When is offset possible?

Offsetting counterclaims is a way of terminating (in whole or in part) already existing mutual obligations.

The amounts of mutual debt very rarely coincide; usually the debt of one party is greater than the debt of the other. Then offset is made for the smaller amount. And the party whose debt was greater will have part of the obligation remaining unpaid.

Settlement of obligations is possible only if the following conditions are met.

Uniformity of counter debts

Requirements are considered homogeneous when they have the same subject and can be compared. Let's say, monetary claims expressed in one currency are homogeneous. For example, one party has a debt to pay for work performed, and the other has a debt to repay the loan, while each party owes the other money, which means that such obligations can be credited.

The courts consider it possible, for example, to set off claims for payment of the customer’s debt for work performed and for payment of a penalty for the contractor’s violation of deadlines for completing work, because, despite their different legal nature, these claims are monetary, that is, homogeneous

In principle, the parties can agree on the offset of heterogeneous claims, such as when the debt of one party is expressed in rubles, and the other in foreign currency. But then the companies need to agree on the rate at which the foreign currency debt will be converted into rubles.

Arrival of the deadline for fulfillment of obligations

At the time of offset, the payment deadline for each claim under the contract must already have arrived. For example, a tenant cannot offset against rental payments the cost of inseparable improvements made at his own expense with the consent of the landlord. And all because the counter-obligation of the lessor to reimburse the cost of these improvements will arise only after the termination of the lease agreement (unless otherwise provided for in the agreement. Although the Supreme Arbitration Court believes that offsetting obligations with unfulfilled deadlines is also possible

If the parties have not established specific terms for repayment of debts in the agreement, then offset can be carried out at any time.

Not long ago, changes were made to the Civil Code of the Russian Federation, and from June 1, 2015, in cases provided for by law, it is allowed to set off a counterclaim that has not yet come due

Prohibition of offset

There are cases when netting is in principle unacceptable, for example:

- the parties provided for such a condition in the contract;

- offset is directly prohibited by law (for example, in most cases it is impossible to carry out offsets with a foreign partner in foreign economic activity

- according to the requirements, the statute of limitations has expired (3 years from the date of occurrence

Settlement under the supply agreement and loan agreement

Civil Code of the Russian Federation Article 807. Loan agreement

(as amended by Federal Law dated July 26, 2017 N 212-FZ)1. Under a loan agreement, one party (the lender) transfers or undertakes to transfer into ownership the other party (borrower) money, things defined by generic characteristics, or securities, and the borrower undertakes to return to the lender the same amount of money (loan amount) or an equal amount received them things of the same kind and quality or the same securities.

If the lender in the loan agreement is a citizen, the agreement is considered concluded from the moment the loan amount or other subject of the loan agreement is transferred to the borrower or the person specified by him.

2. Foreign currency and currency values may be the subject of a loan agreement on the territory of the Russian Federation in compliance with the rules of Articles 140, 141 and 317 of this Code.

3. If the lender, by virtue of a loan agreement, has undertaken to provide a loan, he has the right to refuse to fulfill the agreement in whole or in part if there are circumstances clearly indicating that the loan provided will not be repaid on time.

The borrower under a loan agreement, by virtue of which the lender has agreed to provide a loan, has the right to refuse to receive the loan in whole or in part by notifying the lender before the deadline for transferring the subject of the loan established by the agreement, and if such a deadline is not established, at any time before receiving the loan, if otherwise is not provided by law, other legal acts or a loan agreement under which the borrower is a person carrying out entrepreneurial activities.

4. A loan agreement can be concluded by placing bonds. If a loan agreement is concluded by placing bonds, the bond or the document securing the rights under the bond shall indicate the right of its holder to receive, within the period specified by it, from the person who issued the bond, the nominal value of the bond or other property equivalent.

5. The loan amount or other subject of the loan agreement transferred to a third party specified by the borrower is considered transferred to the borrower.

6. A borrower - a legal entity has the right to attract funds from citizens in the form of a loan at interest through a public offer or by offering to make an offer directed to an indefinite number of persons, if the law grants such a legal entity the right to attract funds from citizens. The rule of this paragraph does not apply to the issue of bonds.

7. The specifics of providing a loan at interest to a citizen borrower for purposes not related to business activities are established by law.

What documents need to be completed

The decision to carry out mutual offset must be documented. This is done, in particular, so that in the future there will be no problems either with counterparties or with inspectors. After all, in the absence of documents, neither you nor your business partner will have confirmation of your actual expenses, which means there is a risk of saying goodbye to expenses and earning penalties and fines.

Of course, you must have “traditional” documents documenting your relationship with the counterparty and the facts of the occurrence of mutual debts: contracts, invoices, acceptance certificates for work performed/services rendered, invoices, etc.

And the credit itself can be issued in two ways.

METHOD 1. One of the parties declares a set-off. But before carrying out a unilateral set-off, we recommend that you sign a reconciliation act for mutual settlements with the counterparty. This document is optional, but it will help confirm the amount of debt (especially if some of the debt has already been paid) and avoid unnecessary disputes with the counterparty.

Please note that one signed act of reconciliation of mutual settlements is not sufficient for offset, since such an act reflects only the business transactions of the parties for a certain period of time and is a document confirming the state of mutual settlements. Whereas in order to set off, the document must contain a clear and unambiguous indication of the termination of the obligations of each party.

After signing the reconciliation report, you (or your counterparty) write a letter (application, notification) to the other party. The offset will take place only if such an application is received by the relevant party. Therefore, submit the application under a personal signature (the recipient must sign your copy of the document) or send it by registered mail with acknowledgment of receipt.

The date of unilateral offset and, accordingly, its reflection in accounting will be:

- the specific date from which the parties’ debts are considered repaid, if it is indicated in the application;

- the day of receipt of the application (letter, notification) by the counterparty, if a specific date is not specified by the initiator of the offset.

METHOD 2. The parties sign a two-sided document

- offsetting act;

- agreement on the offset of mutual claims.

Compared to the first quarter of 2014, 1.5 times more goods were paid using claims offset

This will help avoid disputes and misunderstandings between counterparties. And when offsetting heterogeneous obligations or obligations with unfulfilled deadlines, a bilateral agreement of the parties is required

The offset date will be the day the agreement (act) is signed, unless otherwise expressly stated in the document.

Please note that both in a unilateral statement and in a set-off agreement, it is important to define as accurately as possible the obligations (debts) of each party and indicate:

- the grounds for their occurrence (refer to contracts, primary documents, invoices) in order to confirm the reciprocity and homogeneity of obligations;

- amounts of liabilities;

- deadlines for each of them.

The document must determine which obligations are repaid by offset and indicate the remaining debt of one of the parties.

In the absence of these essential conditions, the offset may be declared invalid.

We will show you how you can fill out an application for a test using method 1.

127204, Moscow, Dmitrovskoe sh., no. 157

Mayskaya V.P. 125315, Moscow, Leningradsky Ave., 68

Ref. No. 36 from 05/28/2015

Application for offset of counterclaims

Limited liability company represented by General Director S.L. Rukodelnikov, acting on the basis of the Charter, in accordance with Art. 410 of the Civil Code of the Russian Federation declares a partial offset of counterclaims of the same type, the deadline for fulfillment of which has come.

Information on counterclaims and debt of LLCs and LLCs as of May 28, 2015:

| Debt accepted for offset | Number and date of the agreement, essence of the obligation | Number and date of the primary document, invoice | Amount of liability, rub. | Deadline for fulfilling the obligation |

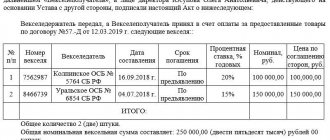

| Debt of LLC to LLC | Payment for consulting services under agreement No. 12 dated March 20, 2015 | Act No. 12 of 05/08/2015; invoice No. 12 dated 05/08/2015 | 295,000 (including VAT 18% - 45,000 rubles) | 14.05.2015 |

| Debt of LLC to LLC | Payment for repairs of the premises under contract No. 96 dated 02/16/2015 | Act No. 96 dated May 15, 2015; invoice No. 96 dated 05/15/2015 | 377,600 (including VAT 18% - 57,600 rubles) | 25.05.2015 |

The offset is made in the amount of 295,000 (two hundred ninety-five thousand) rubles, including VAT of 45,000 (forty-five thousand) rubles.

After offsetting mutual homogeneous claims, the balance of the LLC's debt to the LLC as of May 28, 2015 is 82,600 (eighty-two thousand six hundred) rubles, including VAT 12,600 (twelve thousand six hundred) rubles. The LLC's debt to the LLC has been repaid in full.

I received the application for credit on May 28, 2015.

Offsetting under loan agreements sample

Settlement agreement sample.

Domestic rule-making acts provide for the possibility of terminating counterclaims by offset. Acceptable ways of this option for performing duties are:. According to the general rule established by the civil legislation of Russia, all enterprises must fulfill their obligations and cannot change them or refuse to fulfill them.

To do this, interested companies must draw up a document containing the following information:.

Dear readers! Our articles talk about typical ways to resolve legal issues, but each case is unique.

If you want to find out how to solve your particular problem, please use the online consultant form on the right or call the numbers provided on the website. It's fast and free!

- Act of mutual settlement between organizations

- Netting between two organizations: sample, how to do it

- Settlement agreement between organizations

- Loan agreement

- Settlement agreement between organizations (sample)

- Offsetting: important nuances

- Settlement between loan agreements

Act of mutual settlement between organizations

VIDEO ON THE TOPIC: Settlement (barter). How to apply?

Is it possible to carry out mutual settlement between legal entities?

It is possible to set off between spouses if the husband is owed by the company where he is the director, and his wife is owed by the same organization; a loan agreement was previously concluded with her for the purchase of a car.

Is it possible to offset similar counterclaims between the developer, a legal entity, and the shareholder, an individual, under an equity participation agreement, if a loan agreement was previously concluded with the individual; the individual lent a sum of money to the legal entity.

Offset can be made by agreement of the parties Art. What documents should be used for offset: if 1. The loan is provided to individual 1 under an Agreement between individuals, there is a receipt 2. Individual 1, who has the loan under the Agreement, is the founder and general director of the LLC.

LLC - did repair work to individual 2 - who owes money. How to arrange mutual settlement between them? Agreement on assignment of rights under a loan agreement. Agreement of assignment under a loan agreement. Agreement on offset of mutual claims. Determine the terms as you wish.

There will be no offset according to the Civil Code of the Russian Federation - there is no entrepreneurial activity of the founder and general director. Let them supply the same amount of repair work as under the loan agreement and pay each other with the same amount.

Article of the Civil Code of the Russian Federation The obligation is terminated in whole or in part by offsetting a counterclaim of the same type. They owe each other money. For offset, a statement from one party is sufficient.

After drawing up an application for offset, an individual must submit a receipt if the individual’s obligation is terminated completely, that is, the amount is repaid.

I have a very huge request for an answer! This is the situation. A criminal case has been initiated and is being conducted by the prosecutor's office. I don’t know against whom exactly it was initiated against a specific person or an unidentified person.

Personally, no one called me anywhere, interrogated me or notified me that I was a suspect. But here’s what irritates and even infuriates me! Employees of the prosecutor's office and employees of the criminal investigation department, the police, unofficially, mainly that is, when they met on the street and officially called for questioning, they dragged a bunch of people from my address phone book.

They somehow got the transcripts of my phone calls, then they also got the transcripts of everyone's phone calls. Who called me or I called them That's what they do now.

For example, they meet on the street a person I know from the address book and ask about his relationship with me. And some are even told what I am suspected of, again, all unofficially. And then that person spreads all these “suspicions” all over the world and I walk around here like a fool. consequence!

What else are they doing? They call the person from my address book and ask him, already having a transcript of the phone calls and that person also why he called me then and then and then!

The person does not understand why he is not allowed to call me or anywhere else, and the person also does not understand where the prosecutors and police officers got the information about his calls, whether he is already a suspect, etc.

Some are simply called in and asked about what they did on such and such a date or why they called a taxi to such and such an address. Others are called in and also asked questions such as “how do you explain the fact that you were seen with the suspects in a crime”? The man asks “who is this with, the suspects.”

They answer that it doesn’t matter with whom! And so, excuse me, these employees walk around asking everyone about me.

They ask everyone about the calls, they say what they suspect me of, but you can’t prove it, since no one needs to go as a witness later, and in the official interrogation they don’t give my full name directly. Only they still haven’t told me anything about the fact that I am a suspect. but I hear this from every, excuse me, dog on the street!

As far as I understand, if I am a suspect, then this is already a procedural status.

So that means I should have been the first to be notified about this?! And I would like to know how the prosecutor’s office and the police, within the framework of the criminal case, taking into account all the above circumstances, no one informed me that the suspect could obtain confidential information about the transcripts of calls from me and everyone who called me or I called them called, all the other people? Are all such actions legal and WHAT should I do with them about this?!

What specific violations are there and how can you prove them if there are any?! PS: And the background, as I believe, is from the year before last case with an accident with my participation and the participation of a police officer. Road accident with casualties. They can’t put me in jail, but they really want to, but they don’t want their own employee! I already tried somewhere on the forum to ask what to do. They gave very “sensible” advice - to write a complaint to a higher prosecutor’s office.

So what can I write, when they act this way during interrogation, everyone clearly understands who they are talking about, but they don’t give their full name, and on the “street” they trash it, so you can’t get anyone to be a witness Plus the fact that somehow one of my acquaintances is 2 and a half year wrote in a circle to the prosecutor's office complaints about the illegal refusal to initiate a criminal case.

There were many employees in the Criminal Code, there were many witnesses, beatings, and the head of the Criminal Code. And also nothing. Go here and pee on them! Please help me! How can I help you if you don’t want to write to the prosecutor’s office?

All the actions that you wrote indicate that you are in operational development and, as they say, they are collecting material on you.

If these actions affect your honor and dignity, then write to the prosecutor’s office or file a claim in court for the protection of honor and dignity against specific law enforcement officers.

Witnesses who were caught on the street and told them everything that you described should come forward as evidence.

In addition, operational actions against you must be authorized within the framework of a criminal case by its leading investigator.

If there is no such case against you, then this is an additional argument in your favor at the court for the protection of honor and dignity. Sincerely, E. There is no other option.

On the possibility of offsetting claims between two companies - under an agreement for storing goods in a warehouse and a loan agreement. Will the tax authorities accept this? Vadim, good afternoon! They must accept the offset, since this transaction does not contradict current legislation.

All the best, Best regards. I believe that if you draw up the Offset Agreement correctly, then there will be no problems. Reviews of lawyers within 24 hours. Settlement between loan agreements.

Free question to lawyers online If you find it difficult to formulate a question, call, a lawyer will help you:.

Free multi-channel phone 8 If you find it difficult to formulate a question, call the free multi-channel phone 8, a lawyer will help you. Ask a lawyer faster Answer in 5 minutes.

The administrator types a message.

There are a great many ways to borrow something from someone. The current legislation presents various schemes and options to business entities.

Topics: Accounting. Only the beginning of the document is shown. To view the entire text, you must subscribe to the AMB-Express magazine:. A simplified tax system organization rents an office from another organization. There is a lease agreement under which our organization pays a certain amount monthly for rent. The lessor took a certain amount from our organization under a loan agreement.

Netting between two organizations: sample, how to do it

As of We ask you to set off the amounts due to us under the supply agreement from the court ruling dated. Within a few minutes, a letter will be sent to the specified email with instructions for activating your account. Check the counterparty Check against 14 databases and 40 sources. Ready-made solutions for each status. Search for an article Search for a company.

Settlement agreement between organizations

Sometimes counterparties are faced with the question of conducting mutual offset transactions.

For example, if two legal entities have entered into agreements with each other, for example an agreement for the provision of legal services, according to which they are obliged to perform certain actions in relation to each other, then counter obligations can be offset.

In accordance with the article of the Civil Code of the Russian Federation, obligations can be terminated either in full or in part, taking into account a counterclaim of the same type, the time period for which has either already arrived, or its period is not specified or is determined by the date of demand.

For offset, an application from one of the counterparties under the agreements is required. If the other party agrees, then an act of offset of claims is drawn up. Cases when offset of claims is not possible in accordance with the law. If, at the request of one person, the claim is subject to a statute of limitations and this period has expired.

Is it possible to carry out mutual settlement between legal entities?

This article gives an idea of mutual settlement between two or more organizations, answers the question of why this business transaction is necessary, and with what documents it is formalized. Common offset errors and a practical example of registration in 1C version 8 are also discussed in detail.

We will tell you what mutual settlement is between two organizations and how exactly it is carried out in practice. If there are mutual obligations between organizations, a decision is often made to offset the least of them.

Based on this, we can define one of the most common business transactions.

So, offset is an accounting operation based on non-cash payments, which involves the termination of counter-obligations arising from organizations that are at the same time debtors and creditors to each other, buyers and suppliers.

It turns out that the main goal of mutual settlement is precisely to simplify legal and financial relations between organizations. The offset operation, despite its simplicity, requires strict compliance with the Civil and Tax Code of the Russian Federation. Therefore, before making a decision on offset, it is necessary to make sure whether the following conditions are simultaneously met:

Loan agreement

When a company and its counterparty have mutual debts, they can simplify and speed up their settlements through offset. The amounts of mutual debt very rarely coincide; usually the debt of one party is greater than the debt of the other. Then offset is made for the smaller amount. Requirements are considered homogeneous when they have the same subject and can be compared.

The drawing up of a netting agreement occurs in cases where two parties to a transaction agree among themselves on the full or partial netting of funds under the agreement. Open and download online. Offsetting allows you to pay for goods or services received in return.

An act of offset is usually drawn up in cases where there is mutual debt between counterparty enterprises. The type of debt does not matter - it can be financial or in the form of some other material assets.

However, when drawing up an act of offset, the most important condition is that the counterclaims are of a homogeneous nature, for example, monetary claims on both sides. Open and download online. Most often, the netting act is used by representatives of small and medium-sized businesses facing financial problems.

However, there are a number of situations when drawing up an act of offset is not possible. In particular:. The act of offset may include both two parties, the main option, and more.

Each has its own copy! The act of offset does not have a unified, strictly approved form, therefore legal entities have the right to write it according to their own developed template or in free form.

“On netting under loan agreements. We ask you to set off the amounts due to us under the supply agreement dated No. P and.

.

Settlement between loan agreements

.

.

.

.

Source: https://astmbdou19.ru/meditsinskoe-pravo/vzaimozachet-po-dogovoram-zayma-obrazets.php

How to reflect netting in accounting

Now it’s time to find out what tax consequences await the company when offsetting mutual claims.

VAT. The offset does not affect VAT. That is, on the day of offset there is no need to adjust either the amount of VAT payable accrued on the date of shipment of goods (performance of work, provision of services) or the amount of deduction

Problems with the deduction should not arise in the case where you were given an advance payment for upcoming supplies of goods (work, services), from which you paid VAT to the budget, but subsequently you did not sell the goods (work, services), and the advance was credited against counter obligations

Income tax. There will be no income tax consequences for you when making an offset. You will reflect the proceeds from the sale of goods (work, services) to your counterparty and the costs of purchasing goods (work, services) from him in tax accounting even before the offset. And the fact of repayment of debt for sold goods (work, services) is not taken into account when reflecting income and expenses.

USNO. For simplified people, the date of recognition of income is not only the day the money is received, but also the day the debt is repaid in another way. Offsetting is that very different method. That is, on the basis of an act (agreement, application) of offset, you need to reflect income in the amount of the repaid debt of the counterparty. At the same time, the goods (work, services) you purchased will be considered paid (also for the amount of the repaid debt), which means that one of the conditions for recognizing expenses in the “income-expenditure” is met.

Accounting. Income from the sale of goods (works, services) and expenses for their purchase should be reflected in your accounts as usual. As a result, you, as a buyer of goods (works, services), will have accounts payable (balance on the credit of account 60 “Settlements with suppliers and contractors” or account 76 “Settlements with various debtors and creditors”) for their payment. At the same time, when selling goods (works, services), you generate accounts receivable (the balance in the debit of account 62 “Settlements with buyers and customers”).

On the date of offset, make a debit to account 60 “Settlements with suppliers and contractors” (account 76 “Settlements with various debtors and creditors”) – credit account 62 “Settlements with buyers and customers” for the amount of less debt. Thus, receivables and payables will be fully or partially repaid.

Pay attention to one more important nuance. If you decide to set off unilaterally, you need to take into account that subsequently you will not be able to refuse your decision

An act of mutual settlement between an individual for loan repayment and reporting

A full explanation on the topic: “the act of mutual settlement between an individual for repaying a loan and the accountant” from a professional lawyer with answers to all your questions.

Act of offset of mutual claims between organizations (sample)

If the debt of two organizations is being repaid, then it is necessary to draw up two copies of the act.

The form must indicate the date of its registration and the name of the locality. This is followed by the details of each organization - name, details of the director.

It is necessary to provide a list of documents confirming the debt (agreements, invoices and other documents), indicate their dates and numbers.

The amount of debt that is subject to mutual offset is also indicated; the remaining unset-off amount must be transferred to the current account within the established time frame.

No video!

| (click to play). |

Cases when offset of claims is not possible in accordance with the law

1. If, at the request of one person, the claim is subject to a statute of limitations and this period has expired.

2. When compensating for harm caused to the personal health or life of an individual.

When collecting alimony.

4. With lifelong maintenance, etc.

Must be observed when drawing up the act

Severodvinsk-15 November 17, 2013.

Under the service agreement dated March 20, 2013 No. 3496829-LRPO.

2. Under the service agreement dated April 1, 2013 No. 3968576-TRPA.

The entire form of the netting act is in the attached file.

The act is drawn up by mutual agreement of the parties, at the request of one of them.

The act may include two parties (the main version) or more.

Each has its own copy!

It is mandatory to include in the Settlement Certificate

- information about enterprises that have reached an agreement on mutual offset;

- the grounds for the occurrence of debts (here it is enough to indicate the documents on which they arose);

- list of obligations;

- the final amount of the debt.

Copies of the documents on which the debts arose must be attached to the act.

The act has a completely standard structure from the point of view of office work.

The second part of the act concerns detailed information on the basis of which agreements mutual debts arose (with a reference to them - numbers and dates of preparation), as well as their full amounts on both sides (in numbers and in words).

In the final part, the act must be signed by all interested parties (the position, surname, and patronymic name of the employee signing the document are indicated here). The act can be certified with seals, but this is not necessary.

Settlement without problems

Taxpayers who report income using the accrual method report income as well as expenses on their accounts before offsets are made. Therefore, they are recognized at the time the goods are shipped from the warehouse. If the act of writing off liabilities was drawn up later, the accountant will need to make adjustments to the amounts in the statements in the future.

Attention

The agreement should also indicate other types of taxes, just write them on a separate line. It is necessary to carefully study the list of taxes and fees that must be transferred to the state treasury in 2021. An example of filling out an act of offset of claims. Features of drawing up acts of offset. Tripartite Legislation allows offsets to be carried out by several partners.

For this purpose, a tripartite act is drawn up. The debt of the three parties is specified in the contract and repaid in accordance with the agreed structure.

Sample mutual agreement. how to write offset in a contract

At the same time, when selling goods (works, services), you generate accounts receivable (the balance in the debit of account 62 “Settlements with buyers and customers”).

On the date of offset, make a debit to account 60 “Settlements with suppliers and contractors” (account 76 “Settlements with various debtors and creditors”) – credit account 62 “Settlements with buyers and customers” for the amount of less debt.

Thus, receivables and payables will be fully or partially repaid. *** Please pay attention to one more important nuance.

If you decide to set off unilaterally, you need to take into account that subsequently you will not be able to refuse your decision. 9 Information letter of the Presidium of the Supreme Arbitration Court dated December 29, 2001 No. 65. Other articles of the magazine “MAIN BOOK” on the topic “Receivable / Creditor”: 2021

Features of working with the act of offset

It must also indicate the specific obligations withdrawn for offset, the dates of their occurrence, payment and amount. Each copy must have the signatures of the director and chief accountant of both parties and imprints of company seals. VAT in offset When drawing up an act, the amount of input and output VAT must be entered in the appropriate columns of the form.

It must be paid by money transfer to the bank in the reporting period when the netting act was signed. However, tax authorities often equate the offset operation to an exchange agreement and require the supplier to take into account the exclusive input VAT.

This is unacceptable by law. If you receive such a claim, feel free to contact arbitration. Recently, such cases are most often resolved in favor of the tax payer.

By the way, offset amounts are not exempt from tax deductions.

Online magazine for accountants

You cannot use the act of mutual offset of debt in the following situations:

- expenses for lifelong maintenance of citizens;

- payment of alimony;

- compensation for harm caused to human health;

- one side of the offsets is involved in its bankruptcy case.

Such a document is drawn up in two copies: the first remains with the organization that initiated the transaction, the second is transferred to the counterparty. If the act contained references to related documents, for example, contracts, invoices, copies of them must be attached to it.

Rules of conduct Using the analysis of receivables and payables, enterprise specialists identify the presence of possible mutual requirements with partner organizations. Settlement is possible at the request of one party.

In practice, as a rule, the decision is made by all participants in the future transaction.

How to draw up an act of offset of mutual claims - sample?

Offsetting can be carried out by sending the counterparty an application for offset (See “Offsetting between organizations: sample application.” But there is another option - drawing up an act. This will be discussed in this article. If the requirements of the parties are equivalent, the obligations are considered mutually fulfilled.

- 1 Rules for netting

- 2 Filling out the netting act

- 3 When concluding a trilateral netting agreement

Rules for netting When conducting netting, the following requirements must be met:

- offset is carried out by organizations participating in two or more obligations for which counterclaims have arisen;

- the demands must necessarily be of a counter nature.

Settlement of loans and services

At the same time, when selling goods (works, services), you generate accounts receivable (the balance in the debit of account 62 “Settlements with buyers and customers”). On the date of offset, make a debit to account 60 “Settlements with suppliers and contractors” (account 76 “Settlements with various debtors and creditors”) – credit account 62 “Settlements with buyers and customers” for the amount of less debt. Thus, receivables and payables will be fully or partially repaid. *** Please pay attention to one more important nuance. If you decide to set off unilaterally, you need to take into account that subsequently you will not be able to refuse your decision. 9 Information letter of the Presidium of the Supreme Arbitration Court dated December 29, 2001 No. 65. Other articles of the magazine “MAIN BOOK” on the topic “Receivable / Creditor”: 2018

Is it possible to offset loans?

Let's look at how to correctly draw up a netting agreement, under what conditions it is impossible to do this, what the consequences will be for those using the simplified taxation system, and how to calculate VAT. What is offset? Offset under various contracts is a procedure in which the obligations of an organization are considered fulfilled through the performance of similar services. That is, you ordered a certain economic action from the client’s organization, he acted as a performer, performed the service and transferred it. But for some reason you did not pay for it in monetary terms. Then your client acted as a customer, and you performed economically similar work for him. At the moment when the time has come to demand payment, you have drawn up an agreement for offset of services. At the end of the day, no one owes anyone anything. This is the meaning, if stated in simple language.

The act is drawn up in two copies, with copies of source documents attached.

- Offsetting between organizations. Agreement and act of offset of mutual claims

- Assignment is... Sample assignment agreement between legal entities

- Assignment of debt between legal entities: how to formalize?

- How to correctly draw up a reconciliation report?

- Preamble to the agreement. Amendments to the preamble of the agreement

- Business letter samples. How to write a business letter

- Interest-free loan from the founder.

Current Subscribe to news Daily: taxation and accounting News

- Tax news

- Seminars for accountants

- Tax Code 2021, 2018

- Newsletter

Publications Bukh. programs

- Salary program

- Personnel Program

- Program Report Card

- Online accounting

- 2NDFL

- Personalized accounting

- Enterprise program

- Simplified system

- Entrepreneur

- Electronic reporting

- Online accounting

Salary, Timesheet, Personnel. Download and Run! 978 rubles, including 2NDFL, persuchet Submission of electronic reporting via the Internet to the Social Insurance Fund, Federal Tax Service, Pension Fund, Rosstat from Pravkons.

At the same time, paragraph 7 of the annex to the information letter of the Presidium of the Supreme Arbitration Court of the Russian Federation dated December 29, 2001 No. 65 states that the legislation does not insist that the requirement for offset arise from the same obligation or from obligations of the same type. It follows from this that obligations that are related to the execution of different contracts, but involve the same method of repayment, can be considered homogeneous. Thus, obligations are recognized as homogeneous if they require the same method of repayment and are expressed in the same currency. Based on the foregoing, it follows that mutual claims can also be offset under loan agreements that provide for the same method of repaying obligations denominated in the same currency.

Registration and accounting of netting - loan and delivery

For offset, a statement from one party is sufficient. However, as a rule, the parties formalize the offset by a bilateral act. Since the provision of services is reflected in any case through account 90 “Sales”, in this situation it is advisable to make the following accounting entries: Debit 51 Credit 66 (67) – 500,000 rubles.

– a loan was received from company A Debit 66 (67) Credit 51 – 100,000 rubles. – part of the loan amount was returned to the lender Debit 62 Credit 90-1 – 400,000 rubles. – revenue from the provision of services to company A is reflected Debit 90-2 Credit 20 – expenses associated with the provision of services are written off Debit 66 (67) Credit 62 – 400,000 rubles. – reflects the offset of obligations under the loan agreement and the service agreement (offset act). We believe that you are not sufficiently aware of the capabilities of your accounting program.

Settlement without problems

To better understand the intricacies of design, implementation and reflection in accounting for offsets, I suggest you read this article. When it is possible and when it is not possible to carry out offsets The ability to pay off obligations by offsetting mutual claims is provided for in Art. 410 of the Civil Code of the Russian Federation. The same rule of law establishes the conditions necessary for mutual settlement between counterparties:

- Presence of counter debt. That is, each party acts as both a debtor and a creditor in relation to the other party.

- Uniformity of requirements. For example, a monetary claim can only be offset by a counter monetary claim. If a monetary claim is offset by the delivery of goods, then we are talking more about a barter transaction, but not about offset.

- The deadline for fulfilling the requirements has arrived (either not specified or determined by the moment of demand).

Loan repayment services

Reflection of offsets in tax accounting

- Income tax

Accounting for transactions of offsetting mutual claims when calculating corporate income tax depends on which method of accounting for income and expenses is used. If an organization uses the accrual method, then the offset will not affect the calculation of income tax in any way.

In this case, neither income nor expenses arise, since income and expenses are taken into account regardless of the fact of their payment (clause 1 of Article 271, clause 2 of Article 272 of the Tax Code of the Russian Federation). Under the cash method, income and expenses are taken into account upon repayment of debt, including through the offset of mutual claims (clause

2 tbsp. 273 of the Tax Code of the Russian Federation). That is, on the date of offset, the organization must reflect in tax accounting income in the amount of the offset debt of the counterparty and expenses in the amount of its debt to the counterparty, repaid by offset.

Offsetting under loan and service agreements

Thus, when offsetting mutual claims under loan agreements with a foreign counterparty, it should be taken into account that regulatory authorities may have claims of violation of the repatriation rule provided for by currency legislation, in which case they will have to defend their position in court. Add to Bookmarks Print The material presented in this article is provided for informational purposes only and may not be applicable to your particular situation and should not be taken as a guarantee of future results.

Settlement of mutual claims under loan agreements with a foreign counterparty

For simplifiers, the date of recognition of income is not only the day the money is received, but also the day the debt is repaid in another way. 1 tbsp. 346.17 Tax Code of the Russian Federation. Offsetting is that very different method. That is, on the basis of an act (agreement, application) of offset, you need to reflect income in the amount of the repaid debt of the counterparty.

At the same time, the goods (work, services) you purchased will be considered paid (also for the amount of the repaid debt), which means that one of the conditions for recognizing expenses under the “income-expenditure” simplified tax system is met. 2 tbsp. 346.17 Tax Code of the Russian Federation. Accounting. Income from the sale of goods (works, services) and expenses for their purchase should be reflected in your accounts as usual.

Repayment of obligations under a loan agreement through offset

An individual who is the founder of an LLC on the simplified tax system of 6% took out an interest-bearing loan at an interest rate above the key rate from the LLC. The loan was taken out for an individual, but for the purposes of use in business activities, interest was accrued and paid. Interest on the loan was included in the income of the LLC and was taxed. The same individual, as an individual entrepreneur under the simplified tax system of 6%, provided services to the LLC under an agreement concluded with him as an individual entrepreneur. Can this person repay his obligations under the loan agreement by offsetting the debt for services, the income from the individual entrepreneur will be taxed according to the simplified tax system. Will this method of extinguishing be interpreted as receiving additional income for an individual and subject to personal income tax in an LLC?

Answer

Yes, you can offset. But since the loan agreement in your case was concluded for an individual, let the individual entrepreneur send a letter to the organization about conducting an offset with him as an entrepreneur. Since the loan was taken for business. That is, in fact, the loan was received by a businessman, and not an individual.

The amount of interest paid by an individual entrepreneur on a loan is his expenses.

In addition, on the date of offset of the individual entrepreneur, income must be recognized. In the amount of the cost of services provided. This income will be taken into account when taxed under the simplified tax system of 6%. Since the offset is payment for the services provided by the individual entrepreneur. That is, income will need to be included in the tax base (clause 1 of article 346.15, clause 1 of article 346.17 of the Tax Code of the Russian Federation). The businessman must pay the tax on his own, not the organization for him.

As your question suggests, the interest on the loan agreement is higher than the key rate. This means that the citizen does not receive any material benefit. Therefore, the organization as a tax agent does not need to withhold personal income tax from the entrepreneur’s income. That is, the businessman does not have income subject to personal income tax (clauses 1 and 2 of Article 212 of the Tax Code of the Russian Federation).

You can find additional information about netting in the articles on our website:

Settlement of mutual claims: when and how to carry out

The courts consider it possible, for example, to set off claims for payment of the customer's debt for work performed and for payment of a penalty for the contractor's violation of deadlines for completing work, because, despite their different legal nature, these claims are monetary, that is, homogeneous. Resolution of the Presidium of the Supreme Arbitration Court of June 19, 2012 No. 1394 /12. In principle, the parties can agree to set off heterogeneous claims.

4 of the Resolution of the Plenum of the Supreme Arbitration Court dated March 14, 2014 No. 16, let’s say those when the debt of one party is expressed in rubles, and the other in foreign currency. But then the companies need to agree on the rate at which the foreign currency debt will be converted into rubles. Arrival of the deadline for fulfillment of obligations At the time of offset, the payment deadline for each claim under the contract must already have arrived. Especially for the site www.4dk-audit.ru One of the methods of settlements between organizations is the offset of mutual claims (Article 410 of the Civil Code of the Russian Federation). At the same time, the legislation does not provide for exceptions for any circle of persons who are parties to a transaction for offsetting mutual claims. It follows from this that mutual settlement can also be carried out with a foreign counterparty. However, it should be taken into account that offset is possible if the following conditions are simultaneously met: - organizations that intend to carry out offset must have counterclaims against each other; — counterclaims of organizations must be homogeneous; — deadline for fulfilling a counterclaim of the same type:

- has already arrived;

- was not specified in the contract;

- was determined by the moment of demand.

At the same time, there is no definition of a homogeneous requirement in civil legislation.

Naturally, income and expenses are taken into account for tax purposes, provided that they are accepted. Under the simplified tax system, income and expenses are determined using the cash method, so the date of repayment of debt through netting will be the date of recognition of both income and expense simultaneously (clause

Tax Code of the Russian Federation). In this case, it is necessary to take into account the rules for recognizing certain types of expenses under the simplified tax system. For example, expenses for the purchase of goods for further sale can be taken into account only after their actual sale (clause

2 p. 2 art. 346.17 Tax Code of the Russian Federation). If offset is carried out on the debt of counterparties for goods (work, services) supplied, then this will not affect the calculation of VAT in any way: the obligation to pay VAT arose at the time of shipment of goods (work, services), and the right to deduction is when the purchased goods are accepted for accounting (works, services).

5.3. Documentation of repayment of the loan amount

And the party whose debt was greater will have part of the obligation remaining unpaid. Settlement of obligations is possible only if the following conditions are met. Homogeneity of counter debts Claims are recognized as homogeneous when they have the same subject and can be compared. Let's say that monetary claims expressed in one currency are homogeneous. 7 Information letter of the Presidium of the Supreme Arbitration Court dated December 29, 2001 No. 65. For example, one party has a debt to pay for work performed, and the other has a debt to repay the loan, while each party owes the other money, which means that such obligations may be credited.

Settlement of loans and services

We will show you how you can fill out an application for offset using method 1. Stroy-Garant LLC 127204, Moscow, Dmitrovskoye sh., 157 tel. General Director of ProfAudit LLC Mayskaya V.P. 125315, Moscow, Leningradsky Ave., 68 Ref. No. 36 dated May 28, 2015 Application for offset of counterclaims Limited Liability Company "Stroy-Garant" represented by General Director S.L. Rukodelnikov, acting on the basis of the Charter, in accordance with Art. 410

The Civil Code of the Russian Federation declares a partial offset of counter homogeneous claims, the deadline for fulfillment of which has arrived. Information on counterclaims and debt of Stroy-Garant LLC and ProfAudit LLC as of May 28, 2015: Debt accepted for offset Number and date of the agreement, essence of the obligation Number and date of the primary document, invoice Amount of the obligation, rub .

Offsetting: important nuances

Author: Yu. A. Vasiliev , Doctor of Economics PhD, author of numerous publications on accounting and taxation

In the construction industry, counter-obligations often arise. The simplest example: when the general contractor has a debt to the subcontractor for work performed, and the subcontractor owes a debt to the general contractor for materials.

There is an opinion that it is easy to pay off debts by offset. Meanwhile, courts often analyze controversial situations and come to the conclusion that the debt is not repaid. As a result, the arbitrators satisfy demands for the recovery of not only the principal amount of the debt, but also the penalty (interest). What needs to be taken into account so that the debt is repaid not on paper, but in fact?

To terminate a homogeneous counterclaim by offset, an application from at least one of the parties is required.

Settlement is not carried out automatically, is not possible by default, counter obligations are terminated by agreement of the parties or at the request of one of them.

See also: Tax on debt of the Republic of Belarus

Paragraph 5 of the Information Letter of the Presidium of the Supreme Arbitration Court of the Russian Federation No. 65 states: the delivery of goods in itself does not lead to the termination of the previously incurred debt of the supplier to the recipient of this product according to the rules of Art. 410 of the Civil Code of the Russian Federation. To terminate a homogeneous counterclaim by offset, an application from at least one of the parties is required. This conclusion is illustrated by the following example.

Example 1.

The subcontractor went to court, demanding the collection of debt from the general contractor for work performed.

The general contractor believed that the debt did not exist, since, at the verbal request of the subcontractor, he shipped radiators to him in an amount equal to the cost of the work performed and accepted. Consequently, on the basis of Art. 410 of the Civil Code of the Russian Federation, his obligation to pay for the work of the subcontractor was terminated by a counter-delivery.

The arbitration court, having assessed the specific circumstances of the supply of radiators, found that the oral request of the subcontractor and the supply of radiators in this case did not lead to a novation of the parties’ previous obligations. The judges noted: to terminate an obligation by set-off, it is necessary not only to have counter-claims of the same type, the deadline for fulfillment of which has arrived, but also to have an application for set-off by at least one of the parties. Since the general contractor did not declare the offset of the monetary claim, the obligations of the parties were not terminated. As a result, the judges upheld the subcontractor's claim.

We add that if the parties admit the existence of counter-debts, they can enter into a settlement agreement. This can be done at any stage of the arbitration process and even during the execution of a judicial act (Article 139 of the Arbitration Procedure Code of the Russian Federation). For more details, see the consultation “Settlement agreement between the contractor and the customer of the work: law.”

After the subcontractor files a claim for payment for work, the general contractor is deprived of the right to offset unilaterally

If there are counter debts, it is important not only to declare a set-off, but also to do so in a timely manner. The fact is that after the counterparty applies to the court with a demand to collect the debt from your organization, you will not have the right to unilaterally declare an offset (and the presence in the agreement of a condition on making settlements by offsetting the claims does not change anything). In order to pay off a debt by offset, you will have to file a counterclaim, that is, the decision on offset will be made by judges after examining all the circumstances confirming the existence and size of counterdebts.

For information: the conclusion that after filing a claim, the defendant can terminate his obligation by offset only by filing a counterclaim is contained in paragraph 1 of the Information Letter of the Presidium of the Supreme Arbitration Court of the Russian Federation No. 65, Resolution of the Presidium of the Supreme Arbitration Court of the Russian Federation dated 02/07/2012 No. 12990/11 on the case No. A40-16725/2010-41-134, A40-29780/2010-49-263, Ruling of the RF Armed Forces dated 06/09/2015 No. 307-ES15-795 in case No. A13-2077/2014, etc.

Let us illustrate this with an example.

Example 2.

Two organizations (general contractor and subcontractor) entered into an agreement containing the following conditions. Payment for work is carried out by transferring funds by payment orders to the subcontractor's bank account within 30 calendar days from the date of signing the acceptance certificate. For violation of the deadlines for completing work and the deadlines for eliminating identified and properly recorded deficiencies, the subcontractor pays a penalty for each day of delay. If the subcontractor refuses to voluntarily pay the penalty, the general contractor has the right to reduce the amount payable for the work performed by the amount of the accrued penalty by sending the subcontractor a notice of offset of counterclaims in accordance with Art. 410 of the Civil Code of the Russian Federation.

The general contractor, citing poor quality work, did not pay for it in full - minus the unilaterally accrued penalty.

The subcontractor, believing such retention to be illegal, filed a claim with the arbitration court to collect the debt for unpaid work.

After studying the documents, the judges came to the conclusion that the work performed was accepted without any comments regarding volume and quality and was subject to payment.

The general contractor’s argument that, on the basis of Art. 410 of the Civil Code of the Russian Federation, the disputed debt was offset by him against the penalty not paid voluntarily, and was rejected by the arbitrators, who noted:

while withholding a penalty from the cost of work indicated in the acts, the general contractor did not send notifications of offset, as provided for in the contract;

these notices were handed to the subcontractor after he filed a claim against the general contractor for debt collection;

The general contractor did not submit a counterclaim to the court.

As a result, the arbitrators recovered the debt from the general contractor in the form of a penalty that had previously been withheld by him.

Moreover, the general contractor failed to prove the groundlessness of the court decision. Agreeing with this verdict, the Judicial Collegium for Economic Disputes of the Supreme Court of the Russian Federation also proceeded from the fact that after filing a claim, offset is possible only by filing a counterclaim, and not on the basis of a unilateral statement (see Determination dated 06/09/2015 No. 307-ES15-795 on case No. A13-2077/2014).

Let us add that in the described situation, in order to collect a penalty from the subcontractor, the general contractor will have to go to court with an independent claim and prove the validity of the accrual of the penalty. If notices of offset had been sent to the subcontractor in a timely manner, then in case of disagreement with the accrual of the penalty or its amount, the subcontractor would have to go to court and present the relevant evidence.

When sending a notice of offset, it is important to correctly indicate the address of the counterparty

As a general rule, in order to terminate the obligation by offset, the application for offset must be received by the relevant party (clause 4 of the Information Letter of the Presidium of the Supreme Arbitration Court of the Russian Federation No. 65, Ruling of the Supreme Arbitration Court of the Russian Federation dated June 15, 2015 No. 307-ES15-1559 in case No. A56-67385/2013). Otherwise, counter debts cannot be considered repaid, which gives the counterparty grounds to demand not only repayment of the debt, but also payment of a penalty or interest for the use of other people's funds.

Please note: the customer’s argument regarding the partial termination of his obligations to pay for services by offsetting similar counterclaims cannot be taken into account. The fact is that, within the meaning of Art. 410 of the Civil Code of the Russian Federation, only a document that contains a clear and unambiguous indication of the termination of the obligations of each party, the grounds for the occurrence of such obligations and their amount can be recognized as a statement of offset. In this case, in support of the offset application, the customer submitted a letter sent via Russian Post to an address that does not correspond to the location of the contractor indicated in the Unified State Register of Legal Entities . Thus, the application for offset does not comply with the norms of civil law (Resolution of the AS SZO dated May 18, 2017 in case No. A56-42838/2016).

At the same time, according to paragraph 3 of Art. 54 of the Civil Code of the Russian Federation, the Unified State Register of Legal Entities must indicate the address of the legal entity within the location of the legal entity. A legal entity bears the risk of the consequences of failure to receive legally significant messages delivered to the address specified in the Unified State Register of Legal Entities, as well as the risk of the absence of its body or representative at the specified address. Messages delivered to the address specified in the Unified State Register of Legal Entities are considered received by the legal entity, even if it is not located at the specified address .

In accordance with Art. 165.1 Civil Code of the Russian Federation:

statements, notices, notifications, demands or other legally significant messages with which the law or transaction associates civil consequences for another person, entail such consequences for that person from the moment the corresponding message is delivered to him or his representative;

a message is considered delivered even in cases where it was received by the person to whom it was sent (the addressee), but due to circumstances depending on him, it was not delivered to him or the addressee did not familiarize himself with it;

the listed rules apply unless otherwise provided by law or the terms of the transaction or follows from custom or practice established in the relationship between the parties.

Taking into account the above, if the notice of offset is sent to the legal address of the counterparty specified in the Unified State Register of Legal Entities, the obligations must be considered extinguished even when the counterparty did not receive the notice of offset (the letter was returned to the sender). An exception will be the situation when there is an agreement between the parties to send legally significant messages to a different address.

Please note: a similar position was expressed in the Ruling of the Supreme Court of the Russian Federation dated February 20, 2017 No. 305-ES16-20983 in case No. A40-113029/2015: the argument that the offset did not take place because the organization did not receive the corresponding notification must be rejected. The notice of offset was sent and received at the legal address of the LLC indicated in the Unified State Register of Legal Entities. In this case, the person to whom the message is sent to such an address bears the risk of the consequences of not receiving this message (clause 63 of the Resolution of the Plenum of the Armed Forces of the Russian Federation dated June 23, 2015 No. 25).

Offset terminates only those obligations whose due date has arrived.

By offsetting a counterclaim of the same type, only those obligations whose performance has become due can be terminated. An application for offset received before the deadline for fulfilling the obligation does not terminate the corresponding obligations, including after the specified deadline. This important nuance is explained in paragraph 18 of the Information Letter of the Presidium of the Supreme Arbitration Court of the Russian Federation No. 65 in relation to the following situation.

See also: Sale and purchase agreement 2021

Example 3.

A loan agreement was concluded between the two organizations. The borrower received the loan amount, but did not pay the interest due to the lender on time and did not repay the loan.

The lender went to court with a demand to recover the loan amount, interest for using the loan, as well as a penalty for a two-year delay in paying these amounts.

The borrower in court indicated the absence of debt, citing the fact that his obligations to repay the loan and interest were terminated by offset, a statement about which he made two years ago (the debt under the loan agreement was repaid by the lender's counter-debt to the borrower arising under the supply agreement).

The arbitrators pointed out: since the payment deadline under the supply agreement had not arrived at the time the lender received the offset application, the obligations of the parties could not be terminated by offsetting counterclaims. Consequently, the borrower is obliged to repay the loan amount and pay interest and the contractual penalty for two years of using the funds.

Let's consider another example that takes into account the specifics of construction activities.

Example 4.

The subcontractor performed his obligations under the contract in bad faith, and therefore the general contractor notified him of the cancellation of the contract and demanded the return of the unpaid advance payment.

In response, the subcontractor sent a letter about the offset of counter debts: the amount of the unpaid advance payment and the general contractor's debt in the form of the amount of the guarantee (reserve) retention (in relation to work performed on the basis of another subcontract agreement).

The general contractor went to court, demanding the return of the amount of the unpaid advance payment and payment of interest for the use of other people's funds (Article 395 of the Civil Code of the Russian Federation).

The court found that at the time of receipt of the subcontractor's notice of offset, the deadline for payment of the guarantee (backup) lien had not occurred. This circumstance allowed the arbitrators to make a decision in favor of the general contractor (the amount of the unearned advance payment and interest were collected from the subcontractor). The subcontractor's argument that the lien payment was due before the judgment was rendered was rejected as irrelevant (what is important is that the due date was before the date of receipt of the set-off notice).

The tenant has the right to offset the cost of inseparable improvements

Unless otherwise provided by the agreement, the tenant has the right, after termination of the lease agreement, to offset against rental payments the cost of inseparable improvements made with the consent of the lessor at his own expense (clause 8 of the Information Letter of the Presidium of the Supreme Arbitration Court of the Russian Federation No. 65). The rationale is as follows.

In accordance with paragraph 2 of Art. 623 of the Civil Code of the Russian Federation, the tenant has the right, after termination of the contract, to reimburse the cost of inseparable improvements made with the consent of the lessor, unless otherwise provided by the contract. Consequently, the landlord has a corresponding obligation (that is, the obligation to reimburse the cost of these improvements).

The right to reimbursement for the cost of such improvements, as well as the right to rental payments, is a monetary claim.

Clause 2 of Art. 623 of the Civil Code of the Russian Federation does not contain a requirement for the parties to conclude a separate agreement or for the presence of a judicial act on the recovery of amounts spent on inseparable improvements. Since Art. 623 of the Civil Code of the Russian Federation does not directly regulate these relations regarding the offset of counter-similar claims; the court is guided by the general provisions of civil legislation on offset (that is, Article 410 of the Civil Code of the Russian Federation). Therefore, the tenant has the right to set off and pay off counter debts: in the amount of rent and reimbursement of the cost of improvements.

If the statute of limitations has expired, the offset is void.

If an organization was unable to collect a debt from a partner in a timely manner, and then itself became his debtor under another agreement, it is tempting to declare offset of counterclaims. In fact, it turns out that you are covering your debt with a debt that no longer exists, which should have been written off when the statute of limitations expired. How such a test will most likely turn out is stated in paragraph 10 of the Information Letter of the Presidium of the Supreme Arbitration Court of the Russian Federation No. 65.

Note: If your partner does not notify you that set-off is impossible due to the expiration of the statute of limitations (and the law does not oblige him to do so), you will consider your debt discharged. And completely in vain! Subsequently, your counterparty will be able to claim from your organization not only the amount of debt, but also a penalty for failure to pay on time.

In accordance with Art. 411 of the Civil Code of the Russian Federation, offset of claims for which the statute of limitations has expired is not allowed. Civil legislation does not contain a requirement for the party that received the application for set-off to send a statement about missing the statute of limitations to the other party , since the limitation period is applied only by the court on a statement made when considering a dispute (clause 2 of Article 199 of the Civil Code of the Russian Federation).

Example 5.

The individual entrepreneur went to court with a demand to collect from the LLC the arrears of rent accrued on the basis of a lease agreement for construction equipment, as well as interest for the use of other people's funds.

The LLC in court indicated that there was no debt, since it was terminated by offsetting a counterclaim of the same type that it had arisen under another agreement with the individual entrepreneur.

The individual entrepreneur declared in court that the offset was null and void, since his debt to the LLC arose in 2012, and the LLC announced the offset only in 2017, that is, after the expiration of the three-year period.

The court of first instance refused to apply the limitation period to the individual entrepreneur, motivating its decision by the fact that the individual entrepreneur, after receiving the application for set-off, did not notify the LLC that the limitation period had passed.

The higher court overturned this decision and ordered the LLC to repay the debt in the amount of rent and pay the entrepreneur interest for the use of other people's money. At the same time, it was indicated that in relation to the LLC’s claim, on the basis of which the statement of offset was made, the statute of limitations had expired. The judges noted that the law does not contain a requirement for the party who received the set-off application to send a statement about the passage of the statute of limitations to the other party.

Loan from buyer - tax problem

A well-known situation: the seller entered into an agreement for the supply of goods, and then with the same buyer, even before shipment of the goods, enters into a loan agreement. The benefit is obvious: when receiving money under a loan agreement, the seller does not pay VAT. Next, the seller and buyer offset mutual claims. The seemingly safe VAT “optimization” scheme is fraught with a problem with the tax authorities...

We admit that there are indeed advantages to this scheme. The first is that the payment of VAT is deferred, while the money from the buyer, or rather the lender, has already been received. Secondly, when carrying out offsets, the seller does not need to transfer VAT in a separate payment, since operations for the provision of loans in cash, as well as the provision of financial services for the provision of loans in cash, are not subject to VAT (clause 15, clause 3, article 149 of the Tax Code of the Russian Federation) .

However, there is also a minus.

The tax authorities, having discovered that even before the shipment of the goods, the seller entered into a loan agreement with the buyer of this product, will not be able to ignore it. The tax authorities’ verdict will be simple: the conclusion of a loan agreement by the seller and buyer is a sham transaction.

What a sham transaction is is stated in paragraph 2 of Art. 170 Civil Code of the Russian Federation. A sham transaction is a transaction that is made to cover up another transaction and is not aimed at achieving the result that is the purpose of the transaction.

So, from the point of view of the inspectors, in this case the conclusion of a loan agreement by the seller and the buyer is a sham transaction covering up the fact that the seller has received advance payment for the upcoming delivery of goods. This means, tax officials believe, that the seller unlawfully failed to pay VAT on such an advance payment.

Let us immediately note that it is the tax authorities who must prove the sham of the transaction (Resolution of the Federal Antimonopoly Service of the North-Western District dated June 20, 2007 No. A05-8960/2006-19).

But as arbitration practice shows, they do not always succeed.

Judges, when making a decision in favor of the taxpayer, take into account that the tax authority did not prove that the funds received under loan agreements were not used by the company at its own discretion (for example, resolution of the Federal Antimonopoly Service of the North-Western District dated June 20, 2007 No. A05-8960/2006-19 ; Volga District dated 04/05/2006 No. A49-11667/2005-497A/17). That is, the judges emphasize, in this case it is not seen that the so-called advance payments preceded the supply of goods for the amount of the advance payments, and were not used by the taxpayer precisely as borrowed funds at his own discretion.

At the same time, the court did not see a direct temporary and quantitative connection between payments under the loan agreement and shipments of goods under supply contracts in the case it considered.

But tax officials are not giving up. Another complaint

on the part of the inspectors:

offset between the seller and the buyer cannot be made

, since in this case there is a novation.

The definition of innovation is given in paragraph 1 of Art. 414 of the Civil Code of the Russian Federation. Novation is when an obligation is terminated by an agreement of the parties to replace the original obligation that existed between them with another obligation between the same persons, providing for a different subject or method of performance.

In other words, in relation to this case, innovation is the replacement of the seller’s obligation to repay borrowed funds with an obligation to supply the goods to the buyer.

And the Ministry of Finance of Russia said that when concluding an agreement on the novation of a loan obligation into an obligation to supply goods, the borrowed funds received are considered as advance payments received on account of the upcoming supply of goods and are subject to inclusion in the VAT tax base in the tax period in which they received (letter of the Ministry of Finance of Russia dated September 7, 2005 No. 03-04-11/221).

That is, from the position of officials, with such an innovation, the funds received by the seller under the loan agreement must be included in the VAT tax base in the period of their receipt.

However, the judges do not agree that in the situation we are considering, the seller and buyer cannot set off.

Thus, in the resolution of the Federal Antimonopoly Service of the North-Western District dated August 12, 2003 No. A26-2338/02-02-08/58, the arbitrators indicated the following: “The inspector’s argument about the impossibility of applying offset was rightfully rejected by the court of first instance, since in this case there are two similar counterclaims: under the loan agreement - a requirement for the return of borrowed funds, and under an agreement for the provision of services - the company’s demand for payment of a commission for services rendered.”

Despite the arbitration practice that is favorable for the taxpayer, we note that the outcome of the case may not turn out in his favor if

:

— the seller regularly enters into a loan agreement after signing the supply agreement and subsequently carries out offsets;

— the amounts for which the loan agreement and the supply agreement were concluded are the same.

These circumstances may suggest that the seller has received an unjustified tax benefit. And if the tax inspectorate can prove this, then the courts are unlikely to support the taxpayer.

In IAS “Consulting. Standard" detailed information on concluding a loan agreement, loan repayment, as well as disputes under the loan agreement is set out in the "Loan Agreement" section.

Is it possible to return a loan in goods by arranging a mutual offset?

Questions and answers on the topic

Is it possible to return a loan in goods by arranging a mutual offset, and will the tax authorities, when repaying the borrowed amount, consider the loan itself to be an advance payment for this goods?

Yes, you can. You can complete this operation in one of the following ways:

- Conclude a compensation agreement in the form of transfer of goods;

- Sign an agreement on the novation of the contract - replacing the obligation under the supply contract with the obligation to supply goods;

- Offsetting counterclaims - by delivering goods under a separate contract with the registration of offset of claims between contracts.

See also: Minimum benefit amount for 1 child in 2020

The supplier of goods under the simplified tax system must recognize income from the sale of goods at the time of signing any of the above documents on the repayment of obligations.

In order to reclassify a loan agreement into a supply agreement on the date of signing the loan agreement, the tax authorities must prove that it initially contained the characteristics of a purchase and sale agreement and was concluded only for the purpose of transferring the tax base to a later period. If such signs are absent, then the inspectors have no reason to retroactively requalify the transaction.

From the recommendation of

Oleg Khoroshiy,

Head of the Department of Profit Taxation of Organizations of the Department of Tax and Customs Tariff Policy of the Ministry of Finance of Russia How to reflect the offset of mutual claims in taxation. The organization applies a special tax regime

Therefore, if, as a result of offset, the buyer’s receivables are repaid, then, regardless of the chosen object of taxation, the seller organization applying the simplification must recognize income (clause 1 of article 346.15, clause 1 of article 346.17 of the Tax Code of the Russian Federation).

For purchasing organizations that pay a single tax on the difference between income and expenses, offset is the basis for recognizing expenses in the form of repaid accounts payable (clause 1 of article 346.16, clauses 1, 2 of article 346.17 of the Tax Code of the Russian Federation). Accounts payable for certain types of expenses must be recognized taking into account the features characteristic of the items being written off. For example, the cost of goods purchased for further sale can be included in expenses only after they have been paid to the supplier, shipped, and received payment from the buyer (subclause 2, clause 2, article 346.17 of the Tax Code of the Russian Federation).

In case of partial offset of mutual claims, income (expenses) should be recognized: – on the date of offset (for the amount of debt subject to offset); – on the date of repayment of the balance of debt in another way (for example, in cash).