The list of expenses (Article 346.16 of the Tax Code of the Russian Federation) that a tax payer of the simplified tax system can take into account includes expenses for the acquisition, construction and production of fixed assets, as well as for their completion, additional equipment, reconstruction, modernization and technical re-equipment. The costs of acquiring fixed assets are significant, so accounting errors can be costly to the taxpayer. Let's see how to properly account for expenses.

Fixed assets are part of the property used as means of labor for the production and sale of goods (performing work, providing services), for managing an organization or leasing, with a useful life of more than 12 months. The organization sets the initial cost of an object for classification as fixed assets for accounting purposes independently - the lower limit of the cost can be set no higher than 40,000 rubles.

Tax accounting of fixed assets is carried out only by simplified simplified tax systems “income minus expenses”. The fixed assets include property that is recognized as depreciable in accordance with Art. 346.16 Tax Code of the Russian Federation. The following conditions must be met:

- the property is owned or is an integral improvement to the leased property;

- the property is used to generate income;

- useful life exceeds 12 months;

- the initial cost of the OS exceeds 100,000 rubles (40,000 rubles until 2021);

The Tax Code requires that the initial cost of an asset include the costs of its acquisition, construction, manufacturing, delivery and bringing it to a state in which it is suitable for use. Additional costs that are included in the initial cost of the OS are the costs of state duty, installation, repairs (if the purchased OS requires repairs), and so on.

Now let's see how to correctly attribute fixed assets to tax expenses

If an organization operates on the simplified tax system “Income”, the cost of purchased or created operating systems is not written off as expenses. If the object of taxation is “income minus expenses,” the value of the property reduces the tax base. To do this, it is important to fulfill the following conditions:

- The OS has been put into operation;

- paid to the supplier;

- documents for registration have been submitted (for OS requiring state registration);

- expenses are documented, and the property is actually used in the activity to generate income.

Remember that for fixed assets acquired during the application of the simplified tax system, and for fixed assets acquired in the period before the application of the simplified tax system, the procedure for recognizing expenses is different.

First, let's look at the situation when a fixed asset is purchased during the period of application of the simplified tax system.

Expense recognition algorithm for such fixed assets:

- We monitor the fulfillment of all the above conditions;

- we determine how many reporting dates are left until the end of the year (these are 31.03, 30.06, 30.09, 31.12);

- divide the initial cost of fixed assets by the number of reporting dates remaining until the end of the year;

- The resulting amount after division is included in expenses on the last dates of the reporting periods.

Example 1.

On August 15, we purchased a computer worth 60,000 rubles, paid it to the supplier and began using it in business. There are two reporting dates before the end of the year: September 30 and December 31. With these two dates of 30,000 rubles each (60,000 rubles / 2 = 30,000 rubles), we include the cost of the computer in expenses.

The useful life of an asset does not affect the accounting procedure. Including if the purchased object was already in operation from another company.

Example 2.

In December 2021, equipment worth RUB 38,000 was purchased. Its transportation, installation and configuration cost 10,000 rubles. As a result, the initial cost of the OS was 48,000 rubles. Installation of the equipment was completed in January 2021, and at the same time the equipment was put into operation and began to be used in business activities.

48,000 rub. /4 = 12,000 rub.

On March 31, June 30, September 30 and December 31, 2021, 12,000 rubles will be included in expenses.

Now let’s look at the procedure for accounting for the cost of fixed assets acquired before the transition to the simplified system

Easy online accounting

In Kontur.Accounting it is convenient to create a primary account, calculate salaries and contributions, submit reports to the Pension Fund of Russia, Social Insurance Fund, Federal Tax Service

Try it

Fixed assets acquired before the transition to the simplified tax system are accepted for accounting at their residual value. Let us determine the residual value of fixed assets according to tax accounting data as of the beginning of the first year of application of the simplified tax system. It is defined:

- when switching from OSNO - the purchase price (construction, manufacturing) - depreciation accrued according to tax accounting data;

- when switching from UTII - the purchase price (construction, manufacturing) - depreciation accrued according to accounting data.

If the property is not fully paid for at the time of transition to the simplified tax system, only the paid part of the residual value must be taken into account. To do this, distribute the payment amount between the residual value and depreciation charges according to the formula:

Residual value of fixed assets to be reflected in accounting = Residual value of fixed assets on the date of transition / Initial cost of fixed assets × Paid part of the cost of fixed assets

Inclusion in expenses of the cost of fixed assets purchased before the transition to the simplified tax system depends on the useful life. We are talking about the deadline that was set when putting the facility into operation, and not about the one that remains to be finalized. Depending on the useful life, three situations are possible.

- With a useful life of up to 3 years inclusive, the residual value of fixed assets is included in expenses during the first calendar year of application of the simplified tax system in equal shares at the end of each reporting period: March 31, June 30, September 30 and December 31.

Example 3.

When purchasing a copy machine, the useful life is set at 3 years.

On January 1, 2021, the organization switched to the simplified tax system. The residual value of the copier according to tax accounting data is 42,000 rubles.

The organization will reflect in expenses March 31, June 30, September 30 and December 31, 2021, 10,500 rubles each (42,000 rubles / 4 = 10,500 rubles), provided that there is no debt to the copier supplier.

- With a useful life of more than 3 years and up to 15 years inclusive, in the first year of application of the simplified tax system, 50% of the residual value of the asset is included in expenses, in the second year - 30% and in the third year - 20%. Expenses are expensed in equal installments: March 31, June 30, September 30 and December 31.

Example 4.

On January 1, 2021, the organization switched from OSNO to simplified tax system. The residual value of a car with a useful life of 4 years (48 months) as of January 1, 2021 was 600,000 rubles. During 2020, expenses take into account 50% of the residual value of the vehicle.

600,000 rub. × 50% = 300,000 rub.

300,000 rub. / 4 = 75,000 rub.

March 31, June 30, September 30 and December 31 are included in expenses of 75,000 rubles.

During 2021, expenses take into account 30% of the vehicle's residual value.

600,000 rub. × 30% = 180,000 rub.

180,000 rub. / 4 = 45,000 rub.

March 31, June 30, September 30 and December 31 are included in expenses of 45,000 rubles.

During 2022, expenses take into account 20% of the vehicle's residual value.

600,000 rub. × 20% = 120,000 rub.

120,000 rub. / 4 = 30,000 rub.

March 31, June 30, September 30 and December 31 are included in expenses of 30,000 rubles.

- If the useful life is more than 15 years, the residual value of the fixed assets is included in expenses in equal shares on the last dates of the reporting periods during the first 10 years of application of the simplified tax system.

Example 5.

On January 1, 2021, the organization switched from OSNO to simplified tax system. Before switching to the simplified tax system, the organization acquired a building, the residual value of which as of 01/01/2020 was 10 million rubles.

For 10 years, from 2021 to 2029, the organization will include in expenses the residual value of fixed assets on the last numbers of reporting dates (March 31, June 30, September 30 and December 31) in equal shares of 10,000,000 rubles. / 10 years / 4 = 250,000 rubles.

When switching from OSNO to simplified tax system, there is an additional obligation to restore the tax accepted for deduction. VAT is not restored in full, but in proportion to the residual value of fixed assets in the last quarter before the transition and is taken into account among other expenses.

Example 6.

An organization at OSNO in 2021 purchased a production line worth 500,000 rubles, including 20% VAT. VAT in the amount of 100,000 rubles (500,000 × 20%) was fully deductible. From 01/01/2020, the organization switches to the simplified tax system. The residual value of the fixed asset at the time of transfer is 300,000 rubles.

VAT must be restored in the amount of 60,000 rubles (100,000 rubles × 300,000 rubles / 500,000 rubles).

Proceeds from the sale and disposal of a fixed asset cannot be reduced by any costs associated with its disposal. The same is true if the disposal of fixed assets occurred for reasons that do not depend on the organization: theft, fire, flooding, etc., and the costs of its acquisition were not completely written off.

Example 7.

In the 1st quarter, the organization purchased a structure worth 1 million rubles, having fulfilled all the conditions necessary to include the cost of fixed assets in expenses. On March 31, expenses included 1,000,000 / 4 = 250,000 rubles.

On April 1 of the same year, the structure was destroyed by the elements. In this case, the organization will not be able to take into account the remaining 750,000 rubles as expenses, since one of the conditions for recognizing expenses is not met: the OS has ceased to be used in the organization’s activities.

The procedure for registering the disposal of fixed assets

The procedure for documenting the write-off of fixed assets from the balance sheet may differ slightly depending on the established reason.

Disposal of an asset as a result of its sale

When a fixed asset is transferred under ownership to another person (individual or legal), it must leave the balance sheet of the “parent” company. In this case, a purchase and sale agreement is concluded. In addition to this basic document, disposal is accompanied by the preparation of the following papers:

- overhead;

- act of acceptance and transfer of fixed assets (drawn up according to standard sample No. OS-1).

In accounting, this process is carried out as follows: account 01 “Disposal of fixed assets” is completed with the corresponding subaccount, then you need to write off the depreciation amount for the disposed object, and the remainder of its value is added to “other expenses”. These expenses may also reflect expenses incurred on dismantling, packaging and other actions with the fixed asset. Postings:

- debit 02 “Depreciation of fixed assets”, credit 01 – adding the remaining cost of fixed assets to other expenses;

- debit 91 “Other income and expenses”, credit 23 “Auxiliary production” - expenses for preparing OS for sale (disassembly);

- debit 91, credit 44 “Sales expenses” - expenses for the sale of fixed assets;

- debit 62 “Settlements with customers”, credit 91/1 – sales (receiving income from the sale of fixed assets);

- debit 91/2, credit 68 “Calculations for taxes and fees” - VAT calculation.

Disposal of worn-out fixed assets

Unsuitability revealed during operation or inventory is a good reason for writing off the operating system. It is carried out by drawing up an Act in form OS-4, which is signed by a specially created commission. The act must reflect the following information:

- name of the asset and its inventory number;

- original cost and accrued depreciation;

- the reason why the product became unusable;

- expenses for asset liquidation (dismantling, disassembly, removal, etc.);

- income possibly received upon disposal (sale or use of individual parts, components, elements of the operating system);

- the result of disposal (original cost minus depreciation amount plus write-off expenses minus income from write-off).

REFERENCE! If a vehicle is written off, this act is drawn up in the OS-4a form and a certificate issued by the State Inspectorate on deregistration of the vehicle is attached to it.

Accounting entries go to account 47 “Sales and other disposals of fixed assets”, and the financial result is attributed to account 80 “Profits and losses”.

IMPORTANT! The same scheme applies to the disposal of fixed assets liquidated as a result of accidents and disasters.

Wiring example: in a carpentry shop, a woodworking machine, which at the beginning of operation cost 30,000 rubles, completely broke down. Depreciation accrued on this equipment is RUB 28,000. The machine was dismantled in the workshop, which cost 200 rubles. After disassembly, several spare parts remained that could be used in the future; they were capitalized at the warehouse at a cost of 1,000 rubles, the rest was scrap metal worth 800 rubles. The accounting entries will be as follows:

- debit 01, credit 01 – RUB 30,000;

- debit 02, credit 01 – 28,000 rubles;

- debit 91/2, credit 01 – 2,000 rub. (residual value of the machine);

- debit 91/2, credit 23, 25 – dismantling costs;

- debit 10/5, credit 91/1 – 1000 rub. (posting of spare parts);

- debit 10, credit 91/2 – 800 rub. (posting of scrap metal).

Disposal of stolen fixed assets

If the OS is absent from the organization due to an illegal action, this action becomes the responsibility of the criminal authorities. Regardless of the outcome of the investigation, since the asset is no longer available, it must be written off. For this purpose, an act is drawn up in form INV-26. Other accounting documents must be accompanied by a copy of the resolution to initiate a criminal case or investigation, that is, confirmation of the illegality of the action in relation to the OS.

The accounting entry of stolen material assets is carried out using the debit of account 73/2, credit 94 “Calculations for compensation for material damage.” If the culprit is found, then compensation for the loss through the cash register is carried out by debit 50, credit 73-2.

Disposal of fixed assets contributed to someone else's authorized capital

When an asset is transferred to the authorized capital of another organization, this is a kind of monetary investment. In accounting, you need to reflect the depreciation carried out, register the asset as a financial investment, restore VAT and reflect the share of profit/loss on the transfer of fixed assets.

Posting example : a private enterprise is registered as a participant in an LLC, it invests in the authorized capital equipment, which the meeting of participants valued at 250,000 rubles. When this equipment was used by a private enterprise, its value on the balance sheet was 210,000 rubles, and depreciation was 40,000 rubles. The postings will be like this:

- debit 02, credit 01/2 - 40,000 rub. (depreciation);

- debit 58/1, credit 01/2 - 170,000 rubles (residual value);

- debit 19, credit 68 - 30,600 rub. (VAT restoration);

- debit 58/1, credit 19 - 30,600 rubles;

- debit 91/2, credit 58/1 - 49,400 rub. (displaying the amount of loss from the transfer of equipment as other expenses). It is calculated as follows: the share contributed to the authorized capital (250 thousand rubles), minus the residual value (170,000 rubles). minus restored VAT (RUB 30,600).

Correct registration and display of disposal of fixed assets during their accounting is the key to avoiding problems when checking the relevant reports.

What to do when fixed assets are purchased in installments?

The cost of property purchased in installments can be written off as an expense as it is paid. But it is impossible to take into account the amount paid immediately in the current quarter - it must be divided among the remaining reporting periods until the end of the year. That is, proceed by analogy with what you would do if you took into account the completely obtained OS. If the debt cannot be repaid by the end of the year, then the unpaid portions are transferred to the next year and are taken into account in the same manner.

Let's look at this algorithm using examples.

Example 8.

On September 2, 2021, the organization purchased in installments, accepted for accounting and began to use in its activities a boat worth 3,600,000 rubles, paying the seller 600,000 rubles. According to the terms of the agreement, the organization must repay the debt in the amount of 600,000 rubles quarterly. Let's consider how much the cost of purchasing a boat will be taken into account in expenses.

On September 30, 2021, expenses include half of the paid amount of 600,000 rubles / 2 = 300,000 rubles. The remaining half is taken into account in expenses on December 31, 2021. In addition, in the 4th quarter of 2020, the organization will transfer another 600,000 rubles, which should also be taken into account in expenses. As a result, on December 31, 2021, the organization will reflect 300,000 rubles in expenses. + 600,000 rub. = 900,000 rub.

In 2021, the organization will transfer 600,000 rubles to the boat seller quarterly.

600,000 rubles paid in the 1st quarter will be attributed to expenses in equal shares - 150,000 rubles each = 600,000 rubles. /4, the last numbers of four reporting dates: March 31, June 30, September 30 and December 31.

600,000 rubles paid in the 2nd quarter will be expensed in equal shares of 600,000 rubles. / 3 = 200,000 rub. the last numbers of three reporting dates: June 30, September 30 and December 31.

600,000 rubles paid in the 3rd quarter will be expensed in equal shares of 600,000 rubles / 2 = 300,000 rubles. the last numbers of two reporting dates: September 30 and December 31.

600,000 rubles paid in the 4th quarter will be expensed as a lump sum on December 31.

As a result, in 2021 expenses take into account:

March 31: 150,000 rubles

June 30: 150,000 + 200,000 = 350,000 rubles

September 30: 150,000 + 200,000 + 300,000 = 650,000 rubles

December 31: 150,000 +200,000 + 300,000 + 600,000 = 1,250,000 rubles

Accounting for fixed assets for economic entities using the simplified tax system

You can write off the cost of fixed assets as expenses in a situation where an enterprise uses the simplified tax system after it has been put into operation. That is, after all documents on the OS have been completed:

- Act OS-1 on acceptance and transfer of OS;

- OS-6 card;

- Commissioning order.

The cost is written off as enterprise expenses in the amount of the initial cost, installation costs and bringing it to a state of readiness for use, including value added tax on fixed assets.

Important! When applying the simplified tax system, the cost of fixed assets is written off as enterprise expenses for tax purposes in equal shares during the first year of purchase of this fixed asset in each quarter of the year.

Let's look at examples of writing off the cost of operating systems as expenses.

Example 1.

Alpha LLC, operating under the simplified tax system, purchased in April 2021 a fixed asset - a car for delivering its products to customers. The cost of the car is 750 thousand rubles. The cost of the car will be written off as expenses for the purpose of calculating tax under the simplified tax system in the following order:

In the second quarter, 250,000 rubles as of June 30, 2021;

In the third quarter, 250,000 rubles as of September 30, 2017;

In the fourth quarter, 250,000 rubles as of December 31, 2017.

Example 2.

Omega LLC, operating under the simplified tax system, acquired an OS - a press for the production of minced meat in November 2021. The cost of the press is 195,000 rubles. The write-off of cost shares as expenses will occur in the following order:

In the fourth quarter, 195,000 rubles as of December 31, 2017.

The cost is written off before the end of the year in equal shares for each quarter, but since the OS was purchased in the fourth quarter, the write-off will take place entirely in the fourth quarter.

We sorted out the acquisition. It remains to be seen what will happen when fixed assets are disposed of.

The cost of retiring fixed assets that was under-depreciated is subject to write-off from the organization’s accounting records. The operation is formed on the date of disposal with the following transactions: Dt 02 Kt 01 and Dt 91 Kt 01.

Different reasons for disposal of fixed assets may lead to different tax consequences.

Let's consider several situations. First of all, it is necessary to separate cases of disposal of fixed assets in which ownership is transferred from those cases when ownership is not transferred.

In cases where ownership of a fixed asset is not transferred (liquidated, stolen, destroyed by disaster, etc.), expenses do not need to be restored and updated declarations do not need to be submitted.

When a transfer of ownership occurs (sale, donation, transfer to the authorized capital of another organization, etc.), the costs of purchasing fixed assets will not have to be restored in the following cases:

- transfer of ownership of fixed assets with a useful life of up to 15 years inclusive occurred 3 or more years after the end of the year in which the cost of the fixed assets was included in expenses.

- transfer of ownership of fixed assets with a useful life of more than 15 years occurred 10 or more years after the end of the year in which the cost of the fixed assets was included in expenses.

In other cases, expenses for the acquisition (construction, manufacturing, etc.) of fixed assets will have to be excluded from tax expenses, including instead depreciation accrued according to the rules of Chapter 25 of the Tax Code of the Russian Federation. The tax base must be recalculated for the entire period of use of the property. That part of the cost that will not be expensed by calculating depreciation cannot be taken into account for tax purposes under the simplified tax system.

In this case, it is necessary to submit updated declarations according to the simplified tax system for all tax periods in which the base is recalculated and pay additional tax to the budget. You also need to pay additional penalties for the period of delay and make corrections to the KUDiR for the current year.

Example 9.

On April 15, 2021, the organization purchased a laptop for 72,000 rubles and included 24,000 rubles in expenses on June 30, September 30 and December 31, 2020. When an asset is accepted for registration, the useful life is set at 36 months.

On May 5, 2021, the laptop was sold for 60,000 rubles. How will the organization's expenses change in 2020-2021?

Instead of 72,000 rubles, depreciation should be reflected in expenses, which will be 72,000 rubles monthly. / 36 months = 2,000 rub.

Based on the results of the 1st half of 2021:

- The costs of purchasing an operating system in the amount of 24,000 rubles are excluded from expenses.

- Depreciation in the amount of RUB 2,000 is included in expenses.

Total expenses for the first half of 2021 will decrease by 22,000 rubles.

Based on the results of 9 months 2021:

- The costs of purchasing an operating system in the amount of 24,000 rubles are excluded from expenses. × 2 = 48,000 rub.

- Depreciation for June-September is included in expenses in the amount of 2,000 rubles. × 4 = 8,000 rub.

Total expenses for the first 9 months of 2021 will decrease by 40,000 rubles.

Based on the results of 2021:

- The costs of purchasing an operating system in the amount of 24,000 rubles are excluded from expenses. × 3 = 72,000 rub.

- Depreciation for June-December is included in expenses in the amount of 2,000 rubles. × 7 = 14,000 rub.

Total expenses at the end of 2021 will decrease by 58,000 rubles. — the tax base will increase by the same amount.

It is necessary to pay additional tax in the amount of 58,000 rubles. × 15% = 8,700 rubles, penalties and submit an updated declaration under the simplified tax system for 2021.

Expenses for 2021 from January to May should take into account depreciation in the amount of 2,000 rubles. monthly.

The question of whether it is possible to take into account its residual value in expenses when selling an operating system is controversial. It does not directly follow from the code that this cannot be done, but the Ministry of Finance and the Federal Tax Service believe that this is prohibited, since the list of expenses under the simplified tax system is limited, and such type of expenses as the residual value of fixed assets is not provided for in it. The courts resolve this issue in different ways - sometimes simplifiers manage to prove that they had the right to write off both depreciation and residual value (decision of the Arbitration Court of the Yamalo-Nenets Autonomous Okrug dated 02/06/2018 in case No. A81-8554/2017, resolution of the Arbitration Court of the Central district dated June 23, 2017 No. F10-1838/2017 in case No. A54-5594/2016).

Accounting for fixed assets under the simplified tax system “Income”

Simplified people who have chosen the simplified tax system “Income” cannot take into account any expenses for tax purposes. Therefore, they cannot reduce the tax due to expenses associated with the acquisition of the operating system. But this does not mean that fixed assets can be ignored - you will still have to keep records.

The residual value of fixed assets is important as a criterion or limitation that allows you to switch to the simplified tax system and apply it. All simplifiers must comply with it, regardless of the chosen object of taxation. The threshold for the residual value of fixed assets in 2021 is 150 million rubles and is calculated according to accounting data.

When selling fixed assets, organizations and entrepreneurs using the simplified tax system of 6% take into account proceeds from sales in the general manner.

Author of the article: Natalya Sorokina, expert of the Kontur.Accounting service

Regulatory regulation

If a fixed asset has fallen into disrepair, the organization must write it off based on the decision of the commission (clause 77, clause 78 of the Guidelines for accounting of fixed assets, approved by Order of the Ministry of Finance of the Russian Federation dated October 13, 2003 N 91n, hereinafter referred to as Guidelines for accounting for fixed assets N 91н).

BOO. Liquidation costs and the residual value of fixed assets are included in the write-off period in other expenses (clause 86 of the Guidelines for accounting OS N 91n, clause 31 PBU 6/01, clause 11 PBU 10/99).

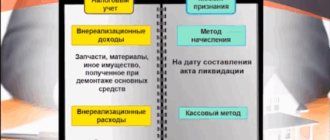

Materials generated as a result of the disposal of a fixed asset are accounted for at the current market value on the date of write-off of the fixed asset (clause 79 of the Methodological Guidelines for Accounting OS N 91n).

WELL. Expenses for the liquidation of fixed assets (including depreciation accrued using the straight-line method) are recognized:

- as part of non-operating expenses for fixed assets (paragraph 1, paragraph 8, paragraph 1, article 265 of the Tax Code of the Russian Federation).

For fixed assets depreciated by the non-linear method, depreciation continues to be accrued as part of the group, despite disposal (paragraph 2, paragraph 8, paragraph 1, article 265 of the Tax Code of the Russian Federation, paragraph 13, article 259.2 of the Tax Code of the Russian Federation, Letters of the Ministry of Finance of the Russian Federation dated December 3, 2015 N 03-03-06/1/70529, dated 04/27/2015 N 03-03-06/1/24095).

The generated waste at market value (confirmed by an accountant's certificate or an appraiser's report) is subject to inclusion in non-operating income (clause 13 of Article 250 of the Tax Code of the Russian Federation).

VAT. If fixed assets are written off ahead of schedule, there is no need to restore VAT (Letter of the Federal Tax Service dated April 16, 2018 N SD-4-3 / [email protected] ).