How is the OS created?

In fact, there are two possible ways to organize the OS creation process:

- create an object on your own;

- involve contractors and third-party resources in the process - accounting for the contract method of construction.

In both cases, the accountant’s task is to correctly take into account all expenses and reflect the accepted object correctly at its original cost.

To organize correct accounting of a created, constructed, erected object, it is necessary to correctly determine the costs incurred, make sure that the created property is really a fixed asset, and determine how VAT on expenses will be taken into account. Accounting depends on the method of creating an asset - business or contract. Postings and paperwork will be slightly different.

When can an object be capitalized?

Conditions for including created property in the OS:

- Long service life - over 12 months.

- Making a profit from use - the object must participate in economic activity to obtain benefits.

- No intention to sell the asset in the next year.

If these three conditions are not met, the manufacturing object is not accepted as part of fixed assets, but is included as inventory.

Important! If we are talking about construction, then the constructed real estate before the state registration of rights to it is accounted for in an independent subaccount 01 of account.

Accounting when creating in an economic way

The economic method assumes that the company will engage in construction, creating an OS facility on its own, without receiving the help of contract companies.

Acceptance of independently created or constructed fixed assets for accounting is carried out at a cost called the initial one.

Components of the initial cost of an OS when manufactured independently:

- cost indicator of the materials used, spare parts, components (MP) without added tax;

- salary of the company’s own personnel involved in the creation of the OS object;

- insurance contributions for employee salaries;

- depreciation of equipment used in the process;

- VAT on inventories, which cannot be accepted for reimbursement, for example, due to the lack of an invoice.

The sum of all these costs forms the initial cost of an economically created fixed asset, at which it must be accepted for accounting.

Formation of the initial cost when creating an OS

Initial cost of fixed assets in accounting

In accounting, assets are recognized as fixed assets (clause 4 of PBU 6/01):

- used for a long time (more than 12 months);

- not intended for resale, i.e. the asset is intended for use in the production of products, performance of work (provision of services), management needs, rental;

- the use of which is aimed at generating income in the future.

Fixed assets are accepted for accounting at their original cost (clause 7 of PBU 6/01).

When creating an OS, the initial cost consists of all the actual costs of constructing, manufacturing, producing the OS and preparing it for working condition (clause 8 of PBU 6/01).

Accounting and formation of costs for the production of fixed assets is determined similarly to the accounting of costs for finished products (clause 26 of the Guidelines for accounting of fixed assets, approved by Order of the Ministry of Finance of the Russian Federation dated October 13, 2003 N 91n).

The amount of VAT and other refundable taxes is not taken into account in the initial cost of fixed assets (clause 27 of the Guidelines for accounting of fixed assets, approved by Order of the Ministry of Finance of the Russian Federation dated October 13, 2003 N 91n).

All actual costs associated with the creation of fixed assets are taken into account in Dt 08.03 “Construction of fixed assets” (Chart of Accounts 1C).

Initial cost of fixed assets in tax accounting

In tax accounting, assets are divided into depreciable and non-depreciable.

Depreciable property is recognized as having (clause 1 of Article 256 of the Tax Code of the Russian Federation):

- useful life more than 12 months;

- initial cost more than 100,000 rubles.

Fixed assets include depreciable property, which is a means of labor in the activities of the organization (paragraph 1, paragraph 1, article 257 of the Tax Code of the Russian Federation).

The initial cost of the OS is determined based on all the actual costs of constructing, manufacturing and bringing the OS to working condition, and when producing the OS on its own - as the cost of the finished product (clause 1 of Article 257 of the Tax Code of the Russian Federation).

VAT

If, when creating an operating system, construction and installation work (CEM) was carried out in an economic way for one’s own consumption, it is necessary to charge VAT on the amount of construction and installation work performed (clause 3, clause 1, Article 146 of the Tax Code of the Russian Federation).

Study the accrual of VAT on construction and installation work performed in-house for your own needs

Accounting in 1C

When creating an OS on your own, the costs that form the initial cost of the OS are reflected in different documents depending on the type of costs, for example:

- document Payroll - to reflect in the initial cost of the fixed assets the costs of wages for employees creating the fixed assets;

- document Requirement invoice - for writing off the necessary materials when creating an operating system;

- other documents, the costs of which will be reflected in Dt 08.03 “Construction of fixed assets”.

If the creation of fixed assets is carried out by contract or mixed method, the costs are also charged to account 08.03 “Construction of fixed assets”.

In this case, the documents may be the following:

- Receipt (act, invoice) - to reflect the services of contractors in the costs of constructing fixed assets;

- Transfer of equipment for installation - to reflect the installation and construction of OS by contract.

In 1C, the distinction between the creation of fixed assets using an economic method or a contract method is carried out by analytics on account 08.03 “Construction of fixed assets” subconto Construction Methods .

Filling out the Construction Methods is required for correct accounting, since VAT must be charged at the end of the quarter on construction and installation work carried out in a self-employed manner.

Paperwork

Accounting for incurred costs and recording of transactions is carried out using the following documents :

- invoices for receipt and transfer of goods;

- accounting information;

- invoice – in relation to tax on construction work, subject to accounting as part of the cost of a fixed asset due to the full application of the latter in non-VAT-taxable activities;

- payslips.

Postings

Account 08 is used to collect all expenses . All cost amounts are collected in the debit of this accounting account; upon completion of the creation of the object, the total value of the recorded costs is transferred to account 01 , where the object will be accounted for until it is disposed of from the organization or written off.

When collecting costs for the construction or creation of an object, account 08 corresponds with various accounts, depending on the type of expense.

List of corresponding accounts:

- 10 – to account for inventories invested in the manufacture of an object;

- 02 – to account for depreciation charges if depreciable equipment is involved in construction or manufacturing;

- 70 – to account for the remuneration of employees of the enterprise engaged in the creation of fixed assets;

- 69 – to account for insurance contributions accrued for employee benefits.

As a result of production, the total indicator of all expenses is transferred in one transaction from credit 08 to debit 01. Thus, the created object is accounted for as a fixed asset at its original cost.

A summary table with accounting entries for the construction (creation) of an operating system using an economic method using one’s own resources is given below.

Postings for the economic method:

| Business transaction | Debit | Credit |

| The cost of inventories allocated for the construction (manufacturing) of fixed assets is taken into account (excluding tax) | 08 | 10 |

| Expenses for paying staff are taken into account | 08 | 70 |

| Reflects the costs of compulsory labor insurance for personnel | 08 | 69 |

| Depreciation on equipment used in creation is taken into account | 08 | 02 |

| VAT on SMP is shown in the cost of an object intended entirely for non-taxable activities | 08 | 19 |

| The constructed (created, manufactured) object is capitalized as a fixed asset | 01 | 08 |

Accounting for other methods of acquiring fixed assets:

- contribution to the management company in the form of a contribution from the founder;

- free receipt;

- purchase.

Manufacturing example

Example conditions:

The company purchased computer components for RUB 448,400. (VAT including RUB 68,400).

From these components, 7 computers were assembled on our own without the involvement of third parties, while all components were involved in the assembly.

All computers were capitalized as fixed assets on the balance sheet of the enterprise.

The cost of wages for workers involved in the manufacture of computers amounted to 75,000 rubles, the total amount of insurance contributions was 22,500 rubles.

The assembly of computers from components does not relate to construction and installation work, and therefore this operation is not subject to VAT, and accordingly, in this example there is no need to account for VAT.

Example accounting entries:

| Sum | Operation | Debit | Credit |

| 380000 | Computer components supplied to the parish | 10 | 60 |

| 68400 | VAT allocated on supplier invoice | 19 | 60 |

| 68400 | VAT is accepted for deduction | 68 | 19 |

| 448400 | Transferred non-cash payment to the supplier for components | 60 | 51 |

| 380000 | All components were transferred for computer assembly | 08 | 10 |

| 75000 | Reflects the calculation of salaries for personnel engaged in the manufacture of computers | 08 | 70 |

| 22500 | The accrual of insurance coverage is reflected | 08 | 69 |

| 477500 (380000 + 75000 + 22500) | 7 computers accepted for registration | 01 | 08 |

Example of building construction

Example conditions:

The company built an office building for itself using its own resources.

Expenses:

- materials – 1,180,000 (180,000 – tax included);

- builders' salary – 300,000;

- wage contributions for builders – 90,000;

- depreciation of construction equipment – 150,000.

Example accounting entries:

| Sum | Operation | Debit | Credit |

| 1000000 | Construction materials were delivered to the parish | 10 | 60 |

| 180000 | VAT allocated on supplier invoice | 19 | 60 |

| 180000 | Tax accepted for deduction | 68 | 19 |

| 1180000 | Transferred non-cash payment to the supplier for construction materials | 60 | 51 |

| 1000000 | All materials were transferred to construction | 08.3 | 10 |

| 300000 | Reflects the calculation of salaries for personnel involved in construction | 08.3 | 70 |

| 90000 | The accrual of insurance coverage is reflected | 08.3 | 69 |

| 150000 | Accrued depreciation on equipment is taken into account | 08.3 | 02 |

| 1540000 (1000000 + 300000 + 90000 + 150000) | The office is included in fixed assets | 01 | 08.3 |

| 277200 (1000000 + 300000 + 90000 + 150000) * 18% | VAT accrued on SMP for own needs | 19 | 68 |

| 277200 | VAT is accepted for deduction, since the constructed office is planned to be used in taxable activities | 68 | 19 |

Accounting for the construction of fixed assets in 1C: Accounting

Published 12/12/2019 09:46 Author: Administrator Many companies are faced with a situation in their activities when they need to build a fixed asset. To do this, they often hire a contractor, and for greater control over the contractor, they purchase materials themselves. This is especially true in companies involved in the management and operation of residential real estate. For example, the management company decided to improve the territory of the village it serves and build a children's playground, or, as an option, build a winter shed for storing equipment. To do this, she purchased materials and hired a contractor. Accountants may have questions in such cases. How to organize inventory accounting in this case? What closing documents are required from the contractor? How to register a constructed object? Let's consider accounting for such construction using the example of the 1C: Enterprise Accounting version 3.0 program.

So, in such a situation, you need to start with the main thing - with the concluded agreement. It must clearly state who purchases what materials to carry out construction work. At the same time, the Contractor may use partly its own materials for construction, and partly those provided by the Customer. For example, a clause of the contract may read like this: “The Customer instructs, and the Contractor undertakes, to carry out work on the construction of a shed at the address: ____________ with proper quality and within the time period established in the contract. The work is carried out by the Contractor using its own rough materials. Materials for finishing are provided by the Customer. The list of materials used for finishing is given in Appendix No. 1 to this agreement.”

In this case, the customer should take into account that the total cost of the work will consist of the contract price plus the cost of materials. This is not always profitable, but many Customers go for it, thereby ensuring themselves control over the quality of the materials used.

The next step will be the purchase of goods and materials necessary for construction and their transfer to the Contractor. There are two ways to reflect this step in 1C: Accounting:

1) By recording inventory items transferred to the Contractor in a separate warehouse

2) Through the document “Transfer of raw materials for processing”

Let's look at the pros and cons of these methods using an example.

Method 1

The customer purchases materials and brings them to his warehouse:

In order to reflect the transfer of inventory and materials to the Contractor, a separate warehouse should be created in the program, for example, “Contractor”.

The transfer of materials to the Contractor is formalized through the document “Movement of Goods”:

Disadvantage of this method: the document does not provide a printed form M-15 “Invoice for issue of materials to third party”, so if necessary, it will have to be generated manually.

After the Contractor reports on the consumption of materials, the costs are collected on account 08 using the document “Requirement-invoice”:

If the Contractor has unspent inventory items, then their return to the organization’s warehouse is formalized again through the “Movement of Goods” document:

This method of accounting is good because it does not require manual adjustments.

But in practice, many people use the second method.

Method 2

The customer purchases materials and brings them to his warehouse, similar to the first method:

The transfer of purchased goods and materials to the Contractor is documented in the document “Transfer of raw materials for processing”:

Documentary evidence of the transfer of goods and materials to the Contractor will be the printed form of the document “Invoice for the release of materials to the third party (M-15)”.

Print it out in three copies: one for you, the second for your warehouse manager and the third for the Contractor.

After the Contractor has used up all the materials and submitted to the Customer’s accounting department the “Act on the use of customer-supplied raw materials” (the form of such an act, by the way, is also better provided for in the contract), the accountant must write off the materials transferred for processing to account 08. The standard document “Receipt from Processing” does not provide for postings using account 08, so this can be done in manual adjustment mode:

As you can see, the second method is convenient in that it allows you to generate a printed form of the M-15 invoice in automatic mode, but it also has its drawbacks in terms of manual adjustment of postings.

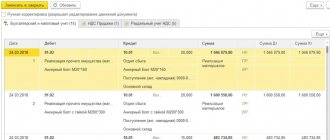

Regardless of the chosen method, the further sequence of operations will be the same. The collected costs on account 08 should form the cost of the constructed fixed asset item. Upon completion of construction work, the Contractor will provide you with an acceptance certificate for the completed construction of the facility. Based on it, you generate the document “Receipt of construction projects”:

The final stage will be the acceptance of the constructed facility for accounting:

The amount of the object accepted for accounting will be the sum of the cost of work and materials under the contract plus the cost of customer-supplied materials.

Author of the article: Anna Kulikova

Did you like the article? Subscribe to the newsletter for new materials

Add a comment

JComments