Home / Taxes / What is VAT and when does it increase to 20 percent? / Book of purchases and sales

Back

Published: November 20, 2018

Reading time: 4 min

0

550

The purpose of maintaining a purchase ledger is to determine the amount of VAT that is subject to deduction. In it, buyers must register invoices issued by sellers, received on paper and electronic media.

- Transaction type code in the purchase book

- How to reflect the advance refund

- Filling out the declaration

It contains primary invoices, as well as adjustment and corrected invoices.

Transaction codes in the VAT return

In some sections of the VAT return there are columns called “Operation code”. These are sections such as:

- section 2 – to be filled out by tax agents;

- sections 4-6 - filled out by organizations and individual entrepreneurs who had export operations;

- section 7 - filled out by organizations and individual entrepreneurs for transactions that are not subject to taxation (exempt from taxation), transactions that are not recognized as an object of taxation, transactions for the sale of goods (work, services), the place of sale of which is not recognized as the territory of the Russian Federation, as well as for payment amounts, partial payment on account of upcoming deliveries of goods (performance of work, provision of services), the duration of the production cycle of which is more than 6 months.

As you can see, with certain codes, the declaration reflects not ordinary transactions for the sale of goods on the territory of the Russian Federation, but “special” VAT transactions.

All VAT transaction codes are given in Appendix No. 1 to the Procedure for filling out the declaration (approved by Order of the Federal Tax Service dated October 29, 2014 No. ММВ-7-3/558).

View codes for VAT returns with explanations

If you do not fill in the necessary codes in the declaration, the declaration will not pass format-logical control and will not be accepted by the tax authority.

Read also

05.10.2016

Fill in column 3

The next column, which is difficult to fill out, is column 3 “Number and date of the seller’s invoice.” The rules establish that when reflecting in the purchase book the amount of VAT paid when importing goods into the territory of the Russian Federation, column 3 indicates the number of the customs declaration for goods imported into the territory of the Russian Federation. When importing into the territory of the Russian Federation from the territory of a member state of the Customs Union of goods in respect of which VAT is collected by tax authorities in accordance with the Agreement on the principles of collection of indirect taxes for the export and import of goods, performance of work, provision of services in the Customs Union of January 25, 2008 . and the Protocol on the procedure for collecting indirect taxes and the mechanism for monitoring their payment when exporting and importing goods in the Customs Union of December 11, 2009, in column 3 of the purchase book the number and date of the application for the import of goods and payment of indirect taxes with marks from the tax authorities are indicated on payment of value added tax.

Note. The Agreement and Protocol mentioned in the Rules became invalid as of 01/01/2015 (that is, from the date of entry into force of the Treaty on the Eurasian Economic Union of 05/29/2014).

Despite the fact that this norm contains references to documents that have become invalid, it continues to apply: organizations importing goods from EAEU member countries must reflect in column 3 the number and date of the application for the import of goods and the payment of indirect taxes with marks from the tax authorities on the payment of VAT .

Where do you get these details from? In clause 8.1.3 of the Methodological Recommendations for maintaining the information resource “EAEU-Exchange” (Approved by Order of the Federal Tax Service of Russia dated 04/08/2015 N ММВ-7-15 / [email protected] ) it is stated that the registration number is assigned to the application automatically and cannot be edited . The structure of the registration number is a 16-digit digital code consisting of a sequence of numbers.

From left to right, the code states the following:

- code of the tax authority that assigned the registration number (NNNN);

- date of registration of the application (DDMMYYYY);

- serial number of the registration record during the day (XXXX).

Thus, column 3 reflects the registration number of the application corresponding to this structure. It is not necessary to indicate the date of filling out the application, since the 16-digit code already contains the date of registration of the application (similar explanations are given in the Letter of the Federal Tax Service of Russia dated March 21, 2016 N ED-4-15 / [email protected] ).

For reference. A taxpayer who is an importer of goods from member states of the EAEU, along with a tax return, submits an application for the import of goods and payment of indirect taxes on paper (in four copies) and in electronic form or in electronic form, certified by an electronic digital signature. When submitting an application in electronic form, certified by an electronic digital signature, the taxpayer does not need to contact the tax authority for a tax payment stamp, since this is done automatically (Letter of the Federal Tax Service of Russia dated July 1, 2015 N ZN-4-17 / [email protected] ) .

Consultation

Dzhaarbekov Stanislav, tax expert, lawyer. Website: Taxd.ru

Advance payment

Advance payment (advance payment) is payment by the buyer (customer) for goods (work, services) before their delivery (fulfillment).

The buyer has the right to deduct VAT from the advance payment issued.

It should be noted that the buyer has the right to deduct VAT on advances issued. But you don't have to do this. Thus, the Ministry of Finance of the Russian Federation in its letters informs that the buyer has the right not to deduct such VAT (Letter of the Ministry of Finance of the Russian Federation dated May 20, 2016 N 03-07-08/28995, Letter of the Ministry of Finance of the Russian Federation dated November 22, 2011 N 03-07-11 /321). If you decide not to deduct VAT, then simply do not register the invoice received from the seller for the advance payment in the purchase book. Subsequently, upon receipt of the goods (works, services) for which an advance was issued, you will not need to restore VAT, since you did not deduct it.

VAT deduction on advances issued is regulated by:

clause 12 art. 171 Tax Code of the Russian Federation:

“Deductions from the taxpayer who transferred the amounts of payment, partial payment for upcoming deliveries of goods (performance of work, provision of services), transfer of property rights, are subject to tax amounts presented by the seller of these goods (work, services), property rights.”

clause 9 art. 172 of the Tax Code of the Russian Federation:

“Deductions of the tax amounts specified in paragraph 12 of Article 171 of this Code are made on the basis of invoices issued by sellers upon receipt of payment, partial payment for upcoming deliveries of goods (performance of work, provision of services), transfer of property rights, documents confirming the actual transfer of payment amounts, partial payment for upcoming deliveries of goods (performance of work, provision of services), transfer of property rights, if there is an agreement providing for the transfer of these amounts.”

To confirm the deduction of VAT on the advance payment issued, the buyer must have:

— Invoice (advance) from the seller;

— Agreement providing for the transfer of an advance;

- Payment documents.

Recovering VAT on an advance payment

Advance VAT is temporary. It is accepted as a deduction for the period before the acquisition of goods (works, services), and then restored.

The rules for recovering VAT on issued accounts are specified in paragraphs. 3 p. 3 art. 170 Tax Code of the Russian Federation.

“The restoration of tax amounts is carried out by the buyer in the tax period in which the tax amounts on purchased goods (works, services), property rights are subject to deduction in the manner established by this Code, or in the tax period in which there was a change in conditions or termination of the relevant agreement and return of the corresponding amounts of payment, partial payment received by the taxpayer on account of the upcoming supply of goods (performance of work, provision of services), transfer of property rights.

Amounts of tax accepted for deduction in relation to payment, partial payment for future deliveries of goods (performance of work, provision of services), transfer of property rights, are subject to restoration in the amount of tax accepted by the taxpayer for deduction on goods purchased by him (work performed, services rendered) , transferred property rights, in payment of which the amount of previously transferred payment, partial payment in accordance with the terms of the agreement (if such conditions exist) are subject to offset;”

That is, VAT should be restored in the tax period (quarter) when:

— accepted for deduction of VAT on goods (works, services) for which the advance was transferred;

— the seller returned the advance due to termination or modification of the contract;

According to the Ministry of Finance of the Russian Federation, VAT on the advance payment should be restored even if the seller’s receivables are written off as a bad debt, if the seller never fulfilled the obligation to supply the goods (Letter of the Ministry of Finance dated August 17, 2015 N 03-07-11/47347).

Example

The buyer issued an advance payment in the amount of 1000 rubles to pay for the goods, which are subject to VAT at a general tax rate of 18%1.

The buyer received an advance invoice from the seller, which indicated the amount of VAT of 152.54 rubles (1000 * 18/118). The buyer has the right to deduct this VAT.

Invoice

No later than 5 calendar days from the date of receipt of the advance payment, the seller must draw up an advance invoice in two copies (Articles 168, 169 of the Tax Code of the Russian Federation).

The seller must transfer one copy of the invoice to the buyer (clause 3 of Article 168 of the Tax Code of the Russian Federation).

The invoice issued when receiving advances has its own characteristics and is called an Advance invoice.

Reflection in the purchase book

VAT accepted for deduction on an advance invoice is reflected in the Purchase Book with the VAT transaction type code - 02 “Payment, partial payment (received or transferred) on account of upcoming supplies of goods (work, services), property rights, including transactions carried out on based on commission agreements, agency agreements providing for the sale and (or) acquisition of goods (work, services), property rights on behalf of the commission agent (agent) or on the basis of transport expedition agreements, with the exception of transactions listed under codes 06; 28".

Reflection in the sales book

1) If the buyer received goods (accepted work or services) on account of the advance payment:

VAT restored in connection with the purchase of goods (work, services) is reflected in the Sales Book with the VAT transaction type code - 21 “Operations for the restoration of tax amounts specified in paragraph 8 of Article 145, paragraph 3 of Article 170 (except for subparagraphs 1 and 4 of paragraph 3 of Article 170), Article 171.1 of the Tax Code of the Russian Federation, as well as when performing transactions taxed at a tax rate of 0 percent for value added tax"

2) If the contract is terminated and the seller returns the advance:

VAT restored in connection with the termination or change of the contract and the return of the advance is reflected in the Sales Book with the VAT transaction type code - 22 “Operations for the return of advance payments in the cases listed in paragraph two of paragraph 5 of Article 171, as well as the operations listed in paragraph 6 Article 172 of the Tax Code of the Russian Federation"

Reflection in the VAT return

The amount of VAT on the advance payment accepted for deduction is reflected on line 130 “13. The amount of tax presented to the taxpayer - the buyer when transferring the amount of payment, partial payment on account of upcoming deliveries of goods (performance of work, provision of services), transfer of property rights, subject to deduction from the buyer" Section 3 of the VAT return for that tax period (quarter), in which the advance was issued.

The amounts of restored VAT are reflected in line 090 “6.1. tax amounts subject to restoration in accordance with subparagraph 3 of paragraph 3 of Article 170 of the Tax Code of the Russian Federation" section 3 of the VAT return for the tax period (quarter) in which the goods were received on account of the advance payment issued or when the advance was returned.

Reflection of advance VAT from the buyer in accounting

An advance was issued for the delivery of goods:

D 60 - K 51 - advance payment issued

D 68 - K 60-advance - VAT on the advance is accepted for deduction

Items received from seller:

D 41 - K 60 - Goods received

D 19 - K 60 - VAT on purchased goods (works, services) is reflected

D 68 - K 19 - VAT on purchased goods (works, services) is accepted for deduction

D 60-advance - K 68 - Restored VAT on advance

Example

The buyer and seller entered into a purchase and sale agreement for goods in the amount of 23,600 rubles (including VAT of 3,600 rubles at a rate of 18%). According to the contract, the buyer makes an advance payment in the amount of 11,800 rubles and after delivery of the goods the final payment is made.

20.02 The buyer paid the seller an advance in the amount of 11,800 rubles to pay for the goods (including VAT of 1,800 rubles).

The buyer deducts VAT in the amount of 1,800 rubles (based on the advance invoice received from the seller).

Buyer's accounting:

D 60 K 51 11 800 advance payment transferred

D 19 K 60 1,800 VAT calculated on advance payment

D 68 K 19 1,800 VAT accepted for deduction

10.03 The seller transfers the goods to the buyer in the amount of 23,600 rubles (including VAT 3,600 rubles).

The buyer calculates (restores) the VAT previously accepted for deduction on the advance payment (1,800 rubles) and accepts for deduction the VAT on the goods received (3,600 rubles).

Buyer's accounting:

D 41 K 60 20 000 goods registered

D 60 K 68 1,800 VAT previously accepted for deduction on the advance payment was restored

D 19 K 60 3,600 VAT in the cost of goods

D 68 K 19 3,600 VAT accepted for deduction

12.03 The buyer transfers 11,800 rubles to the seller.

The buyer does not take this amount into account either in the tax base or as a deduction.

Buyer's accounting:

D 60 K 51 11 800 payment for goods

Notes

1) from 2021 the basic VAT rate is 20% (until 2021 - 18%). The estimated VAT rate from 2021 is 20/120 (until 2021 - 18/118).

To consolidate the material, consider example 2:

| The organization Fortura LLC (TIN/KPP 7816*****/780101001), under a contract for the supply of goods, received from Nadezhda LLC (TIN/KPP 7743******/997850001) an advance payment for upcoming deliveries of goods. Fortuna LLC issues invoice No. A100010331 dated June 17, 2021 to Nadezhda LLC for a total amount of 291,000.00 rubles, incl. VAT – 44,389.83 rubles, and is registered in the sales book with code “02”. LLC "Nadezhda" received from LLC "Fortuna" invoice No. A100010331 dated June 17, 2021 for an advance in the total amount of 291,000.00 rubles, incl. VAT – 44,389.83 rubles, reflected in the purchase book with code “02” (clause 12 of article 171, clause 9 of article 172 of the Code). After shipment of goods to Nadezhda LLC, Nadezhda LLC issues an invoice for sales No. 10331 dated July 20, 2021 for a total amount of 177,000.00 rubles, incl. VAT – 27,000.00 rubles, and is registered in the sales book with code “01”. In the purchase book, Fortuna LLC registers previously issued invoice No. A100010331 dated June 17, 2021 to Nadezhda LLC for advance payment in the amount of 291,000.00 rubles, incl. VAT – 27,000.0 rubles with code “22”. After receiving and registering the goods, Nadezhda LLC registers invoice No. 10331 dated July 20, 2021 in the purchase book for a total amount of 177,000.00 rubles, incl. VAT – 27,000.0 rubles with code “01”, and restores the amount of VAT previously accepted for deduction on the basis of an advance invoice, registering in the sales book invoice No. A100010331 dated 06/17/2021 for a total amount of 291,000.00 rubles , incl. VAT – 27,000.00 rubles with code “21”. |

| N p/p | Operation type code | Seller's invoice number and date | Seller's name | Seller's INN/KPP | Cost of purchases according to the invoice, difference in cost according to the adjustment invoice (including VAT) in the invoice currency | The amount of VAT on the invoice, the difference in the amount of VAT on the adjustment invoice, accepted for deduction, in rubles and kopecks | |

| 1 | 2 | 3 | 9 | 10 | 15 | 16 | |

| 1 | 22 | No. A100010331 dated 06/17/2021 | Fortuna LLC | 7816*****/780101001 | 291 000,00 | 27 000,00 | |

Transaction code 22 in the purchase ledger

Organizations and individual entrepreneurs carrying out their financial and economic activities with the calculation of value added tax “VAT” and submitting tax reports on it are required to use the appropriate transaction codes and reflect these codes in registers, as well as in VAT returns.

Codes of types of transactions for tax accounting registers were approved by order of the Federal Tax Service dated March 14, 2016 No. ММВ-7-3/ [email protected] Their list is periodically updated with the introduction of new codes. To reflect codes in documents, special columns are provided: No. 2 in the sales/purchase books, No. 3 in the invoice journals. In 2021, the cipher registry has changed slightly, some of the codes used have been canceled, others have been added, and others have been detailed.

Correct indication of codes when documenting transactions is very important, since information from registers is transferred to the declaration and analyzed by tax authorities. The code details the type of operation and characterizes the algorithm for issuing an invoice and calculating VAT. For example, when deducting VAT on a transaction confirmed by documents, code 23 is indicated. When checking, the software resource of the Federal Tax Service recognizes that invoices are not registered using this code. An error in specifying the code will indicate a discrepancy, and the Federal Tax Service will request an explanation. True, the law does not provide for the imposition of penalties for such inaccuracies.

The transaction type code is used when entering an invoice into the purchase/sales ledger. The list of codes was approved by order of the Federal Tax Service of Russia dated March 14, 2016 No. ММВ-7-3/136. This list is amended by law as necessary.

| Each individual code marks a specific operation or series of operations. From the table above we see that code “01” is used when purchasing or selling goods (work; it is applied to the operation of full or partial payment for deliveries in future periods, including under agency agreements, etc. The use of code “22” in the purchase book occurs in two groups of transactions. |

Returning goods to the supplier in 1C: Accounting

Published 01/18/2020 22:06 Author: Administrator Since 2021, the procedure for returning goods has been significantly simplified. According to the innovations, the buyer no longer formalizes this operation as a reverse sale and does not issue an invoice. All the buyer needs to do is issue an invoice or a return certificate from the island. In this way, the return of both defective and high-quality goods is processed, regardless of the date of purchase.

In accordance with the recommendations of the Federal Tax Service (letter dated October 23, 2018 No. SD-4-3 / [email protected] ), upon receipt of the returned goods, the seller issues an adjustment invoice, which the buyer should reflect in the sales book. That is, the restoration of VAT previously accepted for deduction on returned goods is carried out on the basis of an adjustment invoice received from the seller.

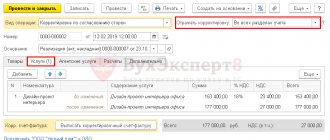

Let's look at a practical example in 1C: Enterprise Accounting, processing the return to the supplier of goods purchased and registered in 2021.

This operation will be reflected in the document “Return of goods to the supplier”.

In the “Receipt Document” line, you must select the document that reflected the receipt of goods to be returned.

Particular attention must be paid to the VAT rate. From 2021, the VAT rate is 20%. But if the goods were purchased before 2021, then the VAT rate in the document “Return of goods to the supplier” is indicated as 18%, that is, the VAT rate when returning goods will be the same as when purchasing.

In our example, the purchase of goods was made in 2021, which means the VAT rate for returning goods will be 20%.

In the printed form of the consignment note (form TORG-12), the line “Base” requires special attention of the buyer. Here, in addition to o, you must manually enter the details of the supply agreement, delivery notes and other documents that are directly related to this business transaction.

Upon receipt of an adjustment invoice from the supplier, the buyer registers it in the same “Return of goods to supplier” document that was used to issue the return of goods and the return invoice.

Please note that the document generates transactions using account 76.02 “Calculations for claims”.

The return of goods to the supplier is reflected in the sales book with transaction type code 18.

In the VAT return, the refund to the supplier is reflected on line 080 of Section 3.

Author of the article: Marina Alenina

Did you like the article? Subscribe to the newsletter for new materials

Add a comment

Comments

0 Irina 02/29/2020 00:29 I quote PAWS:

Hello! How is the return of goods reflected by the seller?

Hello.

There is an article on the site about this. Return of goods from the buyer in 1C: Accounting. Quote 0 Sergey 02/09/2020 12:39 Quote Irina:

I quote Anna: Don’t be misled. Adjustment only based on a claim for a defective product. If you decide to return a quality product after the transfer of ownership, then this is a reverse sale if the seller agreed to take it back.

You are misleading.

What if the product was purchased in 2021 at a rate of 18%, and then sold back in 2021 at a rate of 20%? And at whose expense is the difference? )) Read the new legislation! Since last year, there is no concept of reverse implementation. Well, you decide what business transaction you want to reflect: return of goods or sell this product to the buyer (reverse sale)? The article talks specifically about returns, so the rate is 18%. Quote 0 PAWS 02/01/2020 02:54 Hello! How is the return of goods reflected by the seller?

Quote

0 Irina 01/27/2020 09:12 I quote Alena Mikhailovna Vostrilova:

Good afternoon Is the scheme the same if sales and returns occur in different quarters?

Same Quote

0 Irina 01/27/2020 09:11 Quote Anna:

Don't be misled. Adjustment only based on a claim for a defective product. If you decide to return a quality product after the transfer of ownership, then this is a reverse sale if the seller agreed to take it back.

You are misleading.

What if the product was purchased in 2021 at a rate of 18%, and then sold back in 2021 at a rate of 20%? And at whose expense is the difference? )) Read the new legislation! Since last year, there is no concept of reverse implementation. Quote 0 Anna 01/26/2020 14:34 Don’t be misleading. Adjustment only based on a claim for a defective product. If you decide to return a quality product after the transfer of ownership, then this is a reverse sale if the seller agreed to take it back.

Quote

0 Irina 01/20/2020 16:39

Quote

0 Alena Mikhailovna Vostrilova 01/20/2020 14:27 Good afternoon! Is the scheme the same if sales and returns occur in different quarters?

Quote

Update list of comments

JComments