay due to him on the day of dismissal.

If he is absent from the workplace at this time, the corresponding amounts must be transferred no later than the next day after the dismissed person submits a request for payment.

To establish the average salary, the amount accrued for a regular working day is used in the following cases:

- vacation pay;

- issuing compensation for vacations that the employee did not take;

- other cases provided for by the Labor Code of the Russian Federation, with the exception of the situation when the average earnings are determined in relation to an employee for whom summarized recording of working time has been introduced.

Average earnings are calculated according to the rule: the daily payment that an employee receives under normal conditions is multiplied by the number of days (calendar, working) in the period to be calculated.

How is severance pay calculated for employees during layoffs?

The issuance of severance pay upon dismissal is a mandatory detail during the personnel reduction procedure. Its size in 2018 can be calculated using the following formula:

VP = RD*NW, in which

VP is the amount of severance pay;

RD - the number of working days in the month following dismissal;

SZ – average daily earnings.

Average daily earnings are calculated using the formula:

SZ = GD/730, in which GD is the income for the last 2 years worked at the enterprise.

Let's look at an example:

Ivanov M.I worked for the company for 2 years, after which he was laid off due to a reduction in the number of staff. His earnings during this time amounted to 153,750 rubles, minus sick leave, travel allowance and other payments not related to payroll. Based on this, we calculate the average earnings using the formula: 153,750 rubles / 730 = 210.62 rubles.

To determine the amount of severance pay, we turn to the formula indicated above: 20 * 210.62 rubles = 4212.40 rubles.

Thus, the amount of benefits for dismissal due to reduction due to M.I. Ivanov is 4212.40 rubles.

Calculation

The fact is that the average amount of earnings per day is calculated for the day on which the employee worked, and not for the one indicated in the calendar . To correctly calculate the benefit amount, you need to take the wages received 12 months before the employee was fired.

In this case, you do not need to take into account vacations and sick leave. Next, you need to divide the resulting value by the working day in the above-mentioned periods, which are marked in the production calendar.

Weekends and vacation pay are not taken into account because during these periods the employee did not fulfill his work duties.

Is severance pay taxable due to a reduction in headcount or workforce? If we are talking about a tax such as personal income tax, then all of the above payments are not subject to taxation of this type.

The only exceptions to this are the salary that is paid for the month of dismissal and compensation for vacation that the dismissed employee did not use. This is regulated by Articles 208, 210 and 217 of the Tax Code of the Russian Federation.

What insurance premiums are deducted from the severance pay upon dismissal due to reduction?

Severance pay paid to an employee upon dismissal from work is not subject to insurance contributions, but only if its limit does not exceed the amount established by law. As a rule, its amount is determined based on the average monthly salary for the last 2 years of work.

Insurance contributions are accrued on severance pay assigned upon dismissal due to reduction in the following cases:

- the amount of payments accrued to a laid-off employee for the period of searching for a new job exceeds the average monthly salary by 3 times. In this situation, the amount of deductible contributions will be calculated from the excess amount;

- the amount of payments given to an employee dismissed due to layoffs from an enterprise located in the Far North exceeds the average monthly salary by more than 6 times. In this case, insurance premiums will be deducted from the excess portion of the benefit.

What is due to an employee being laid off due to redundancy?

When dismissal due to staff reduction, the law protects the rights of the more vulnerable party - the employee. The Labor Code of the Russian Federation provides for several types of guarantees that make it possible to make the separation of an employee and an employer less painful. This includes money that the employer is obliged to pay in order not to violate labor laws:

- Salary. It is important to note that you must pay everything that is due to the employee on the date of dismissal, incl. employer's debts for previous periods. But if an employee has any debts to the employer, then most of them can be deducted from the salary only with the written consent of the employee.

Example

The employee still has accountable amounts for which he did not submit an advance report. You cannot simply adjust the severance payment to the amount of the employee's debt. You need to negotiate with him and get his consent to deduct from your salary.

- Compensation for unused vacation. When dismissal due to staff reduction is calculated in the usual manner, without any nuances.

- Severance pay in case of layoff. Below we will discuss in detail how to calculate it.

- Average earnings during employment. It must be paid for the 2nd and 3rd months after dismissal (for workers in the Far North - also for 4-6 months). But the former employee is required to confirm that he has not been employed anywhere in the past period. To do this, he must submit a work book that does not contain a record of employment, or information about work activity - in accordance with the new rules for maintaining electronic work books (Article 66.1 of the Labor Code of the Russian Federation). The average salary for the 3rd month after dismissal (for 4-6 for northerners) is paid only if the employee has presented a decision from the employment authority that he needs to retain his earnings for this period (Article 178 of the Labor Code of the Russian Federation).

- Sick leave benefit. If the employee falls ill within 30 days after the date of dismissal due to reduction. True, unlike “working” sick leave, “dismissal” leave is always paid in the amount of 60% of average earnings.

There is no doubt that if the reduction is made due to coronavirus infection, the employment service will be more willing to issue decisions on maintaining the average salary from the previous employer for the dismissed person for the maximum possible period.

Is personal income tax withheld from severance pay assigned upon dismissal due to reduction?

Income tax on wages and compensation for unused vacation, which are paid upon dismissal, is withheld at 13%. The reason for the employee leaving work does not play any role here.

Severance pay assigned to an employee resigning due to staff reduction, according to Article 217 of the Tax Code of the Russian Federation, is not subject to taxes. However, as mentioned earlier, its size should not exceed the average monthly earnings by more than 6 times in the regions of the Far North, and more than 3 times in other constituent entities of the Russian Federation.

From the obviously inflated amount of payments, a tax deduction will be withheld to the budget according to all the rules. Based on Article 226 of the Tax Code of the Russian Federation, the transfer of personal income tax in this case is carried out no later than the next working day after the total payment amount is transferred to the employee.

How are severance payments not specified in the Labor Code of the Russian Federation taxed?

In some situations, the employer may have difficulty classifying payments as compensation in terms of their taxation with personal income tax using benefits, for example, upon retirement or dismissal by agreement of the parties.

According to para. 1 clause 3 art. 217 of the Tax Code of the Russian Federation, benefits are provided in relation to payments established at the legislative level (federal, regional, municipal).

In Part 4 of Art. 178 of the Labor Code of the Russian Federation provides that an employment or collective agreement may establish other cases of payment of severance pay, except for those provided for in Parts 1–3 of Art. 178 of the Labor Code of the Russian Federation, and increased amounts of severance pay.

Consequently, compensation paid upon retirement or dismissal by agreement of the parties can be regarded as provided in accordance with the law, provided that they are provided for by an employment or collective agreement (Part 4 of Article 178 of the Tax Code of the Russian Federation).

IMPORTANT! In case of dismissal by agreement of the parties, the condition for payment of compensation may be provided for in a separate agreement, which is an integral part of the employment contract (Article 57 of the Labor Code of the Russian Federation).

In paragraph 3 of Art. 217 of the Tax Code of the Russian Federation provides that compensation paid upon dismissal is not subject to personal income tax if it does not exceed three times the average monthly earnings (six times the average monthly earnings for workers dismissed from organizations in the Far North and equivalent areas). Provisions of paragraph 3 of Art. 217 of the Tax Code of the Russian Federation are applied regardless of the grounds on which the dismissal is made (see letter of the Federal Tax Service of Russia dated May 25, 2017 No. BS-4-11/9933).

Consequently, if the two above conditions are met, compensation paid upon dismissal, including by agreement of the parties or upon retirement, is not subject to personal income tax (clause 3 of Article 217 of the Tax Code of the Russian Federation, letter of the Ministry of Finance of Russia dated February 12, 2018 No. 03-04- 06/8420, dated 02.28.2017 No. 03-04-06/11087, Federal Tax Service of Russia dated 05.25.2017 No. BS-4-11/9933, ruling of the Supreme Court of the Russian Federation dated 06.16.2017 No. 307-KG16-19781).

If the compensation payment is more than three times the average monthly earnings (six times the average monthly earnings for workers dismissed from organizations in the Far North and similar areas), then personal income tax is withheld from the excess amount (letter of the Ministry of Finance of Russia dated February 12, 2018 No. 03-04-06/8420 , dated 02.28.2017 No. 03-04-06/11087, Federal Tax Service of Russia dated 05.25.2017 No. BS-4-11/9933). The tax must be withheld upon actual payment of compensation and transferred to the budget no later than the day following the day of payment to the employee (clauses 4, 6 of Article 226 of the Tax Code of the Russian Federation).

Severance pay for layoffs in 2021, personal income tax and insurance contributions

In this article, we will look at whether severance pay is subject to insurance premiums during layoffs. In general, the personnel reduction procedure is a very costly project for an enterprise, so many managers try to avoid this by asking employees to write a letter of resignation of their own free will, but not all employees succumb to this persuasion, yes, in fact, this is wrong. There is another opportunity to avoid quite serious expenses - to offer the employee another, vacant position in the same organization, but here the employee has the right to refuse this offer.

Are severance pay subject to insurance premiums upon layoffs in 2021: features and most common mistakes

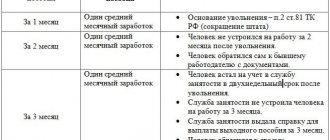

For example, upon liquidation of an organization, as well as upon reduction of the number or staff of a company (clause 1.2 of Article 81 of the Labor Code of the Russian Federation), the employee is paid severance pay in the amount of average monthly earnings, and for the period of employment - as a general rule, no more than 2 months from day of dismissal - he retains his average monthly earnings (Article 178 of the Labor Code of the Russian Federation). All employee salaries are subject to insurance contributions: to the pension fund, medical and social insurance fund.

Severance pay, as well as other compensation (except for compensation for unused vacation) paid to a dismissed employee, are subject to contributions when their amount exceeds a certain limit (subclause “e”, paragraph 2, part 1, article 9 of the Law of July 24, 2009 No. 212-FZ, paragraph 2, clause 1, article 20.2 of the Law of July 24, 1998 No. 125-FZ). Limits for different categories of employees are shown in the table below.

In addition to legally established cases, the payment of severance pay may be provided for by an employment or collective agreement, a local regulatory act of the organization, as well as a separate agreement with the employee (Articles 178, 181 of the Labor Code of the Russian Federation).

Basis for payment of severance pay and other compensation

For example, upon liquidation of an organization, as well as upon reduction of the number or staff of a company (clause 1.2 of Article 81 of the Labor Code of the Russian Federation), the employee is paid severance pay in the amount of average monthly earnings, and for the period of employment - as a general rule, no more than 2 months from day of dismissal - he retains his average monthly earnings (Article 178 of the Labor Code of the Russian Federation).

What payments are due to an employee upon dismissal?

Retrenched employees must receive:

1. Standard charges that are transferred to the account on the last business day:

- salary for the period of time worked, as well as due allowances, bonuses and other payments;

- compensation for unused vacation days;

- severance pay, the amount of which is not less than the average monthly salary for one month, unless a different amount of this payment is specified in the employment or collective agreement;

- additional compensation paid in the event of dismissal ahead of the time specified in the notice of layoff. The amount of this compensation is equal to the average salary for a given period. Thus, an employer can dismiss an employee only with the latter’s consent.

We recommend

“How to resolve conflicts with employees - instructions for managers” More details

2. Benefits due to non-employment from the moment of dismissal in case of staff reduction (not paid to employees hired for less than two months):

- payment of sick leave if temporary disability occurred within a period of up to 30 calendar days from the last working day;

- payments in the amount of the average salary for the second and third months if it is impossible to find a job (the amount for the first month is transferred on the last working day), if the employee provides documents confirming the lack of work.

To receive unemployment benefits for the second month from the date of dismissal, you must fill out an application and present your work record book at your former place of work. Severance pay for the third month in the amount of the average salary is accrued only under special circumstances.

To do this, the following conditions must be met:

- the employee does not have material resources;

- disabled family members are dependent on the person;

- the employee contacted the employment center within 14 days from the date of dismissal, and they could not find him a job;

- availability of a decision on the right to receive this payment, issued by the employment service.