Civil Code of the Russian Federation part 2

Article 706. General contractor and subcontractor

If the law or the contract does not provide for the contractor’s obligation to perform the work provided for in the contract personally, the contractor has the right to involve other persons (subcontractors) in the performance of his obligations. In this case, the contractor acts as a general contractor.

A contractor who has engaged a subcontractor to perform a work contract in violation of the provisions of paragraph 1 of this article or the contract shall be liable to the customer for losses caused by the subcontractor’s participation in the execution of the contract.

The general contractor is responsible to the customer for the consequences of non-fulfillment or improper fulfillment of obligations by the subcontractor in accordance with the rules of paragraph 1 of Article 313 and Article 403 of this Code, and to the subcontractor is responsible for the non-fulfillment or improper fulfillment by the customer of obligations under the work contract. Unless otherwise provided by law or contract, the customer and the subcontractor do not have the right to make claims against each other related to the violation of contracts concluded by each of them with the general contractor.

Article 780. Execution of a contract for paid services

Unless otherwise provided by the contract for the provision of paid services, the contractor is obliged to provide the services personally.

Article 801. Transport expedition agreement

Under a transport expedition agreement, one party (the forwarder) undertakes, for a fee and at the expense of the other party (the client - the shipper or consignee), to perform or organize the performance of services related to the transportation of goods specified in the forwarding agreement. A transport expedition agreement may provide for the forwarder’s obligations to organize the transportation of cargo by transport and along the route chosen by the forwarder or the client, the forwarder’s obligation to conclude on behalf of the client or on his own behalf an agreement (agreements) for the carriage of goods, to ensure the sending and receipt of cargo, as well as other obligations related with transportation. As additional services, the transport expedition contract may provide for the implementation of operations necessary for the delivery of cargo, such as obtaining documents required for export or import, performing customs and other formalities, checking the quantity and condition of cargo, loading and unloading it, paying duties, fees and others. expenses imposed on the client, storing the cargo, receiving it at the destination, as well as performing other operations and services provided for by the contract.

The rules of this chapter also apply to cases when, in accordance with the contract, the duties of the forwarder are performed by the carrier.

Vladislav Volkov answers:

Deputy Head of the Department of Taxation of Personal Income and Administration of Insurance Contributions of the Federal Tax Service of Russia

“Inspectors will compare the income of individuals in 6-NDFL with the amount of payments calculated for insurance premiums. Inspectors will begin to apply this control ratio starting with reporting for the first quarter. All control ratios for checking 6-NDFL are given in. For instructions and samples of filling out 6-NDFL for the first quarter, see the recommendations.”

Services are the same object of civil rights as things, and they can be freely alienated by one person to another person (Articles 128, 129 of the Civil Code of the Russian Federation). We will tell you in our consultation what entries need to be made in accounting when providing services.

VAT when re-invoicing expenses (Misnikovich L.)

The company is an intermediary for the sale of goods and is a VAT payer. NK KTZ issued invoices for the railway tariff (VAT 0%) for the month of March. The company wants to re-list them to the purchasing company. Is it necessary to increase VAT + 12% or re-invoice from 0%? Forwarder - Russia issued a 0% s/f for the provision of railway cars and technical equipment for international transportation. How can these costs be re-invoiced to the purchasing company - 0% or +12% VAT? This method of rebilling transportation costs is the most common, although it is quite labor-intensive in terms of its documentary maintenance.

In the supplier's accounting, operations for organizing the delivery of goods are reflected in the same way as during intermediation, only the supplier has no grounds for re-issuing invoices to the buyer for the cost of transport services. The absence of an invoice will create problems for the buyer if he wants to deduct VAT from the cost of transport services reimbursed to the supplier (clause 1 of Article 172 of the Tax Code of the Russian Federation).

Question: ...The supplier re-invoices the costs of payment for transport services for the delivery of goods by a third party to the buyer. Is it necessary to issue an invoice to the buyer for VAT purposes?

In this case, the increase in the supplier's document flow occurs due to the preparation of invoices for the delivery of goods, reissued to the buyer on the basis of invoices of involved carriers, as well as a log of received and issued invoices, which are required to be maintained by intermediaries carrying out transactions on their own behalf (see clause 3.1 of Article 169 of the Tax Code of the Russian Federation).

But, you can once again attach a certified copy of the TTN to the act. In this case, again, depending on what is provided for in the Agreement between the Supplier and the Buyer.

Options for organizing and paying for delivery The scheme of the relationship between the buyer and the seller in terms of organizing the transportation (delivery) of the purchased goods is usually stated directly in the purchase and sale or delivery agreement. Although it is also possible to conclude contracts separately for the goods themselves and for their transportation.

For transport services, we provide the buyer with a bill of lading on our behalf, generated on the basis of primary documents from the carrier organization. Don't forget to attach a copy of the carrier's bill of lading to it.

Alternative option

If you don’t want to enter into a mediation agreement, but re-issuing invoices seems too complicated and troublesome, you can formalize the relationship in a different way.

Current civil legislation does not prohibit the parties from independently determining the principles for determining the price of goods in a sales or supply agreement. In particular, the contract may provide that the price of the product is subject to change depending on the indicators that determine the price of the product (cost, expenses, etc.) (Clause 3 of Article 485 of the Civil Code of the Russian Federation).

In such a situation, it also makes sense to prescribe a specific method for revising the price.

This means that it is quite acceptable to stipulate in the contract that the price of the product consists of two parts. The first is a constant part corresponding to the “basic” price of the product, determined based on the delivery condition “ex-supplier warehouse” (i.e., on a pickup basis). The second is the variable part, which is calculated based on the costs of transporting goods to the place specified by the buyer (based on the tariffs of third-party carriers, taking into account distance and other factors).

In this case, both parts of the price will form a single final price, which will determine the full cost of the goods sold, that is, the proceeds from its sale.

With this scheme, it turns out that, on the one hand, the buyer actually compensates the seller for the real costs of transporting the goods, but, on the other hand, the entire amount paid is the price (cost) of the goods, and therefore there is no question of any “intermediary” services at all .

That is, accounting and taxation will be carried out in exactly the same way as in the case when the supplier organizes the delivery of goods to the buyer at his own expense, including transport costs in the final price of the goods.

In other words:

- at the supplier, the entire amount presented to the buyer is recognized as “single” revenue from the sale of goods in both accounting and tax accounting;

- the buyer is issued one invoice (for goods sold), in which transport services are not even mentioned, while the price of each product, naturally, is formed taking into account the cost of transport costs included in the variable part;

- VAT in the invoice is allocated as a single amount - from the full cost of the goods (which includes transportation costs);

- the buyer can easily submit this entire amount for deduction based on this invoice;

- Within the framework of this scheme, the carrier issues an invoice to the supplier for transport services, as well as a certificate of provision of transport services. Based on these documents, the supplier calmly assigns the cost of transport services to his business expenses (account 44 “Sales expenses”) and claims “input” VAT on transport services for deduction, thereby reducing the amount of VAT that was charged to the buyer.

Method 2. Changing the cost of the product

This type of re-invoicing of transport costs is not common in practice, but it is simpler in terms of documentation compared to the first.

- Agreement

Clause 3 Art. 485 of the Civil Code of the Russian Federation provides that in the sales contract it is possible to include a clause on changing the value of the goods upon the occurrence of certain circumstances. Alternatively, you can add a condition: if the delivery of the goods to the buyer is organized by the supplier, then the cost of the goods increases by the cost of transporting the goods to the buyer.

- Source documents

At the time of transfer of the goods to the carrier organization, you will already have an agreement on the provision of transport services and an invoice for payment for these services. Using these documents, we determine the amount of transportation costs (including VAT) and add it to the cost of the goods shipped to the buyer. We indicate the amount received in the delivery note. If several types of goods are shipped, then we distribute transportation costs between them in equal shares.

You can familiarize yourself with the form of the consignment note in the article “Unified form TORG-12 - form and sample” .

IMPORTANT! Do not include the cost of transport services as a separate line in the invoice. You do not provide services for the transportation of goods, therefore such a service should not be included in the invoices you issue.

If the cost of transport services changes after the buyer receives the invoice, adjustments are made to it in one of two ways:

- registration of a new adjusted invoice;

- making corrections to already completed 2 copies of the invoice: yours and the buyer’s.

Read about changes to primary documents in this material.

The invoice received from the carrier organization will be considered the basis for reflecting expenses associated with the sale of goods (subclause 1, clause 1, article 253 of the Tax Code of the Russian Federation).

- Invoice

We issue an invoice for the amount indicated in the delivery note: the cost of the goods, increased by the cost of transport services. We record it in the sales book. If the cost of transport services included in the price of the goods changes, we generate an adjustment invoice for the amount of the increase (decrease) in transport costs (paragraph 3, clause 1, article 169 of the Tax Code of the Russian Federation). There is no need to correct the old invoice.

For an example of filling out adjustment invoices, see the article “Sample of filling out an adjustment invoice (2019 - 2020)”.

We register the invoice received from the carrier organization in the purchase book.

Re-invoicing of transport services to the buyer without VAT posting

Intellectual property

VAT when re-invoicing expenses (Misnikovich L.)

606 of the Civil Code, under a lease agreement, the lessor undertakes to provide the tenant with property for a fee for temporary possession and use or for temporary use. The tenant is obliged to maintain the property in good condition, carry out routine repairs at his own expense and bear the costs of maintaining the property, unless otherwise provided by law or the lease agreement (clause

2 tbsp. 616 of the Civil Code of the Russian Federation). The costs of maintaining the rented premises include, in particular, electricity costs. Based on clause 1 of Art.

539 of the Civil Code, under an energy supply agreement, the energy supplying organization undertakes to supply energy to the subscriber (consumer) through the connected network, and the subscriber undertakes to pay for the received energy, as well as to comply with the regime of its consumption stipulated in the agreement, to ensure the safe operation of the energy networks under its control and the serviceability of those used

Re-billing of transport services

The trade organization in this case acts as an intermediary between the carrier and the buyer, who bears the burden of the costs of transporting the products.

The tax base for VAT for intermediary agreements is income in the form of remuneration. Since the final buyer is reimbursed for the amount of the transportation tariff, the organization’s tax base will be zero.

At the same time, re-invoicing services for the transportation of goods to the final buyer without an appropriate condition in the supply contract and not reflecting the VAT amounts invoiced by the supplier of goods and the organization itself to the end buyer will most likely be met with skepticism by fiscal officials, since re-invoicing of services is not provided for by law. Therefore, they recommend including the transportation tariff billed to the end buyer in the VAT base, and deducting the VAT paid to the carrier in the manner established by Articles 171 and 172 of the Tax Code of the Russian Federation.

Transportation costs in accounting: entries and examples

VAT - RUB 81,000.00 Transport costs amounted to RUB 29,500.00, VAT RUB 4,500.00.

Description of the transaction for the transaction Basis document 15 60 450 000.00 The purchase price of the purchased equipment is taken into account Bill of lading (TORG-12), Invoice received 19 60 81 000.00 VAT on the purchased equipment is taken into account 15 60 25 000.00 The cost of transportation costs is taken into account 19 60 4,500.00 VAT on transport costs is taken into account 41 15,475,000.00 The actual cost of purchased equipment is taken into account. VESNA LLC purchased goods for a total amount of RUB 413,000.00, incl.

All about VAT payer invoice and re-invoicing of services

Consequently, not 1.53 million rubles are paid to the budget, but 460 thousand rubles.

This can be a simplification, imputation or unified agricultural tax.

Typically, the choice in favor of one of the preferential regimes without VAT is due to the desire to reduce the tax burden and time costs for maintaining accounting records.

What are the disadvantages for the counterparty? On the one hand, when purchasing goods from a company under a special regime, an organization using OSNO can take into account the entire amount of costs when calculating income tax.

But on the other hand, she will not be able to receive VAT compensation in the future for the amount of the purchase from the budget.

For example, a company bought air conditioners for the office for 100,000 rubles.

Rebilling shipping costs to the buyer

Don't forget to attach a copy of the carrier's bill of lading to it.

We record the invoices received from the carrier organization in the journal of received and issued invoices (clause

3 of the Decree of the Government of the Russian Federation “On filling out documents for VAT calculations” dated December 26, 2011 No. 1137), we register in the invoice journal;

How to rebill transport services to another organization

It is necessary to make a note about the amount for transportation services.

In this case, the cost of the goods including VAT is indicated, the total amount payable from the buyer is calculated and the amount of transportation is indicated.

You can also make a note for the buyer that if the product is returned, shipping costs will not be refunded. Failure to allocate the amount of transport services in a separate line can result in the following troubles:

- The tax office will not count this amount as a deduction when calculating income tax.

- if the buyer returns the products, he will have to return the entire amount back, including delivery costs;

The best option would be to conclude a separate contract/agreement for the transportation of sold goods.

It specifies all the supplier's costs and the buyer's obligation to reimburse.

How to reflect the re-invoicing of transportation costs in transactions?

After we have dealt with the documentation of the re-billing of transport services to the buyer, we will consider the reflection of these operations in postings using a clear example.

Example

- The seller sold goods to the buyer in the amount of 895,420 rubles. (including VAT RUB 149,236.67).

- The purchase price of the goods is 762,710 rubles. (including VAT RUB 127,118.33).

- The cost of delivery of goods by the carrier under agreement with the seller amounted to 26,630 rubles. (including VAT RUB 4,438.33).

NOTE: with method No. 1, the intermediary seller reissues the delivery note and invoice for the cost of delivery (the sale of goods is not reflected in the intermediary’s accounting); With method No. 2, the shipping cost increases the cost of the product.

- The cost of intermediary services, reflected in method No. 1, is RUB 1,200.00. (including VAT 200 rub.).

- The costs of transporting the goods are reimbursed by the buyer.

| Operation | Method 1. Intermediary services | Method 2. Change in product cost | ||||

| Dt | CT | Sum | Dt | CT | Sum | |

| Product purchased by seller | 41 | 60 | 635 591,67 | 41 | 60 | 635 591,67 |

| 19 | 60 | 127 118,33 | 19 | 60 | 127 118,33 | |

| 68 | 19 | 127 118,33 | 68 | 19 | 127 118,33 | |

| Item sold to buyer | 62 | 90-1 | 895 420,00 | 62 | 90-1 | 922 050 = 895 420 + 26 630 |

| 90-3 | 68 | 149 236,67 | 90-3 | 68 | 153 675 = 149 236,67 + 4438,33 | |

| The costs of transporting the goods to the buyer are reflected (included in the price of the goods) | – | – | – | 41 | 76 | 22 191,67 |

| 19 | 76 | 4438,33 | ||||

| 68 | 19 | 4438,33 | ||||

| The cost of goods sold is written off | 90-2 | 41 | 635 591,67 | 90-2 | 41 | 657 783,34 = 635 591,67 + 22 191,67 |

| Reflected intermediary remuneration for transport services | 76 | 91-1 | 1 200,00 | – | – | – |

| 91-3 | 68 | 200,00 | ||||

| The results at the end of the month are reflected | 90-9 | 99 | 110 591,66 = 895 420 – 149 236,67 – 635 591,67 | 90-9 | 99 | 110 591,66 = 922 050 – 153 675 – 635 591,67 – 22 191,67 |

| 91-9 | 99 | 1 000,00 = 1 200,00 – 200,00 | ||||

| Profit tax accrued | 99 | 68 | 22 318 = (110 591,66 + 1 000,00) ×20% | 99 | 68 | 22 118 = 110 591,66 ×20% |

| VAT paid | 68 | 51 | 22 318 = 149 236,67 + 200,00 – 127 118,33 | 68 | 51 | 22 118 = 153 675 – 127 118,33 – 4438,33 |

You can learn more about the accounting of intermediary transactions in our article “Features of an agency agreement in accounting.”

Read about the specifics of taxation of transport services in the article “What is the procedure for assessing VAT on transport services?”

As can be seen from the example discussed above, method No. 2 is beneficial not only from the point of view of simpler documentation, but also as one in which the tax burden is lower - in this case, you do not need to pay taxes on income in the form of remuneration for intermediary.

Transport wiring services

If a commercial company delivers goods to the buyer using its own transport, then the delivery cost is included in the sales cost structure, i.e. expenses associated with operating the car will be accumulated in the account. 44 and increase the cost of the goods. The entries in the company's accounting will be as follows:

| Operation | D/t | K/t |

| Depreciation calculation for vehicles | ||

| Write-off of fuels and lubricants, auto parts | ||

| Driver salary calculation | ||

| Calculation of insurance premiums to funds | ||

| Write-off of vehicle operating costs |

When transporting goods, a mandatory accompanying document is a waybill for the vehicle, and the goods are indicated in the waybill.

A manufacturing company produced a batch of products - 100 units at a cost of 2,000 rubles. An agreement has been concluded with the buyer for the delivery of this consignment using the seller’s transport. The selling price of one product is 3,600 rubles. It is necessary to include in the selling price of a unit of goods transport costs totaling 19,580 rubles, which includes costs for:

- Fuel and lubricants – 8000 rub.;

- Vehicle depreciation – RUB 3,000;

- Driver’s salary – 6600 rubles;

- Contributions to funds (6600 x 30%) – 1980 rubles.

The accountant will distribute these costs by postings:

| Operation | D/t | K/t | Sum |

| Payment for fuel and lubricants | |||

| Vehicle wear and tear | |||

| Driver wages | |||

| Insurance premiums | |||

| Delivery costs are written off to cost of sales along with other sales costs. | 19 580 |

The cost of transport services will increase the selling price of a consignment of goods to 379,580 rubles. (3600 x 100 + 19,580), and the price of each product will be 3795.8 rubles. (3795.8/100).

In the accounting of the seller company delivering the goods, the cost of transportation is included in the cost of the goods and is taken into account in the amount of direct costs of producing the goods.

Accounting in a transport company

The provision of transportation services - passenger and cargo, carried out on vehicles owned or leased by the company, in specialized transport companies is a separate type of activity. The formation of the cost of transportation here will not be an integral part of the sales process, therefore it is carried out on production accounts:

- Account 20, generating costs directly related to the transportation process;

- Account 26, which combines the company's management costs.

In the accounting of a specialized logistics enterprise, transport services are accompanied by the following entries:

| Operation | D/t | K/t |

| Revenue from the provision of services | ||

| VAT | ||

| Costs associated with delivery: | ||

| - straight | 02, 05, 10, 60, 68, 69, 70, 71, 76 | |

| - indirect | 02, 05, 10, 60, 68, 69, 70, 71, 76 | |

| Write-off of expenses | 20, 26 |

The provision of transport services is formalized by an agreement, which specifies the cost of transportation, and may also include additional services that are within the competence of the forwarder or provide for the involvement of third-party performers (loading/unloading).

Example: accounting in a transport company

under an agreement with Krona LLC, it transports equipment worth 550,000 rubles. The cost of the transportation service was 118,000 rubles. in view of VAT. The total amount of services includes the actual transportation and forwarding support of the cargo; their cost was 56,000 rubles. The following entries are generated in the accounting of AUTO LLC:

| Operation | D/t | K/t | Sum |

| The equipment has been accepted for storage | 550 000 | ||

| Payment for services according to the contract | 118 000 | ||

| Revenue | 118 000 | ||

| VAT charged on the service | 18 000 | ||

| Delivery costs included the following: | |||

| Vehicle depreciation | |||

| fuels and lubricants | 24 000 | ||

| Driver/forwarder salary | 12 000 | ||

| Insurance premiums from salary | |||

| Travel expenses | 10 400 | ||

| Process management costs | |||

| Costs included in results | 20, 26 | 56 000 | |

| Upon delivery of the cargo, the equipment is removed from storage | 550 000 | ||

| The financial result from transportation was derived (118,000 – 18,000 – 2000 – 24,000 – 12,000 – 3600 – 10,400 – 4000) | 44 000 |

At the end of the month, when production accounts are closed, the amounts accumulated on accounts 20 and 26 are written off to the cost of transportation. In companies with an extensive cost formation system, accounts for service and auxiliary production can be used in accounting for transport services (23, 29).

Accounting for goods for resale: postings in a trading company

One of the most common options for accounting for goods in retail is their accounting at the sales price, i.e. using an account. 42, which accumulates the amount of trade margin (the difference between the purchase and sales price), which forms the organization’s profit. The accounting entries for the resale of goods will be as follows:

| Inventory purchased for resale |

| VAT allocated for them |

| The cost of inventory items increased by the amount of expenses for their acquisition |

| Trade margin reflected |

| VAT on goods sold |

| The purchase price of goods sold is written off |

| Trade markup taken into account |

| Selling expenses included |

| The result of the sale is reflected |

In wholesale trade enterprises, accounting for goods sold is carried out without using a trade markup account; the result of the sale is formed directly on account 90.

Requirements for the vehicle when loading

The completion of re-invoiced services is reflected by the receipt/expense of the amount excluding VAT on one of the accounts for settlements with counterparties. Is it possible to detail the terms of the price of a transport expedition agreement, highlighting the amounts of all expenses (the forwarder’s client insists on this)?

That is, accounting and taxation will be carried out in exactly the same way as in the case when the supplier organizes the delivery of goods to the buyer at his own expense, including transport costs in the final price of the goods. How to correctly calculate VAT in one of the special cases arising during the transportation of goods is described in the commented Letter of the Ministry of Finance of Russia dated August 15, 2012 N 03-07-11/299.

Postings for rebilling services to the customer

The debit of the account indicates the expense account, and the credit of account 60 shows subaccount 01, which in the accounting chart of accounts is called “Settlements with suppliers and contractors.”

When receiving (receiving) different services, the same accounting account is not always indicated by debit; the following postings for services are generated, for example:

- For transport costs, the accounting account may be different, it could be:

- Account 26, when receiving office supplies for office workers by transport supplier; - Account 44.02 “Business expenses in organizations engaged in industrial or other production activities” when transporting products of its own production by a transport organization;

- For audit purposes, the account is indicated by debit.

- Account 26, reflected when sending correspondence when using the Internet line;

How is the re-billing of the services in question to the end buyer processed? — video, comments

The supplier does not provide any more documents; he explains the absence of documents by the fact that he himself does not provide transportation services, but simply reissues them.

Civil legal aspect In the situation under consideration, the tax obligations of the parties, the procedure for drawing up primary documents and accounting records will depend on the qualification of their legal relations based on the terms of the agreement (agreements) concluded between them. By virtue of paragraph 1 of Art. 509 of the Civil Code of the Russian Federation, the supply of goods is carried out by the supplier by shipment (transfer)

In accounting, the seller makes the following entries: “Debit 76 Credit 60” - receipt of documents for transport services from the carrier; Debit 76 Credit 62 - rebilling of transport services to the buyer. A supply agreement is a type of purchase and sale agreement (clause

5 tbsp. 454 of the Civil Code of the Russian Federation). In accordance with paragraph 1 of Art. 454 of the Civil Code of the Russian Federation, under a purchase and sale agreement, one party (seller) undertakes to transfer the thing (product) into ownership of the other party (buyer), and the buyer undertakes to accept this product and pay a certain amount of money (price) for it.

By virtue of paragraph 1 of Art. 509 of the Civil Code of the Russian Federation, the supply of goods is carried out by the supplier by shipping (transferring) the goods to the buyer, who is a party to the supply agreement, or to the person specified in the agreement as the recipient.

institutions;

Services in trade (work of consultants with clients, merchandisers for displaying goods, etc.); Other types of services.

The main document issued upon completion of the service is the Service Provision Certificate.

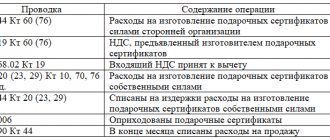

Method 1. Intermediary services

This method of rebilling transportation costs is the most common, although it is quite labor-intensive in terms of its documentary maintenance.

- Agreement

In the contract with the buyer, we fix a clause that we undertake on our own behalf to find a suitable carrier, enter into an agreement with him on the transportation of goods and monitor the implementation of this agreement until the goods are transferred to the buyer. That is, we indicate that we undertake the obligations of an intermediary between the buyer and the carrier organization. The main condition is to specify at least a symbolic amount of remuneration, since intermediary agreements must be compensated (Articles 990, 1005 of the Civil Code of the Russian Federation).

- Source documents

For transport services, we provide the buyer with a bill of lading on our behalf, generated on the basis of primary documents from the carrier organization. Don't forget to attach a copy of the carrier's bill of lading to it.

For intermediary services, we present to the buyer a report from the intermediary indicating the amount of his remuneration (Article 999 of the Civil Code of the Russian Federation). We develop the report form independently with its mandatory approval in the accounting policy.

- Invoice

We record the invoices received from the carrier organization in the journal of received and issued invoices (clause 1, subclause “a”, clause 11, section II, appendix 3 to the Decree of the Government of the Russian Federation “On filling out documents for VAT calculations” dated December 26, 2011 No. 1137).

For the buyer:

- we issue an invoice for transport services on our behalf and attach to it a copy of the invoice of the carrier organization (clause 1, subparagraph “a”, clause 7, section II, appendix 3 of the Decree of the Government of the Russian Federation “On filling out documents when making payments for VAT" dated December 26, 2011 No. 1137), registered in the invoice journal;

- We register the invoice for the brokerage fee in the sales book.

NOTE! When re-issuing an invoice for transport services, in lines 1 (date), 2, 2b, put the information of the carrier organization, not yours (subparagraphs “a”, “c”, paragraph 1, section II, appendix 1 to the resolution of December 26 .2011 No. 1137).

Read more about issuing invoices by intermediaries in our article “How to issue invoices when selling goods through an intermediary?”

Own costs

Before making a delivery, you must choose how it will be reflected.

There are two ways to account for supply costs:

- by written agreement, including in the price of the product;

- by written agreement (counted separately).

Transport services included in the price of products must be reflected in the sales contract as a separate line. It is necessary to make a note about the amount for transportation services.

Failure to allocate the amount of transport services in a separate line can result in the following troubles:

- if the buyer returns the products, he will have to return the entire amount back, including delivery costs;

- The tax office will not count this amount as a deduction when calculating income tax.

The best option would be to conclude a separate contract/agreement for the transportation of sold goods. It specifies all the supplier's costs and the buyer's obligation to reimburse. In this case, the accounting for sales and transportation expenses will be separated.

Documentation

In the case of organizing the accounting of transport services included in the price of products, the document accompanying the cargo will be the consignment note.

When organizing the accounting of transport services using an additional contract/agreement, the primary documentation can be prepared in three ways:

- filling out the consignment note;

- filling out separately the goods and transport invoices;

- filling out the consignment note and the act, which will reflect transport services.

Each of the above documents must be recorded in the sales book.

How to rebill transport services to another organization

If you don’t want to enter into a mediation agreement, but re-issuing invoices seems too complicated and troublesome, you can formalize the relationship in a different way.

We record the invoices received from the carrier organization in the journal of received and issued invoices (clause 1, subclause “a”, clause 11, section II, appendix 3 to the Decree of the Government of the Russian Federation “On filling out documents for VAT calculations” dated December 26, 2011 No. 1137).

Continuing the topic. Since, judging by the description, purchase and sale and service agreements, and not agency agreements, were concluded between the Transport Company and the Supplier, and then between the Supplier and the Buyer, a standard package of documents is issued to the Buyer - Act and Invoice, as well as other documents , if they are provided for in the contract. Invoice We record invoices received from the carrier organization in the journal of received and issued invoices.

Receipt of services: postings

The receipt of services in an organization is reflected depending on the characteristics, as well as the type of expenses. The organization’s services can be reflected both as part of current expenses (accounts 20, 26 “General business expenses”, 44, etc.) and as part of property under certain conditions.

For example, expenses for information or consulting services related to the purchase of goods will be reflected as follows (clause 6 of PBU 5/01, Order of the Ministry of Finance dated October 31, 2000 No. 94n):

Debit account 41 “Goods” – Credit account 60

And if a trading company incurs expenses for certification of copies of constituent documents when concluding an agreement with a buyer, then the accounting entry for notary services will be as follows:

Debit of account 44 – Credit of account 71 “Settlements with accountable persons”, 60

Sales of goods or services are the main sources of income for a company. The sale is reflected in accounting either at the time of shipment or at the time of payment. Each shipment involves its own postings.

Sales of goods are reflected in the debit of the “Cost” subaccount () and Credit 41 of the account, the subaccounts for which are determined by the type of trade (wholesale/retail, etc.):

Revenue from the sale of goods is reflected in the Credit of account 90 subaccount “Revenue” in correspondence with the account.

Sales of goods can be carried out through an intermediary. Then it is necessary to make entries Debit 45 Credit 41 “Goods in warehouses”. As inventory items are sold, business entries are made to debit account 90 “Cost” and credit. When exporting goods, the same transactions are made.

In the main taxation system, it is necessary to pay VAT on sales. The tax is reflected by posting Debit VAT Credit.

In retail trade, goods are sold at selling price. The markup is made according to . When selling at the end of the month, you need to make reversing entries:

Debit 90 “Cost” Credit 42.

How is the resale of goods from a commission agent reflected?

The intermediary, depending on the terms of the contract, receives remuneration before fulfilling obligations, during the sale of goods, or after completion of the transaction. The goods accepted by him on commission are taken into account off the balance sheet, since they are not his property. The commission agent's accounting is reflected by the following entries:

| Goods accepted for sale |

| Sales to the buyer (revenue) are reflected |

| The goods have been shipped to the buyer |

| Intermediary costs reimbursed by the seller are taken into account |

| Payment of intermediary costs incurred during the sale |

| The commission fee for the transaction is reflected |

| VAT charged on remuneration |

| Reward transferred from the seller |

Thus, goods (for resale or not) in production or trading organizations are always reflected on balance sheet accounts, in companies specializing in intermediary services - behind the balance sheet.