How to take into account the “Platonic” fee and transport tax (advance payments) in tax expenses? How to reflect the fee for "Platon" on the accounting accounts? What documents can be used to confirm the deduction of transport tax on the “Platonov” fee?

At the end of 2021, companies that own trucks weighing more than 12 tons were given the opportunity to reduce the amount of transport tax by the amount of the accrued fee (“Platonovsky” fee) to compensate for the damage caused to public federal roads by such vehicles (Article 361.1 of the Tax Code RF, clause 2 of article 362 of the Tax Code of the Russian Federation).

Thus, a transport tax benefit (deduction) is provided to transport tax taxpayers in connection with their payment of compensation for damages in respect of vehicles with a permissible maximum weight of over 12 tons.

OUTSOURCING LEGAL fees reduce the amount of transport tax only for a specific truck weighing more than 12 tons, and not the total amount of accrued transport tax (Letter of the Ministry of Finance of the Russian Federation dated January 13, 2017 No. 03-05-05-04/739).

Deductions for the “Platonic” fee are provided for tax periods 2021 - 2021.

Accounting for transport tax and “Platonov” fee as expenses

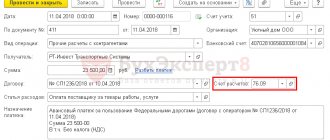

The amount of the advance payment made to the operator of the state toll collection system LLC RT-Invest Transport Systems (hereinafter referred to as LLC RTITS) is not an expense and, accordingly, is not reflected in tax accounting (clause 14 of article 270 of the Tax Code of the Russian Federation ).

“Profitable” expenses recognize the difference between the “Platonovsky” fee and the amount of transport tax calculated for the tax (reporting) period in relation to heavy trucks - vehicles with a permissible maximum weight of over 12 tons (clause 48.21 of Article 270 of the Tax Code of the Russian Federation, Letter of the Ministry of Finance of the Russian Federation dated November 21, 2016 No. 03-05-05-04/68317).

PROPERTY “ENERGY EFFICIENT” BENEFITS

Important!

That is, the tax expenses will not include the entire “Platonov” payment in its entirety, but in part of the excess of the amount of transport tax calculated for the heavy cargo for which it was paid (clause 48.21 of article 270 of the Tax Code of the Russian Federation - for companies on the OSN, clause 37 Clause 1 of Article 346.16 of the Tax Code of the Russian Federation - for “simplers”, Clause 45 of Clause 2 of Article 346.5 of the Tax Code of the Russian Federation - for payers of the Unified Agricultural Tax).

Calculation of transport tax taking into account the fee according to the Platon system in 1s 8.3

Drawing up a transport tax return To perform the operation “Drawing up a transport tax return”, you need to create a regulated report, Transport Tax Declaration (annual). Creating a report “Declaration of transport tax” (Fig. 12), menu: Reports – 1C-Reporting – Regulated reports – Create button. When filling out the document, please indicate the following:

- In the “Types of reports” form that opens – “Declaration of transport tax (annual)”.

- In the window that opens, in the “Period” field – 2021, in the “Form revision” field – “dated 12/05/2016 No. ММВ-7-21/”.

- Create button.

- Check the completion of the title page indicators (“Taxpayer”, “Tax period (code)”, “Reporting year”, etc.), which will be automatically filled in with the data contained in the information base.

FOR EXAMPLE

The advance payment for transport tax was 120 rubles, and the “Platonov” fee was 100 rubles. In this case, the company, based on the results of the first quarter, half of the year and 9 months, will not take into account the difference in terms of the excess of the transport tax over the “Platonov” fee. And only at the end of the year he will include 20 rubles in tax expenses.

As a general rule, one company can reduce transport tax by the amount of the “Platonov” fee. For example, if vehicles were leased, and heavy trucks were registered to the lessor, then the transport tax cannot be reduced by the “Platonic” fee paid by the lessee (Letter of the Ministry of Finance of the Russian Federation dated July 18, 2016 No. 03-05-04-04/41940 ).

That is, in this situation (heavy trucks are registered to the lessor), and not to the lessee, the lessor has no right to reduce the transport tax by the amount of the “Platonic” fee for the heavy truck.

In “profitable” expenses, you can only take into account the amount of transport tax actually paid (clause 1, clause 1, article 264 of the Tax Code of the Russian Federation, clause 48.21, article 270 of the Tax Code of the Russian Federation, clause 2, article 362 of the Tax Code of the Russian Federation). This means that it is impossible to simultaneously take into account in tax expenses both the amount of accrued transport tax and the deduction for the “Platonic” fee.

CHECKING THE CONTRACTOR

Important!

Thus, the “Platonic” fee reduces profits only to the extent of excess transport tax, and not in full.

If the vehicle is leased, the owner of the vehicle will charge and recognize the transport tax in full, and the lessee will charge and pay the “Platonic” fee and take it into account as part of other expenses.

Plato system and transport tax in 2021

Author: Ekaterina Solovyova Accountant-consultant

The beginning of 2021 was marked not only by an increase in the VAT rate, changes also affected the Platon system. Among the innovations is the abolition of the transport tax deduction for the amount of payments into the system. We tell you how owners of heavy trucks can avoid mistakes when calculating the necessary contributions to the budget and how to return the overpayment, if any.

What tax collection procedure was in place for heavy trucks before 2020?

Until December 31, 2018, two types of payments were “assigned” to owners of heavy-duty transport:

- contributions to the Platon system, through which roads are repaired;

- regional transport tax allocated for road maintenance.

In addition, owners of cars with a maximum permitted weight of more than 12 tons had the opportunity to reduce the fuel charge by the amount listed in Plato.

It is important that only owners of heavy trucks registered in the system as tax payers for this vehicle could take advantage of this right (letter of the tax service dated July 11, 2021 No. BS-4-21/13355).

Tax calculation was based on the following rules:

- Records were kept for each vehicle separately. It was not possible to reduce the tax amount for one truck by the amount of contributions paid for another vehicle.

- A reduction in budget payments was allowed only in the case when in the reporting year the car “traveled” advance contributions to the system.

- If payments to Platon exceeded the accrued tax, the payer was completely released from the obligation. The difference between the amount of contributions and the transport tax was allowed to be taken into account in the tax base for profits.

- If the payment for damage to roads was less than the tax, the amount not covered by the funds spent on Platon was paid to the budget.

From January 1, 2021, the benefit with which car owners reduced the amount of transport tax was cancelled. In addition, innovations have complicated the accounting of expenses according to Plato. To be able to include them in total costs, you will need to separately account for payments into the system.

Cancellation of transport tax benefits: prospects for innovation

From 2021, the amount of payments paid to the Platon system does not matter for the purposes of calculating TN. According to the new rules, payers are required to pay taxes for all existing vehicles in full (letter of the Federal Tax Service No. BS-4-21 / [email protected] dated March 22, 2019).

Thus, all owners of heavy trucks are simultaneously responsible for calculating and paying advance payments of transport tax, as well as payment for travel on federal highways to the Platon system.

Article 12.21.3 of the Code of Administrative Offenses establishes a number of fines for failure to use the on-board device or for fraud with it.

Reflection of transport tax and Platon fee in accounting

The procedure for reflecting in accounting transactions for the calculation and transfer of “Platonovsky” fares with the subsequent deduction of transport tax in relation to heavy trucks is recommended by financiers in the Letter of the Ministry of Finance of the Russian Federation dated December 28, 2016 No. 07-04-09/78875.

The amount of the advance payment made to the operator of the state toll collection system, RTITS LLC, is not an expense and, accordingly, is not reflected in the cost accounts, but is taken into account as part of accounts receivable (clause 3, clause 16 of the Accounting Regulations PBU 10/ 99 “Expenses of the organization”, approved by Order of the Ministry of Finance of the Russian Federation dated May 6, 1999 No. 33n).

Thus, the transferred advance payment of funds to the Platon operator is reflected in the debit of account 76 “Settlements with various debtors and creditors.”

In accordance with clause 16 of PBU 10/99, expenses are recognized as a decrease in economic benefits as a result of the disposal of assets (cash, other property) and (or) the emergence of liabilities, leading to a decrease in the capital of this organization, with the exception of a decrease in contributions by decision of participants (owners of property ). Taking this into account, the amount of the “Platonic” fee payable by an economic entity is recognized as an expense in accounting.

Based on this and the Instructions for the application of the Chart of Accounts for accounting of financial and economic activities of organizations, approved. By Order of the Ministry of Finance of the Russian Federation dated October 31, 2000 No. 94n, the accrued amount of the “Platonovsky” fee is reflected in the debit of cost accounting accounts in correspondence with the account for accounting settlements with the budget.

This means that the full amount of the fare accrued by the operator RTITS LLC is included in expenses for ordinary activities during the period when the operator charges the fare (clause 18 of PBU 10/99).

When reflecting in the accounting records the transport tax due for payment to the budget at the end of the tax period, the amount of such tax minus the amount of the “Platonov” fee actually paid in a given tax period is credited to the account for accounting settlements with the budget.

INTRODUCTION OF DOWNTIME FOR REASONS NOT DEPENDING ON THE EMPLOYER

Important!

Advance payments for transport tax for heavy loads for which the “Platonov” fee has been paid are not reflected in accounting.

That is, in relation to heavy trucks for which the “Platonov” fee is paid, the transport tax is reflected in the accounting accounts at the end of the year and in terms of the excess of the transport tax accrued at the end of the calendar year over the toll accrued during this period.

Reducing transport tax

From July 3, 2021, transport tax can be reduced for payments to the Platon system . The payment reduces the amount of transport tax only for a specific truck weighing over 12 tons.

A company can take into account only one of two possible amounts as expenses:

- transport tax, which was reduced by the road tax if the tax was less than the tax;

- portion of the toll that exceeds the tax.

If a company has overpaid advances on transport tax for a cargo vehicle, they can be returned at the end of the year.

The question often arises: do you need to pay transport tax if you pay Platon?

If the amount payable to the system is equal to or greater than the amount of transport tax, you do not need to pay tax. If the fee is less, the owner reduces the tax by the amount he paid.

How to reduce transport tax on Platon?

Procedure for applying for tax reduction benefits, documents

Legal entities and individuals are in an equal position when it comes to the calculation and payment of transport tax. The tax is paid based on a notification from the Federal Tax Service.

To apply the benefit, the Federal Tax Service provides the following documents:

- statement;

- information about the owner of the vehicle (documents confirming ownership);

- vehicle passport (indicating the permitted weight over 12 tons);

- information on making payments for using the trails.

It is recommended to use extracts from the system’s Personal Account.

Documents are provided in person, through a representative, sent by mail (along with a list of attachments), through the Public Servants Portal (https://www.gosuslugi.ru/10054) or the “Taxpayer Personal Account” service (https://lkfl.nalog .ru/lk/).

An application for the “Platonov” benefit is sent to the Federal Tax Service before the tax inspectorate begins to generate notifications for the expired tax period.

The application is drawn up in two copies . The first is given to the inspection, the second remains with the applicant. Request that the inspector affix a stamp indicating acceptance of the application and documents from the current date.

The amount of transport tax, which is subject to transfer to the budget by car owners, is calculated by the tax authorities. Grounds - information provided to tax authorities by the authorities carrying out state registration of vehicles.

If the taxpayer is late in submitting the application, he remains entitled to the benefit. The amount of overpaid tax due to recalculation is returned for the period of recalculation.

An application for the return of overpaid funds must be submitted within three years from the date of payment of this amount. This means that individuals can provide documents that confirm their right to a deduction under the Platon system within three years from the date the right to the benefit arises.

Let’s find out how to include “Plato” in transport tax:

- At the end of the year, pay the difference between the tax and the fee for the year. The amount is taken from the operator's report. If the fee is greater than the tax, it may not be paid.

- In line 280 of the Tax Declaration, enter the code 40200. In line 290 - the fee for the year. Line 300 is the tax that was reduced by the fee. If the fee is larger, enter 0.

- In tax accounting, the difference between “Plato” and tax is taken into account in expenses. Example: the tax for the year was 14,000 rubles, the fee to the system was 11,000 rubles. Take into account only 3,000 rubles of tax.

- Advance tax payments on heavy goods vehicles can be calculated, but do not have to be paid. They are not reflected in the declaration. Calculated advance payments are also not taken into account in expenses.

The declaration is easy to fill out, but you must first confirm payment of the fee for using federal highways. Without this, the deduction will not apply.

Let's find out how to confirm the transport tax benefit using the Platon system.

Confirmation procedure

Car owners have the right to confirm the deduction if they meet the following conditions:

- vehicle weight exceeds 12 tons;

- The vehicle is included in a special register;

- the system submitted a report on the payment.

The report is generated once a year . It can be ordered through the official website or mobile application. First, create an account and enter the required information about the vehicle.

If it is more convenient for you to receive documents in paper form rather than electronically, go to the Platon representative office.

They also use their personal account:

- They go to the vehicles section, find the desired car, which gives the right to a deduction.

- In the “Request a Federal Tax Service certificate” section, indicate the period and confirm the entered data.

- The document will be automatically downloaded.

- The file is protected by an electronic signature. It is served without printing.

This document and other information about the vehicle owner will help you obtain a tax break. If you own several heavy trucks, repeat the above steps for each of them.

When is it impossible to reduce transport tax?

If the payers of the transport tax and the system are different persons, the deduction does not apply . This procedure is valid if the car is leased.

The heavy truck is registered to the lessor, but the recipient of the service (the one who moves the cargo on the vehicle) pays for the use of the routes.

Payment amounts are made not by the owner, but by the lessee . This solution to the problem is very fair, since the costs are borne by different individuals or companies.

The state system “Platon” was created to attract extra-budgetary funds for the development of road infrastructure. All funds received are used for road repair and development.

More than 25 billion rubles have already been collected for the Road Fund (https://www.rtits.ru/ru/press_centr/press_relizi/1/102).

There are more than 50,000 federal roads in the system. You can reduce transport tax using the Platon system . You only need to confirm your right to the benefit and also submit the necessary documents to the tax office.

Video: Plato reduces transport tax

FOR EXAMPLE

The company transferred an advance payment of 50,000 rubles to the operator of the Platon system. According to the report of the operator RTITS LLC, the fare for the first quarter of 2021 amounted to 20,000 rubles.

In the accounting accounts, these transactions will be reflected in the following accounting entries:

| Debit 76 “Settlements with the operator RTITS LLC” | Credit 51 “Current account” | — | 50,000 rub. | An advance payment was transferred to the operator RTITS LLC |

| Debit 20,23,25,26,29,44 | Credit 68 “Calculations with the budget using the Platon fee” | — | 20,000 rub. | Tolls for heavy trucks are taken into account as expenses for ordinary activities |

| Debit 68 “Calculations with the budget using the Platon payment” | Credit 76 “Settlements with the operator LLC RTITS” | — | 20,000 rub. | Payment of tolls for heavy trucks to the budget is reflected |

Questions and answers

- I am an individual entrepreneur and the owner of a heavy truck. Back in February, I sent documents to the Federal Tax Service regarding payment of payments to Platon, but I received a notification about the need to pay transport tax in full. What can be done in this case?

Answer: In this case, you need to contact the Federal Tax Service with an application and documents confirming payment of payments to the Platon system. You will be recalculated. Transport tax for 2021 must be paid by December 1, 2021.

2. I plan to lease a heavy truck, but I cannot figure out the responsibility for paying transport tax and payments to the Platon system. Who should pay for what?

Answer: The owner of a vehicle with a permissible weight of over 12 tons is required to pay transport tax, i.e. the lessor, but to pay a fee to compensate for damage caused to public roads of federal significance, i.e. payments to the Platon system are required by the user of the vehicle, i.e. lessee (in this case, you will be the lessee).

Note.

Accounting entries are provided for heavy cargo vehicles for which the “Platonov” fee is transferred. For other vehicles, advance payments are still made (if the Law of the subject of the Russian Federation provides for such a procedure), which are reflected quarterly in the accounting accounts (in the last month of the reporting quarter).

It should be noted that the company determines the procedure for accounting for fares independently and enshrines it in its accounting policy (clause 4 and clause 7 of the Accounting Regulations PBU 1/2008 “Accounting Policy of the Organization”, approved by Order of the Ministry of Finance of the Russian Federation dated 06.10.2008 No. 106n).

Therefore, the company may use a different accounting record scheme.

Accounting

Transport tax expenses are reflected in the accounting department in account 68. Transport tax relates to expenses for ordinary activities. The procedure for how it will be reflected in accounting depends on the organization in which the vehicle is used.

Here are the entries that reflect this tax:

- Dt 76 - Ks 51 - advance payment is transferred to the operator;

- Dt 20 - Kt 76 - the fee that was calculated for travel is included in expenses.

If this is provided for by the organization’s accounting policies, then the amount of fees that the operator transfers to the budget may additionally be reflected. This amount is reflected in the subaccounts of account 76.

What amount will expenses be reflected in tax accounting in the first quarter of 2021?

As already noted, for the purpose of calculating income tax, the “Platonovsky” fee is taken into account as part of other expenses, taking into account the restrictions provided for in clause 48.21 of Article 270 of the Tax Code of the Russian Federation.

Let’s assume that the amount of calculated advance payments for heavy cargo (the amount is determined solely for calculating tax liabilities, but is not reflected in the accounting accounts) amounted to 5,000 rubles.

Then for the first quarter of 2021 the company will take into account 15,000 rubles (20,000 rubles - 5,000 rubles) in tax expenses.

And the company does not include advance payments for transport tax as part of tax expenses, since advance payments are preliminary payments, the payment of which is provided for during the tax period (clause 3 of Article 58 of the Tax Code of the Russian Federation), and therefore take them into account on the basis of clause 1 Article 264 of the Tax Code of the Russian Federation is impossible.

That is, for each last day of the 3rd month of the 1st, 2nd and 3rd quarters, the “Platonic” fee can be taken into account in expenses in a portion exceeding the advance payment for transport tax calculated for the same truck and for the same quarter.

ACCOUNTING SERVICES FOR TRANSPORT AND LOGISTICS COMPANIES

How to pay advance payments

A payment made to the Platon program reduces the transport tax when paying for a specific heavy load and does not affect the taxation of other vehicles.

At the end of the year, it is necessary to reimburse the difference between the transport tax and the total amount of money contributed to the Platon system.

The amount of payment must be taken from the operator’s report.

If the aggregate of payments is greater than the tax, then the person does not have to pay the tax amount.

In the tax report, in the expenses column, the amount that is obtained when transport tax is deducted from the total amount of payments to the Platon system is recorded. if payments are greater than the tax amount, then you need to enter 0.

For example, the tax for the year was 15,000 rubles, and the amount of payments to Platon was 10,000 rubles. You must write 5,000 rubles in expenses, but payments are not subject to accounting.

If the tax was 4,000 rubles, and the payment to “Plato” was 7,000 rubles, then 3,000 rubles are included in expenses, and the tax amount is not taken into account.

Documentary evidence of transport tax deduction

The operator, in relation to each registered heavy load in the register of the toll collection system, maintains a personalized record of the owner (possessor) of the vehicle, containing the following information, updated at least once a day, for each vehicle of the owner (possessor):

- the route traveled by the vehicle;

- planned route;

- time and date of movement of the vehicle on public roads of federal significance in accordance with the route map;

- operations for the vehicle owner to pay a fee to the operator, indicating its amount, as well as the date and time of receipt;

- other operations.

Documentary evidence of the toll fee is the operator's report, which indicates the route of the heavy truck with reference to the time (date) of the start and end of the movement of heavy trucks, and primary accounting documents drawn up by the taxpayer himself, confirming the use of this heavy truck on the corresponding route (Letters of the Ministry of Finance of the Russian Federation dated 11.01. 2016 No. 03-03-RZ/64, dated December 28, 2015 No. 03-03-06/1/76740).

In order to recognize expenses for the purpose of calculating income tax, it is necessary to have documentary evidence of expenses (clause 1 of Article 252 of the Tax Code of the Russian Federation).

TAX BENEFITS FOR SMALL BUSINESSES USING THE EXAMPLE OF MOSCOW

Important!

The deduction when calculating transport tax in relation to heavy goods must be applied based on the amount indicated in the route map or register (for the corresponding calendar year) in relation to this heavy goods. And the use of a deduction when calculating transport tax in the amount of the advance payment paid to the toll collection system on account of planned routes is unlawful (Letter of the Ministry of Finance of the Russian Federation dated January 26, 2017 No. 03-05-05-04/3747).

Thus, the deduction of transport tax on the “Platonov” fee is applied based on the amount of the fee only for the route actually traveled by the heavy load.

Why was the Plato system introduced?

The Platon system was introduced in the Russian Federation in 2015. The reason for the adoption of this innovation was the calculation of damage to federal highways caused by heavy vehicles (weighing more than 12 tons). It has been established that 56% of damage to federal highways is caused by heavy trucks.

According to the Resolution of the Constitutional Court of the Russian Federation dated May 31, 2016 No. 14-P “In the case of verifying the constitutionality of the provisions of Article 31.1 of the Federal Law “On Highways and Road Activities in the Russian Federation and on Amendments to Certain Legislative Acts of the Russian Federation”, resolutions of the Government of the Russian Federation Federation “On levying a fee to compensate for damage caused to public roads of federal significance by vehicles with a permissible maximum weight of over 12 tons” and Article 12.21.3 of the Code of the Russian Federation on Administrative Offenses in connection with a request from a group of deputies of the State Duma” mandatory payment is collected to compensate for damage caused to public roads of federal significance, and as such relates to non-tax revenues of the federal budget. Mandatory payment is provided for in Art. 31.1 of the Federal Law of November 8, 2007 No. 257-FZ (as amended on August 3, 2021) “On highways and road activities in the Russian Federation and on amendments to certain legislative acts of the Russian Federation,” which states that the movement of vehicles, having a permissible maximum weight of over 12 tons, on public roads of federal significance is permitted subject to payment of a fee to compensate for the damage caused to roads by such vehicles .

Thus, this payment is intended to compensate for the costs associated with restoring the proper transport and operational condition of public roads of federal importance, i.e. has a target orientation and economic basis.

FOR EXAMPLE

RUB 3.73/km, coefficient 0.41

— the distance traveled by vehicles registered in the Toll System Register (km).

For example, 4,975.311 km.

| Balance at the beginning of period (rub.) | Accrued for the period (RUB) | Accrual adjustment (RUB) | Funds credited (RUB) | Refund/transfer of enrollment (RUB) | Balance at the end of the period (RUB) |

| 0 | 7 608,51 | 0 | 50 000,00 | 0 | 42 391,49 |

The amount of the fee to be paid when moving a heavy load along the planned route is indicated in the route map or calculated through a toll collection system based on data received from the on-board unit or a third-party on-board unit in automatic mode.

The calculation looks like this:

3.73 rub./km x 0.41 x 4,975.311 km = 7,608.51 rub.

In this case, the calculation takes into account the amounts for canceled route cards and adjustments made to charges for on-board devices.

Such a report is generated automatically from the state toll collection system “Platon”. A similar document is prepared by the operator of the state toll collection system, RTITS LLC, acting on the basis of the Order of the Government of the Russian Federation of August 29, 2014 No. 1662, the Decree of the Government of the Russian Federation of June 14, 2013 No. 504, of May 18, 2015 No. 474, dated 03.11.2015 No. 1191.

The extract is necessary to track the status of settlements on the “Platonic” fee.

It does not contain information about the dates of movement, numbers of heavy trucks.

To do this, you need to order details of transactions by travel date through the company’s personal account.

Detailed operations by travel date.

Plato and the transport tax

- Personal account on the official website. The program will ask you to provide some information and attach documents to the car. Registration takes place the next business day.

- If you are uncomfortable using the Internet, take documents for your car and personal (if you are an individual) or statutory (if a representative of a legal entity) documents and go to the User Information Support Center.

- Another way is a self-service terminal.

You can use this link to find your nearest service center or self-service terminal.

Operator Plato works on a deposit system, that is, the user first needs to top up the account and then hit the road.

The payment will be calculated and debited from your personal account automatically. If the deposit has been exhausted, in any case the debt must be repaid before the end of the reporting period.

Is it possible to reduce the transport tax by the amounts paid according to Plato?

- intended for transporting people (exception: passenger-and-freight vans);

- equipped with devices that provide light and sound signals for the work of the police, medical ambulance, fire department, emergency rescue services;

- intended for transportation of military weapons and equipment.

The Platon toll collection system was created and is used to ensure compliance with the procedure for collecting tolls to compensate for damage that was caused to public roads of federal significance. This is compensation for the destruction of highways by trucks.

The amount of transport tax for trucks weighing over 12 tons can be reduced by a fee to compensate for the damage caused to roads by such heavy trucks.

And if the amount of the “road toll” exceeds the amount of the transport tax, the remainder can be taken into account when calculating income tax or when calculating the single tax according to the simplified tax system.

The relevant amendments to the Tax Code were adopted by the State Duma in the third reading and sent for consideration to the Federation Council.

We recommend reading: State duty for registering a garden house

Another amendment concerns “simplified workers” with the object “income minus expenses”: they will be able to reduce the single tax by part of the amount of “road toll” that exceeds the amount of transport tax (subclause 37, clause 1, article 346.16 of the Tax Code of the Russian Federation).

But after the amendments come into force, organizations on OSNO will also be able to reduce the tax base for income tax only by part of the amount of “road toll” that exceeds the amount of transport tax (clause 48.21 of Article 270 of the Tax Code of the Russian Federation).

Thus, legislators have established the same approach to accounting for “road tolls” in expenses under the simplified tax system and under the general taxation regime.

Transport tax and the Platon system

If the fee to the Platon system is equal to or higher than the amount of transport tax that is payable, then the tax is considered equal to zero. If the amount of transport tax is higher than the fee paid to the Platon system, then a benefit is provided for the amount of the fee paid. This benefit is provided for each heavy load for which the taxpayer pays a fee.

Organizations and individual entrepreneurs that are payers of transport tax and have cars with a maximum weight of more than 12 tons must be registered in the appropriate register (that is, payers of the Platon system) calculate the tax in a special manner. Since November 15, 2015, owners of such heavy trucks are required to pay a fee for damage caused by their multi-ton trucks to roads. If these vehicles are driven on toll roads, then this fee is not charged.

Transport tax and the Plato system (nuances)

The transport tax and the Platon system, through which payments for heavy vehicles are collected, in the period 2016–2018 do not lead to an increase in the tax burden on the payer. For information on how transport tax fees and the Plato system are linked in this regard, read the article.

This report provides the following data:

Account number, balance, number of heavy loads and then details of transactions by date and heavy load.

| Movement date | GRZ | Type of transaction | Path along the federation routes, km | Enrollment | Write-off |

| 30.12.2016 | E285VA174 | Charging (BC) | 75.129 km | RUB 114.88 | |

| 30.12.2016 | E275MA174 | Charging (BC) | 74.03 km | 115.22 rub. |

At the end of the year, you can confirm your right to deduct transport tax using the report “Information on motor vehicles with a permissible maximum weight of over 12 tons, as well as information on payment of payment for compensation for damage caused to federal highways,” which is generated for each heavy load (Letter of the Federal Tax Service of the Russian Federation dated August 26, 2016 No. BS-4-11/15777).

Procedure for paying fees in 2021

Operator Plato works on a deposit system, that is, the user first needs to top up the account and then hit the road. The payment will be calculated and debited from your personal account automatically. If the deposit has been exhausted, in any case the debt must be repaid before the end of the reporting period.

For late payment, lack of a portable on-board terminal or failure to submit a route card, the car owner will be fined. According to Art. 12.21.3 of the Code of Administrative Offenses of the Russian Federation, the fine will be 5,000 rubles for a primary violation and 10,000 for a secondary violation.

You can make a deposit using one of the following methods:

- If the owner is a legal entity, then the fastest and easiest way is to make an advance payment by bank transfer from your current account

- Payments are also available in your personal account (you can log in if you have Internet access from any personal PC, tablet, or smartphone)

- Using a self-service terminal

- In the User Service Center

- E100 and DKV fuel cards

When calculating the tax base of the transport tax, payments for travel on federal highways are taken into account. For owners of cars with a maximum permissible weight over 12 tons, advance deductions for transport tax are not provided.

Organizations calculate the tax amount independently, individuals receive notifications from the tax office.

So, payments for travel on federal highways according to the Plato system and transport tax in 2021 are linked quite logically and do not duplicate each other.

Where can the owner(s) of the vehicle obtain such information?

Information interaction between the owner and operator is carried out through the use of the following service channels:

- user information support centers;

- information resource of the toll collection system, located on the Internet information and telecommunications network (www.platon.ru), and the personal account of the owner (owner) of the vehicle, which ensures that the owner (owner) of the vehicle is provided with information contained in the personalized record of the owner (owner) of the vehicle funds that include a settlement entry(s);

- a user information support center, which is a complex of technical means without personnel, providing, among other things, the possibility of registration in the toll collection system and payment of fees by the owner (possessor) of the vehicle.

Important!

All of the above reports can be generated by the owner of heavy trucks through his personal account on the official Platon website (https://platon.ru) or in a similar mobile application.

Is it always possible to reduce transport tax when using the Plato system?

Both individuals and legal entities can count on a reduction in transport tax:

| Car owner | Who calculates the amount of transport tax? | How is transport tax paid? |

| Individual | Inspectorate of the Federal Tax Service | After receiving a notification about the need to pay transport tax |

| Entity | Legal entity independently | After making an independent calculation |

Attention should be paid to the fact that only the owner of the vehicle who makes payments to the Platon system can claim a tax deduction for the amount of payment to the Platon system.

According to Letter of the Ministry of Finance of the Russian Federation dated July 18, 2021 No. 03-05-04-04/41940, certain rules apply to vehicles with a permissible weight of over 12 tons that are leased:

| Pays transport tax | Makes payments to the Platon system | Providing a tax deduction |

| Lessor* | Lessee** | No |

*Lessor is a party to a leasing agreement who acquires ownership of the property and provides it as a leased asset to the lessee for temporary possession.

**Lessee is an individual or legal entity who, in accordance with the leasing agreement, is obliged to accept the leased asset for a certain fee, for a certain period and under certain conditions for temporary possession and use.

Thus, if a heavy vehicle is registered to a lessor who pays transport tax, and the lessee makes a payment to the Platon system, the transport tax will not be reduced by the amount of the fee paid to the Platon system.

Reflection of the “Platonov” fee in the transport tax return

The transport tax declaration, in which the taxpayer can indicate a tax benefit and (or) deduction for a vehicle with a permissible maximum weight of over 12 tons, was approved by Order of the Federal Tax Service of the Russian Federation dated December 5, 2016 No. ММВ-7-21/ [email protected]

Despite the fact that the Order of the Federal Tax Service is in effect starting with the submission of a tax return for 2021, those taxpayers who need to apply the heavy-duty exemption could already report using the new form for 2021 (clause 3 of the Letter of the Federal Tax Service of the Russian Federation dated December 29, 2016. No. PA-4-21/ [email protected] ).

Tax benefits of the Platon system

Many motorists are interested in the question: how to reduce transport tax? Not long ago, some innovations were approved regarding the Plato system. According to them, a tax benefit was established for some vehicles. It applies to both individuals and legal entities.

If, according to the Platon system, the amount of payments is greater than the transport tax or equal to it, then there is no need to pay the tax. Individuals can apply for a reduction in the amount of transport tax. Legal entities will have to apply for the benefit through a tax return. All organizations that have a benefit will be exempt from paying advances on transport tax.

Any taxpayer can recalculate taxes from the date of entry into force of “Plato” and reduce the tax deduction.

To achieve a reduction in payments, you must provide an application, documents for the vehicle, a car passport, and data on payments made.

It is also recommended to make extracts from the Plato system.