Why do we need a nomenclature of cases and how is it related to the storage periods of documents?

Let us analyze the storage periods for documents according to the nomenclature of cases using a practical example.

A graduate of the Financial Academy, Maria went to work at Virazh LLC, which is engaged in the renovation and construction of offices. Since the former student had no experience in financial matters, the management decided to assign her to the office for the duration of the probationary period - this way they could quickly become familiar with the structure of the company and study the specifics of its activities. This division consisted of 5 employees who dealt with various organizational issues, including responsibility for organizing the company’s document flow.

The department employee to whom Maria was assigned was developing a list of cases for the next year.

IMPORTANT! The list of cases for the next year is drawn up in the last quarter of the current year, approved by the head and put into effect on January 1 (clause 3.4.6 of the Rules for the operation of company archives dated 02/06/2002).

Maria was also involved in this work - she was tasked with setting storage periods for documents according to the nomenclature of cases opposite the names of case headings strictly according to the standard list.

IMPORTANT! The storage periods for documents are reflected in standard and departmental lists. From 02/18/2020, the basis for determining the deadlines is the List of standard documents and their storage periods, approved by order of the Federal Archive of Russia dated 12/20/2019 No. 236. The previously valid order of the Ministry of Culture dated 08/25/2010 No. 558 was cancelled.

Regulatory documents regulating storage periods

The responsibilities of HR department employees, in addition to recording the personnel of the organization and office work, include ensuring the safety of personnel documentation. The retention periods for personnel documents are approved by law and are periodically reviewed.

| Important! In 2021, with the adoption of Order No. 236 (valid from February 18, 2020), a new list of standard documentation with updated storage periods came into force. |

The lists according to which the storage periods for archival documentation, personnel documents, etc. are determined are listed in Part 3 of Art. 6 and part 1 and 1.1 of article 23 N 125-FZ. These are the following standards:

- List of standard management archival documents. Put into effect by Order of the Federal Archive of December 20, 2021 N 236 (until 02/18/2020, the list of the Ministry of Culture of the Russian Federation dated 08/25/2010 N 558 was in effect);

- Instructions for use of the List - Order dated December 20, 2019 N 237;

- Methodological recommendations: how to organize the accounting and storage of personnel documents, developed by VNIIDAD;

- The list of standard archival documents that are formed in the scientific, technical and production activities of companies is Order of the Ministry of Culture of the Russian Federation dated July 31, 2007 N 1182.

When determining how long personnel documents are stored for the eighties and the first half of the nineties of the 20th century. and for the industry nomenclature, the Standard List approved by the Main Archive of the USSR on August 15, 1988 was used.

Structure of the company's business portfolio

The list of cases of Virage LLC was formed based on the organizational structure of the company. The following departments took part in the document flow process:

- organizational issues division (office);

- personnel department;

- Department of Labor and Wages;

- Department of Economic Planning, Statistics and Finance;

- accounting and reporting department;

- Department of Tax Accounting and Declaration;

- labor protection department;

- production and technical department (PTO);

- other divisions.

Before putting storage periods next to those indicated in the nomenclature, Maria studied in detail the structure of the company and understood the functional purpose of each structural unit. Then she began to thoroughly understand the List approved by Order No. 236. Maria reflected information about the storage periods of certain documents in column 4 of the nomenclature. She started with the office and especially carefully studied the document flow of the department in which she was currently working.

Rules and terms for storing documents

The rules for storing documents are enshrined at the state level in the Rules for organizing the storage, acquisition, recording and use of documents of the Archive Fund of the Russian Federation and other archival documents in government bodies, local governments and organizations, approved by order of the Ministry of Culture of the Russian Federation dated March 31, 2015 No. 526.

Based on storage periods, documents can be divided into 3 groups:

- permanent storage,

- temporary storage over 10 years,

- temporary storage up to 10 years.

Refer to standard lists for storage periods for documents. The main one used in any organization is the List of standard management documents generated in the activities of state organizations, local governments and organizations, indicating their storage periods, approved by Order of the Ministry of Culture of Russia dated August 25, 2010 No. 558.

In order to organize the storage of a large volume of documents, organizations create an archive - an independent structural unit that ensures the safety of documents with long storage periods. At the same time, cases that have a storage period of more than 10 years are transferred to the archive no earlier than one year and no later than 3 years after their completion. Documents with a temporary storage period of up to 10 years are not transferred to the archive and are stored in the structural units in which they were created.

If an organization does not have the opportunity to store documents at its location, then it can enter into a depository storage agreement with specialized organizations that will independently monitor the safety of documents and destroy them in a timely manner.

Formed and completed files, before they are transferred to the organization’s archive, are stored in structural units that must ensure the safety of documents and protection from the negative effects of light and dust.

Office documents: how long will they have to be stored?

The nomenclature of the office contained a list of a wide variety of files, the storage periods of which were strikingly different from each other. For example, a retention period of only 1 year applies to internal labor regulations (after replacement with new ones), and the collective agreement is required to be kept permanently.

The nomenclature of the office affairs was as follows (abbreviated):

| Case index | Case title | Number of storage units | Shelf life and article numbers according to the list | Note |

| 1 | 2 | 3 | 4 | 5 |

| 01. Office | ||||

| 01-01 | Charter of Virage LLC | Constantly Art. 28 | ||

| 01-02 | Collective agreement of Virage LLC | Constantly Art. 386 | Sent for information - until the need has passed | |

| 01-03 | Internal labor regulations of Virage LLC | 1 year Art. 381 | After replacing with new ones | |

| 01-04 | Orders of the director of Virage LLC on core activities | Constantly Art. 19 | ||

| 01-05 | Orders of the director of Virage LLC on administrative and economic activities | 5 years Art. 19 | ||

| 01-06 | Minutes of meetings with the manager | Constantly Art. 18 "e" | Minutes of operational meetings - 5 years | |

| 01-07 | Nomenclature of cases | Constantly Art. 157 | Structural divisions - 3 years | |

| — | — | — | — | — |

| Reserve | ||||

| Reserve | ||||

While filling out column 4 of the nomenclature, Maria drew attention to the last 2 lines in column 2 “Case title”. As it turned out, it is customary to leave several reserve lines in the nomenclature of any division of the company in case headings of cases appear that were not previously provided for in the nomenclature. Retention periods in these lines will be entered only after the reserve lines are filled with the names of cases - while Maria left them empty.

After entering the storage periods for documents reflected in the office nomenclature, Maria began documenting the personnel department.

CONSTANTLY – HOW MUCH IS THIS?

The storage periods for documents are established by standard lists:

- A list of standard management archival documents generated in the course of the activities of state bodies, local governments and organizations, indicating storage periods (approved by Order of the Ministry of Culture of Russia dated 08/25/2010 No. 558, as amended on 02/16/2016; hereinafter referred to as the 2010 List);

- A list of standard archival documents generated in the scientific, technical and production activities of organizations, indicating storage periods (approved by Order of the Ministry of Culture of Russia dated July 31, 2007 No. 1182, as amended on April 28, 2011; hereinafter referred to as the 2007 List).

The document storage period can also be established in industry regulations. In this case, the word “permanently” can be replaced by a synonym, for example, “indefinitely”.

- If the organization is not the source of acquisition of the state archive.

Column 3 “Document storage period” of the 2010 List contains a footnote <*>, which states that the “permanent” (Permanent) storage period of documents in organizations that are not sources of acquisition of state and municipal archives cannot be less than ten years. We are talking only about those documents whose storage periods are indicated in the 2010 List.

Thus, if an organization is not the source of acquisition of the state (municipal) archive, it must store documents with a “permanent” period of at least 10 years, and then is free to destroy them as usual, along with files that have expired by that time. At the same time, it is advisable to establish a minimum storage period for these documents in the instructions for office work or in other local regulations on the storage of documents. For example:

Since the Company is not an organization that is a source of acquisition of state (municipal) archives, the “permanent” storage period for management documents is 10 years.

note

The 2007 List does not contain any such footnotes or instructions issued in any other way. Therefore, if a document according to the 2007 List has a “permanent” shelf life, this means storage for the entire existence of the organization.

- If the organization is the source of acquisition of the state archive, then the storage period “permanently” means “the entire existence of the organization.” If the liquidated organization has a successor, then “permanently” will last as long as the successor organization exists. If an organization is liquidated without successors, the state archive to which it belongs conducts an examination of the value of documents with a permanent shelf life and takes into its storage those that it considers useful. Documents that are not of interest to the archive may be destroyed.

We determine the storage periods for HR department documentation

HR documentation is distinguished by one nuance: many files are subject to storage for 50/75 years. Such a long storage period is provided for documents related to personal information about company employees.

Maria also filled out the personnel nomenclature with retention periods, which are presented in the table (abbreviated):

| Case index | Case title | Number of storage units | Shelf life and article numbers according to the list | Note |

| 1 | 2 | 3 | 4 | 5 |

| 02. Personnel | ||||

| 02-01 | Staffing table | Constantly Art. 40 | ||

| 02-02 | Personal files of employees | 50 years - if the documents were completed after 01/01/2003; 75 years - if documents were completed before 01/01/2003. Art. 445 | ||

| 02-05 | Vacation schedules | 3 years Art. 453 | ||

| 02-06 | Lists of persons subject to military registration | 5 years Art. 457 | ||

| 02-07 | Lists of retired employees | 5 years Art. 462 "w" | ||

| 02-08 | Documents (memos, reports, certificates, characteristics) on bringing to justice violators of labor discipline | 3 years Art. 434 "d" | ||

| 02-09 | Journal of registration of employment contracts | 50 years - if the documents were completed after 01/01/2003; 75 years - if documents were completed before 01/01/2003. Art. 463 "b" | ||

| — | — | — | — | — |

| Reserve | ||||

| Reserve | ||||

Maria studied individual documents from the nomenclature in particular detail. She was interested in questions related to what regulatory requirements they should meet and how they should be filled out correctly.

Maria found answers to her questions on our website.

For example:

- You can learn about the type and content of the staffing table from the material “Unified Form No. T-3 - Staffing Schedule (form)” ;

- the timing of approval of the vacation schedule and punishment for its absence is discussed in the article “Unified Form No. T-7 - Vacation Schedule” .

Retention periods for personnel documentation

So, the following are stored for 5 years:

- Documents (certificates, information, statements, etc.) relating to the availability, recruitment or movement of workers.

- Documents (lists, information, certificates) relating to the release or need for workforce, creation of jobs, gender, age, professional qualifications of employees.

- Correspondence regarding employment issues.

- Documents on the transfer of employees to a shortened working day or week.

- Documents related to labor disputes.

- Reports regarding the status and verification of work with employees are stored on an ongoing basis, and applications (certificates) for release and needs of employees are also stored for five years.

The following are stored for 3 years:

- Documents (information, working time balances, information, memos) relating to the recording of working time.

- Acts (information, characteristics, messages, certificates, etc.) that contain information about labor discipline.

- Acts (reports and other information) relating to the accounting of labor inserts and books.

Retention for a period of one year applies to timesheets and time logs, as well as vacation schedules.

An employee’s personal file and personal card are stored for 75 years, and if we are talking about this documentation for managers, employees with state awards or titles, members of the executive, management or control structures of the organization, then permanently.

The organization's staffing table and changes to them are stored on a permanent basis, and staffing arrangements are stored for 75 years.

A standard job description at the place of approval and development is stored permanently, a personal one (as part of personal files) - for 75 years.

The copy of the employment contract remaining with the employer, filed in the employee’s personal file, must be kept for 75 years, and then handed over to the archives. If personal files are not maintained, then such agreements should be formed into a separate file under the same storage conditions.

Account cards, books, magazines also have their own deadlines for storing documents in office work:

- Hiring, relocating, dismissing employees - 75 years.

- Accounting for business travelers - 5 years from the date of dismissal.

- Registration of persons liable for military service - 3 years.

- Information about vacations - 3 years.

- Personal files, cards, employment contracts and agreements - 75 years.

- Issuance of work inserts and books - 50 years.

- Issuance of salary certificates (place or work experience) - 3 years.

- issuance of travel certificates - 5 years.

Summarizing all of the above, for the convenience of people who need information in collected form, they can independently present the storage periods for documents in office work in a table.

Papers of the “salary” department and their storage periods

The retention period for documentation related to the calculation and payment of wages in most cases does not exceed a 5-year period, with the exception of certain documents that cannot be destroyed for 50/75 years (for example, employee personal accounts). And local acts, on the basis of which settlements with personnel are carried out, are subject to permanent storage.

The nomenclature and storage periods for this type of document are presented in the table (abbreviated):

| Case index | Case title | Number of storage units | Shelf life and article numbers according to the list | Note |

| 1 | 2 | 3 | 4 | 5 |

| 03. Labor and wages | ||||

| 03-01 | Regulations on remuneration and bonuses | Permanently or 5 years after replacement with new ones Art. 294 "a" | ||

| 03-02 | Personal accounts for employee wages | 50 years - if the documents were completed after 01/01/2003; 75 years - if documents were completed before 01/01/2003. Art. 296 | ||

| 03-03 | Applications for financial assistance | 5 years Art. 298 | ||

| 03-04 | Payroll statements for the payment of wages to employees of Virage LLC | 6 years Art. 295 | In the absence of personal accounts: 50 years - if the documents were completed after 01/01/2003; 75 years - if documents were completed before 01/01/2003. | |

| 03-05 | Employees' sick leave certificates | 5 years Art. 618 | ||

| 03-06 | Writs of execution for employees of Virage LLC | 5 years after execution Art. 299 | ||

| — | — | — | — | — |

| Reserve | ||||

| Reserve | ||||

The names of the cases of this division of the company were familiar to Maria - during her internship, she assisted the payroll accountant and carried out individual calculations herself. But this is the first time I’ve heard about the storage periods for these statements, certificates and registers.

You can find out more about the form and procedure for filling out documentation related to salary calculations on our website. For example:

- A sample of filling out a pay slip for a company employee is available for viewing in the material “Unified Form No. T-51 - Pay Slip” ;

- You can find out more details about preparing a payroll slip from the material .

Periods for storing documents in the archive

Keeping in mind the above points, we come to the most fundamental issue - determining the storage period for documents , including establishing a “permanent” storage period. In some cases, storage periods for certain categories of documents are established by the laws of the Russian Federation, decrees of the President of the Russian Federation, decrees and orders of the Government of the Russian Federation.

The storage periods for specific types of documents established by these regulatory documents are mandatory for use by all other bodies and organizations and must be reflected in their regulatory acts developed by them (lists of documents, approximate and specific nomenclatures of cases).

Lists of standard archival documents created by federal archival authorities in the Russian Federation also use these storage periods without changes. In this case, the issue of changing the storage periods for these types of documents can only be resolved as a result of a complex procedure for submitting proposals to change the storage periods to the highest legislative body or the highest executive body and making a decision to amend the relevant legal act.

In a number of cases, the retention periods for files of certain categories of documents are established by the federal government and management body by its normative act (order, resolution, decree). As a rule, these types of documents reflect the performance of a specific function inherent in a given industry or line of activity and have a temporary storage period.

In addition, it should be borne in mind that, based on the provisions of the current archival legislation, only the archival management body has the right to classify documents as part of the Archival Fund of the Russian Federation, and for specific documents - the archival management bodies of the constituent entities of the Russian Federation and federal state archives. Moreover, if these documents are standard, their storage periods should not contradict the periods specified in the standard list .

If these are new types of documents , then their storage periods must be agreed upon with the Federal Archives Management Authority. Unfortunately, this condition is not always met, which leads to discrepancies in determining the storage periods for documents and negative consequences, including judicial intervention. This happens when a federal industry governing body sets a shorter retention period for certain types of documents, which is reflected in the list of standard documents, and the question arises about the legality of destroyed documents .

Sometimes federal executive authorities, when developing their departmental lists, try to change, more often than not, the retention periods for certain categories of documents, not considering them standard, but inherent only to the system of their bodies and institutions.

As evidence, they argue that these archival documents are not part of the Archival Fund of the Russian Federation and, therefore, are not subject to transfer to state and municipal archives, their storage periods are not established by the highest legislative body or the highest governing body (the Government of the Russian Federation), but a departmental list only agreed (not approved) with the federal executive body in the field of archival affairs.

Periods during which tax documents cannot be disposed of

Studying the headings of the nomenclature files for the tax accounting and declaration department, Maria made the following conclusion for herself: this type of documentation refers to short-term storage papers. Almost all files of this department, including tax reporting and declarations, were subject to storage for 5 years:

| Case index | Case title | Number of storage units | Shelf life and article numbers according to the list | Note |

| 1 | 2 | 3 | 4 | 5 |

| 04. Tax accounting and declaration | ||||

| 04-01 | Tax accounting policy of Virage LLC | 5 years after replacement with new ones Art. 267 | ||

| 04-02 | Certificates of registration with the tax authority | until the need passes Art. 24 | ||

| 04-03 | Correspondence regarding tax disagreements | 5 years Art. 314 | ||

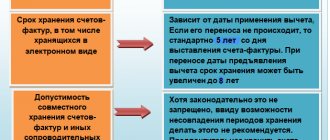

| 04-04 | Invoices | 5 years (before 02/18/2020 it was 4 years) Art. 317 | ||

| 04-05 | Documents (calculation of tax amounts, messages about the impossibility of withholding tax, tax accounting registers) on personal income tax | 5 years Art. 311 | In the absence of personal accounts: 50 years - if the documents were completed after 01/01/2003; 75 years old - if documents were completed before 01/01/2003 | |

| 04-06 | Declarations (calculations) for all types of taxes | 5 years Art. 310 | ||

| 04-07 | Calculations for insurance premiums (annual and quarterly) | 50 / 75 years Art. 308 | ||

| 04-08 | Cards for individual accounting of the amounts of accrued payments and other remunerations and the amounts of accrued insurance premiums | 6 years Art. 309 | In the absence of personal accounts: 50 years - if the documents were completed after 01/01/2003; 75 years old - if documents were completed before 01/01/2003 | |

| 04-09 | Registers for calculating land tax of Virage LLC | 5 years Art. 307 | ||

| 04-09 | Certificates of fulfillment of the obligation to pay taxes, fees, insurance premiums, penalties and tax sanctions, certificate of the status of settlements with the budget | 5 years Art. 305 | ||

| 04-10 | Certificates of income and tax amounts for individuals | 5 years Art. 312 | In the absence of personal accounts: 50 years - if the documents were completed after 01/01/2003; 75 years old - if documents were completed before 01/01/2003 | |

| — | — | — | — | — |

| Reserve | ||||

| Reserve | ||||

Maria was familiar with tax documentation only theoretically. Therefore, to expand her knowledge, she used the materials on our website, from where she learned not only about all types of invoices (regular, corrected and adjustment), but also became acquainted with the rules for preparing tax returns and other similar documents.

You can learn more about filling out an amended invoice from the material “In what cases is an amended invoice used?” .

A practical example of filling out an adjustment invoice is contained in the article “Sample of filling out an adjustment invoice (2019 - 2020)” .

“What is the procedure for filling out a VAT return (example, instructions, rules)” will help you fill out the VAT return correctly .

Administrative responsibility

For non-compliance with the rules for the formation and content of documentation, administrative and civil liability is provided. Depending on the seriousness of the violation, the penalty: warning, fine or disqualification. This issue is regulated by Articles 13.20, 13.25, 19.5, 19.6, 19.7 of the Code of Administrative Offenses of the Russian Federation.

Legal documents

- “Basic rules for the work of archives of organizations”, approved by the decision of the board of Rosarkhiv dated 02/06/2002

- Federal Law of October 22, 2004 No. 125-FZ (as amended on December 28, 2017) “On archiving in the Russian Federation”

- “Basic rules for the work of archives of organizations” (approved by the decision of the board of Rosarkhiv dated 02/06/2002)

- Order of the Ministry of Culture of Russia dated March 31, 2015 No. 526

- Federal Law of June 18, 2017 No. 127-FZ

- 13.20

- 13.25

- 19.5

- 19.6

- 19.7 Code of Administrative Offenses of the Russian Federation

Nuances of storage periods for some tax documents

From the knowledge she acquired at the academy, Maria remembered that the loss received by the company can be carried forward to future periods, reducing the volume of the tax base by its amount (or part of it). But in this case, how to store documentation related to confirmation of the amount of loss and the procedure for transferring to subsequent periods? Is it possible to get rid of the calculations and declarations justifying the loss 5 years after its receipt, as provided for in the list for primary documents?

IMPORTANT! In accordance with paragraph 4 of Art. 283 of the Tax Code of the Russian Federation, the company must have documents confirming the amount of the loss incurred.

What are these documents and what is their shelf life? Maria leafed through the entire Tax Code, but did not find this information. Then she turned to judicial practice, from which she found out that the amount of loss received can be confirmed with an income tax return and a primary report (Resolution of the Federal Antimonopoly Service of the Moscow Region dated August 31, 2010 No. KA-A40/9849-10-2). Officials of the Ministry of Finance include all primary accounting documentation that substantiates the financial results of the company as such confirmations (letter dated April 23, 2009 No. 03-03-06/1/276).

Thus, the primary accounting document must be kept during the entire period of loss transfer plus 4 years after its complete write-off. Fortunately, Virage LLC was a prosperous and profitable company, and this nuance associated with calculating the storage periods for tax and accounting documentation did not concern it.

For more information about the nuances of loss transfer, see the materials in this section of our website.

How to determine the shelf life of a document?

When working with accounting documents, it is necessary to solve almost all risk management problems. But the main one is documentary confirmation of the legality and validity of the enterprise’s income and expenses during tax inspections.

There are situations when the general storage period of accounting documents determined by law is insufficient to fully ensure the protection of the interests of the organization.

To begin with, let us explain the concept of “accounts receivable”, which is used by tax legislation. In real practice, situations often arise when, for one reason or another, an enterprise is unable to collect debts from counterparties. In this case, accounts receivable arise (it is not the organization that owes money, but it is owed to it). It happens that accounts receivable “hang” for many months, and maybe even years.

As a rule, such situations arise due to the insolvency of the debtor.

But another reason is also possible - an unscrupulous entrepreneur (taxpayer) can thus withdraw quite significant funds from taxation. For example, the goods were delivered, but payment for them was made not to the bank account or to the cash desk of the enterprise, but “unofficially”. In tax accounting, such a transaction reduces the profit received by the enterprise - as a result, the amount of tax payments to the budget is reduced.

It would seem that this kind of situation should occur as a rare exception, but the tax authorities remember about them - they show vigilance and distrust, from which bona fide companies also suffer2. The current legislation on accounting and taxation contains special rules for accounting and writing off receivables that will not be repaid in the foreseeable future.

Arbitration practice shows that courts consider the tax inspectorate’s requirement to provide documents confirming the occurrence of receivables to be justified, even if the storage period for such documents (5 years) has already expired. And if you cannot provide them, then, alas, you will have to pay additional tax on profits that you never even saw, as well as fines and penalties.

We suggest recalling the 5-year storage period for primary accounting documents promised by the accounting law. And after that, make a simple arithmetic calculation to calculate the period during which you may need accounting documents.

Let us emphasize once again: difficulty arises if a loss occurs in the organization’s activities. According to tax accounting rules, it is written off within 10 years. Considering that a tax audit can be carried out for the past 3 years, the required storage period for such documents increases to 13 years.

And in a situation where the loss arose as a result of the write-off of accounts receivable (and its write-off is allowed no earlier than 3 years after the occurrence), the period increases to 16 years! In reality, an even longer storage period may be required, because The 3-year countdown period for determining the period for writing off receivables may be delayed if the debtor somehow confirms his obligations (for example, signs a statement of reconciliation of accounts).

And if there are no documents - the tax inspectorate’s conclusion about the unreasonable write-off of costs, understatement of the taxable base for income tax, fines for non-payment of taxes and penalties for the entire period of non-payment. How many of them will come in 16 years?!

When assessing the shelf life of accounting documents, the versatility of such documents should also be taken into account.

For example, an invoice, in addition to being used for calculating VAT, may contain a customs declaration number that will be needed by customs authorities.

If an enterprise has purchased a batch of goods as raw materials for production, it will not need a customs declaration number in the future. But if you purchased a product from an importer and eventually plan to resell it, then you can answer questions from customs authorities about the source of the goods only with the help of an invoice (only there will be the number of the customs declaration under which the goods were imported into Russia).

Storage periods for accounting documentation

Starting to understand the storage periods for accounting documents, Maria began the most voluminous section of the nomenclature. Even the larger cases, united under the same headings, struck her with their diversity. Only accounting documentation had such a variety of forms and types. Starting from invoices and acts of work performed to inventory lists and reporting. Reporting was subject to permanent storage, in contrast to invoices, acts and other primary documents, the storage period of which did not exceed (according to the list) 5 years:

| Case index | Case title | Number of storage units | Shelf life and article numbers according to the list | Note |

| 1 | 2 | 3 | 4 | 5 |

| 05. Accounting and reporting | ||||

| 05-01 | Accounting policy for accounting of Virage LLC | 5 years Art. 267 | After replacing with new ones | |

| 05-02 | Annual financial report of the organization | Constantly Art. 268 "a" | ||

| 05-03 | Quarterly financial statements of the organization | 5 years Art. 268 "b" | ||

| 05-04 | Documents (protocols, acts, certificates, calculations, statements, conclusions) on revaluation, determination of depreciation, write-off of fixed assets and intangible assets | 5 years Art. 323 | After disposal of fixed assets and intangible assets | |

| 05-05 | Documents (minutes of meetings of inventory commissions, inventories, lists, acts, statements) on the inventory of assets and liabilities | 5 years Art. 321 | Subject to verification | |

| 05-06 | Documents (copies of reports, applications, lists of employees, certificates, extracts from protocols, conclusions, correspondence) on the payment of benefits, payment of sick leave, financial assistance | 5 years Art. 298 | ||

| 05-07 | Primary accounting documents and related supporting documents (cash documents and books, bank documents, counterfoils of cash check books, orders, time sheets, bank notices and transfer requests, acts of acceptance, delivery, write-off of property and materials, receipts, invoices and advance reports , correspondence) | 5 years Art. 277 | Subject to verification. If disputes arise, disagreements remain until a decision is made on the case | |

| 05-08 | Agreements on financial liability of financially responsible persons | 5 years Art. 279 | After the dismissal (change) of the financially responsible person | |

| 05-09 | Accounting (budget) accounting registers (general ledger, order journals, memorial orders, account transaction journals, turnover sheets, accumulative sheets, development tables, registers, books (cards), statements, inventory lists) | 5 years Art. 276 | Subject to verification | |

| 05-10 | Cash book of Virage LLC | 5 years Art. 277 | Subject to verification. If disputes arise, disagreements remain until a decision is made on the case | |

| 05-11 | General ledger of Virage LLC | 5 years Art. 276 | ||

| 05-12 | Fixed asset accounting cards | Before the liquidation of the organization Art. 329 "a" | ||

| — | — | — | — | — |

| Reserve | ||||

| Reserve | ||||

You can find a detailed list of unified documents in the material “Unified forms of primary documents (list)” .

Details about each of these documents are described in separate articles posted on our website.

For example, about the nuances of preparing a consignment note from the material “Unified form TORG-12 - form and sample” .

Accounting documentation

For documentation produced by accounting departments, separate conditions and periods for storing documents in office work apply. Primary documentation, balance sheets, data from accounting registers, reports after processing are required to be stored either in a special room or in a closed cabinet - until they are transferred to the organization’s archive. Strict reporting forms must be kept in metal cabinets or safes. The chief accountant appoints a person authorized to monitor these issues.

If documents of this type are lost, damaged, or illegally transferred to third parties, then the management of the organization must necessarily report this fact to law enforcement agencies. The destruction or seizure of documentation must occur solely in accordance with the requirements prescribed by law.

Nomenclature of files of the labor protection department and periods of their storage

After the storage periods for accounting and tax documents were reflected in the company’s nomenclature, Maria proceeded to a section that was completely unknown to her—the affairs of the labor protection department. All the case headings indicated in the nomenclature were present in the standard list approved by Order No. 326, so it was easy to set their storage periods:

| Case index | Case title | Number of storage units | Shelf life and article numbers according to the list | Note |

| 1 | 2 | 3 | 4 | 5 |

| 06. Occupational safety | ||||

| 06-01 | Health and safety instructions | constantly Art. 8 "a" | ||

| 06-02 | Reports on the implementation of special labor safety measures and documents for them (protocols, decisions, conclusions, lists of workplaces, information, data, summary statements, declarations of conformity, cards for special assessment of working conditions for specific workplaces, lists of measures to improve working conditions and labor protection) | 45 years Art. 407 | Under harmful and dangerous working conditions: 50 years - if the documents were completed after 01/01/2003; 75 years old - if documents were completed before 01/01/2003 | |

| 06-03 | Journals, accounting books: training on labor protection (introductory and on-the-job); preventive work on labor protection, testing knowledge on labor protection | 45 years old, art. 423 "a" 5 years old, art. 423 "b" | ||

| 06-04 | Fire safety briefing log | 3 years Art. 613 | ||

| 06-05 | Documents (reports, acts, lists, schedules, correspondence) of periodic medical examinations | 3 years Art. 635 | ||

| — | — | — | — | — |

| Reserve | ||||

| Reserve | ||||

As can be seen from the nomenclature, the labor protection department prepared a variety of journals, which had to be stored from 3 (for example, a fire safety briefing journal) to 45 years (SOUT documents).

The importance of documents of permanent and long-term storage

The permanent and long-term storage of documents (up to 75 years) in the archive is usually determined by the significance of these documents for the state. The historical, cultural and scientific value of documentation is determined by an expert commission, and unauthorized destruction of potentially valuable documents is prosecuted by law.

Permanent documents

Permanent documents include all papers that are the cultural heritage of the country or contain historical and scientific facts (for example, some types of design documentation; government documents, etc.).

Planning and statistical documentation: how long to store it

The next section of the nomenclature was small in volume. It consisted mainly of plans and statistical reporting. All forecast and planning papers as a whole according to the list were ordered to be kept permanently. Only individual employee plans and reporting did not require such a long retention period - the period of time during which they cannot be disposed of is only 1 year.

| Case index | Case title | Number of storage units | Shelf life and article numbers according to the list | Note |

| 1 | 2 | 3 | 4 | 5 |

| 07. Planning, statistics and finance | ||||

| 07-01 | Economic and social development plans of Virage LLC | Constantly Art. 196 | ||

| 07-02 | Business plans of Virage LLC, documents (feasibility studies, conclusions, certificates, calculations) to them | Constantly Art. 197 | ||

| 07-03 | Annual plans of Virage LLC for main areas of activity | Constantly Art. 198 | ||

| 07-04 | Operational plans (quarterly, monthly) for all areas of activity | Until the need disappears Art. 201 | ||

| 07-05 | Individual employee plans | 1 year Art. 203 | ||

| 07-06 | Documents (tables, certificates, calculations) of summary statistical reports | Until the need passes Art. 338 | ||

| 07-07 | Individual employee reports | 1 year Art. 216 | ||

| — | — | — | — | — |

| Reserve | ||||

| Reserve | ||||

Where can I find out the storage periods for documents not included in the standard list?

The section of the nomenclature for cases formed or used in the production and technical department (PTO) included headings of cases that were not at all familiar to Maria. And in the standard list approved by Order No. 236, she did not find documents with similar names. Since the shelf life in column 4 of the nomenclature must be entered in any case, Maria turned to her immediate supervisor for help, who entrusted her with this task.

From him, Maria learned that the storage periods for company documents are determined on the basis of a standard list approved by Order No. 236, as well as departmental lists. For example, periods of storage of VET documents must be determined according to the List of standard archival documents generated in the scientific, technical and production activities of organizations, indicating storage periods (as amended by Order of the Ministry of Culture dated April 28, 2011 No. 412).

According to the specified list, Maria indicated in the nomenclature the corresponding storage periods for VET documentation:

| Case index | Case title | Number of storage units | Shelf life and article numbers according to the list | Note |

| 1 | 2 | 3 | 4 | 5 |

| 08. VET | ||||

| 08-01 | ||||

| 08-02 | Technological maps | Constantly Art. 141 | ||

| 08-03 | Technological rules and regulations | Before replacing with new ones Art. 143 | ||

| 08-04 | Technological process specifications | Before the liquidation of the organization Art. 145 | ||

| 08-05 | Technological passport | As long as the need exists Art. 197 | ||

| 08-06 | Tool setting chart | Before replacing with new ones Art. 213 | ||

| — | — | — | — | — |

| Reserve | ||||

| Reserve | ||||

Having studied the above list, Maria asked another question to her supervisor: how to determine the periods during which VET documents are subject to storage if they are not indicated in this list? You will find out the answer to this question in the next section.

Definition of a typical archival document

One of the most serious is the very concept of “standard archival documents” generated in the activities of organizations. It would seem that the answer is simple. These are documents that are formed in all or most (many? group?) organizations, regardless of type of activity and form of ownership.

What is the criterion for the concept of “standard document” ? An illustrative example: 504 items were included in the List of standard management documents generated in the activities of organizations, with storage periods (2000), and in the List of standard management archival documents generated in the process of activities of state bodies, local governments and organizations, with an indication of the dates storage (2010) 1003 items have already been added.

In other words, the number of documents falling into the concept of “standard” has doubled in a short period of time. Is this an objective reality or an unjustified expansion of the concept of “standard document”? Of course, with the introduction of new types and forms of activity into our economic, social, financial structure, some types of documents reflecting these and new types of activity become de facto standard.

However, one cannot deny the obvious fact that, for a number of reasons, the List of standard archival documents has been unnecessarily expanded by including a number of categories of documents that sometimes are not and cannot in the future fall under the concept of standard documents.

For example, what do wills, gift agreements, issuer reports, reports of professional participants in the securities market (also in certain forms), passports of buildings and structures, documents on shared ownership of property, documents on the return of property of rehabilitated citizens have to do with standard documents? The list goes on.

Undoubtedly, when including these types of documents in the standard list, a number of factors were taken into account, including such serious ones as proposals from federal executive authorities, archival management bodies of the constituent entities of the Russian Federation, and state bodies. They were dictated by the natural desire “not to miss, not to lose, to set a storage period,” taking into account the existing shortage of industry lists of documents with storage periods. There was a subjective desire of some departments to include a number of their important industry documents in the List, making their work easier and removing some of the responsibility for establishing storage periods for archival documents.

For all its external attractiveness, the ideology of further expanding the composition of documents included in the List of Standard Documents is systemically incorrect for a number of objective reasons.

Firstly, the time of universal reference books has passed and an attempt to give an answer to most questions in one standard is unrealistic.

Secondly, the very basic concept of a “standard document” actually disappears.

Thirdly, the sphere of responsibility is being blurred between the Federal Archives Management Body, whose prerogative is to identify standard types of documents, establish their storage periods and develop standard lists, and federal government and administrative bodies, whose task is to create sectoral (departmental) lists of documents with storage periods in the archive , as established by the current archival legislation.

Results

Retention periods are established by standard or departmental lists in order to ensure the safety of important documents.

The storage period for documents is set in the range from 1 year to 75 years, depending on the significance. Certain types of documentation must be stored on a permanent basis.

If temporary storage documents with different periods are grouped in one case (1 year, 3 years, 5 years, etc. - which means different degrees of their significance), then the storage period of the case according to the nomenclature is established according to the most valuable documentation, that is, longer .

It is prohibited to reduce the storage periods established by the list and to arbitrarily establish them for documents for which there is no information about storage periods in the standard and departmental lists. To determine the storage period for such documentation, you must contact Rosarkhiv specialists.

Sources:

- Basic Rules for the work of archives of organizations (approved by the decision of the Board of Rosarkhiv dated 02/06/2002)

- Order of Rosarkhiv dated December 20, 2019 No. 236

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

Determining the storage periods for documents

However, the periods for storing documents in the archive are strictly determined by the archival legislation of our country, and violation of these terms can result in lawsuits, fines and even criminal liability for the company.

Types of shelf life

So, what period of storage of documents in the archive does Russian legislation determine?

Documents of permanent, long-term and temporary storage periods

All documents according to their storage periods in the archive are divided into three types: permanent, long-term (up to 75 years) and temporary (up to 10 years) storage periods. The storage period for documents in the archive does not depend on the form in which the document is stored - paper or electronic. When an organization is liquidated, documents with permanent and long-term storage periods are transferred for storage to the state archive, and temporary documents are destroyed after an inventory is carried out and an order for the destruction of documents is drawn up. As a matter of fact, an order for the destruction of documents with temporary storage periods must be drawn up without fail every time a company decides to clear its premises of unnecessary documentation.