BASIC

All organizations and entrepreneurs that apply the general taxation system are VAT payers. Foreign organizations operating in Russia are also recognized as VAT payers. This follows from Article 143 and paragraph 2 of paragraph 2 of Article 11 of the Tax Code of the Russian Federation.

Foreign organizations registered with the tax office pay tax on their own. This follows from the provisions of paragraph 1 of Article 143, Article 83, paragraph 7 of Article 174 of the Tax Code of the Russian Federation. If they are not registered for tax purposes in Russia, then VAT for them is transferred by organizations acting as tax agents for:

- purchasing goods (works, services) from them (clause 2 of article 161 of the Tax Code of the Russian Federation);

- sales in Russia of their goods (works, services, property rights) on the basis of agency agreements, agency or commission agreements (clause 5 of Article 161 of the Tax Code of the Russian Federation).

VAT is charged when performing the following transactions:

- sale of goods (work, services) and property rights on the territory of Russia (in this case, the gratuitous transfer of goods, work and services is also considered a sale);

- transfer of goods on the territory of Russia (performance of work, provision of services) for one’s own needs, the costs of which are not taken into account when calculating income tax;

- performing construction and installation work for own consumption;

- import of goods.

This is stated in paragraph 1 of Article 146 of the Tax Code.

When carrying out transactions that are subject to VAT, issue an invoice (clause 5 of Article 168, subclause 1 of clause 3 of Article 169 of the Tax Code of the Russian Federation).

There is no need to charge VAT on transactions that:

- are not recognized as subject to VAT (clause 2 of Article 146 of the Tax Code of the Russian Federation);

- exempt from taxation (Article 149 of the Tax Code of the Russian Federation).

Sequence and features of accounting for additional expenses

The algorithm for distributing additional costs includes two successive stages:

- posting of materials (goods, services);

- recording of additional expenses.

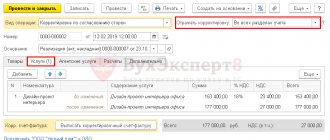

In Fig. 1 and Fig. 2 - the document “Receipt of goods, services” and postings on it. For simplicity, let’s round up the prices (timber - 5,000 rubles, lumber - 7,000) and take into account VAT “on top”.

Fig.1

Fig.2

Our video about registering a regular admission to 1C:

Compensation payments

Situation: should the contractor (performer) pay VAT on compensation for additional costs associated with the execution of the main contract? The customer reimburses the contractor (performer) for additional expenses above the price of the main contract.

Yes, I should.

VAT is imposed on transactions involving the sale of goods (work, services) on the territory of Russia (Clause 1, Article 146 of the Tax Code of the Russian Federation). At the same time, the tax base increases by all amounts associated with payment for goods, works, and services sold (subclause 2, clause 1, article 162 of the Tax Code of the Russian Federation). In this regard, compensation for additional costs (for example, travel or transportation expenses) incurred during the execution of the contract, which the customer pays to the contractor, should be included in the VAT tax base. Moreover, regardless of whether these expenses were immediately provided for in the contract (initial estimate), or the invoice for their payment was issued separately.

This point of view is reflected in letters of the Ministry of Finance of Russia dated August 15, 2012 No. 03-07-11/300 and October 14, 2009 No. 03-07-11/253.

An exception is compensation with which the customer reimburses the contractor (performer) for the cost of lost or damaged property. The Russian Ministry of Finance admits that such amounts are not related to payment for work (services) performed. Therefore, there is no need to include them in the VAT tax base (letter of the Ministry of Finance of Russia dated July 29, 2013 No. 03-07-11/30128).

An example of how compensation for additional expenses incurred by the performer (contractor) is reflected in accounting and taxation

Alpha LLC (customer) entered into an agreement with Proizvodstvennaya LLC (contractor) to carry out commissioning work on gas equipment. Contract price – 118,000 rubles. (including VAT – 18,000 rubles). In addition, the parties entered into an agreement that the customer reimburses the contractor for travel expenses in excess of the price of the main contract. The amount of travel expenses for “Master” employees involved in the execution of the contract amounted to 30,000 rubles. (including VAT - 4000 rubles (part of the expenses is not subject to VAT)).

After signing the acceptance certificate for the work performed, Alpha transferred payment in the amount of 118,000 rubles to the Master. and reimbursed travel expenses in the amount of 30,000 rubles.

When calculating VAT on compensation for travel expenses, Master’s accountant was guided by the position of the Russian Ministry of Finance.

The following entries were made in the organization's accounting:

Debit 71 Credit 50 – 30,000 rub. – money was given to the employee on account;

Debit 20 Credit 71 – 26,000 rub. (RUB 30,000 – RUB 4,000) – travel expenses are taken into account;

Debit 19 Credit 71 – 4000 rub. – VAT on travel expenses is taken into account;

Debit 68 subaccount “Calculations for VAT” Credit 19 – 4000 rub. – accepted for deduction of VAT on travel expenses;

Debit 62 Credit 90-1 – 148,000 rub. (RUB 118,000 + RUB 30,000) – revenue from the sale of work performed is reflected, taking into account compensation for travel expenses;

Debit 90-3 Credit 68 subaccount “VAT calculations” – 22,576 rubles. (RUB 148,000 × 18/118) – VAT is charged;

Debit 51 Credit 62 – 148,000 rub. – payment was received from the customer for the work performed, taking into account compensation for travel expenses.

When calculating the income tax, the Master's accountant included in the income the proceeds from the sale of work performed (taking into account compensation for travel expenses) minus VAT - 125,424 rubles. (RUB 148,000 – RUB 22,576).

Advice: there are arguments that allow contractors (performers) not to pay VAT on compensation for additional expenses that are reimbursed by the customer in excess of the contract price. They are as follows.

If additional expenses (for example, travel expenses of the contractor, expenses of the buyer for eliminating defects in the delivered goods, etc.) are not included in the cost of the main work under the contract (initial estimate) and are reimbursed by the customer separately in the amount of actual costs, then the amount of compensation cannot be qualified as proceeds from sales. The fact is that when additional expenses are reimbursed, the ownership rights to any goods, results of work performed, or services provided do not transfer to the customer (clause 1 of Article 39 of the Tax Code of the Russian Federation). Consequently, funds received by the contractor (performer) as compensation for additional expenses are not recognized as revenue and are not subject to VAT (clause 1 of Article 146 of the Tax Code of the Russian Federation). This conclusion is confirmed by arbitration practice (see, for example, the rulings of the Supreme Arbitration Court of the Russian Federation dated September 11, 2009 No. VAS-12036/09, dated June 14, 2007 No. 6950/07, resolutions of the FAS Moscow District dated February 2, 2012 No. A40 -35336/11-140-155, Ural District dated May 25, 2009 No. Ф09-3324/09-С3, Volga-Vyatka District dated February 19, 2007 No. A17-1843/5-2006, Northwestern District dated May 26, 2010 No. A66-7801/2009, dated August 25, 2008 No. A42-7064/2007 and dated August 25, 2008 No. A42-190/2008, East Siberian District dated March 10, 2006 No. A33 -20073/04-С6-Ф02-876/05-С1). However, taking into account the position of the financial department, the legality of excluding from the VAT tax base the amount of additional expenses reimbursed by the customer will have to be proven in court by the organization.

Situation: is it necessary to pay VAT on income received by a Russian sports club under a transfer contract? The contract was concluded in connection with the transfer of an athlete (professional football player) to another club.

No no need.

When a professional football player moves from one club to another, a transfer contract is concluded. It, in particular, stipulates the conditions and amount of compensation payments (transfer payments) associated with the athlete’s transfer. During the execution of this contract, the sale of goods (works, services) in the meaning defined in Article 39 of the Tax Code of the Russian Federation does not occur. Such relations cannot be considered as an operation of transfer of property rights. Consequently, compensation payments received under transfer contracts are not subject to VAT.

The legality of this approach is confirmed by the Resolution of the Presidium of the Supreme Arbitration Court of the Russian Federation dated February 27, 2007 No. 11967/06 and the letter of the Ministry of Finance of Russia dated November 22, 2010 No. 03-07-07/74, in which the financial department shares the position of the Supreme Arbitration Court of the Russian Federation.

It should be noted that previously the regulatory agencies took a different position. Representatives of the Ministry of Finance of Russia (in oral explanations) and the Department of Tax Administration of Russia for Moscow, in a letter dated November 2, 2001 No. 02-11/50841, equated compensation payments under the transfer contract to payment for services for the professional training of an athlete. That is, to revenue from the sale of services, which is subject to VAT (subclause 1, clause 1, article 146 of the Tax Code of the Russian Federation). Some courts supported this point of view (see, for example, the resolution of the Federal Antimonopoly Service of the Ural District dated August 23, 2006 No. F09-7230/06-S2). However, with the release of the Resolution of the Presidium of the Supreme Arbitration Court of the Russian Federation dated February 27, 2007 No. 11967/06 and the appearance of the letter of the Ministry of Finance of Russia dated November 22, 2010 No. 03-07-07/74, the previous explanations have lost their relevance, and arbitration practice on this issue should become uniform .

Situation: is it necessary to charge VAT on the amount of payment for a negative impact on the operation of a centralized sewerage system? The organization provides water supply and sanitation services to the population and urban organizations.

Yes need.

Payment for the negative impact on the operation of the centralized sewerage system is essentially a payment for preventive (repair) measures that neutralize the impact of pollutants on the water supply and sewerage network. Such activities are carried out by organizations that provide water supply and sanitation services. They issue invoices to subscribers for transferring fees and are the recipients of these funds. This procedure is provided for in paragraphs 118 and 119 of the Rules, approved by Decree of the Government of the Russian Federation of July 29, 2013 No. 644.

Sales of services on the territory of Russia are subject to VAT (subclause 1, clause 1, article 146 of the Tax Code of the Russian Federation). And the tax base is revenue from the sale of services, which includes all income associated with settlements for payment for these services (clause 2 of Article 153 of the Tax Code of the Russian Federation).

The list of services not subject to VAT is given in Article 149 of the Tax Code of the Russian Federation. But water supply and sanitation services are not among such operations. And the benefit provided for by paragraph 29 of paragraph 3 of Article 149 of the Tax Code of the Russian Federation applies only to intermediaries in settlements between service providers and consumers (management companies, homeowners' associations). Based on this, payments for negative impacts on the operation of the centralized sewerage system are subject to VAT on a general basis.

The tax base is the size of the fee. Determine the value of this indicator using the formulas given in paragraphs 120 and 123 of the Rules, approved by Decree of the Government of the Russian Federation of July 29, 2013 No. 644. The fee does not include VAT. Therefore, the tax should be calculated not at an estimated rate, but at a direct rate of 18 percent.

Similar clarifications are contained in the letter of the Ministry of Finance of Russia dated June 23, 2014 No. 03-07-RZ/29787.

Situation: is it necessary to charge VAT on the amount of compensation that a Russian importing organization receives from a foreign seller located abroad? The latter compensates for the cost of mandatory certification of imported goods; the certificate remains at the disposal of the Russian organization.

No no need.

Compensation for certification costs is in no way connected with payment for goods, works or services sold, therefore there is no reason to increase the VAT tax base by this amount (subclause 2, clause 1, article 162 of the Tax Code of the Russian Federation). In addition, there is no implementation of services for organizing certification, since the Russian importer receives a certificate for himself (clause 1 of Article 39 of the Tax Code of the Russian Federation). This means that the object of VAT taxation does not arise and VAT does not need to be charged (clause 1 of Article 146 of the Tax Code of the Russian Federation).

Reimbursement of additional expenses under the contract: VAT issues

13.04.2018

Reimbursement of additional expenses of the seller (performer) under a transaction is not uncommon: under a purchase and sale agreement, buyers compensate suppliers for costs associated with the conditions of transportation of goods; under a lease agreement, tenants reimburse landlords for utility costs. It happens when performers include “their” taxes in the price of the contract (for example, under a land lease agreement - the cost of paying land tax). There are plenty of similar situations (as well as errors related to the taxation of funds received). In this consultation we will pay attention to some of them.

Additional costs: part of the contract price or compensation payment

First of all, we note: if the price of the contract (whichever of them we are talking about) is formed taking into account the “covering” of additional costs of the supplier (performer), the VAT base will be the contract price

services (works). In this case, tax is not calculated on individual components of the contract price.

Relevant clarifications (with reference to clause 1 of article 154 of the Tax Code of the Russian Federation

, according to which, when selling goods (work, services), the VAT tax base is established as the cost of goods (work, services), calculated on the basis of prices determined under

Art.

105.3 of the Tax Code of the Russian Federation , and without including tax) are presented in numerous letters from the Ministry of Finance (some of them are listed in the table below).

| Details of letters from the Ministry of Finance | Topic: determining the tax base for VAT... |

| Letter dated February 16, 2018 No. 03-07-14/9856 | …when providing services for organizing recreation and health care for children |

| Letter dated March 30, 2017 No. 03-07-11/18544 | …when selling vehicles by a VAT payer who pays a recycling fee in respect of these goods |

| Letter dated 02/06/2017 No. 03-05-05-04/6115 | ... when providing services for the rental of vehicles by a taxpayer paying a fee to compensate for damage caused to public roads of federal significance by trucks weighing over 12 tons |

| Letter dated 06/06/2016 No. 03-07-11/32518 | ...in relation to transportation services provided by a taxpayer paying a fee for causing damage to highways by trucks weighing over 12 tons |

| Letter dated May 27, 2016 No. 03-07-11/30606 | ...when the buyer of self-propelled vehicles and (or) trailers compensates for the recycling fee paid by the seller |

| Letter dated August 19, 2015 No. 03-07-11/47815 | …when providing services for the transportation of goods, the price of which is determined taking into account the cost of a special permit for the right to travel on toll roads |

| Letter dated 02/01/2016 No. 03-07-08/4466 | …when providing services for the transportation of passengers and baggage by air |

| Letter dated November 11, 2015 No. 03-07-11/64840 | …when the lessor provides services, the price of which includes the cost of paying land tax |

| Letter dated 02/05/2013 No. 03-07-10/2415 | ...in relation to construction and installation works, the price of which is determined taking into account insurance payments made by the contractor in accordance with the contract |

At the same time, part of the seller’s (performer’s) expenses may additionally

be compensated (reimbursed) by the buyer (customer).

These funds are included in the VAT base on the basis of paragraphs.

2 p. 1 art. 162 Tax Code of the Russian Federation .

According to this norm, the tax base determined in accordance with Art.

153 –

158 of the Tax Code of the Russian Federation

, increases by amounts received for goods (work, services) sold in the form of financial assistance, to replenish special-purpose funds, to increase income, or otherwise related to payment for goods (work, services) sold.

Upon receipt of such amounts, the VAT amount is established by the calculation method using the rate 18/118 or 10/110 ( clause 4 of Article 164 of the Tax Code of the Russian Federation

). The table below contains explanations from officials that testify to this.

| Details of letters from the Ministry of Finance | Topic: VAT taxation... |

| Letter dated November 23, 2015 No. 03-07-11/67917 | …reimbursement of expenses for transportation of workers during a rotational work organization |

| Letter dated April 22, 2015 No. 03-07-11/22989 | …reimbursement by the customer of expenses for train tickets, hotel accommodation and meals for business travelers, if they are related to the execution of the contract and are not included in its price |

| Letters dated October 22, 2013 No. 03-07-09/44156, dated February 6, 2013 No. 03-07-11/2568 | …reimbursement of expenses by the buyer for goods transportation services |

| Letter dated August 15, 2012 No. 03-07-11/300 | …monies received by the organization supplying equipment, performing installation and commissioning work, for reimbursement of travel, transportation and insurance expenses not included in the contract price and incurred in connection with the execution of the contract |

Pros and cons of the two options

Both options, as we see, lead to the accrual of VAT on the amounts received (as part of the price or as an additional payment). Then what are the advantages of one over the other? In tax deductions! Let us explain using the example of a supply agreement, the terms of which provide for the delivery of goods to the buyer’s warehouse. For these purposes, the supplier engages a transport company, whose services (according to the contract) are paid by the buyer of the goods (reimbursing the corresponding amount to the supplier).

The carrier will issue an invoice to the supplier of the goods. However, he, in fact, is not a buyer of services, and therefore has no right to claim a tax deduction (even though he has an invoice in his name).

In such situations, it is most convenient to include the delivery of goods into the price of the goods (option 1, discussed above). Then, having purchased services from a transport company, the supplier has the right to take advantage of a tax deduction. In the invoice issued to the buyer of the goods, the supplier will write only the name of the goods, the amount of the delivery itself is not allocated. The buyer has the right to deduct VAT from the entire specified amount.

Well, if reimbursement of transportation costs is still provided in excess

the amount of the contract for the supply of goods?

As a rule, in practice, the supplier acts as follows: re-invoices the buyer for goods transportation services or includes the cost of transport services as a separate line in his (“commodity”) invoice.

But such registration, officials say, is illegal. If, according to the terms of the supply agreement, the seller of goods undertakes to organize their delivery to the consignee, and the buyer undertakes to reimburse the transportation costs incurred by the seller, in the invoice issued by the seller for shipped goods, the services for transporting goods sold by the carrier are not indicated ( letters from the Ministry of Finance of Russia dated 10/22/2013 No. 03-07-09/44156

,

dated 08/15/2012 No. 03-07-11/299

,

dated 03/21/2013 No. 03-07-09/8906

).

Indeed, in accordance with paragraph 3 of Art. 168 Tax Code of the Russian Federation

invoices are issued upon the sale of goods (works, services), and since transport services are actually provided not by the supplier of the goods, but by the carrier, re-issuance (on behalf of the supplier) of the invoice is illegal. And if the supplier (contrary to recommendations) issues an invoice in his own way (includes an additional line with transport services), the buyer should not count on a tax deduction for the costs of delivering goods on the basis of such a document.

You can avoid “troubles” by following the recommendations of officials in the indicated letters.

Example.

The contractual cost of the goods is 1,180,000 rubles, including VAT – 180,000 rubles.

The terms of the contract determine: the supplier delivers the goods to the buyer’s warehouse; The cost of delivery is compensated by the buyer of the goods in excess of the price of the delivery contract.

The supplier entered into an agreement with a transport company, according to which the cost of transporting goods is 35,400 rubles. (including VAT – 5,400 rubles).

The transport company issued an invoice in the name of the buyer of services - the supplier of the goods. The consignee in this case is the buyer of the goods.

Provider

issues an invoice for the goods to the buyer and registers the document in the sales book.

Having an invoice of a transport organization, “input” VAT on transport services (subject to the necessary conditions for this – Article 171

and

172 of the Tax Code of the Russian Federation

) the supplier has the right to accept for deduction.

The Ministry of Finance is not against such actions, which is confirmed by Letter No. 03-07-09/44156 dated October 22, 2013

. Therefore, appropriate entries must be made in the purchase ledger.

The amount of reimbursement of transportation costs (as related to payment for goods) is included (based on clause 2, clause 1, article 162 of the Tax Code of the Russian Federation

) into the VAT tax base.

The supplier will issue one invoice for this amount and register it in the sales book ( clause 18 of the Rules for maintaining the sales book

).

Sales of goods (including their delivery by the transport company) will be reflected in the amount of RUB 1,215,400. (1,180,000 + 35,400) (entry: Debit 62 Credit 90-1

).

VAT charged on sales will be 185,400 rubles. ( Debit 90-3 Credit 68

).

The amount to be deducted for “input” VAT (assuming the absence of other transactions) is RUB 5,400. ( Debit 68 Credit 19

).

Buyer

– a VAT payer (subject to the conditions

of Articles 171

and

172 of the Tax Code of the Russian Federation

) has the right to deduct the tax on the purchased goods (180,000 rubles).

Since the supplier will not issue an invoice for the amount of compensation for the costs of transporting the goods to the buyer (the document, as stated above, is issued in one copy), there are no grounds for deducting VAT ( Letter of the Ministry of Finance of Russia dated 02/06/2013 No. 03-07-11/2568

).

Arbitrage practice

Now let’s look at what disputes arise in practice and how judges resolve them.

Case No. A32-41237/2016: on the re-invoicing of fees using the Platon system to the customer of services

The parties entered into an agreement for the provision of services related to the transportation of petroleum products and gas processing products to gas stations. According to the contract, the customer is obliged to reimburse the carrier for additional costs associated with transportation conditions (tolls for toll bridges, road sections, weight control, permits, etc.), based on actual costs based on documents confirming the costs incurred.

The dispute arose due to expenses not reimbursed to the carrier under acts of reimbursement of fees to compensate for damage caused to public roads of federal significance by heavy trucks (the maximum weight of which is over 12 tons). The acts were drawn up on the basis of extracts from the Platon toll collection system. The customer did not sign the acts due to the inclusion of VAT amounts in the debt.

For your information:

in itself, the transfer of payment to compensate for damage caused by heavy trucks to federal highways is not related to the determination of the VAT base (

Letter of the Ministry of Finance of Russia dated October 6, 2015 No. 03-11-11/57133

). In other words, compensation for damage caused to roads is not the sale of goods (work, services) recognized as subject to VAT. This means that when transferring the fee, “input” VAT is not charged to the carrier.

Since the carrier did not receive the indicated amounts, he went to court. All three instances ( Decision of the Arbitration Court of the Krasnodar Territory dated February 13, 2017

,

decisions of the Fifteenth Arbitration Court of Appeal dated August 11, 2017 No. 15AP-5374/2017

and

AS SKO dated December 14, 2017

) supported the taxpayer.

The courts indicated that the amount of compensation for additional expenses of the contractor forms the price of the contract for the provision of transport services and is subject to inclusion in the VAT tax base on the basis of Art.

146 and

154 of the Tax Code of the Russian Federation

and are reimbursed by the customer including tax.

The defendant’s arguments that such expenses are not included in the contract price and are reimbursed separately

(according to the “primary” presented), therefore, the amount of compensation is not sales revenue (determined at the end of each month as the product of the amount of transported petroleum product by the amount of the agreed tariff), and also subject to VAT, were not accepted by the court of cassation.

For your information:

It is quite strange that

the Letter of the Ministry of Finance of Russia No. 03-11-11/57133

was not accepted by the judges (they say that this relates to the application of the simplified tax system).

In the cassation appeal, the taxpayer focuses on the fact that the mentioned letter does not classify the fee for the transportation of heavy cargo on federal highways and highways of constituent entities of the Russian Federation as services for the purposes of VAT for the taxpayer and the payer of the “simplified” tax. According to statements of the carrier’s transactions with RTITS LLC from November 1, 2015 to July 31, 2016, VAT was not charged on payment for compensation for damage caused to federal roads by twelve-ton trucks. These payments are not services for VAT purposes, as they are established by government authorities, and the collection of such payments cannot be classified as services subject to VAT, since there is no sign of sale established by Art.

39 Tax Code of the Russian Federation .

The courts indicated that under the contract the customer agreed to reimburse the actual costs associated with the transportation of the customer’s goods. Payment for compensation for damage to federal roads by heavy trucks is an additional expense for the carrier associated with the provision of services under the contract. This expense is taken into account by him as part of his own expenses, and income in the form of reimbursement amounts is taken into account as part of revenue.

The indicated amounts are related to payment for services provided to the customer and in accordance with paragraphs. 2 p. 1 art. 162 Tax Code of the Russian Federation

subject to inclusion in the performer’s VAT tax base.

Taking into account the terms of the contract of carriage and art. 431 Civil Code of the Russian Federation

the courts, taking into account the specific circumstances of the case, reasonably indicated that in this case, the amount of compensation for additional expenses of the contractor forms the price of the contract, is subject to inclusion in the VAT tax base on the basis of the above-mentioned norms of the Tax Code of the Russian Federation and is subject to reimbursement by the customer, including tax.

Case No. A40-161795/13: on compensation of costs when renting premises

The amounts of cost compensation received by the company from tenants and included in non-operating income (for electricity, reception and transportation of wastewater, water disposal, security, payment of property taxes) were not included in the VAT base, which was the reason for the dispute with the regulatory authorities.

The taxpayer, the lessor of the property, believing that the indicated amounts do not contain “input” VAT, therefore he had no obligation to calculate the tax, did not agree with the approach of the tax authorities and went to court.

For your information:

Apparently, the taxpayer’s reasoning was supported by

Letter of the Federal Tax Service of Russia dated 02/04/2010 No. ШС-22-3/

[email protected] , according to which (

clause 2

) in the event that the lease agreement stipulates the cost of a certain amount of leased area (that is, a constant rent), and payments for utility services (including the use of communications, as well as security, cleaning) of premises provided for rent are not recognized as an additional (variable) part of the rent and are collected by the lessor from the tenant without VAT on the basis of a separate agreement for reimbursement of the lessor's maintenance costs premises provided for rent or on the basis of a lease agreement as payments that are reimbursement of the lessor's costs for the maintenance of premises provided for rent, by virtue of

letters of the Federal Tax Service of Russia dated October 27, 2006 No. ШТ-6-03/

[email protected] and

dated April 23, 2007 No. ШТ -6-03/

[email protected] , sent in accordance with the established procedure to the tax authorities, the named payments (compensation payments) for reimbursement of the lessor's costs for the maintenance of the premises provided for rent are not taken into account by the lessor when determining the tax base and, accordingly, the invoice from the lessor to the tenant for the amount of payments (compensation payments) does not amount to.

All three instances ( Decision of the Moscow Arbitration Court dated December 11, 2014

,

Resolution of the Ninth Arbitration Court of Appeal dated 02/13/2015 No. 09AP-1554/2015

, supported by the AS MO in

Resolution dated 05/15/2015 No. F05-5185/2015

) took the side of the tax authorities, pointing out the following. Without providing non-residential premises with electricity, water, heat, and other types of utilities, tenants could not exercise the right to use the rented premises they needed to carry out their activities. Consequently, this service is inextricably linked with the provision of rental services, and the procedure for payment between the tenant and the landlord for these services does not matter.

Thus, it is not possible to actually use the leased item for its intended purpose without consuming electricity, and the tenant’s expenses for its use are a component of the rent. This conclusion corresponds to the position of the Supreme Arbitration Court, set out in Resolution No. 12664/08 dated February 25, 2009

and

Determination dated May 22, 2008 No. 4855/08

.

When the lessor provides real estate rental services, the lessor, in accordance with Part 3 of Art.

168 of the Tax Code of the Russian Federation must issue an invoice to the tenant no later than five calendar days counting from the date of provision of the service, in which, regardless of the date of payment for the variable amount of rent, the single cost of the service should be reflected (filling in the invoice or one line with the total sum, or two lines indicating separately constant and variable quantities).

So, the verdict of the judges (with references to paragraph 1, paragraph 1, article 146

,

clause 2 art.

153 and

paragraphs.

2 p. 1 art. 162 of the Tax Code of the Russian Federation ): compensation expenses of the lessor are recognized as subject to VAT.

Additionally, you can read the consultation by N. N. Lugova “We take into account the “utility” VAT under the lease agreement

.

Cases No. A40-144005/2015 and No. A40-144012/15: on compensation to the landlord for the costs of paying land tax

Let's start with the first of these. The taxpayer, the lessor of the land plots, did not include in the tax base the funds received from the lessee company on the basis of long-term land lease agreements concluded with it. These amounts (which are directly provided for in the lease agreements) are reimbursement of the lessor’s costs for paying land tax and (as related to payment for services sold) are subject to accounting in the VAT tax base (clause 2, clause 1, article 162 of the Tax Code of the Russian Federation

).

The taxpayer did not agree with the position of the controllers. In his opinion, the disputed payments are not compensation and are not included in the rent. No invoices were issued for these payments. In other words, there is no basis for charging VAT.

In addition, by not subjecting the disputed payments to VAT, the taxpayer (by analogy with utility payments) was guided by clause 2 of Letter No.

ShS-22-3/

[email protected] .

However, attempts to prove that they were right were unsuccessful: all courts ( Decision of the Moscow Arbitration Court dated November 16, 2015

,

decisions of the Ninth Arbitration Court of Appeal dated February 10, 2016 No. 09AP-60736/2015

and

AS MO dated May 5, 2016 No. F05-5070/2016

) supported the tax authorities.

Moreover, by Resolution of the Supreme Court of the Russian Federation dated August 12, 2016 No. 305-KG16-10312,

the taxpayer was denied the transfer of his cassation appeal for consideration at a court hearing of the Judicial Collegium for Economic Disputes of the Supreme Court of the Russian Federation.

This judicial act is included in the Review of legal positions reflected in judicial acts of the Constitutional Court of the Russian Federation and the Supreme Court of the Russian Federation, adopted in the second half of 2021 on taxation issues (position 9), sent for use in work by Letter of the Federal Tax Service of Russia dated December 23, 2016 No. SA-4- 7/

[email protected] .

Taking into account the presented case, a decision was made on a similar situation in case No. A40-144012/15 (the consideration of the case was completed by the second instance court). Let us quote from the Resolution of the Ninth Arbitration Court of Appeal dated September 14, 2016 No. 09AP-35703/2016

. The court of first instance came to the correct conclusion that the payment made by the tenant to the taxpayer for reimbursement of land tax is precisely an integral part of the rent; the opposite would be contrary to both the norms of civil and tax legislation. Consequently, funds received from a tenant of land plots in the form of reimbursement of additional expenses of the lessor (land tax) directly related to the provision of services for the provision of land plots for rent are subject to inclusion by the recipient of such funds in the VAT tax base. A similar position is taken by the Federal Tax Service for Moscow (Letter dated March 18, 2015 No. 16-12/ [email protected] ).

* * *

The consultation provides examples regarding the calculation of VAT when reimbursing additional expenses of the seller (performer) under various contracts (supply, transportation, rental) by the buyer (customer). Attention is drawn to the fact that, no matter how the condition for compensation of these expenses is formulated (as part of the contract price or in addition to it), these amounts are directly related to the contracts and are subject to inclusion in the VAT tax base. Moreover, regardless of the presence of “input” VAT on such expenses.

Zaitseva S. N., expert of the information and reference system “Ayudar Info”

Send to a friend

Residential maintenance

Situation: can an organization use a VAT benefit when selling maintenance services for residential premises (garbage removal, cleaning staircases, heating services, elevator maintenance, etc.)?

Only homeowners' associations (HOAs), housing cooperatives or other specialized consumer cooperatives, as well as management organizations can apply VAT benefits for the sale of maintenance services for residential premises (subclauses 29, 30, clause 3, article 149 of the Tax Code of the Russian Federation). However, this benefit can be used subject to the following conditions:

- utilities were purchased directly from resource supply organizations specified in paragraph 1 of Article 2 of Law No. 210-FZ of December 30, 2004. It should be taken into account that utility services include payments for cold and hot water supply, sewerage, electricity supply, gas supply and heating (Part 4 of Article 154 of the Housing Code of the Russian Federation);

- utilities are sold at a cost corresponding to the cost of their acquisition from the resource supplying organization (including input VAT).

In the same manner, the performance of work (provision of services) for maintenance (maintenance and repair) of common property in apartment buildings is also exempt from VAT. That is, you can take advantage of the VAT benefit if:

- works (services) were purchased from contractors (organizations and entrepreneurs) who perform (provide) them, including with the involvement of subcontractors. It should be taken into account that the maintenance of property in apartment buildings includes the work (services) listed in paragraph 11 of the Rules, approved by Decree of the Government of the Russian Federation of August 13, 2006 No. 491;

- works (services) are sold at a cost corresponding to the cost of their acquisition (including input VAT).

If homeowners' associations, cooperatives or management organizations sell work (services) performed (provided) on their own or at a price higher than the cost of their acquisition, the benefits provided for in subparagraphs 29 and 30 of paragraph 3 of Article 149 of the Tax Code of the Russian Federation do not apply.

Similar clarifications are contained in letters of the Ministry of Finance of Russia dated August 6, 2010 No. 03-07-11/345, dated April 27, 2010 No. 03-07-07/18, dated March 12, 2010 No. 03-07-14/ December 18 and December 23, 2009 No. 03-07-15/169 (the last letter was addressed to the Federal Tax Service of Russia for use in the work of tax inspectorates).

An additional condition for using the benefit is the performance of maintenance (maintenance and repair) work on common property in apartment buildings under the apartment building management agreement. The requirements for such an agreement are established by Article 162 of the Housing Code of the Russian Federation. If such work (services) are performed (provided) within the framework of an agreement that does not comply with the requirements of Article 162 of the Housing Code of the Russian Federation, the benefit provided for by subparagraph 30 of paragraph 3 of Article 149 of the Tax Code of the Russian Federation does not apply. This conclusion is confirmed by the Ministry of Finance of Russia in a letter dated August 6, 2010 No. 03-07-11/345.

VAT benefits for the sale of utility services and for the performance of maintenance (maintenance and repair) work on common property in apartment buildings are provided regardless of to whom these services (work) are provided (performed): the population or organizations (letter from the Ministry of Finance of Russia dated April 30, 2010 No. 03-07-07/21), owners or tenants (users) of premises (letter of the Federal Tax Service of Russia dated May 28, 2010 No. ShS-37-3/2791).

Arbitrage practice

Now let’s look at what disputes arise in practice and how judges resolve them.

Case No. A32-41237/2016: on the re-invoicing of fees using the Platon system to the customer of services

The parties entered into an agreement for the provision of services related to the transportation of petroleum products and gas processing products to gas stations. According to the contract, the customer is obliged to reimburse the carrier for additional costs associated with transportation conditions (tolls for toll bridges, road sections, weight control, permits, etc.), based on actual costs based on documents confirming the costs incurred.

The dispute arose due to expenses not reimbursed to the carrier under acts of reimbursement of fees to compensate for damage caused to public roads of federal significance by heavy trucks (the maximum weight of which is over 12 tons). The acts were drawn up on the basis of extracts from the Platon toll collection system. The customer did not sign the acts due to the inclusion of VAT amounts in the debt.

For your information: the transfer of payment in itself to compensate for damage caused by heavy trucks to federal highways is not related to the determination of the VAT base (Letter of the Ministry of Finance of Russia dated October 6, 2015 No. 03-11-11/57133). In other words, compensation for damage caused to roads is not the sale of goods (work, services) recognized as subject to VAT. This means that when transferring the fee, “input” VAT is not charged to the carrier.

Since the carrier did not receive the indicated amounts, he went to court. All three instances (Decision of the Arbitration Court of the Krasnodar Territory dated 02/13/2017, decisions of the Fifteenth Arbitration Court of Appeal dated 08/11/2017 No. 15AP-5374/2017 and AS SKO dated 12/14/2017) supported the taxpayer. The courts indicated that the amount of compensation for additional expenses of the contractor forms the price of the contract for the provision of transport services and is subject to inclusion in the VAT tax base on the basis of Art. 146 and 154 of the Tax Code of the Russian Federation and are reimbursed by the customer including tax.

The defendant’s arguments that such expenses are not included in the cost of the contract and are reimbursed separately (according to the “primary” presented), therefore, the amount of compensation is not sales revenue (determined at the end of each month as the product of the amount of petroleum product transported by the amount of the agreed tariff), and also subject to VAT, were not accepted by the court of cassation.

For your information: it is quite strange that the Letter of the Ministry of Finance of Russia No. 03-11-11/57133 was not accepted by the judges (they say that this relates to the application of the simplified tax system). In the cassation appeal, the taxpayer focuses on the fact that the mentioned letter does not classify the fee for the transportation of heavy cargo on federal highways and highways of constituent entities of the Russian Federation as services for the purposes of VAT for the taxpayer and the payer of the “simplified” tax. According to statements of the carrier’s transactions with RTITS LLC from November 1, 2015 to July 31, 2016, VAT was not charged on payment for compensation for damage caused to federal roads by twelve-ton trucks. These payments are not services for VAT purposes, as they are established by government authorities, and the collection of such payments cannot be classified as services subject to VAT, since there is no sign of sale established by Art. 39 Tax Code of the Russian Federation.

The courts indicated that under the contract the customer agreed to reimburse the actual costs associated with the transportation of the customer’s goods. Payment for compensation for damage to federal roads by heavy trucks is an additional expense for the carrier associated with the provision of services under the contract. This expense is taken into account by him as part of his own expenses, and income in the form of reimbursement amounts is taken into account as part of revenue.

The indicated amounts are related to payment for services provided to the customer and in accordance with paragraphs. 2 p. 1 art. 162 of the Tax Code of the Russian Federation are subject to inclusion in the performer’s VAT tax base.

Taking into account the terms of the contract of carriage and Art. 431 of the Civil Code of the Russian Federation, the courts, taking into account the specific circumstances of the case, reasonably indicated that in this case, the amount of compensation for additional expenses of the contractor forms the price of the contract, are subject to inclusion in the VAT tax base on the basis of the above-mentioned norms of the Tax Code of the Russian Federation and are subject to reimbursement by the customer including the tax.

Case No. A40-161795/13: on compensation of costs when renting premises

The amounts of cost compensation received by the company from tenants and included in non-operating income (for electricity, reception and transportation of wastewater, water disposal, security, payment of property taxes) were not included in the VAT base, which was the reason for the dispute with the regulatory authorities.

The taxpayer, the lessor of the property, believing that the indicated amounts do not contain “input” VAT, therefore he had no obligation to calculate the tax, did not agree with the approach of the tax authorities and went to court.

For your information: apparently, the taxpayer’s reasoning was supported by Letter of the Federal Tax Service of Russia dated 02/04/2010 No. ШС-22-3 / [email protected] , according to which (clause 2) in the event that the lease agreement stipulates the cost of a certain amount of leased area ( that is, a constant rent), and payments for utility services (including the use of communications, as well as security, cleaning) of premises provided for rent are not recognized as an additional (variable) part of the rent and are collected by the lessor from the tenant without VAT on the basis of a separate agreement for reimbursement of costs the lessor for the maintenance of the premises provided for rent or on the basis of a lease agreement as payments that are reimbursement of the costs of the lessor for the maintenance of the premises provided for lease, by virtue of letters of the Federal Tax Service of Russia dated October 27, 2006 No. ШТ-6-03/ [email protected] and dated April 23. 2007 No. ШТ-6-03/ [email protected] , sent in accordance with the established procedure to the tax authorities, the named payments (compensation payments) for reimbursement of the lessor's costs for the maintenance of the premises provided for rent are not taken into account by the lessor when determining the tax base and, accordingly, the invoice The landlord does not make payments (compensation payments) to the tenant for the amount.

All three instances (Decision of the Moscow Arbitration Court dated December 11, 2014, Resolution of the Ninth Arbitration Court of Appeal dated February 13, 2015 No. 09AP-1554/2015, supported by the AS MO in Resolution dated May 15, 2015 No. F05-5185/2015) took the side of the tax authorities , pointing out the following. Without providing non-residential premises with electricity, water, heat, and other types of utilities, tenants could not exercise the right to use the rented premises they needed to carry out their activities. Consequently, this service is inextricably linked with the provision of rental services, and the procedure for payment between the tenant and the landlord for these services does not matter.

Thus, it is not possible to actually use the leased item for its intended purpose without consuming electricity, and the tenant’s expenses for its use are a component of the rent. This conclusion corresponds to the position of the Supreme Arbitration Court, set out in the Resolution No. 12664/08 dated 02.25.2009 and the Determination No. 4855/08 dated 05.22.2008. When the lessor provides real estate rental services, the lessor, in accordance with Part 3 of Art. 168 of the Tax Code of the Russian Federation must issue an invoice to the tenant no later than five calendar days counting from the date of provision of the service, in which, regardless of the date of payment for the variable amount of rent, the single cost of the service should be reflected (filling in the invoice or one line with the total sum, or two lines indicating separately constant and variable quantities).

So, the verdict of the judges (with references to paragraph 1, paragraph 1, Article 146, paragraph 2, Article 153 and paragraph 2, paragraph 1, Article 162 of the Tax Code of the Russian Federation): the landlord’s compensation expenses are recognized as subject to VAT. Additionally, you can read the consultation by N. N. Lugova “We take into account the “utility” VAT under the lease agreement.”

Cases No. A40-144005/2015 and No. A40-144012/15: on compensation to the landlord for the costs of paying land tax

Let's start with the first of these. The taxpayer, the lessor of the land plots, did not include in the tax base the funds received from the lessee company on the basis of long-term land lease agreements concluded with it. These amounts (which are directly provided for in the lease agreements) are reimbursement of the lessor’s expenses for paying land tax and (as related to payment for services sold) are subject to accounting in the VAT tax base (clause 2, clause 1, article 162 of the Tax Code of the Russian Federation).

The taxpayer did not agree with the position of the controllers. In his opinion, the disputed payments are not compensation and are not included in the rent. No invoices were issued for these payments. In other words, there is no basis for charging VAT.

In addition, by not imposing VAT on the disputed payments, the taxpayer (by analogy with utility payments) was guided by clause 2 of Letter No. ShS-22-3 of the Federal Tax Service of Russia / [email protected]

However, attempts to prove their case were unsuccessful: all courts (Decision of the Moscow Arbitration Court dated November 16, 2015, decisions of the Ninth Arbitration Court of Appeal dated February 10, 2016 No. 09AP-60736/2015 and AS MO dated May 5, 2016 No. F05-5070 /2016) supported the tax authorities. Moreover, by Resolution of the Supreme Court of the Russian Federation dated August 12, 2016 No. 305-KG16-10312, the taxpayer was denied the transfer of his cassation appeal for consideration at a court hearing of the Judicial Collegium for Economic Disputes of the Supreme Court of the Russian Federation. This judicial act is included in the Review of legal positions reflected in judicial acts of the Constitutional Court of the Russian Federation and the Supreme Court of the Russian Federation, adopted in the second half of 2016 on taxation issues (position 9), sent for use in work by Letter of the Federal Tax Service of Russia dated December 23, 2016 No. SA-4- 7/ [email protected]

Taking into account the presented case, a decision was made on a similar situation in case No. A40-144012/15 (the consideration of the case was completed by the second instance court). Let us quote from the Resolution of the Ninth Arbitration Court of Appeal dated September 14, 2016 No. 09AP-35703/2016. The court of first instance came to the correct conclusion that the payment made by the tenant to the taxpayer for reimbursement of land tax is precisely an integral part of the rent; the opposite would be contrary to both the norms of civil and tax legislation. Consequently, funds received from a tenant of land plots in the form of reimbursement of additional expenses of the lessor (land tax) directly related to the provision of services for the provision of land plots for rent are subject to inclusion by the recipient of such funds in the VAT tax base. A similar position is taken by the Federal Tax Service for Moscow (Letter dated March 18, 2015 No. 16-12/ [email protected] ).

* * *

The consultation provides examples regarding the calculation of VAT when reimbursing additional expenses of the seller (performer) under various contracts (supply, transportation, rental) by the buyer (customer). Attention is drawn to the fact that, no matter how the condition for compensation of these expenses is formulated (as part of the contract price or in addition to it), these amounts are directly related to the contracts and are subject to inclusion in the VAT tax base. Moreover, regardless of the presence of “input” VAT on such expenses.

Educational services

Situation: can an organization use VAT benefits when providing services in the field of education (conducting lectures, seminars, etc.) if, based on the results of training, it does not conduct certification and does not issue educational documents?

Only non-profit organizations can use VAT benefits when providing services in the field of education (subclause 14, clause 2, article 149 of the Tax Code of the Russian Federation). Therefore, if educational services are provided by a commercial organization, it is obliged to charge VAT on their entire cost.

Non-profit organizations are exempt from taxation when selling educational services within the framework specified in the licenses:

- general education programs;

- professional (main and (or) additional) educational programs;

- vocational training programs or educational process.

A complete list of services for the implementation of educational programs is given in the appendix to the regulations on licensing of educational activities, approved by Decree of the Government of the Russian Federation of October 28, 2013 No. 966.

In addition, VAT is not assessed on the sale of additional educational services that, in terms of level and focus, correspond to the programs specified in the license.

If an organization licensed for educational activities, as part of this activity, conducts one-time classes in the form of lectures, seminars, internships, then these additional educational services are also not subject to VAT.

Similar clarifications are contained in the letter of the Ministry of Finance of Russia dated April 28, 2012 No. 03-07-07/47.

Services related to the sale of precious metals

Situation: can an organization use VAT benefits when providing services related to the sale of precious metals to the Bank of Russia (sorting, weighing, packaging, storage)?

No, he can not.

In accordance with subparagraph 9 of paragraph 3 of Article 149 of the Tax Code of the Russian Federation, it is the sale of precious metals on the interbank market that is exempt from VAT. At the same time, tax legislation means the transfer of ownership of property from one person to another on a compensated and gratuitous basis (clause 1 of Article 39 of the Tax Code of the Russian Federation). The benefits provided for in subparagraph 9 of paragraph 3 of Article 149 of the Tax Code of the Russian Federation do not apply to services for sorting, weighing, packaging and storage of precious metals.

Compensation for legal costs

Disputes involving citizens that are not related to their business activities are subject to the jurisdiction of courts of general jurisdiction (clause 1, clause 1, article 22 of the Code of Civil Procedure of the Russian Federation). In this case, the party in whose favor the court decision was made, the court awards compensation to the other party for all legal expenses incurred by the “winner” in the case (clause 1 of Article 98 of the Code of Civil Procedure of the Russian Federation).

Note. In the event of a labor dispute, the employee is exempt from paying legal costs, including state fees (Article 393 of the Labor Code of the Russian Federation).

Note. What do legal costs consist of? Legal costs consist of state fees and costs associated with the consideration of the case (clause 1 of Article 88 of the Code of Civil Procedure of the Russian Federation). The costs associated with the consideration of the case include (Article 94 of the Code of Civil Procedure of the Russian Federation), in particular: - travel and accommodation expenses of the party incurred in connection with the appearance in court; — payment for representatives’ services; — postal costs associated with the consideration of the case.

Sale of medical property

Situation: is it necessary to pay VAT on the sale of products intended for internal prosthetics?

Yes need.

In accordance with the All-Russian Classification of Products, products intended for internal prosthetics have code 93 9818 and are included in subgroup 93 9800 “Other medical materials and devices.” This means that these products do not belong to prosthetic and orthopedic products (code 93 9600 according to the All-Russian Product Classifier), the sale of which is exempt from VAT on the basis of subparagraph 1 of paragraph 2 of Article 149 of the Tax Code of the Russian Federation.

Thus, when selling products intended for internal prosthetics, the organization cannot take advantage of the VAT benefit provided for in subparagraph 1 of paragraph 2 of Article 149 of the Tax Code of the Russian Federation. Therefore, when selling them, pay VAT, and apply a rate of 10 percent (clause 1 of Article 146, subclause 4 of clause 2 of Article 164 of the Tax Code of the Russian Federation).

Situation: is it necessary to pay VAT when selling an ambulance?

Yes need.

The list of the most important and vital medical equipment, the sale of which is not subject to VAT, was approved by Decree of the Government of the Russian Federation of September 30, 2015 No. 1042. In accordance with it, preferential equipment includes means for movement and transportation, which are included in the group of products with the code according to the All-Russian Product Classifier 94 5100. An ambulance does not belong to this group, since it is assigned code 45 1485. Therefore, when selling it, pay VAT in the general manner (subclause 1, clause 1, article 146 of the Tax Code of the Russian Federation). A similar point of view is reflected in the letter of the Ministry of Finance of Russia dated June 2, 2008 No. 03-07-07/65.

An example of VAT calculation on the sale of an ambulance

Alpha LLC is a commercial medical center. In 2013, the organization purchased an ambulance. The initial cost of the car, both according to accounting and tax records, was 350,000 rubles. The car was used in the main activity of the organization - providing paid medical services to the population. When selling medical services, the organization used the benefit in the form of exemption from VAT, provided for in subparagraph 2 of paragraph 2 of Article 149 of the Tax Code of the Russian Federation. Therefore, the VAT paid to the supplier was taken into account in the original cost of the car. The vehicle was not revalued.

In February 2015, Alpha sold the car. The selling price of the car was 200,600 rubles. (including VAT – RUB 30,600). At the time of sale, the amount of depreciation accrued on the car in both accounting and tax accounting amounted to 161,200 rubles. Thus, the residual value of the car at the time of sale was 188,800 rubles. (RUB 350,000 – RUB 161,200). In the same month, the buyer transferred money for the car to the organization.

Since the initial cost of the car included the amount of “input” VAT, when it was sold, a special procedure was established for calculating the tax base. Its accountant calculated it as the difference between the sales price (including VAT) and its residual value (clause 3 of Article 154 of the Tax Code of the Russian Federation). Thus, when selling a car, the accountant charged VAT in the amount of: (200,600 rubles – 188,800 rubles) × 18/118 = 1,800 rubles.

Alpha's accountant reflected the sale of the car as follows:

Debit 76 Credit 91-1 – 200,600 rubles. – revenue from the sale of a car is reflected;

Debit 01 subaccount “Disposal of fixed assets” Credit 01 – RUB 350,000. – the original cost of the car has been written off;

Debit 02 Credit 01 subaccount “Disposal of fixed assets” – 161,200 rubles. – the amount of accrued depreciation is written off;

Debit 91-2 Credit 01 subaccount “Disposal of fixed assets” – 188,800 rubles. – the residual value of the car is written off;

Debit 91-2 Credit 68 subaccount “VAT calculations” – 1800 rubles. – VAT payable to the budget has been accrued;

Debit 51 Credit 76 – 200,600 rub. – money received from the buyer.

Situation: is it necessary to pay VAT when leasing medical equipment, the sale of which is exempt from VAT?

Yes need.

Subparagraph 1 of paragraph 2 of Article 149 of the Tax Code of the Russian Federation provides that the sale of medical equipment that is listed in the List approved by Decree of the Government of the Russian Federation of September 30, 2015 No. 1042 is exempt from VAT. Thus, this benefit applies only to operations for its sale . Therefore, when leasing medical equipment, pay VAT in the general order (clause 1, article 39, subclause 1, clause 1, article 146 of the Tax Code of the Russian Federation).

VAT from the performer

If, under the terms of the contract for the provision of paid services, the customer organization, in addition to paying the cost of the services provided by the contractor, reimburses the costs of travel, accommodation of the contractor’s employees, etc., then when deciding on the inclusion of the amount of compensation received from the customer in reimbursement of expenses, the tax base for VAT the following options are possible <*>.

Safe option Compensation by the customer for the contractor's expenses incurred in the provision of services is associated with payment for these services and increases the VAT tax base. Moreover, regardless of the fact that, under the terms of the contract, reimbursable expenses may be indicated separately from the cost of services provided. The amount of VAT is calculated at the calculated rate of 18/118 in the tax period in which funds were actually received to reimburse expenses (clause 2 of Article 153, clause 2 of clause 1 of Article 162, clause 4 of Article 164 of the Tax Code of the Russian Federation, Letters of the Ministry of Finance of Russia dated March 2, 2010 N 03-07-11/37, dated November 9, 2009 N 03-07-11/288). For the amount of VAT accrued on the compensation received, the contractor issues an invoice in one copy and registers it in the sales book (clauses 3, 18 of the Rules for maintaining the sales book used in calculations of value added tax, approved by the Decree of the Government of the Russian Federation dated 12/26/2011 N 1137). At the same time, the contractor does not have any tax consequences in relation to the “input” VAT, which was previously legally accepted for deduction when accepting expenses for accounting (clauses 2, 7, Article 171 of the Tax Code of the Russian Federation).

The amount of compensation by the customer for the contractor's expenses is not included in the VAT tax base. This conclusion can be drawn from Letter of the Ministry of Finance of Russia dated February 22, 2018 N 03-07-09/11443. As for the “input” VAT in the part attributable to the costs incurred by the contractor, we note the following. In general, the right to deduct VAT arises after the registration of goods (work, services) acquired for the implementation of transactions recognized as objects of taxation (clause 1, clause 2, article 171, clause 1, article 172 of the Tax Code of the Russian Federation). Since the contractor does not take into account the reimbursed expenses and does not include the amount of compensation received in the VAT tax base, the contractor does not have the right to deduct “input” VAT (if it is presented by counterparties).

<*> When, under the terms of the contract, the contractor’s costs are not allocated as a separate amount in the contract price, the tax base for VAT is determined based on the contract price (clause 1, clause 1, article 146, clause 1, article 154 of the Tax Code of the Russian Federation, Resolution of the FAS Western- Siberian District dated March 12, 2009 N F04-1010/2009 (961-A27-31), F04-1010/2009 (962-A27-31) in case N A27-5996/2008-6). In this case, no later than five calendar days from the date of provision of services (signing of the acceptance certificate for services provided), the corresponding invoice should be issued to the customer (clauses 1, 3 of Article 168 of the Tax Code of the Russian Federation). Income tax for the contractor upon reimbursement of his expenses under a contract for the provision of paid services

With regard to accounting for profit tax purposes the amount to be received from the customer in reimbursement of expenses incurred by the contractor in fulfilling obligations under the contract, the following options may be available.

Risky option The amount to be received from the customer in reimbursement of expenses is recognized as revenue from the provision of services (clause 1 of Article 248, clause 1 of Article 249 of the Tax Code of the Russian Federation). At the same time, the performing organization takes into account for profit tax purposes expenses incurred on the basis of a contract for the provision of paid services and compensated by the customer, subject to their compliance with the requirements of Art. 252 of the Tax Code of the Russian Federation (Letter of the Federal Tax Service of Russia for Moscow dated December 19, 2007 N 20-12/121656). A similar conclusion can be drawn from Letters of the Ministry of Finance of Russia dated November 30, 2015 N 03-11-06/2/69446, dated August 15, 2012 N 03-11-06/2/109. Despite the fact that these Letters concern organizations that apply the simplified tax system, the conclusion made in them, in our opinion, is applicable in this case to organizations that pay income tax. The Contractor does not include in income for profit tax purposes the amount of reimbursement of its costs to be received from the customer in accordance with the terms of the contract for the provision of paid services. This is due to the fact that when receiving compensation, the contractor does not receive any economic benefit (clause 1 of Article 41 of the Tax Code of the Russian Federation). Accordingly, expenses incurred by the contractor during the provision of services and reimbursed by the customer are not taken into account by the contractor for tax purposes.

Rationale: Accounting for the contractor when reimbursement of his expenses under a contract for the provision of paid services

The procedure for reflecting in accounting transactions related to the reimbursement of costs incurred by the contractor depends on how the contractor classifies the amount to be received from the customer. If the contractor considers this compensation as a compensation payment, then the costs incurred by the contractor and fully reimbursed by the customer under the terms of the contract for paid services are not recognized as expenses and are included in settlements with the customer (clause 2 of PBU 10/99). In this case, an entry is made to the debit of account 62 “Settlements with buyers and customers” and the credit of account 71 “Settlements with accountable persons” (60 “Settlements with suppliers and contractors”, etc.) (Instructions for using the Chart of Accounts). When receiving funds from the customer to reimburse expenses, the customer’s receivables are repaid in accounting, but no income is generated (clause 2 of PBU 9/99). If the amount of compensation for costs incurred by the contractor is taken into account in accounting as part of the revenue from the provision of services, then the amount to be reimbursed is reflected as an entry on the credit of account 90 “Sales”, subaccount 90-1 “Revenue”, in correspondence with the debit of account 62 (clause clause 5, 12 PBU 9/99, Instructions for using the Chart of Accounts). Revenue is recognized in accounting when the conditions listed in clause 12 of PBU 9/99 are met. That is, the amount to be reimbursed is included in income from ordinary activities on the date the customer approves the contractor’s report on expenses actually incurred and paid. The contractor's costs under the contract are included in expenses for ordinary activities. In this case, an entry is made in the debit of account 20 “Main production” in correspondence with the credit of account 71 (60, etc.). These expenses are written off to the debit of account 90, subaccount 90-2 “Cost of sales”, on the date of recognition of the amount of compensation as part of revenue from the provision of services (clauses 5, 9, 19 of PBU 10/99). The accounting method chosen by the executing organization in the situation under consideration must be enshrined in its accounting policy (clause 7.1 of PBU 1/2008). The table uses the following designation of the analytical account for account 68: 68-VAT “Calculations for VAT”.

Sale of property of a liquidated organization

Situation: is it necessary to pay VAT when transferring the property of a liquidated organization to the founders?

Yes, it is necessary if the value of the transferred property exceeds the amount of the founder’s initial contribution to the authorized capital of the liquidated organization.

The transfer of property of a liquidated organization to its founders within the limits of their initial contribution is not recognized as a sale and is not subject to VAT (subclause 5, clause 3, article 39, clause 2, article 146 of the Tax Code of the Russian Federation). If the value of the transferred property exceeds the amount of the down payment, then this operation is recognized as a sale and is subject to VAT (subclause 5, clause 3, article 39, subclause 1, clause 1, article 146 of the Tax Code of the Russian Federation). On the amount of excess of the market value of the transferred property over the amount of the initial contribution, the liquidated organization must charge a tax at a rate of 18 percent and issue an invoice to the founder (clause 2 of Article 154, clause 3 of Article 164, clause 1 of Article 168, subclause 1 clause 3 article 169 of the Tax Code of the Russian Federation).

Similar clarifications are contained in the letter of the Ministry of Finance of Russia dated April 17, 2012 No. 03-07-11/112. In arbitration practice there are examples of court decisions confirming the legality of this approach (see, for example, the resolution of the FAS of the North Caucasus District dated January 23, 2006 No. F08-6609/2005-2602A).

It should be noted that when transferring securities or funds to the founders, the liquidated organization should not charge VAT. Such transactions are not subject to taxation. This follows from the provisions of subparagraph 12 of paragraph 2 of Article 149, subparagraph 1 of paragraph 3 of Article 39 of the Tax Code of the Russian Federation and letter of the Ministry of Finance of Russia dated January 20, 2005 No. 03-05-02-04/6.

VAT and re-invoiced amounts of state duties

The situation with payment of state duty when registering a contract for temporary use on a reimbursable basis (rent) looks even more interesting. In this situation, the landlord most often presents the expenses incurred by him to compensate the tenant. What happens to VAT in this situation?

The facts presented in the previous paragraph of the article can be used as a basis for analysis. The provision of services is recognized as subject to VAT on the basis of clause 1 of Art. 146 of the Tax Code of the Russian Federation. When previously incurred expenses are rebilled to the purchaser of services, no amounts appear for inclusion in the tax base, and therefore VAT is not required to be charged. Such cases also do not require drawing up invoices.

***

As you can see, the interpretation of the application of VAT in relation to reimbursable expenses is quite ambiguous. Each specialist in the company’s financial service will have to decide independently which approach to follow. Although most of the explanations provided are advisory in nature, it is possible that if they are not applied in practice, you will not have to defend your views in court. Before finalizing all contractual relations, it is necessary to clearly assess possible future risks from following one or another point of view. In this case, the presence of court decisions in favor of the taxpayer should inspire some optimism. Although this is not a guarantee of a similar position of a particular judge in a seemingly similar case, and in any case there is no need to rush to make a decision.

Similar articles

- Accounting for transport costs

- The organization operates without VAT - features of mutual settlements

- The procedure for calculating and paying VAT when switching from the simplified tax system to the OSNO

- Adjustment invoice VAT declaration

- Accounting entries for VAT - examples

Carrying out post-warranty repairs

Situation: is it necessary to pay VAT when selling post-warranty repair services?

Yes need.

Services provided on the territory of Russia without charging additional fees for the repair and maintenance of goods during the warranty period of their operation are not subject to VAT (subclause 13, clause 2, article 149 of the Tax Code of the Russian Federation). For services related to post-warranty repairs, the Tax Code of the Russian Federation does not provide for VAT exemption.

Therefore, when selling them, you pay VAT in the general manner at a rate of 18 percent (clause 3 of Article 164 of the Tax Code of the Russian Federation).

Reimbursement of expenses to the contractor under a civil contract

Norms of the Civil Code . In paragraph 2 of Art. 709 of the Civil Code directly states that the price of work in a work contract includes:

- compensation of contractor costs;

- the remuneration due to him.

Note. Compensation (from the Latin compencatio - to balance) implies repayment of actual costs incurred.

This approach also applies to the provision of services (Article 783 of the Civil Code of the Russian Federation). From the above formulation one could conclude that income is the difference between the contract price and the amount of costs of the contractor (performer).

Norms of the Tax Code . Tax legislation did not follow the path proposed by the Civil Code.

For the term “compensation” in the sense in which it is used in civil legal relations, there are no “norms established in accordance with the legislation of the Russian Federation,” that is, size restrictions. Therefore, the contractor’s expenses in tax legislation are subject to the benefits of clause 3 of Art. 217 of the Tax Code are not subject to. A special rule has been introduced to regulate the taxation of income of individuals - contractors.

The Tax Code deals with professional deductions, to which, in particular, taxpayers who receive income under civil contracts for the performance of work (rendering services) are entitled to receive them (clause 2, part 1, article 221 of the Tax Code of the Russian Federation). These deductions are practically compensation.

Professional deductions are provided by the tax agent in the amount of expenses actually incurred by the taxpayer and documented expenses directly related to the performance of work or provision of services (clause 2, part 1, article 221 of the Tax Code of the Russian Federation).

Proceeds from participants in shared construction

Situation: is it necessary to pay VAT to the developer on amounts received from participants in the shared construction of a residential building? The residential building has not been put into operation.

Yes, it is necessary, but only from a portion of the funds received from participants in the shared construction of a residential building to pay for construction work performed by the developer himself.

Under an agreement for participation in shared construction, the developer undertakes to build a property and, after receiving permission to put it into operation, transfer it to the participants in shared construction. In turn, each participant must pay the amount stipulated by the contract and, upon completion of construction, accept their part of the facility.

The developer can carry out construction on its own and (or) by contractors.

This is stated in Part 1 of Article 4 of the Law of December 30, 2004 No. 214-FZ.

The contract amount may include:

- the cost of the developer’s services (regardless of the method of construction);

- the cost of construction work, namely, reimbursement of the developer’s costs for attracting contractors (when construction is carried out by contractors) and (or) the cost of work performed directly by the developer (when construction is carried out on its own).

This follows from the provisions of Part 1 of Article 5 of the Law of December 30, 2004 No. 214-FZ.