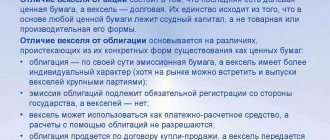

What is it and why is it needed

A discount bill is a bill that is sold at a price lower than its face value (discount is the price difference). Its use allows the drawer to raise borrowed funds and the holder to make a profit.

Thus, a discount bill differs from a bank bill only in the purchase price: the first is sold at a discount, and the second at par. In general, this is still the same debt security that allows its owner to demand money from the person (or company) who issued it.

Features when working with discount bills

- It is not an issue-grade security and does not require state registration.

- Repayment always occurs at par, regardless of the term and other circumstances. The holder can sell it to the bank before the deadline, but in this case the credit institution will take its commission. The purchase of a document by a bank is called bill discounting.

- Unlike bank deposits, investments in bills (including discount bills) are not protected. In the event of bankruptcy of the drawer (and they are not always distinguished by their reliability), the state will not compensate for your losses. However, if the document contains an aval, then the person who supplied it (or the company) is jointly and severally liable for this debt. Such papers are more reliable, but are rarely used in practice.

- A discount bill is used not only as an investment (or fundraising) instrument. It is also used for settlements with counterparties, repayment of debts to creditors, or as collateral.

Accounting for bills of exchange: postings

Often, a promissory note in a buyer-seller relationship plays the role of a promissory note, since it arises in a situation where the buyer cannot pay for the goods with available funds, and the seller agrees to accept the bill. Such a commodity bill is not considered a security until it is transferred to a third party. To account for such bills, the buyer has an account. 60 open a subaccount 60/3 “Bills issued”, and the seller opens a subaccount 62/3 “Bills received”.

Transactions with it are recorded on both sides in the settlement accounts by postings:

| Operation | D/t | K/t |

| Accounting entries for bills issued | ||

| Reflected delivery debt | 60/1 | 60/3 |

| Security for future payment issued (behind balance) | 009 | |

| If the bill is interest-bearing, then the buyer’s debt will increase by the amount of accrued interest | 91 | 60/3 |

| Repayment of a debt | 60/3 | 51 |

| Writing off the bill after payment | 009 | |

| Accounting entries for bills received | ||

| The debt on the shipped goods is reflected | 62/ 3 | 62/1 |

| Payment security received | 008 | |

| Interest income from the bill | 62/3 | 91 |

| Received payment for goods secured by a bill of exchange | 51 | 62/3 |

| Writing off a bill after receiving payment | 008 | |

Example 1

Blitz LLC, to secure payment obligations under the supply agreement, Atrium LLC issued a promissory note in the amount of RUB 236,000. including VAT RUB 36,000. The accounting records of both organizations will reflect:

Operation D/t K/t Sum At Blitz LLC Debt to supplier for goods 41 60/1 200 000 VAT 19 60/1 36 000 A bill of exchange was issued 60/1 60/3 236 000 The bill is included in the balance sheet 009 236 000 Amortization 60/3 51 236 000 Writing off a bill 009 236 000 At Atrium LLC Revenue reflected 62/1 90/1 236 000 VAT charged 90/3 68 36 000 The cost of goods is written off 90/2 41 100 000 Bill received 62/3 62/1 236 000 The bill is included in the balance sheet 008 Payment for goods and materials received 51 62/3 236 000 Writing off a bill 008 236 000

How is bill discount calculated?

As I wrote above, a discount is a discount that allows the buyer to make a profit. Simplified, this can be represented as a formula:

face value = purchase price + discount

However, for the drawer such a formula will not be enough. After all, of these three indicators, he has only one - the amount he should receive.

Therefore, the discount size is calculated as follows. First, the second missing indicator is calculated - the denomination:

N = PC x (1 + CB x C / 365)

- where PC is the purchase price;

- SV - the period for which the paper is issued;

- C is the interest rate.

After this, we subtract the purchase price from the amount received.

For example, if you need to raise 100 thousand rubles. at 8% per annum for 300 days, the calculation will look like this.

H = 100,000 x (1 + 300 x 0.08 / 365).

As a result, we obtain a nominal value equal to 106,575 rubles. This means that the discount (difference) will be: 106,575 - 100,000 = 6,575 rubles.

How to take into account bill discount when calculating income tax

Usually, when repaying a bill, the drawer pays an amount greater than the amount of money received under this bill or the cost of goods, works or services purchased for it. In essence, this is the payment by the bill debtor for the use of money during the circulation of the bill. And often it is expressed in the form of a discount - the difference between the face value of the bill and the funds raised against the bill. Tax accounting for such a discount is not easy. Therefore, let's look at it together using the example of a simple bill of exchange, which had only one holder.

Content

Discount = income/expense on debt obligations

In tax accounting, the discount on a bill of exchange is taken into account in the same manner as income/expenses on any other debt obligation. As you remember, special rules have been established for their recognition:

- income or expense must be taken into account based on the established profitability and duration of the debt obligation;

- for debt obligations whose validity period spans more than one reporting period, income or expense must be reflected at the end of each month. When a debt obligation is repaid before the end of the reporting period, income or expense must be recognized on the date of repayment.

Accounting with the drawer

General conditions for recognizing a discount in expenses

When taking into account the discount in expenses, the drawer must remember two more conditions: the equivalent for the bill (money or goods, work, services for which it was issued) must be received and the bill must be with the bill holder. For example, if a loan is formalized by a bill of exchange and it is issued later than the receipt of money, then the drawer has no right to recognize expenses on it until he issues the bill. The same principle applies when repaying a bill. The drawer, from the moment he repaid the loan or received a bill of exchange from the holder, must stop taking into account the costs of the bill. In order to avoid disputes with the tax authorities regarding the period during which the bill of exchange is held by the holder of the bill, the date of issue of the bill of exchange and its presentation to the drawer must be recorded in the acts of acceptance and transfer of the bill of exchange.

And we must not forget that the discount is exactly the same standardized expense as interest on loans. Therefore, if the total expense on a bill exceeds the expense standard, the difference cannot be taken into account for tax purposes. Let's explain this with an example.

Example. Normalization of bill discount

CONDITION

The organization issued a promissory note in the amount of 550,000 rubles on February 21, 2011. with a payment deadline of 06/01/2011, having received 525,000 rubles for it.

Interest is taken into account in tax expenses according to the standard based on the refinancing rate increased by 1.8 times. The refinancing rate for the period from 02/21/2011 to 06/01/2011 is 7.75% (conditional).

SOLUTION

The discount period for the bill is 100 days (from 02/22/2011 to 06/01/2011).

The maximum discount that can be taken into account for tax purposes is RUB 20,065. (RUB 525,000 x 7.75% x 1.8 / 365 days x 100 days), which is less than the discount on the bill of RUB 25,000. (RUB 550,000 - RUB 525,000). This means that the drawer can take into account the discount in expenses only within the limit - 20,065 rubles.

Deciding whether we will distribute the discount by month

On the one hand, the answer follows directly from the Tax Code of the Russian Federation, which connects the inclusion of interest on debt obligations in expenses not with the actual fact of their payment, but with the end of the month. With this approach, the discount amount must be distributed over months based on the number of days in each of them and the number of days in the total circulation period of the bill.

On the other hand, regarding loans there was one Resolution of the Presidium of the Supreme Arbitration Court of the Russian Federation, in which it indicated that the borrower should take into account interest in expenses only in the period when he has an obligation to pay them. And the tax authorities, when checking, may well, referring to this Resolution, consider that the obligation to pay the discount on the part of the drawer arises only upon presentation of the bill for payment. This means that the discount can be recognized as an expense no earlier than the period of its payment.

In this case, you can show them the explanations of the Ministry of Finance and the Federal Tax Service of Russia, which insist on distributing the discount by month.

How to distribute the discount

You must assume that when paying a bill you will pay an amount equal to its face value, and the payment date will be the deadline for presenting the bill for payment. How to determine this date?

SITUATION 1. Bill of exchange with an exact date. The date of presentation of such a bill is indicated in the bill itself in the “Payment due date” detail.

SITUATION 2. Bill of exchange “at sight”. Here everything is more complicated, because it is not known exactly when the bill will be presented for payment. However, based on the fact that this should happen no later than a year from the date of drawing up the bill, it is quite convenient and logical to take its circulation period as 365 (366) days. This is what the Russian Ministry of Finance is talking about.

SITUATION 3. Bill “at sight, but not earlier.” Its accounting is fraught with the most difficulties. In this case, the drawer of the bill can only very approximately say when the bill will be presented for payment, which means it is impossible to accurately calculate the expense taken into account for taxation.

The Russian Ministry of Finance solves this problem this way: the circulation period of bills “at sight, but not earlier” should be defined as 365 (366) days plus the period from the date of drawing up the bill to the first possible date of presentation for payment - the very date “not earlier”. However, the FAS of the Ural, FAS of the North-Western and FAS of the Volga districts do not agree with this position. In their opinion, expenses on bills of exchange “upon sight, but not earlier” should be distributed over a period calculated from the date of drawing up the bill of exchange until the minimum date of its presentation for payment. After all, the possible presentation of a bill later than the “not earlier” date does not entail an increase in the drawer’s expenses.

Which option to choose is up to you. It is clear that the Ministry of Finance’s version is safer; there will be no complaints against it during verification. Well, if a bill with a payment term “at sight, but not earlier” is presented for payment before the deadline for payment, you can take into account the remaining part of the discount in non-operating expenses at a time. True, only within the limits of the standard calculated based on the actual maturity of the bill.

Accounting with the bill holder

For the bill holder, the discount is non-operating income. And it also needs to be distributed by month in the same way as the drawer does.

If the discount taken into account exceeds the discount paid

It also happens that the income or expense taken into account for tax purposes in the form of a discount exceeds the actual discount paid on the bill. For example, a bill of exchange, by agreement of the parties, is paid ahead of schedule in an amount less than the amount of the equivalent received at the time under the bill of exchange and the already accrued discount.

In the period when the bill is repaid, the drawer needs to increase non-operating income by the part of the discount taken into account in expenses but not paid. There is no need to submit updated declarations for past periods, since expenses of past periods were not overstated.

During the period of repayment of the bill, the holder of the bill must include the discount amount previously taken into account in profit into non-operating expenses. This is the opinion of the Russian Ministry of Finance.

Let's look at how to take into account the discount for early repayment of a bill using an example.

Example. Tax accounting of discount on early repayment of a bill of exchange

CONDITION

Let's use the conditions of the previous example, adding to it.

On 04/20/2011, the drawer and the holder of the bill agreed that the bill would be paid ahead of schedule - 04/30/2011 in the amount of RUB 527,000.

SOLUTION

From the moment the bill was issued until its repayment, 68 days passed (from 02/22/2011 to 04/30/2011). During this time, the drawer will take into account a discount in the amount of 13,644 rubles. (20,065 rubles / 100 days x 68 days), and the holder of the bill - in income in the amount of 17,000 rubles. (RUB 25,000 / 100 days x 68 days).

Since the bill was paid in an amount less than its face value, in April 2011 the drawer must take into account 11,644 rubles in non-operating income. (525,000 rubles + 13,644 rubles - 527,000 rubles), and the holder of the bill in non-operating expenses - 15,000 rubles. (525,000 rub. + 17,000 rub. - 527,000 rub.).

***

In conclusion, advice to bill holders - unless absolutely necessary, do not ask to repay the bill early. Tax inspectors may regard the amount of the discount you did not receive as a forgiven debt and prohibit you from taking it into account as expenses. You will most likely fight off the claims. But why unnecessary conflicts?

First published in the magazine "Glavnaya Ledger" 2011, N 6

Kononenko A.V.

Find out more about the journal "General Ledger"

Discount bill and interest bill: what are the differences?

In general, the difference between them is small. The main difference is the indication of the rate in the text of the bill. There is no such information in the discount. It is simply sold at a price below face value, ensuring that the holder receives a profit upon redemption.

There is no percentage discount. Instead, the text states the interest rate. If the date of mutual settlements is determined in advance, then the full amount to be paid is additionally indicated.