The functioning of the state structure is largely determined by tax revenues. The objects of taxation are, among other things, income received. One of their varieties is dividends, which represent part of the income from an operating business, which is distributed among its owners based on the profit received by the organization. Let us consider in more detail the question of what the concept of dividend tax hides and who is obligated to pay it.

Are dividends taxable?

Due to the fact that dividends are one of the types of income, their amount is subject to tax. However, the amount of tax on dividends depends on a number of factors. First of all, what category the payer belongs to: an individual or a legal entity plays a role. Also of great importance is the fact of whether the payer is a resident of the Russian Federation.

Gold debit card from Sberbank - up to 5% bonuses THANK YOU

Apply now

Dividend tax for individuals in 2021

The last increase in the dividend tax rate took place in 2015. Currently, for individuals, the tax rate on dividends is:

- 13% for residents;

- 15% for non-residents.

One should not confuse the status of a resident of a country with the citizenship one has. It should be remembered that the status of a resident of the Russian Federation is assigned provided that the person has been on its territory for a total of at least 183 calendar days over the past year. It is important to note that the total count also includes days spent abroad for a valid reason (for example, due to the need for treatment or training). Therefore, a foreign citizen can also be a resident.

What taxes are received dividends subject to?

Dividends are treated as income or profit for tax purposes. To calculate tax deductions from them, you need to know to whom the payments were made and under what conditions.

VAT

Dividends are not subject to value added tax, since they are not material value for resale. Although there are precedents. Sometimes property or material assets are transferred as dividends.

If the recipient of dividends is a legal entity or individual entrepreneur, then the fiscal services impose VAT on the transferred property or valuables. The court takes the side of the recipient, with rare exceptions.

Income tax

For investors - legal entities, the situation is clear: income from investments is subject to income tax. An organization that owns shares or liabilities, shares in the authorized capital of an enterprise paying dividends for more than 1 year is exempt from payment.

In this case, the amount of investment must be at least 50%. The broker-tax agent is required to calculate and transfer the fiscal fee.

Personal income tax

Dividends intended for payment to individuals are subject to income tax. The duty of the tax agent is to calculate and transfer the amount of personal income tax to the fiscal authorities. Shareholders receive the amount remaining after paying personal income tax.

How to pay tax on dividends

Responsibility for transferring the required taxes from the amount of dividends to the budget lies with the company itself. In other words, persons who are among the founders receive dividends after their taxation has been carried out. Thus, if this type of income is paid in cash, then the organization itself acts as a tax agent.

If dividends are not paid in cash

Special attention should be paid to the consideration of the situation when the payment of dividends occurs in a different form (for example, as a transfer of fixed assets, goods or any other property). Under such circumstances, the organization must notify the tax office of the impossibility of making the required payments, after which the responsibility to pay taxes on dividends of individuals passes to the citizen himself. Their repayment occurs as follows: at the end of the reporting period, you must submit a tax return in Form 3-NDFL and make the corresponding payment to the budget yourself. It should be borne in mind that receiving dividends in the form of property is further complicated by the fact that tax officials consider it as a sale of goods, as a result of which the taxable value is calculated based on which taxation system the company adheres to. In the event that the adopted system imposes obligations to pay additional tax on sales due to a transaction for the transfer of property, double taxation occurs. Even if the case is brought to court, the latter do not always recognize the lack of implementation process, so such situations are best avoided if possible.

Tinkoff Black debit card from Tinkoff Bank - cashback for purchases

Apply now

Nuances of calculating taxes on dividends

When calculating tax on dividends, it is important to consider the following features:

- The total amount of distributed dividends (in the formula this is indicator D1 and the denominator of indicator K) includes, among other things, dividends in favor of:

- foreign - non-residents of the Russian Federation.

This follows directly from paragraph 5 of Art. 275 of the Tax Code of the Russian Federation (as well as from letters of the Ministry of Finance of Russia dated July 8, 2014 No. 03-08-05/33030 and the Federal Tax Service of Russia dated August 12, 2014 No. GD-4-3 / [email protected] ).

- The total amount of dividends should include those from which the “profitable” tax is not withheld (paragraph 6, paragraph 5, article 275 of the Tax Code of the Russian Federation). In particular, dividends on shares that are state or municipally owned or that constitute the property of mutual funds and public legal entities (letter of the Ministry of Finance of Russia dated June 11, 2014 No. 03-08-05/28295).

- Dividends for past periods are taxed at the rate that is established on the date of issue of these dividends (letter of the Federal Tax Service of Russia for Moscow dated March 14, 2007 No. 20-08 / [email protected] ).

- Indicator D2 takes into account dividends (not counting those taxed at a zero rate) received from both domestic and foreign companies. Moreover, they are taken into account in the so-called pure form, that is, without the tax that the source of payment withheld from them (letter of the Ministry of Finance of Russia dated June 11, 2014 No. 03-08-05/28295).

- If the calculation results in a negative tax amount, then the agent does not need to pay tax. But he won’t be able to get the difference from the budget. This is directly stated in paragraph. 9 clause 5 art. 275 Tax Code of the Russian Federation.

- An organization paying dividends through tax agents must notify about the values of indicators D1 and D2 used in the calculation no later than 5 days from the date of determining the circle of persons entitled to receive dividends (if the organization is an issuer), but no later than the day of their payment each of the tax agents. Notification is carried out by sending information electronically or on paper or posting it on the website or in a payment document for the transfer of money (clauses 5.1 and 5.2 of Article 275 of the Tax Code of the Russian Federation).

See also the material “How to correctly calculate income tax on dividends?” .

Taxes on share dividends

The tax rate depends on the status of the investor:

- individual or company;

- resident or foreign citizen (company).

If dividends from US stocks

All US stocks are purchased exclusively through brokers. Taxes are paid in two ways:

- when US shares are purchased on a Russian stock exchange - in this case, the broker will be responsible for accruals and payments;

- if the shares were purchased through an American broker, taxes on dividends on US shares will have to be paid by the investor himself.

To avoid double taxation, you need to use a special form and withhold 10%. If they were withheld, then all that remains is to pay the remaining 3% to the budget. If a person invests in US companies, then he must sign Form W-8BEN. This paper will confirm that the person is not a US citizen, so he will not have to pay 30%.

They pay taxes once a year. To do this, the investor fills out a declaration and sends it to the Federal Tax Service. This must be done at the place of registration.

Taxes on dividends on shares of Russian companies are 13% of the amount of dividends received. A foreign company pays 15% if it buys Russian shares.

Accounting entries for dividend payments

In accounting, dividend payments are recorded by postings on the date when the participants’ decision to pay them was made.

The recipient and the payer have accounting entries reflected in different accounts.

Accounting of transactions for recipients is documented by the date of the decision - Dt76 Kt91, and upon payment - Dt51 Kt76.

The payer's postings are indicated depending on whether the recipient has an employment relationship with the company, and whether NP or personal income tax is due.

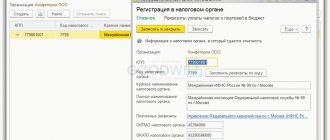

Calculation of dividends in 1C:Accounting 8

To enter information about dividends into the 1C: Accounting 8 program, a basis is required. This is the decision of the founders adopted at the general meeting or the sole decision of the sole participant.

Postings from the payer are made on different accounts based on the status of the founder:

- for a participant who is not in an employment relationship with the company - Dt84 Kt75;

- for an employee – Dt84 Kt70.

Accordingly, depending on whether the recipient works for the payer or not, the postings are also broken down.

For accrued and withheld taxes: Dt75 Kt68 - for non-working shareholders and Dt70 Kt68 - for employees.

For the listed dividends: for non-workers - Dt75 Kt51, for employees - Dt70 Kt51.

Paid taxes are indicated on Dt68 and Kt51.

How to record the accrual and payment of dividends in accounting

To reflect accruals in 1C, on the “Operations” tab, select “Accrual of dividends”, where they indicate all the information about the operation being carried out:

- date;

- name of the payer and recipient;

- accrual period;

- sum;

- necessary explanations.

To reflect the transaction in accounting, all you have to do is select “Record” and “Post”.

The payment is reflected using the same operation. To create a payment document, you must click “Create based on” and select the appropriate method: “Cash withdrawal” or “Payment order”.

How can a tax agent calculate personal income tax at a rate of 13 percent?

The rate of 13% applies to individuals – residents of Russia. The calculation of personal income tax is influenced by whether the tax agent himself received income from participation in the activities of another legal entity. If not, then the tax is calculated as dividends accrued to an individual × 13 percent.

If the tax agent received income from participation in the activities of another organization in the past or present year, then it is necessary to establish whether such income was taken into account when making payments to its founders. If yes, then personal income tax is calculated as in the first paragraph.

Otherwise, first calculate the personal income tax deduction using the formula:

Resident dividends / Total amount of dividends for all participants × Payments received by the payer

Now the tax is calculated at a rate of 13%:

(resident dividends – deduction) × 13%.

How can a tax agent calculate personal income tax at a rate of 15 percent?

The personal income tax rate of 15% is established for non-residents of the Russian Federation, unless otherwise approved by an international treaty (clause 3 of Article 224 of the Tax Code of the Russian Federation).

In this case, the tax for non-residents is calculated using the same formula as for residents of Russia, only with a corresponding coefficient of 15%.

When must a tax agent withhold and transfer personal income tax?

For each type of organizational form of a company, tax legislation establishes different terms for withholding and transferring personal income tax:

- If the payer is a joint-stock company, then personal income tax must be transferred within one month after the payment of dividends (subclause 3 of clause 9 of Article 226.1 of the Tax Code of the Russian Federation).

- If it is an LLC, then the deadline for transferring the tax is one day, not counting the day when dividends are paid (clause 6 of Article 226 of the Tax Code of the Russian Federation).

Tax on dividends on IIS

Using an individual account entitles clients to receive tax benefits. There are two options by which you can receive preferential conditions:

- Option A. You can get a tax deduction - 13% of the amount that was deposited into the account. There is a maximum deduction to which the client is entitled, this is 52,000 rubles. The option is suitable only for people who have an official income, from which 13% is calculated.

- Option B. You don’t have to pay interest on the income received.

In total, an IIS can be opened for 3 years. You can invest a maximum of 1 million rubles annually. In this case, the shareholder can sell the securities at any time and withdraw all invested funds. But if the investor closes the account early, then he loses the right to receive a tax benefit for the past period. All profits that were received during the open period will be subject to a tax rate of 13%.

Features of transferring personal income tax from dividends

The calculated personal income tax must be deducted on the day the dividends are issued. From 01/01/2016 The deadline for paying personal income tax on all income has changed. Now the tax must be transferred on the next day after the income is issued (clause 6 of Article 226 of the Tax Code of the Russian Federation).

When paying personal income tax on dividends, it is necessary to draw up a payment order identical to payment of tax on ordinary types of income. In this case, the BCC will be the same for both the personal income tax of residents, calculated on the basis of 13%, and for the tax of non-residents, calculated on the basis of a 15% rate.

Important! Transfer personal income tax withheld from several individuals. persons, possible with one payment order. In this case, it is necessary to have all accounting documents identifying the recipient of the income (letter of the Ministry of Finance of the Russian Federation dated November 19, 2014 N 03-04-07/58597).