The simplified system is a special preferential regime, the declaration for which is submitted only once a year. Payment of the single tax on the simplified tax system also occurs once a year - no later than March 31 for an LLC and April 30 for an individual entrepreneur. However, these are not all the payments that the simplifier must transfer to the budget. At the end of each reporting period, if there is income, advance tax payments must be calculated and paid.

What are advance payments on the simplified tax system?

Let us repeat, the tax period for the simplified system is a calendar year, so the final payment to the state occurs at the end of the year. But in order for budget revenues to be uniform throughout the year, the Tax Code of the Russian Federation established the obligation of simplified taxpayers to pay tax in installments, based on the results of the reporting periods. In essence, this is how the budget is advanced using earlier revenues.

The reporting periods for calculating advance payments under the simplified tax system are the first quarter, half a year and nine months of the year. If a businessman received income during the reporting period, then within 25 days following it, he must calculate and pay 6% (for the simplified tax system Income) or 15% (for the simplified tax system Income minus expenses) of the tax base. If no income was received, then there is no need to pay anything.

Advance payments are called that way because the tax is paid as if in advance, in advance, without waiting for the end of the year. At the same time, all advance payments under the simplified tax system are taken into account in the declaration and accordingly reduce the total annual amount.

Prepare a simplified taxation system declaration online

For the convenience of paying taxes and insurance premiums, we recommend opening a current account. Moreover, now many banks offer favorable conditions for opening and maintaining a current account.

Fines provided for violation of tax payment deadlines for the annual reporting period

If the declaration is submitted on time, only penalties are charged for late payment of tax (as well as advance payments), there is no fine.

Delay is considered from the next day after the deadline for tax payment specified by law. Penalties are charged for each day of delay, including weekends and holidays. They stop accruing penalties on the day when a legal entity transfers money for paying taxes and penalty payments. It is noteworthy that penalties are also accrued for the day on which the payment was made.

For failure to submit a declaration, an organization or individual entrepreneur will be fined 5% of the unpaid tax for each full or partial overdue month (Article 119 of the Tax Code of the Russian Federation). In this case, the amount of the fine cannot be less than 1,000 rubles and more than 30% of the tax amount.

Additional liability is provided for officials: a fine of 300-500 rubles (Article 15.5 of the Code of Administrative Offenses of the Russian Federation).

If the delay in tax payment is less than 30 days, then penalties are calculated based on 1/300 of the Bank of Russia refinancing rate. If the period of delay is more than 30 days, the calculation is carried out based on the rate of 1/150, that is, doubled.

Deadlines for payment of advance payments

Please note - due to the coronavirus pandemic, for some individual entrepreneurs and organizations the deadlines for paying taxes and filing reports may be postponed, brief information in the summary table from the Federal Tax Service, details are described in this article.

Article 346.21 of the Tax Code of the Russian Federation establishes the deadlines for making advance payments under the simplified tax system in 2021. Taking into account the postponement due to weekends, these are the following dates:

- no later than April 26 for the first quarter;

- no later than July 26th for the half-year;

- no later than October 25th for nine months.

If these deadlines are violated, a penalty in the amount of 1/300 of the refinancing rate of the Central Bank of the Russian Federation is charged for each day of delay. There is no penalty for late payment of advances, because the deadline for paying the tax itself expires only on March 31 for an LLC and April 30 for an individual entrepreneur. But if you are late to pay the balance of tax before these dates, then a penalty of 20% of the unpaid amount will be imposed.

There is no need to submit any documents confirming the correctness of advance payments to the Federal Tax Service; simply reflect these amounts in KUDiR and keep the documents confirming payment. Information about these amounts based on the results of the reporting periods must also be indicated in the annual declaration.

Procedure and terms for payment of the simplified tax system in 2021

Tax according to the simplified tax system is paid 4 times a year. Organizations and individual entrepreneurs make three advance payments and one annual payment.

Throughout the year (no later than the 25th day of the month following the reporting period), advance payments for the simplified tax system are transferred.

According to the rule specified in clause 7 of Article 6.1 of the Tax Code of the Russian Federation, if the deadline for paying the simplified tax system coincides with a weekend or a holiday, a single tax or advance payment can be paid no later than on the next working day after the last one.

The article below shows the deadlines for paying tax under the simplified tax system 2021, taking into account holidays and weekends.

The reporting period for taxpayers of the simplified tax system is:

- quarter;

- half year;

- nine months of the calendar year;

- year.

For 2021, tax according to the simplified tax system must be paid in 2020:

- Individual entrepreneur - until April 30, 2021;

- organizations - until March 31, 2021.

For the reporting periods of 2021, tax according to the simplified tax system must be paid:

- for the first quarter of 2021 - April 27, 2021;

- for the first half of 2021 - July 27, 2021;

- for nine months of 2021 - October 26, 2021.

Reduction of tax on the amount of insurance premiums

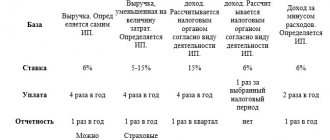

Insurance premiums that an individual entrepreneur pays for himself, as well as contributions for employees of organizations and individual entrepreneurs, reduce the calculated tax amounts. The order of reduction depends on which tax object is selected:

- on the simplified tax system for income, the calculated payment itself is reduced;

- on the simplified tax system Income minus Expenses, contributions paid are taken into account in expenses.

For individual entrepreneurs working on the simplified tax system of 6%, there is another important condition - the presence or absence of employees. If an individual entrepreneur has employees hired under an employment or civil contract, then tax payments can be reduced by no more than 50%. At the same time, to reduce the tax, insurance premiums paid both for yourself and for employees are taken into account.

If there are no employees, then payments to the budget can be reduced by the entire amount of contributions paid for oneself. With small income of an individual entrepreneur without employees, a situation may arise that there will be no tax to pay at all, it will be completely reduced due to contributions.

The simplified taxation system 6% and simplified taxation system 15% regimes are radically different in tax base, rate and calculation procedure. Let's look at examples of how to calculate an advance payment according to the simplified tax system for different tax objects.

Calculate the advance payment according to the simplified tax system

What are the deadlines for paying tax according to the simplified tax system for the year?

The simplified tax system is calculated on an accrual basis from the beginning of the year. At the end of each quarter, the advance tax payment must reach the budget no later than:

- 25th of April;

- July 25;

- the 25th of October.

The deadlines for paying the simplified tax system for the year (final payment) vary depending on the category of taxpayer:

- Legal entities must meet the deadline by March 31, 2021.

- Individual entrepreneurs must make the last payment for 2021 no later than 04/30/2021.

Both dates are working, so there will be no postponements.

The tax amount is calculated in the tax return submitted at the end of the year. If, based on its results, the amount of calculated and paid advances turns out to be greater than the amount of the final payment, then an overpayment of tax arises, which can either be returned or offset against future payments.

It is also impossible not to note one more feature of the simplified system. If the taxpayer has chosen the object “income minus expenses” and the amount of calculated tax for the year is less than 1% of total income, then he will have to pay the so-called minimum tax, which will be equal to this 1%. The deadlines for paying the minimum tax coincide with those established for the final payment.

ConsultantPlus experts explained in detail how to correctly calculate the simplified tax system. Full trial access to K+ is available for free. If you apply the simplified tax system “income”, this ready-made solution will help you, and if “income minus expenses” - then this material is for you.

All economic entities using the simplified tax system, without exception, do not need to be late in paying the single tax, because this may result in sanctions imposed by the tax authorities. We will find out further what such sanctions may be expressed in.

Calculation for simplified taxation system Income

Tax base, i.e. The amount on which the tax is calculated for the simplified tax system Income is the income received. No expenses under this regime reduce the tax base; tax is calculated on the received sales and non-sales income. But due to the contributions paid, the payment to the budget itself can be reduced.

As an example of calculations, let’s take an individual entrepreneur without employees, who received income in the amount of 954,420 rubles in 2021. Individual entrepreneurs' insurance premiums in 2021 consist of a fixed minimum amount of 40,874 rubles. plus 1% of income exceeding RUB 300,000. We count: 40,874 + (954,420 – 300,000 = 654,420) * 1% = 6,544) = 47,418 rubles.

Pay additional fees in the amount of 6,544 rubles. possible both in 2021 and after its end, until July 1, 2022. Our entrepreneur has paid all fees in 2021. Individual entrepreneurs paid insurance premiums for themselves every quarter in order to immediately be able to reduce payments to the budget:

- in the 1st quarter - 10,000 rubles;

- in the 2nd quarter - 10,000 rubles;

- in the 3rd quarter - 17,000 rubles;

- in the 4th quarter - 10,418 rubles.

| Month | Income per month | Reporting (tax) period | Income for the period on an accrual basis | Contributions of individual entrepreneurs for themselves on an accrual basis |

| January | 75 110 | First quarter | 168 260 | 10 000 |

| February | 69 870 | |||

| March | 23 280 | |||

| April | 117 200 | Half year | 425 860 | 20 000 |

| May | 114 000 | |||

| June | 26 400 | |||

| July | 220 450 | Nine month | 757 010 | 37 000 |

| August | 17 000 | |||

| September | 93 700 | |||

| October | 119 230 | Calendar year | 954 420 | 47 418 |

| November | 65 400 | |||

| December | 12 780 |

An important condition: we count the income and contributions of individual entrepreneurs for themselves not separately for each quarter, but as a cumulative total, i.e. year to date. This rule is established by Article 346.21 of the Tax Code of the Russian Federation.

Let's see how to calculate an advance payment under the simplified tax system Income based on these data:

- For the first quarter: 168,260 * 6% = 10,096 minus paid contributions of 10,000, 96 rubles remain to be paid. Payment deadline is no later than April 26th.

- For half a year we get 425,860 * 6% = 25,552 rubles. We subtract the contributions for the half-year and the advance for the first quarter: 25,552 – 20,000 – 96 = 5,456 rubles. You will have to pay extra no later than July 26th.

- For nine months, the calculated tax will be 757,010 * 6% = 45,421 rubles. We reduce by all paid fees and advances: 45,421 – 37,000 – 96 – 5,456 = 2,869 rubles. They must be transferred to the budget no later than October 25th.

- At the end of the year, we calculate how much the entrepreneur must pay extra no later than April 30: 954,420 * 6% = 57,265 – 47,418 – 96 – 5,456 – 2,869 = 1,426 rubles.

As we can see, thanks to the ability to take into account insurance payments for oneself, the tax burden of individual entrepreneurs on the simplified tax system Income in this example amounted to only 9,847 (96 + 5,456 + 2,869 + 1,426) rubles, although the calculated single tax is equal to 57,265 rubles.

Let us remind you that only entrepreneurs who do not use hired labor have this opportunity, and individual entrepreneurs have the right to reduce the tax by no more than half. As for LLCs, the organization is recognized as an employer immediately after registration, so legal entities also reduce payments to the treasury by no more than 50%.

Calculation for simplified taxation system Income minus Expenses

In this mode, contributions can only be taken into account as part of other expenses, i.e. The calculated advance payment itself cannot be reduced. Let’s figure out how to calculate an advance payment under the simplified tax system with the tax object “income reduced by the amount of expenses.”

For example, let’s take the same entrepreneur without employees, but now we will indicate the expenses incurred by him in the process of activity. Contributions are already included in general expenses, so we will not list them separately.

| Month | Income per month | Reporting (tax) period | Income for the period on an accrual basis | Cumulative expenses for the period |

| January | 75 110 | First quarter | 168 260 | 108 500 |

| February | 69 870 | |||

| March | 23 280 | |||

| April | 117 200 | Half year | 425 860 | 276 300 |

| May | 114 000 | |||

| June | 26 400 | |||

| July | 220 450 | Nine month | 757 010 | 497 650 |

| August | 17 000 | |||

| September | 93 700 | |||

| October | 119 230 | Calendar year | 954 420 | 683 800 |

| November | 65 400 | |||

| December | 12 780 |

The standard rate for the simplified tax system Income minus Expenses for 2021 is 15%, let’s take it for calculation.

- For the first quarter: (168,260 – 108,500) * 15% = 8,964 rubles. Payment must be made no later than April 26th.

- For half a year: (425,860 – 276,300) * 15% = 22,434 rubles. We subtract the advance payment paid for the first quarter (22,434 - 8,964), we find that 13,470 rubles will remain to be paid no later than July 26th.

- For nine months, the calculated tax will be (757,010 – 497,650) * 15% = 38,904 rubles. We reduce by advances for the first quarter and half of the year: 38,904 – 8,964 – 13,470 = 16,470 rubles. They must be transferred to the budget no later than October 25th.

- Based on the results of the year, we calculate how much more must be paid no later than April 30: (954,420 – 683,800) * 15% = 40,593 minus all advances paid 38,904, we get 1,689 rubles.

Now we check whether there is an obligation to pay the minimum tax, i.e. 1% of all income received: 954,420 * 1% = 9,542 rubles. In our case, we paid more into the budget, so everything is in order.

Let's compare whose financial burden was higher:

- at the simplified rate of 6%, the entrepreneur paid 9,847 (tax) plus 47,418 (contributions), a total of 57,265 rubles.

- at the simplified 15% tax rate was 40,593 rubles plus 47,418 (contributions), a total of 88,011 rubles.

In this case, the load on the simplified tax system Revenues minus expenses turned out to be higher, although the share of expenses in revenue is quite high (71.65%). If the share of expenses turns out to be even lower, then the simplified tax system of 15% becomes completely unprofitable.

Before choosing a tax regime, we recommend that you receive a free consultation from 1C:BO, where they will help you choose the best option for you.

Free tax consultation

KBK for payment documents

KBK is a budget classification code that is indicated on receipts or bank documents for tax payment. The BCC of advance payments for the simplified system is the same as for the single tax itself. In 2021, the budget classification codes approved by Order of the Ministry of Finance of Russia dated November 29, 2019 N 207n (as amended on October 22, 2020) are in effect.

If you indicate an incorrect BCC, the tax will be considered paid, because Article 45 of the Tax Code of the Russian Federation indicates only two significant errors in the payment document:

- incorrect name of the recipient's bank;

- incorrect Federal Treasury account.

However, paying with an incorrect classification code will result in an incorrect distribution of the amounts paid, which will result in you being in arrears. In the future, you will have to search for the payment and communicate with the Federal Tax Service, so be careful when filling out the details.

- KBK simplified tax system 6% (tax, arrears and debt) – 182 1 0500 110;

- KBK simplified tax system 15% (tax, arrears and debt, as well as minimum tax) – 182 1 05 01021 01 1000 110.