Accounting under the simplified tax system

Accounting in organizations using the simplified tax system is mandatory.

Most often, they belong to small businesses (SMB), and have the right to carry out accounting in a simplified form. In addition, they keep books of income and expenses, which for this taxation system are tax registers. Read about the nuances of accounting under the simplified tax system in the article “Procedure for maintaining accounting under the simplified tax system (2020)”

An accounting register, which is an attribute of both complete ordinary and complete simplified accounting, is understood as a document in which all transactions are systematized by accounts and recorded in chronological order. For example, in account 51, a register is needed so that it can be seen for what purposes the funds were used.

The register forms are approved by the director of the company (Clause 5, Article 10 of Law No. 402-FZ).

The information summarized in the registers is transferred to the turnover sheet, and then to the financial statements. To record information in full simplified accounting, simplified accounting forms can be used - statement forms (Appendices 2–11 to Order of the Ministry of Finance dated December 21, 1998 No. 64n).

When using abbreviated or simple simplified accounting, instead of registers, they use a book for recording the facts of economic activity (Appendix 1 to the order of the Ministry of Finance dated December 21, 1998 No. 64n), and to record wages - form B-8 (Appendix 8 to the order of the Ministry of Finance dated December 21, 1998 No. 64n).

The report on the simplified tax system is prepared in a declaration in the form approved by order of the Federal Tax Service of Russia dated February 26, 2016 N ММВ-7-3/ [email protected]

For information about when you need to submit a “simplified” declaration, read the article “What are the deadlines for submitting a declaration under the simplified tax system?” .

For the declaration form and a sample of how to fill it out, see the article “Declaration under the simplified tax system for the year - how to fill it out?”

Before calculating tax in an accounting program, it is important to calculate it correctly. ConsultantPlus experts explained in detail how to do this. Full trial access to K+ is available for free. If you apply the simplified tax system “income”, this ready-made solution will help you, and if “income minus expenses” - then this material is for you.

Expenses when accounting for the single tax simplified tax system

For those entrepreneurs and organizations that pay tax on net income (minus expenses), it is important to know exactly what costs can be taken into account when calculating budget payments and what expenses can be recognized when determining the tax base. If you use the simplified tax system, then you have the right to recognize the following types of expenses:

- purchase of fixed assets necessary in the course of business (furniture, equipment, computer, etc.);

- purchase of consumables;

- purchasing goods that you plan to resell;

- input VAT;

- other taxes and fees;

- telecommunications services;

- utilities and maintenance services (for example, electricity reimbursement to the landlord);

- payments for employee insurance.

How to take into account expenses and how to reduce the tax base - see the example below.

Master Plus LLC uses the simplified tax system (the “income minus expenses” scheme).

On December 18, 2016, an agreement was concluded between “Master Plus” and the telecom operator “Telecom”, according to which “Master Plus” has the opportunity to send reports to statistical authorities in electronic form. The agreement provides for the following conditions:

- validity period of the agreement is 01.01.-31.12.2017;

- Telecom provided services for the production of an EDS key (electronic digital signature);

- “Master Plus” receives the right to use the software for sending electronic reports (one-time payment under the agreement - 9,325 rubles, VAT 1,422 rubles);

- Telecom undertakes to provide monthly subscription services to Master Plus (annual payment 6,340 rubles, VAT 967 rubles).

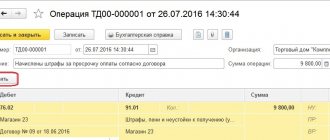

The Master Plus accountant made the following entries in the accounting:

| date | Debit | Credit | Operation description | Sum | A document base |

| 31.12.2016 | 60 | 51 | Payment under the contract was transferred to Telecom's account (RUB 9,325 + RUB 6,340) | RUB 15,665 | Payment order |

| 31.12.2016 | 97 | 60 | The right to use the software is accounted for as deferred expenses (RUB 9,325 – RUB 1,422) | RUR 7,903 | Agreement for the provision of telecommunications services |

| 31.12.2016 | 19 | 60 | The amount of VAT on the cost of the right to use the software has been calculated | 1.422 rub. | Invoice |

| 31.01.2017 | 26 | 60 | Expenses for Telecom subscriber services were paid in January 2021 (RUB 6,340 / 12 months) | 528 rub. | Certificate of completed work for January 2017 |

| 31.01.2017 | 26 | 97 | Written off deferred expenses for January 2021 (RUB 7,903 / 12 months) | 659 rub. | Agreement for the provision of telecommunications services |

| 31.01.2017 | 26 | 19 | VAT on the cost of software is reflected in expenses for January 2021 (RUB 1,422 / 12 months) | 119 rub. | Invoice |

To determine the tax amount for 2021, the Master Plus accountant did not take into account expenses under the agreement with Telecom. In 2021, the monthly amount of 1,306 rubles is included in the Master Plus expenses. (528 RUR + 659 RUR + 119 RUR).

Accounts used in transactions for calculating tax under the simplified tax system

The reliability of the compiled balance sheet depends on the correctness of the reflection of the company’s economic activities in the accounting documents. This is ensured by accounting entries accompanying each financial transaction. Each fact of the company’s economic life must be recorded in its own way. This will create a perfect balance.

To organize using the simplified tax system, you need to correctly reflect costs and income in accounting. To generate transactions for the accrual and payment of income tax (for both options), the following accounts are used:

- account 51 - all transactions on receipt and debit of funds are recorded on it;

- account 68 - accrue income tax, including quarterly advances on it; records for other taxes are also made here;

- account 99 - reflects the amount of accrued simplified tax.

When calculating the simplified tax system, the following posting is used:

Dt 99 Kt 68.

Accounts used

The accounting entry for calculating the simplified tax system is made using the following accounts:

- account 51 “Current accounts” - used to reflect all cash movements in the organization’s accounts;

- account 68 “Calculations for taxes and fees” - with its help the accounting entry is reflected - the calculation of the simplified tax system tax, as well as other operations for settlements with the budget, in accordance with clause 4 of PBU 1/2008, sub-accounts for this account must be recorded in the accounting policy , otherwise the posting of tax accrual to the simplified tax system will be made incorrectly;

- account 99 “Profit and losses” - is intended to summarize information on the formation of the final financial result of the organization’s activities in the reporting year.

The tax has been calculated according to the simplified tax system - we make the posting

Upon completion of each business transaction, the accountant reflects this fact with an accounting entry. The accounts used depend on the chart of accounts adopted by the company.

To keep records of various taxes, subaccounts are allocated in account 68. Their list must be specified in the accounting policy, guided by clause 4 of PBU 1/2008.

Account 68 can be divided into several sub-accounts, for example:

68.1 - calculations for the simplified tax system;

68.2 - calculations for personal income tax, etc.

A situation is possible when, at the end of the year, the total income tax turns out to be either more than the actual tax amount or less. In the first case, the tax amount must be added, in the second, it must be reduced. The wiring is as follows:

- simplified tax system accrued (posting for advance tax payment) - Dt 99–Kt 68.1;

- tax advance is transferred - Dt 68.1 - Kt 51;

- for the year, additional tax was accrued to the simplified tax system - posting Dt 99 - Kt 68.1;

- the tax according to the simplified tax system for the year was reduced (the excessively accrued advance was reversed) - reversal Dt 99 Kt 68.1.

The total amount of tax accrued for the year according to the declaration must be equal to the amount reflected in the accruals for the same period in accounts 99 and 68.1. If more advances are transferred than the tax accrued for the year, then the overpayment amount can be returned.

For information on how to write an application for a refund of overpaid tax, read the article “Sample application for a refund of overpaid tax .

How an LLC uses the simplified tax system to keep records of income and expenses, as well as what kind of reporting to submit, read in the Typical situation from ConsultantPlus. And if you are close to losing the right to use the simplified tax system, find out how the limits will change from 2021 by studying the explanations of ConsultantPlus experts. If you do not have access to the K+ system, get a trial online access for free.

Examples of tax calculations according to the simplified tax system with the object income minus expenses and with the object income

All transactions performed by the organization must be reflected in the accounting accounts.

This can be done using wiring. According to the Federal Law of 06.12. 2011 No. 402-FZ, individual entrepreneurs have the legal right not to conduct accounting and not to go into the nuances of drawing up postings.

But in practice, many entrepreneurs prefer to follow the canons of accounting.

Simplified organizations must maintain accounting records. Despite the fact that the postings do not depend on the taxation system, simplified tax calculations and the formation of corresponding accounting records have a number of features.

Tax under the simplified tax system must be calculated and paid once at the end of the year.

In addition to the tax, the simplifier must calculate advance payments based on the results of three periods: 1st quarter, six and nine months (Article 346.19 of the Tax Code of the Russian Federation).

The tax is calculated on an accrual basis and transferred to the state treasury in full rubles.

Tax under the simplified tax system with the object “income minus expenses”

To calculate the amount of the advance payment, you need to find the difference between the income and expense parts for the reporting period and multiply it by the tax rate.

The amount minus previous advances must be sent to the state budget. The tax rate is most often 15%, but at the discretion of the constituent entity of the Russian Federation it can be reduced (clause 2 of Art.

346.20 Tax Code of the Russian Federation).

The tax is calculated in a similar way. To find out the annual tax to be paid, advance payments should be subtracted from the calculated amount. Tax (advance payment) is calculated by posting:

Debit 99 Credit 68

When writing off tax from a bank account, the accountant needs to make an entry:

Debit 68 Credit 51

Let's look at tax calculation using an example.

According to the reporting documents, Topol LLC managed to earn 120,000 rubles in 2021, while expenses amounted to 75,000 rubles. The following indicators were obtained during the reporting periods:

1st quarter

Income - 10,000 rubles;

Accepted expenses are 1,000 rubles.

Having made the calculation, the accountant received a value of 1,350 rubles ((10,000 - 1,000) x 15%). It is for this amount that you need to draw up a payment order, indicating in the purpose “advance payment for the simplified tax system for the 1st quarter of 2021.”

Debit 99 Credit 68 1,350 rubles - advance payment accrued for the 1st quarter of 2021;

Debit 68 Credit 51 1,350 rubles - advance payment transferred to the Federal Tax Service.

1st half of the year

Income (January - June) - 60,000 rubles;

Accepted expenses (January - June) - 18,000 rubles.

When calculating, the accountant took into account the payment for the 1st quarter. It turned out that the debt to the Federal Tax Service is 4,950 rubles ((60,000 - 18,000) x 15% - 1,350).

Debit 99 Credit 68 4,950 rubles - advance payment for 6 months is reflected;

Debit 68 Credit 51 4,950 rubles - advance payment transferred to the Federal Tax Service.

9 months

Income (January - September) - 100,000 rubles;

Accepted expenses (January - September) - 53,000 rubles.

The accountant made a payment in the amount of 750 rubles and sent the money to the Federal Tax Service ((100,000 - 53,000) x 15% - 1,350 - 4,950).

Debit 99 Credit 68,750 rubles - advance payment accrued for 9 months of 2021;

Debit 68 Credit 51,750 rubles - advance payment sent to the Federal Tax Service account.

Year

Income (January - December) - 120,000 rubles;

Accepted expenses (January - December) - 75,000 rubles.

The tax for the year without deducting advance payments is 6,750 rubles ((120,000 - 75,000) x 15%).

For the entire 2021, advance payments in the amount of 7,050 rubles (1,350 + 4,950 + 750) were sent to the tax office account.

As you can see, this amount is more than the final tax for the year. Therefore, there is no need to pay anything extra to the state budget at the end of the year.

This results in a tax overpayment of 300 rubles.

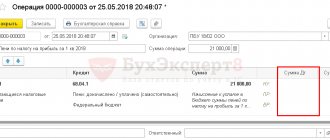

In order for the accounting data to match the actual calculations, you need to make an entry to reduce the tax:

Debit 68 Credit 99,300 rubles - reduced tax according to the simplified tax system.

If at the end of the year a tax is due for additional payment, a standard entry is generated:

Debit 99 Credit 68

Note! If a company has a taxable object of “income minus expenses”, it must also determine the minimum tax. To do this, the total income must be multiplied by 1% (clause 6 of Article 346.18 of the Tax Code of the Russian Federation).

Let's calculate the minimum tax based on the initial data.

120,000 x 1% = 1,200 rubles - this means that Topol LLC must pay at least 1,200 rubles to the state budget at the end of the tax period. In 2021, the tax was 6,750 rubles, which is more than the minimum wage. Consequently, the company will not have to pay anything extra to the state.

Tax under the simplified tax system with the object “income”

Advance payments and the tax itself are calculated based on a rate of 6% (Article 346.20 of the Tax Code of the Russian Federation). Some regions may apply rates below the norm. The accrual of tax (advance payment) is reflected by the posting:

Debit 99 Credit 68

When writing off taxes from a current account, the accountant needs to make the following entry:

Debit 68 Credit 51

Let's look at how to calculate the “simplified” tax using an example.

Individual entrepreneur Georgy Vasilievich Vasnetsov earned 450,000 rubles in 2021. In February, the businessman sent fixed contributions in the amount of 23,153.33 rubles from his bank account. An individual entrepreneur can legally reduce tax and advances on it by this amount.

1st quarter

Individual entrepreneur’s income is 20,000 rubles.

The accountant keeping records of individual entrepreneurs calculated the advance payment using the formula: 20,000 x 6% = 1,200 rubles. In order to avoid paying tax, the accountant reduced it by the transferred insurance premiums.

Since they significantly exceed the advance amount, there is no need to transfer anything to the tax office in the first quarter. Accordingly, no tax should be charged; there will be no postings.

1st half of the year

Income of individual entrepreneurs (January - June) - 150,000 rubles.

The accountant determined the possible payment amount: 150,000 x 6% = 9,000 rubles. Once again, the accountant takes the opportunity to reduce tax by the amount of contributions - 9,000

9 months

Income of individual entrepreneurs (January - September) - 150,000 rubles.

In the 3rd quarter, Vasnetsov earned nothing, there were no accruals, no transactions were generated.

Year

Income of individual entrepreneurs (January - December) - 450,000 rubles.

The specialist calculated the tax for 2021: (450,000 x 6%) – 23,153 = 3,847 rubles.

Since there were no advance payments throughout the year, the tax was reduced only by fixed contributions.

The accountant showed the accrued tax by posting:

Debit 99 Credit 68 3,847 rubles - “simplified” tax accrued for 2016;

Debit 68 Credit 51 3,847 rubles - tax was transferred to the inspectorate according to the simplified tax system.

As can be seen from the examples, the taxation object does not affect transactions. The postings for advance payments and the tax itself are absolutely identical. The only difference is in the calculations.

Elena Rogacheva

Keep records on the simplified tax system in Kontur.Accounting - a convenient online service for calculating wages and benefits and sending reports to the Federal Tax Service, Pension Fund of the Russian Federation, Social Insurance Fund and Rosstat. The service is suitable for collaboration between an accountant and a director.

Try free for 30 days

Results

Reflection in accounting of accrued tax under the simplified tax system is reflected in synthetic accounts 99 and 68. To maintain analytical accounting for synthetic accounts 68, 99, separate sub-accounts are opened, which must be indicated in the working chart of accounts and approved by the head of the organization (clause 4 of PBU 1/2008 ).

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

How to fill out a balance under the simplified tax system?

Filling out the balance sheet under the simplified tax system should begin by filling out all the data about the organization that is indicated in the balance sheet header. The balance lines are filled in in order. The procedure for filling out a balance under the simplified tax system is as follows:

In the line “Tangible assets” indicate the residual value of the enterprise, as well as capital invested in turnover.

In the line “Intangible assets” you should indicate all assets for scientific research, exploration assets, taxes, as well as other non-current assets.

The line “Financial assets” displays all current funds, with the exception of cash reserves.

The line “Debt obligations” includes those funds that the organization took on credit or a loan.

The “Balance Sheet” line contains the total total of all assets of the enterprise.

All other lines are filled out in the same way as in a regular balance sheet.

Usn tax penalties income tax expenses

Tax under the simplified tax system is no exception, and if it is not paid on time, penalties will be charged. The advance payment for the simplified tax system for the 1st quarter of 2021 was paid on April 30. BCC for payment of penalties under the simplified tax system (USN) income minus expenses (15 percent). Tax penalties when calculating income tax in expenses are not taken into account in clause 2 of Art. 270 Tax Code of the Russian Federation. The KBK penalty for the simplified tax system for income 2017-2018 differs both from the KBK for the tax itself and from the KBK for penalties for the object of taxation “income minus expenses.” UTII is often more profitable than the general tax and even the simplified tax system.

Tax under the simplified tax system, when the object of taxation is applied: - “income”. Hello, we have an LLC using the simplified tax system for income and expenses. How to take into account profits from previous years in 2021. When using the abbreviated account or account 68, tax is charged on income, including quarterly advances on it; records are also made here for other taxes. Analytics Income tax and similar payments are used when calculating (additionally accruing) income tax or other taxes, which, for example, are a trade fee or a tax under the simplified tax system. In our article we will look at the BCC, which should be indicated to the “simplified” person when listing penalties according to the simplified tax system. Currently, income tax penalties are levied in accordance with the simplified tax system for UTII Tax on income from the sale of an apartment Tax deduction for the purchase of a plot Income tax refund, review. Penalties do not relate to tax sanctions, and therefore they are taken into account in practice. In practice, penalties are taken into account in different ways: some experts attribute tax penalties to the account. The list of expenses is disclosed in PBU 10/99, and among those listed there are also no tax penalties. 02/27/2018 How to divide the proceeds from the sale of purchased goods and your own goods, works, services in the income tax return?

Accrual of simplified tax system: postings

upon payment.

Subjects of the Russian Federation in their legislation can establish a zero rate for newly registered business entities operating in the production, scientific, social spheres or in the provision of consumer services to the population.

Only income received and expenses paid are included in calculations for reporting periods. Costs are grouped by items and elements, including them in the cost price: depreciation, materials, labor costs and transfers to funds, social services, energy consumption, and others. Expense postings under the simplified tax system are standard - they are accumulated according to cost items, reducing the amount of revenue received.

In accounting for sales they use , shipped goods - . The calculation of the single tax in a company’s accounting is identical to the calculation of income tax and is carried out in stages - they determine, calculate the amount for the reporting quarter, and at the end of the year, calculate the final amount of tax payable.

The accrual of the simplified tax system is recorded by posting: D/t “Profits and losses” C/t “Calculations for taxes/fees”. This entry records the calculation of the advance payment for each reporting period - quarter and the total tax amount at the end of the financial year.

Accrual of penalties for postings upon registration

and, accordingly, do not take part in the formation of accounting profit. To reflect obligations for mandatory payments to the budget, account 68 is provided.

The reliability of the compiled balance sheet depends on the correctness of the reflection of the company’s economic activities in the accounting documents.

Analytical accounting is built from subaccounts that describe each tax or fee that must be paid by the enterprise within a certain period.

The account is active-passive. Tax and other payments to the budget are accrued using the correspondence of credit 68 with the debit of the account to which they relate. For example, income tax is reflected by posting Dt 99 Kt 68 using the corresponding sub-accounts. Accounting recognizes penalties as another expense, which in no way participates in determining the tax base when calculating income tax.

Clause 83 of the PBU and the Instructions for using the standard chart of accounts allow you to make sure that obligations of this kind should really be reflected on account 99. Payment of the advance payment

Posting fines

In addition to penalties, for late payment, regulatory authorities may charge penalties based on 1/300 of the refinancing rate of the Central Bank of the Russian Federation (Article 75 of the Tax Code of the Russian Federation). Penalties = Tax arrears x Number of calendar days of delay x 1/300 of the refinancing rate. Penalties begin to accrue from the next day after the tax payment deadline.

Often the violator of the contract refuses to pay the fine. In this case, you can file a lawsuit. If the court makes a positive decision, the counterparty will be required to pay a fine. Most likely, the violator will be required to reimburse court costs and the state fee paid by the plaintiff for the consideration of the case in court.

Are tax penalties accepted as expenses when recording transactions?

In January 2014, Standard LLC paid its employees the December salary accrued to them in 2013. Due to the fact that the organization is also engaged in the production of building materials, 60% of the employees are production workers. In the same month, the organization’s employees were paid wages for January, which will be paid in February 2014. Insurance premiums accrued on the December salary in December 2013 are transferred to the funds in January 2014, and contributions accrued on the January salary in January are transferred in February 2014.

Due to the fact that not all expenses can be taken into account in tax accounting under the simplified tax system, it is important to determine the type of expenses and then select the appropriate account for their reflection in accounting in accordance with the Chart of Accounts and the Instructions for its use. The adopted methodology for accounting expenses must be reflected in the accounting policy, which must be approved by the head of the organization. In addition, based on the general Chart of Accounts, you should also develop your own working chart of accounts, which will become an annex to the adopted accounting policy.

Reporting when using the simplified tax system

Sometimes, based on the results of the period, the company is subject to the calculation and payment of the minimum tax of the simplified tax system, which is generally reflected in the accounting entries. In this case, it is necessary to submit an application to the Federal Tax Service requesting that advances be credited to the tax account. To calculate the minimum amount of tax due to the simplified tax system, the following accounting entries are used:

- KUDiR is generated in the “Reports” menu.

- The declaration is filled out in the appropriate “Reports” tab, “Tax reporting” section. In reporting, the tax amount is automatically calculated in accordance with which scheme the enterprise uses on the simplified tax system - “income” or “income minus expenses”.

- Tax calculation must be done manually in the “Operations” menu, section “Operations entered manually”.

- Postings: accrual D 99.01.1, K 68.12.