What are shipping costs?

Transport costs represent the costs of an organization associated with the provision of services for the delivery of various goods: goods, materials, fixed assets.

Depending on the method of transportation, type of goods, as well as places of departure and destination, the list of documents justifying expenses may vary. According to paragraph 1 of Art. 252 of the Tax Code of the Russian Federation, a taxpayer can take into account expenses when calculating income tax if they have:

- documenting;

- economic justification.

Thus, in order to display transport costs as expenses when determining the tax base for income tax, it is important to have their real confirmation on paper.

Read about the peculiarities of tax accounting for transport expenses in the material “Transportation expenses when calculating income tax .

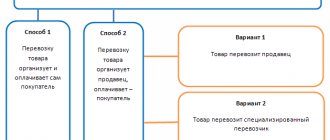

The most common type of transport service is the delivery of goods from the supplier to the buyer. The party who bears the costs themselves is determined by the terms of the sales contracts. Costs may be incurred:

- seller of goods;

- buyer.

In this case, transportation can be carried out by the following persons:

- by the seller himself;

- by the buyer using his own vehicle;

- a third party company with which either the seller or the buyer enters into an agreement.

Next, we will consider the features of documenting delivery costs carried out by the seller and buyer when transporting goods independently or with the involvement of an intermediary.

Read more about how the seller and buyer take into account transport costs in the Ready-made solution from ConsultantPlus. If you don't have legal access, a full access trial is available for free.

On the classification of transport costs for tax accounting purposes, see the material “Transportation costs - are they direct or indirect costs?” .

What documents confirm transportation costs?

Transport costs are those costs of a company or organization that are associated with services for the delivery of various types of products: raw materials, materials, various goods. Based on the method of transportation, places of departure and arrival, types of goods, the list of documents may vary.

According to paragraph 1 of Article 252 of the Tax Code of the Russian Federation, an organization paying taxes has the right to take into account expenses when calculating tax on specific profits if they have:

- confirmation in the form of documents;

- economic feasibility.

It turns out that in order to reflect the costs of transport services in expenses, you need to have documentary evidence of them.

One of the most common forms of transport services is the delivery of various goods from the supplier to the person who purchases them. The party who bears the direct costs must be determined through the terms described in the SPA (purchase and sale agreement). Such expenses may be incurred by:

- sellers of goods;

- buyers.

The transportation itself can be carried out by the following parties:

- directly by the seller;

- a third party company with which either the seller or the buyer can enter into an agreement.

When selling goods, the seller must display to the buyer:

- invoice (which can be ignored when applying a special regime)

- invoice for goods in the form TORG-12

- other trans. commodity documents – TTN (trans. waybill) and TN (trans. waybill)

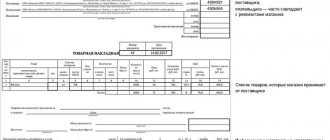

TORG-12 is a primary document that the seller draws up in 2 copies (for himself and the buyer). It contains information about the material assets being sold, which confirm the transfer of ownership rights to them from the one who sells to the one who purchases the goods.

The price list for transportation services is fixed in the TN, that is, the amount of transportation costs itself.

The TN contains the following information:

- about the parties to the agreement;

- about the transported mat. values;

- about other documents;

- about the transport that carries out delivery;

- about the time and place of loading and unloading of goods;

- about the time of delivery of the goods.

However, the TN is not a document according to which it is possible to post the goods, but only serves as a document to justify transport costs.

As for the TTN, it is the primary documentation that not only confirms the organization’s expenses for transport services, but also indicates the information that is needed for recording and writing off the mat. values. The TTN includes two parts - transport and goods, and also details such as:

- TTN number;

- time of its filling;

- information about the product being sold;

- details of the parties to the agreement.

This type of cargo transportation means two delivery options:

- the supplier makes its own efforts to deliver the products to the final buyer;

- The supplier hires a carrier who is responsible for delivering the goods to the final buyer.

If the supplier, when drawing up an agreement with the buyer, provided for the supply of products using its resources, then such delivery can be carried out, taking into account the following nuances:

- the supplier is not obliged to indicate the delivery price as an additional clause in the contract; he can add it to the cost of the goods;

- The supplier has the right to include the delivery price in the contract.

The first case requires the supplier to issue only a waybill. It will indicate the fact of delivery and associated costs.

In the second case, the supplier must necessarily expose the TTN or TN in the direction of the buyer.

In a situation where the supplier engages an intermediary, the following documents are processed:

The supplier may issue a TTN in four copies. One copy goes to the supplier, the remaining three will be given to the intermediary who carries out the transportation. Upon completion of delivery, the intermediary transfers three copies of the TTN to the buyer. The latter must put his signature on them and keep one of the forms for himself. Taking the two remaining copies as a basis, the intermediary company must draw up an act of performance of services (and such an act, together with one of the copies of the TTN, is returned to the seller).

In the case where a decision is made to draw up a technical specification instead of a specification form, three copies are required - one for each party. And then the fact that the transportation service was provided will be confirmed by a copy of the technical specification, which contains the signatures of both the buyer and the carrier.

What documents can be used to confirm the transportation performed by the buyer?

It is worth noting that if the buyer transports the goods from the seller’s warehouse location independently, then neither the TN nor the CTN is drawn up. And the waybills will serve as justification for the fact that the buyer has incurred expenses.

If the buyer decides to enter into an agreement with any intermediary, then the algorithm of actions is as follows:

- A TTN is drawn up in four copies, where the buyer enters data only in the section on transport services, after which these documents must be transferred to the carrier so that the supplier fills out the product section. The supplier then returns three copies to the carrier. After acceptance of the cargo, one of the copies goes to the buyer, and the remaining two to the carrier, who is responsible for drawing up the report.

- or a TN is issued, in which the buyer indicates himself as both the consignee and the consignor. In this case, the TN consists of two copies - one for the buyer, the second for the organization that carried out the transportation.

What documents do you need to have when delivering goods?

When selling goods, the seller is obliged to provide to the buyer:

- invoice (exception - the use of a special regime);

- waybill in the form TORG-12;

- other shipping documents - waybill (Bill of Lading) and bill of lading (BW).

TORG-12 is a primary document drawn up by the seller in 2 copies (one for himself, the other for the buyer). It contains information about the assets being sold and is confirmation of the transfer of ownership of them from the seller to the buyer.

TN (Appendix 4 to the Decree of the Government of the Russian Federation dated April 15, 2011 No. 272) fixes the cost of transportation services, i.e. the amount of transportation costs. It contains information:

- about the parties to the transaction;

- transported goods and materials;

- additional documents;

- delivery vehicle;

- point and date of loading/unloading of goods;

- date of cargo delivery;

- other data.

At the same time, the technical document is not a document on the basis of which goods can be capitalized, but serves as a primary document for justifying transportation costs.

As for the TTN (Form 1-T), it is the primary document that not only confirms the organization’s transportation costs, but also reflects the information necessary for writing off and capitalizing inventory items.

It is with TTN that claims from regulatory authorities are most often associated. You can familiarize yourself with the main controversial issues and find arguments for a dispute with the inspectors in the Encyclopedia of Controversial Situations from ConsultantPlus. Trial access to the system can be obtained for free.

The CTN contains two parts - commodity and transport, and also includes the following details:

- TTN number;

- the date of its preparation;

- information about the product;

- details of the parties to the transaction;

- other data provided for by Decree of the State Statistics Committee of the Russian Federation dated November 28, 1997 No. 78.

Checking the counterparty during preparation

The parties to the contract, namely, the customer and the contractor (or the sender and the carrier), can be individuals and legal entities , that is, citizens, individual entrepreneurs and organizations of various legal forms (LLC, JSC, partnerships, cooperatives, NPOs, institutions, etc. .d.).

A high-quality preliminary check of a potential partner is required to eliminate risks associated with fraudulent actions of the counterparty.

If the contractor or customer under the contract is an individual , you must ask to provide the following documents:

- passport of a citizen of the Russian Federation or another state;

- certificate of assignment of TIN ;

- if an individual acts as a performer, he is required to present a certificate of state registration as an individual entrepreneur .

To verify a legal entity, you need to request the following package of documents:

- articles of association;

- certificate of state registration and tax registration ;

- order on the appointment of a director;

- valid power of attorney , according to which the employee signing the agreement is empowered to enter into transactions on behalf of the company.

The contractor, regardless of whether he is an individual entrepreneur or a legal entity, must request :

- certificate of receipt of a license to carry out transportation;

- documents confirming the ownership of the company or individual entrepreneur of vehicles that will be used to fulfill obligations under the contract, or a vehicle rental agreement, as well as data on the technical condition of the transport;

- documented information about the presence of drivers of the appropriate category , or, if the contractor, an individual entrepreneur, carries out transportation on his own, his driver’s license.

Each counterparty, be it an individual entrepreneur or an enterprise, needs to be checked using four tools:

- special service on the tax office website ;

- file of arbitration court cases , where you can find out about legal disputes in which a potential partner is involved;

- database of judicial enforcement proceedings on the website of the bailiff service ;

- Kommersant publication , which contains information on the reorganization, liquidation and bankruptcy of organizations.

The documents listed above will be needed not only for checking the counterparty, but also directly for drawing up the contract. In the text of the document, it is necessary to indicate a reference to the charter or power of attorney , on the basis of which the company representative acts if a legal entity is involved in the transaction.

In addition, you must provide license details . The last paragraph of the agreement “Addresses and details of the parties” lists the names of organizations or full names of individuals acting as parties to the transaction, their bank details and addresses .

Download for free:

Sample contract for the provision of transport services with individual entrepreneurs.

Sample contract for the provision of transport and forwarding services.

Sample agreement for the provision of transport services with the crew.

Sample contract for the provision of transport services with an individual.

Sample agreement for the provision of services for the transportation of passengers.

Standard contract for the provision of transport services for cargo transportation plus an Agreement for the provision of loader services.

We wrote in more detail about the features of concluding a contract for the provision of paid services with individuals here, and here you will learn how such agreements are drawn up with legal entities.

What documents can justify the transportation of goods by the supplier?

The transportation of goods by the supplier can be understood as 2 delivery options:

- The supplier independently delivers the goods to the buyer.

- The supplier enters into an agreement with the carrier, who transports the goods to the destination.

If the supplier, when drawing up an agreement with the buyer, provides for the supply of goods on its own, then delivery can be made taking into account the following features:

- The supplier may not separately highlight the cost of delivery in the contract, but include it in the price of the goods (the first case).

- The supplier has the right to specify the delivery cost in the contract (second case).

Depending on the above conditions, the documentation of delivery services changes:

- In the first case, the supplier draws up only a waybill, which will confirm the fact of delivery and the costs of it.

- In the second case, he needs to issue a bill of lading (Bill of Lading) or a bill of lading (BW) to the buyer.

If the supplier has engaged an intermediary to transport goods, the document flow will be as follows:

- The supplier can issue a TTN in 4 copies. In this case, one copy remains with the supplier, the other three are transferred to the intermediary carrying out transportation. The intermediary, having completed delivery, transfers 3 copies of the TTN to the buyer, who puts his signature on them. One copy remains with the buyer. Based on the remaining 2, the intermediary draws up an act of services rendered. In this case, one of the copies of the TTN, signed by the buyer, is returned to the seller along with the act.

- If the supplier, instead of the TTN, decides to issue a TTN, three copies of this document will need to be made: one is intended for the carrier, the second for the seller, and the third for the buyer. The fact of provision of transport services for the supplier can be confirmed by the TN signed by the buyer and the carrier.

To learn about filling out a bill of lading using online services, read the article “Online filling out a bill of lading: what services are there?”

Transport services in the Group of companies (taxCOACH® case studies)

In a group that directly interacts with both clients and third-party transport organizations and individual entrepreneurs engaged to provide services. The need to create a “dispatch company” is dictated by Russian realities: today, the risks that the counterparty company will suddenly turn out to be a “fly-by-night” still remain, so business, as a rule, is forced to rely on a company that will not suffer greatly from negative results in relations with it tax audit for this counterparty.

In this case, Transport Company LLC transfers the received vehicles under a lease agreement with the crew to Dispatch Company LLC, that is, ownership and use of the transport is transferred to the lessee, and management and technical operation is carried out by the lessor’s employees.

Commercial operation - direct provision of services to clients - is carried out by the tenant (Dispatch Company LLC).

If a transport company has the opportunity to apply the simplified tax system, formalizing the relationship with just such an agreement will allow for tax savings.

For example, in the Sverdlovsk region, the lease of construction machinery and equipment with an operator (OKVED “Construction of buildings”, “Construction of engineering structures”), or the lease of vehicles with a driver (OKVED “Activities of land and pipeline transport”), provided that this type of activity is the main one will allow the use of the simplified tax system with the income-expenses object at a rate of 5%.

In addition, due to the specifics of the rental agreement for a vehicle with a crew, expenses arising in connection with the commercial operation of the vehicle, including the cost of paying for fuel and other materials consumed during operation and paying fees, are borne by the lessee (Dispatch Company LLC "), unless otherwise provided by the agreement. Art. 636 of the Civil Code of the Russian Federation Thus, it is possible to incur the necessary expenses for this company, including VAT, in this area (if “Dispatcher” is on the OSN).

In addition, the dispatch company, under the terms of the contract, may be required to insure the vehicle and (or) insure liability for damage that may be caused by it or in connection with its operation in cases where such insurance is mandatory by law. Art. 637 Civil Code of the Russian Federation

The negative side of a rental agreement for a vehicle with a crew is that the lessor is responsible for damage caused to third parties by the rented vehicle, its mechanisms, devices, equipment. Art. 640 Civil Code of the Russian Federation. 22 Resolution of the Plenum of the Supreme Court of the Russian Federation of January 26, 2010 No. 1 “On the application by courts of civil legislation regulating relations regarding obligations resulting from harm to the life or health of a citizen”; Determination of the Investigative Committee for civil cases of the Sixth Court of Cassation of General Jurisdiction dated February 19, 2021 in case No. 8G-955/2020[88-2817/2020

At the same time, assigning responsibility to Transport Company LLC is quite logical, since the management of vehicles is carried out by its employees. However, this circumstance is not of a fundamental nature, since the risks of property liability of the group of companies are minimal.

It should be noted that the revenue of Transport Company LLC for the purpose of applying the simplified tax system must fall within the legally established limits (no more than 150 million rubles, from 2021 - no more than 200 million). Obviously, the amount of the rent will be used to cover the costs of paying staff, rental payments for the Asset Custodian, tax obligations and insurance premiums.

Example 3

This option is similar to the previous one: The dispatch company is also a link between clients and transport companies. However, in this example, she performs agent functions.

This is how some taxi services operate today, providing “exclusively informational services.”

The Taxi dispatch service finds and contacts clients. At the same time, Taxi enters into an agreement with them for the provision of passenger transportation services on its own behalf, but in the interests of the taxi fleet.

Functions of the Dispatch Service:

- searching for clients;

- ensuring communication with clients;

- ensuring the operation of the CALL center;

- ensuring the operation of the website and digital applications;

- marketing;

- and so on.

Direct transportation is carried out by Taxi Park. It provides:

- transport, which can be either owned or leased;

- a driver with whom the Taxi Park has an employment contract or a vehicle rental agreement.

In this case, both companies - the Taxi Park and the Dispatch Service - are responsible for causing harm. Despite the fact that it itself did not perform the contract and was in no way involved in the incident that resulted in harm, the Dispatch Service, as the party that entered into the contract, is responsible to the client.

Under a transaction made by an agent with a third party on his own behalf and at the expense of the principal, the agent acquires rights and becomes obligated, even if the principal was named in the transaction or entered into direct relations with the third party for the execution of the transaction. para. 2 p. 1 art. 1005 of the Civil Code of the Russian Federation

This is fully confirmed in judicial practice. Ruling of the Supreme Court of the Russian Federation dated January 09, 2018 in case No. 5-KG17-220

The agent’s responsibility to clients must be taken into account when building a group of companies.

Example 4

Transport is used by a group of companies to deliver goods to customers. This item ships from a related warehouse.

Option for constructing this block in a group of companies:

In this case, the transport can be transferred for use to a company performing the functions of a warehouse. The relationship between this company and the company that sells goods is mediated by a complex agreement for the provision of warehouse services, which contains elements of agreements for storage and the provision of transport services. will include:

- Acceptance of goods;

- Loading and unloading operations;

- Warehousing in accordance with the requirements for a specific product group;

- Ensuring appropriate storage and movement conditions;

- Completing batches of goods, shipping goods to third parties as directed by the customer;

- Delivery of goods to third parties in accordance with the instructions of the customer.

Responsibility for causing damage by a vehicle is borne by the vehicle.

Thus, there can be many options. But the primary reason for any choice: these are the real business processes in the company. Any tool for tax planning, building a system of property and management security should not be “built on top” of a real business process. In this case, it will always be “artificial”, and therefore high-risk. The tool must be “based”, based on the essence and characteristics of the relationship.

How to justify the transportation made by the buyer?

It should be noted that when the buyer independently transports the goods from the seller’s warehouse, TN and TTN are not drawn up. And the justification for the expenses incurred by the buyer will be the travel documents issued by him (letter of the Ministry of Finance of Russia dated December 22, 2011 No. 03-03-10/123).

If the buyer enters into an agreement with an intermediary, then his actions must be as follows:

- You can issue a TTN in 4 copies, where the buyer fills out only the transport section. After this, the specified documents are transferred to the carrier for completion by the supplier of the goods section. Having filled out the TTN, the supplier hands over 3 copies to the carrier. Having accepted the cargo, the buyer keeps one copy for himself, and hands the remaining 2 copies to the carrier, on the basis of which he draws up an act.

- If the buyer draws up a TN, he must indicate himself as the consignee and consignor. This TN is drawn up in 2 copies - one remains with the buyer, the other is transferred to the transport organization.

Waybill

Art. 785 Civil Code of the Russian Federation:

“The conclusion of a contract for the carriage of goods is confirmed by the preparation and issuance of a waybill to the sender of the goods

(bill of lading or other document for cargo provided for by the relevant

transport charter

or code).”

The transport consignment note was developed by the Government for the Charter of road transport and urban ground electric transport (clause 1 of article 3 of the Federal Law of November 8, 2007 N 259-FZ).

- Letter of the Ministry of Finance of the Russian Federation dated April 23, 2013 N 03-03-06/1/14014;

- Letter of the Ministry of Finance of the Russian Federation dated January 28, 2013 N 03-03-06/1/36;

- Letter of the Federal Tax Service of the Russian Federation dated May 17, 2016 N AS-4-15/ [email protected]

Who should apply

Transport documents are issued by the shipper

(unless otherwise provided by the contract) when:

- the goods are delivered by the supplier and delivery is a separate service;

- The product is delivered by a third party carrier.

Settings for printing TN and TTN

Main - Functionality - Trade tab

How to indicate the trailer number in 1C

Directories - Vehicles

Sales (act, invoice) - link Delivery

Printed form TTN

Implementation (deed, invoice) - Print button

Trailer number in TN and TTN

Why in 1C information about the trailer is entered only in the waybill form 1-T (TTN) and not entered in the TN?

Automatic filling of the waybill with trailer data is implemented only for the TTN, since it provides this information. Additional details can be entered into the TN manually.

Pickup

Do we need a technical document to justify the costs of purchasing goods if we remove the goods from the supplier’s warehouse using our own transport (on a pickup basis)?

If the goods are exported by our own transport, i.e. Without an agreement with a third-party carrier (supplier), a document confirming the costs of purchasing goods for income tax will be:

Official position

- TORG-12 + Waybill (Letter of the Ministry of Finance of the Russian Federation dated December 22, 2011 N 03-03-10/123).

Safe position

- TORG-12 + Waybill + TN - proves the reality of the delivery (Resolution of the Federal Antimonopoly Service of the North-Western District dated September 28, 2011 in case No. A13-8941/2010).

Delivery is included in the price of goods

Is a technical documentation needed to justify the costs of purchasing goods if the supplier delivered the goods to our warehouse on their own? Delivery is included in the price of goods under the contract.

If the cost of transportation is taken into account in the cost of the goods, the document confirming the costs of purchasing goods for income tax will be:

Official position

- TORG-12 - TN is not needed (Letter of the Ministry of Finance of the Russian Federation dated June 15, 2010 N 03-03-06/1/413).

Safe position

- TORG-12 + TN (copy) (Resolution of the AS of the East Siberian District dated April 14, 2016 N F02-1543/2016).

See also:

- Consignment note (Bill of Lading) in 1C 8.3

- Typical document flow for commodity transactions

- [04.10.2018 recording] Supporting seminar 1C BP for September 2018

- Registration of technical documentation

- In 1C, changes have been made to the printed form of the Waybill

- [08/18/2020 recording] Supporting seminar 1C BP for July 2020

Did the article help?

Get another secret bonus and full access to the BukhExpert8 help system for 14 days free of charge

Related publications

- Workshop on quickly loading counterparty details...

- Who should prepare the waybill? ...

- Error in mutual settlements with the supplier: an incorrect payment document was specified. Detecting and correcting errors using the Subconto Analysis report Incorrect settlement document with the counterparty When preparing documents in 1C, they can...

- Conclusion of the counterparty's TIN in the Reconciliation Report...

Results

Transportation costs occur in almost any business activity. Having all the necessary supporting documents is of great importance for both suppliers and buyers, as it allows them to reduce the cost of paying income taxes.

Sources:

- Tax Code of the Russian Federation

- Decree of the Government of the Russian Federation of April 15, 2011 No. 272

- Resolution of the State Statistics Committee of the Russian Federation dated November 28, 1997 No. 78

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.