Hello, Vasily Zhdanov is here, in this article we will look at long-term liabilities on the balance sheet. All debts an organization has are reflected in the balance sheet in order to analyze the efficiency of the enterprise, develop a strategy for its development, correct errors in management and timely repayment of debts. Thus, borrowed funds can sometimes be repaid over ten to fifteen years, and in some cases the debt must be repaid no later than in a year. In the first case, long-term liabilities are recorded in the balance sheet, and in the second - short-term ones. The most favorable effect on the company's work is the attraction of long-term borrowed capital.

What are long-term liabilities on the balance sheet

Liabilities of an enterprise are debts existing at the reporting date that the company has incurred as a result of certain facts of its production activities, which will ultimately lead to the expenditure of assets to repay them. An economic entity may have obligations due to:

Take our proprietary course on choosing stocks on the stock market → training course

- business customs;

- legal norm;

- agreement.

Long-term liabilities mean debts to legal entities and individuals that must be repaid no earlier than 12 months from the reporting date . These may be, for example, estimated liabilities, deferred tax payments, and various types of debts.

It also happens that an organization attracts financing with a long repayment period, but part of the loan must be repaid in a fairly short time. Therefore, when financial experts look at existing long-term liabilities on a company's balance sheet to assess its financial condition, such debts are divided into 2 categories:

- The portion of long-term accounts payable that is due to be repaid within the next year, starting from the reporting date.

- The share of long-term accounts payable that will need to be repaid more than 1 year from the reporting date.

The procedure for generating indicators according to the lines of section V of the balance sheet liabilities

The organization’s liabilities (essentially its borrowed capital) are presented in two liability sections of the balance sheet, depending on their maturity date:

- in Sect. IV “Long-term liabilities” – liabilities whose maturity is more than 12 months after the reporting date;

in Sect. V “Short-term liabilities” – obligations that must be repaid within the next year.

Section V “Short-term liabilities” of the liabilities side of the balance sheet reflects information about short-term borrowed sources attracted by the organization.

In line 1510 “Borrowed funds” credit account 66 “Settlements on short-term loans and borrowings” is entered, as well as part of the amounts from the credit account 67 “Settlements on long-term loans and borrowings” (in the part subject to repayment within the next 12 months after the reporting date ).

On line 1520 “Accounts payable,” the organization needs to show the total amount of all types of short-term debt to other organizations and individuals, as well as to the state and extra-budgetary funds. To do this, add up the credit balances of the following accounts (in terms of short-term accounts payable):

Organizations have the right to independently determine the detail of indicators for reporting items.

Therefore, in principle, an organization can add decoding lines to detail the indicator on page 1520 “Accounts payable”.

For example, for separate presentation of information on short-term accounts payable to suppliers and contractors, to the organization’s personnel, to the budget for the payment of taxes and fees, as well as to extra-budgetary funds, if the organization recognizes such information as significant.

The organization must fill out page 1530 “Deferred income” of the balance sheet liability in cases where the accounting provisions provide for the recognition of this accounting object.

For example, commercial organizations here reflect the sum of the credit balances of accounts 98 “Deferred income” and 86 “Targeted financing”.

The fact is that in commercial organizations receiving budget funds, amounts of targeted financing aimed at acquiring non-current assets or inventories are taken into account as part of deferred income. The balances of targeted financing are also reflected within this category of accounting objects.

Line 1540 “Estimated liabilities” is intended to reflect the credit balance of the account (excluding amounts included in long-term liabilities).

Line 1550 “Other liabilities” reflects other types of short-term liabilities that are not included in the above lines.

For example, the amount of targeted financing received by developer organizations from investors and generating an obligation to transfer the constructed object to them within 12 months after the reporting date (in accounting they are taken into account in account 86 “Targeted financing”), or the amount of VAT accepted for deduction when transferring an advance (prepayments) and subject to restoration and payment to the budget upon actual receipt of goods, works, services or upon return of the transferred advance payment (prepayment), usually accounted for in account 76 “Settlements with various debtors and creditors”.

The total amount of lines 1510 - 1550 is reflected on line 1500 “Total for Section V”, which characterizes the total amount of short-term borrowed capital (liabilities) of the organization.

Still have questions about accounting and taxes? Ask them on the accounting forum.

Current liabilities: details for an accountant

- Filling out the balance sheet (f. 0503130) for 2021: what to pay attention to?

Accounting and reporting as a short-term liability; there is no unconditional right to defer repayment... months after the reporting date. Short-term liabilities also include the current share of long-term... - Public disclosure of reporting indicators

Accounting and reporting as a short-term obligation; c) the institution does not have an unconditional... - On the period of use and qualification of assets and liabilities

2010 No. 66n, long-term and short-term liabilities are separated into special sections for... in the reporting as long-term. Some current liabilities, such as trade payables... qualify these operating items as current liabilities even though they are subject to... long-term financial liabilities are defined as short-term liabilities not expected to be repaid within... if for loans that qualify as current liabilities when between the date ... - The procedure for filling out the balance sheet in a general form.

Example 66n is not provided. Section V. Short-term liabilities Borrowed funds. In line 1510…. Line 1550 shows other short-term liabilities that are not reflected in... 1410 - 1450. Section V “Short-term liabilities” Line 1510 “Borrowed... liabilities” = amounts of debt on short-term liabilities not taken into account when determining other... - Features of the presentation of financial statements in 2021

Months after the reporting date Short-term liabilities include (even if the maturity date is... months after the reporting date). Short-term liabilities also include the current share of long-term...

Each organization has assets and liabilities, which, in turn, are divided into long-term and current. If the former influence the development prospects of the company as a whole, then the latter influence the situation in the reporting period. Let's look at them in more detail.

The organization's resources that are directly involved in turnover and are capable of generating income for the company over a short period of time are called current assets. Since such resources are very mobile (as can be seen even from their name), they need to be given special attention in accounting. Moreover, current assets are a separate group in the company’s balance sheet, and the balance must be correctly indicated for all accounts that are included in it. Based on these data, the liquidity ratio is usually determined.

Long-term liabilities on the balance sheet (Section IV)

Important! Liabilities (short-term and long-term) on the balance sheet are always reflected in Liabilities.

In the balance sheet, information on all long-term liabilities of the enterprise can be found in section IV, which includes the following items:

- Borrowed funds (line 1410). These are loans and borrowings issued by a legal entity, interest on the use of funds and associated costs (fees for checking a loan agreement, paid consultations, commercial information, etc.).

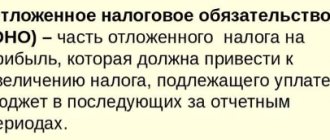

- Deferred tax liabilities (line 1420). This is the portion of the organization's deferred income tax, which will ultimately increase the income tax planned for transfer to the budget in the next reporting period or in later periods.

- Estimated liabilities (line 1430) . Debts of an enterprise that are planned to be repaid no earlier than in a year.

- Other obligations (line 1450) . All other debts that do not fall into any of the categories listed above.

Let's see what the mentioned section IV looks like:

Let’s look at Section IV “Long-term liabilities” line by line and see how each line of the balance sheet is filled out:

| Section IV line | Line formation order | Algorithm for calculating the indicator* *K_ – credit balance |

| 1410 "Borrowed funds" | Information on all obligations of the company taken for a long term (this is considered to be a period of time from 1 calendar year) must be reflected. Accounts payable can arise as a result of receiving a loan in cash or in kind, in the form of an obligation on a bill of exchange, or a bank loan. To form a line, you need to take the credit balance of account 67 only for debts with a long payment period. | K67 (long-term debts only) |

| 1420 “Deferred tax liabilities” | Filled out only by enterprises guided by PBU 18/02. The line is formed by indicating the credit balance of account 77. In cases where firms allow themselves to offset tax liabilities and assets and present them in a consolidated form, the line must be filled out only when the credit balance of account 77 > debit balance of account 09 (by the amount of the difference between these indicators). | K77 |

| 1430 “Estimated Liabilities” | The amount of reserves formed according to PBU 8/2010 for long-term liabilities is indicated. As an example, we can point out the reserves formed for warranty repairs. The line is created by reflecting in it the credit balance of account 96 (for debts with a repayment period of 1 year or more), which was not written off as of December 31 of the reporting period. | K96 (only estimated liabilities with a long period of fulfillment) |

| 1450 “Other obligations” | Contains information about debts to counterparties with a repayment period of 1 year. It is formed as the balance of the following accounts: – account 60 (debts to contractors and suppliers for previously received deferred payments and installment plans for payment for goods supplied, only for credit debts with a long repayment period); – account 62 (debts to customers and consumers for advances received, prepayments for future supplies of goods, commercial loans, only for long-term debts); – account 68 (accounts payable with a long repayment period that arose in connection with payments to the budget (taxes, fees), for example, upon receipt of installment plans and deferrals for federal tax collections, investment tax credit); – account 69 (debts of an enterprise for the payment of insurance premiums with a long repayment period, for example, arising due to the restructuring of debt to extra-budgetary funds); – account 76 (debts not included in other categories with a long repayment period); – account 86 (loan account 86 – targeted financing with a time period for fulfilling obligations of at least 1 year, for example, when a developer becomes obligated to transfer a finished project to investors after receiving targeted financing for construction). | K60+K62+K68+K69+K76+K86 (only long-term liabilities) |

| 1400 “Total for Section IV” | Amount of lines 1410-1450 (total liabilities of the company). |

The total for the “Long-term liabilities” section is calculated in accordance with the following formula:

Long-term liabilities: borrowed funds (line 1410)

Borrowed funds reflected in line 1410 of Section IV include all bank loans issued at the end of the reporting period for a period of 1 year or more, various loans, bonded and bill of exchange debts. Such debts accumulate in the account. 67.

The amount of the loan taken is reflected in accounting in the amount specified in the loan agreement, not exceeding the amount of finance actually taken. Such an agreement is recognized as concluded at the time of actual receipt of funds (or other assets) from the borrower.

Debt on loans and credits is shown on the balance sheet, taking into account interest on the use of funds accumulated at the end of the reporting period.

Important! In the case of receiving a credit (not a loan), the amount under the agreement is subject to reflection in the balance sheet as accounts payable, but taking into account the terms of the agreement. This is due to the fact that banks reserve the right not to issue funds (if such a condition is contained in the agreement), and that in the event of an unreasonable refusal to issue a loan, the bank will be obliged to pay compensation to the client.

Long-term liabilities: deferred tax liabilities (line 1420)

Reflected on account 77 by type of obligation. Accounting entries:

- DEBIT 68.4.2 CREDIT 77 (occurrence of deferred tax liabilities);

- DEBIT 77 CREDIT 68.4.2 (reduction of deferred non-refundable assets).

Deferred tax liabilities appear on the balance sheet because taxable temporary differences arise (in effect, they are deferred taxes that will subsequently increase income taxes payable). These are reflected in accounting taking into account all taxable differences, and such obligations are recognized precisely in the period during which they arose .

A temporary difference is income that forms profit (and expenses that form loss) within one reporting period, while the tax base is formed in another (other) periods.

Important! If a debt or an asset for which deferred tax liabilities were accrued is disposed of, the amount of IT is written off to the profit and loss accounts, which, according to the Tax Code, will not increase taxable profit.

Long-term liabilities: estimated liabilities (line 1430)

They are taken into account by accountants on account 96, recognized if 3 conditions are simultaneously met:

- The impossibility of avoiding the fulfillment of an obligation that arose earlier due to the implementation of economic activities.

- Probability of expense (reduction of economic benefits in order to fulfill an obligation).

- Possibility of a reasonable assessment of the amount of possible expenses (amount of obligation).

The listed conditions for accounting for estimated liabilities are not applicable in some cases. So, they are not taken into account when it comes to:

- amounts that are accounted for according to PBU 18/02 and affect the amount of income tax planned for transfer to the budget in the following periods or in later periods;

- valuation reserves;

- reserves that were formed from retained earnings; reserve capital;

- contracts under which at least one of the parties has not fulfilled its obligations in full as of the reporting date (with the exception of obviously unprofitable contracts, and an agreement under which a party can refuse to fulfill obligations unilaterally without any penalties is not recognized as such) .

Decoding the amount in lines 1410 and 1510

It is not difficult to decipher balance sheet lines 1410 and 1510. They include short-term and long-term borrowed funds, which are reflected in the balance sheet along with interest accrued on them. The enterprise's reporting must display the following information:

- Amounts and terms of repayment of newly acquired liabilities.

- Balances of outstanding debt on existing loans.

- Data on interest due to creditors.

- Information about additional expenses associated with servicing loan agreements.

- Information about securities issued and acquired by the company.

- Data on the effectiveness of investments made with borrowed funds in the formation of an enterprise asset.

Attention! Payment of remuneration to the lender for the use of borrowed funds can be taken into account as part of the investment asset, if such exists on the balance sheet.

Regulatory and legislative acts on the topic

| Order of the Ministry of Finance of Russia dated July 2, 2010 No. 66n | Approval of the balance sheet form |

| clause 7.3 of the Concept approved by the Methodological Council for Accounting under the Ministry of Finance | On the grounds for the emergence of obligations |

| clause 19 PBU 4/99 | Definition of long-term liabilities |

| Order of the Ministry of Finance of Russia dated October 31, 2000 No. 94n | Algorithm for calculating indicators of items of long-term liabilities |

Answers to frequently asked questions on “Long-term liabilities on the balance sheet”

Question: Is accounts payable reduced due to the accrual of value added tax on advances received by the enterprise?

Answer: Yes, accrued VAT on advances received by the company reduces the amount of accounts payable in the balance sheet on which the tax amount was calculated. In the same way, VAT on an advance issued by an organization is not reflected in the Liability side of the balance sheet, but reduces the amount of receivables in the Asset. Regarding your question, let's give an example: on the reporting date, an advance of 118 thousand rubles was received, including the amount of VAT at a rate of 18%, in Liability we will write (118 thousand rubles - 118 thousand rubles x 18/118) = 100 thousand. R.

Question: What to do with the assessment of deferred tax liabilities if the Tax Code of the Russian Federation provides for different income tax rates for certain types of company income?

Answer: In such a situation, the tax rate must correspond to the type of income that will lead to a decrease in the amount or complete repayment of the taxable temporary difference in future years (following the reporting or subsequent periods).