The net profit of Aktiv JSC for the last year amounted to 22,000 rubles. Aktiv has two shareholders.

By decision of the general meeting of shareholders of Aktiv JSC, dividends on shares are paid in the amount of:

A.N. Ivanov – 10,000 rubles;

S.S. Petrov – 12,000 rubles.

Personal income tax on Ivanov’s dividends will be:

10,000 rub. ? 13% = 1300 rub.

The personal income tax on Petrov’s dividends will be:

12,000 rub. ? 13% = 1560 rub.

The Aktiva accountant should pay dividends in the amount of:

A.N. Ivanov – 8,700 rubles. (10,000 ? 1300);

S.S. Petrov – 10,440 rubles. (12,000 ? 1560).

Who makes a decision on the payment of dividends to an LLC and how?

Legislative norms related to LLCs allow the profit received by it (all or part of it) to be used to issue income (dividends) to participants (Clause 1, Article 28 of the Law “On Limited Liability Companies” dated 02/08/1998 No. 14-FZ). The right to make decisions about this is reserved for the LLC participants themselves. To do this, they hold a general meeting. Convening a meeting becomes possible if a number of restrictions are met at the time of the meeting (Clause 1, Article 29 of Law No. 14-FZ):

- The management company is fully paid;

- the withdrawn participant was given the value of his share;

- net assets exceed the sum of the authorized capital and the reserve fund, and this ratio will remain after the issuance of dividends;

- There are no signs of bankruptcy and will not arise as a result of the issuance of dividends.

Compliance with the listed restrictions and the amount of profit that can be distributed are determined based on an analysis of the LLC’s financial statements prepared by the time the meeting is convened.

Analysis of reporting also applies to LLCs on the simplified tax system. For information on preparing reports under the simplified tax system, read the article “Maintaining accounting for an LLC using the simplified tax system: submitting reports .

What documents are required to document the payment of dividends?

The decision on the payment of dividends must be made by the general meeting of shareholders (participants) (clause 3 of Article 42 of the Law of December 26, 1995 No. 208-FZ, clause 1 of Article 28 of the Law of February 8, 1998 No. 14-FZ). It must be formalized in the minutes of this meeting (Article 63 of the Law of December 26, 1995 No. 208-FZ, paragraph 6 of Article 37 of the Law of February 8, 1998 No. 14-FZ).

There are no mandatory requirements for the minutes of the meeting of LLC participants in the legislation. But there are details that should be provided. This is the number and date of the minutes, place and date of the meeting, agenda items, signatures of company participants. The minutes of the general meeting of shareholders differ from the minutes of an LLC in that they are drawn up in two copies and have mandatory details. They are listed in paragraph 2 of Article 63 of the Law of December 26, 1995 No. 208-FZ.

An example of the minutes of a general meeting of LLC participants. Dividend payment

The charter of Torgovaya LLC stipulates that the organization pays dividends quarterly. For the second quarter, the organization’s net profit amounted to 50,000 rubles. At the general meeting of participants, which took place in July, it was decided to use this entire amount to pay dividends. The decision was made unanimously. The minutes of the general meeting of participants were drawn up.

Situation: what documents should be used to document the calculation of dividends due to each participant (shareholder) of the company?

In the minutes of the general meeting, indicate only the total amount of net profit that it was decided to pay to the participants (shareholders). The amount due to each of them must be calculated independently. This calculation must be confirmed by a primary document (Part 1, Article 9 of the Law of December 6, 2011 No. 402-FZ). Such a document could be, for example, an accounting certificate.

Situation: how to formalize the payment of dividends to participants (shareholders)?

There is no special document required to formalize the payment of dividends. Therefore, you can use standard forms that are filled out when paying money from the cash register or when transferring funds from a current account. In addition, an organization can develop a form for processing the payment of dividends independently (clause 4 of article 9 of the Law of December 6, 2011 No. 402-FZ).

Attention: when registering the payment of dividends to shareholders, the following must be taken into account. Dividends must be paid to shareholders in cash.

Moreover, if dividends are paid to a citizen, then the money must be transferred to him by postal order or upon application to his bank account. This is stated in paragraph 8 of Article 42 of the Law of December 26, 1995 No. 208-FZ.

Dividends can be paid to LLC participants either through a cash register or to a bank account.

See additional entries for accrual and payment of dividends to the founder

Situation: can cash proceeds be used to pay dividends?

No you can not.

The procedure for paying dividends is established by the general meeting of shareholders (participants) (clause 3 of Article 42 of the Law of December 26, 1995 No. 208-FZ, clause 1 of Article 28 of the Law of February 8, 1998 No. 14-FZ). At the same time, the meeting of shareholders must take into account that organizations can receive dividends in cash only to their bank accounts. And citizens - both by bank (upon application) and postal transfer. This procedure is established by paragraph 8 of Article 42 of the Law of December 26, 1995 No. 208-FZ. For LLCs, such a restriction is not established by Law No. 14-FZ of February 8, 1998.

But even if LLC participants decide to pay cash dividends from proceeds, they need to consider the following. A number of restrictions have been established regarding the expenditure of cash proceeds from the organization's cash desk. The list of purposes for which funds from the cash register can be spent is given in paragraph 2 of the instruction of the Central Bank of the Russian Federation dated October 7, 2013 No. 3073-U. The payment of dividends is not mentioned in it.

Thus, cash proceeds cannot be used to pay dividends. After all, a direct ban has been established for joint-stock companies, and claims for misuse of cash may be brought against LLCs.

For more information about spending cash proceeds, see How to Follow the Procedure for Conducting Cash Transactions.

How to draw up a protocol on the payment of dividends in an LLC

The issue of profit distribution can be either one of several discussed at the meeting, or the subject of a separate meeting. Regardless of the number of issues on the agenda, the decision of the meeting is formalized by drawing up a protocol, the indispensable details of which will be:

- number, date and indication of whether the document belongs to the LLC;

- list of participants, distribution of shares between them;

- agenda;

- results of consideration and decision on each issue.

With regard to dividends, the meeting must determine:

- for what period they intend to pay them;

- the total amount allocated for this purpose;

- form and terms of issue.

The payment period can range from a quarter to a year. In this case, payments are also possible for the year preceding the previous one.

The total amount is distributed among the participants in proportion to the share of each, unless the charter provides for a different procedure (Clause 2, Article 28 of Law No. 14-FZ), therefore it is enough to establish its value. Although the protocol can also record specific amounts intended for distribution to each participant in accordance with the distribution rules.

The form of payment is most often monetary. However, the law does not prohibit payment in property.

Payment is made subject to tax withholding. Read about its calculation in the article “How to correctly calculate the tax on dividends?” .

Payment is made no later than 60 days from the date of the decision (Clause 3, Article 28 of Law No. 14-FZ). If a period within this period is not established by the charter, the meeting has the right to set it by its decision for each specific payment. The period is considered equal to 60 days if it is not included in the decision and charter.

What to do if the founder did not receive dividends on time

Legislative norms related to LLCs allow the profit received by it (all or part of it) to be used to issue income (dividends) to participants (Clause 1, Article 28 of the Law “On Limited Liability Companies” dated 02/08/1998 No. 14-FZ). The right to make decisions about this is reserved for the LLC participants themselves.

- The management company is fully paid;

- the withdrawn participant was given the value of his share;

- net assets exceed the sum of the authorized capital and the reserve fund, and this ratio will remain after the issuance of dividends;

- There are no signs of bankruptcy and will not arise as a result of the issuance of dividends.

Compliance with the listed restrictions and the amount of profit that can be distributed are determined based on an analysis of the LLC’s financial statements prepared by the time the meeting is convened.

https://www..com/watch?v=upload

Analysis of reporting also applies to LLCs on the simplified tax system. For information on preparing reports under the simplified tax system, read the article “Maintaining accounting for an LLC using the simplified tax system: submitting reports.”

The sole founder has no one to hold the meeting with, so he simply makes his own decision on issuing dividends to himself. It is drawn up in the usual manner for such a document.

The procedure for using income must be enshrined in the organization’s statutory documentation. For an organization, this is indicated by Articles 4, 15, 41 and 59 of Law No. 1576. Typically, the division of income is done at a general meeting of shareholders, which is done after the end of the reporting year.

Participants at this meeting are required to approve the financial report provided to them, and therefore the amount of net income recorded in it. And after approval, they can allocate a specific amount of income to pay dividends.

Thus, the amount of dividends is determined at a general meeting of shareholders, which is held after the preparation of the financial report and no earlier than two months after the end of the reporting period.

If such a decision is stipulated by the charter or made due to various circumstances at a general meeting with changes to the charter papers, taxation of income from dividends is carried out at special rates, as with the proportional division of profits.

Decisions regarding the distribution of profit or its 100% shares between participants are always made at a general meeting of members corresponding to their share in the capital, unless other constituent agreements are specified in the charter and in accordance with Article 28 of the Federal Law No. 14-FZ “On Limited Liability Companies” .

Such mandatory compliance is determined by what, based on accounting analysis, is relevant at the time of the current convening of the meeting.

If all the conditions are met, then it is time to formalize the decision of those participating in the company to direct the net profit received in a certain period to pay dividends.

In this paragraph, we will consider the option when a limited liability company has only one founder member.

Two founders

In the case of two participants, paperwork is necessary as for a company with several participants. That is, first a decision made at a meeting of shareholders is drawn up, then the head of the LLC signs the order.

How the protocol is drawn up

If the organization has a single founder, then he draws up his resolution in the minutes, in free form, since there is no various form on this subject, but he will certainly write down the agenda of the adopted resolutions.

This is not always the only issue discussed at meetings. However, the quantitative issues on the agenda do not play a special role; the results of the meeting are formalized through the drawing up of a special protocol.

The main details of the protocol are:

- number, date and indication of the document’s affiliation with the LLC; listing of participants, distribution of their shares; agenda; results of the study and rendering of verdicts on all issues.

In order to solve the problem with dividend payments, the meeting must clearly define the amount of dividends to be paid, the period for which they are intended, as well as the form of payments, their order and date.

The main form of payment of dividends, as a rule, is cash, but there are no restrictions on property payments, which are now widespread.

Protocol example

The issue of dividends may not be the only one put forward for decision by the participants of the shareholders meeting.

Therefore, a special meeting protocol must be drawn up and approved, which includes the following aspects:

- the number of participants and their shares in the authorized capital of the company;

- an agenda consisting of the issues to be discussed;

- solutions to each of the issues listed on the agenda.

Let's bring an extraordinary meeting.

The issue of profit distribution can be either one of several discussed at the meeting, or the subject of a separate meeting. Regardless of the number of issues on the agenda, the decision of the meeting is formalized by drawing up a protocol, the indispensable details of which will be:

- number, date and indication of whether the document belongs to the LLC;

- list of participants, distribution of shares between them;

- agenda;

- results of consideration and decision on each issue.

With regard to dividends, the meeting must determine:

- for what period they intend to pay them;

- the total amount allocated for this purpose;

- form and terms of issue.

The payment period can range from a quarter to a year. In this case, payments are also possible for the year preceding the previous one.

The total amount is distributed among the participants in proportion to the share of each, unless the charter provides for a different procedure (Clause 2, Article 28 of Law No. 14-FZ), therefore it is enough to establish its value. Although the protocol can also record specific amounts intended for distribution to each participant in accordance with the distribution rules.

The form of payment is most often monetary. However, the law does not prohibit payment in property.

Payment is made subject to tax withholding. Read about its calculation in the article “How to correctly calculate the tax on dividends?”

Payment is made no later than 60 days from the date of the decision (Clause 3, Article 28 of Law No. 14-FZ). If a period within this period is not established by the charter, the meeting has the right to set it by its decision for each specific payment. The period is considered equal to 60 days if it is not included in the decision and charter.

According to paragraph 1 of Art. 28 of the Federal Law of 02/08/1998 No. 14-FZ “On Limited Liability Companies” LLC has the right to make a decision quarterly, once every six months or once a year on the distribution of its net profit among the participants of the company. The decision to determine the part of the company's profit distributed among its participants is made by their general meeting.

The current legislation does not prohibit the payment of dividends based on the results of the current year, taking into account retained earnings of previous years.

At the same time, it is necessary to take into account that there are still restrictions regarding the distribution of the company’s profits between its participants - they are established by clause 1 of Art. 29 of Federal Law No. 14-FZ.

The company does not have the right to decide on the distribution of its profits among participants:

- until full payment of the entire authorized capital of the company;

- before payment of the actual value of a share or part of a share of a company participant in cases provided for by Federal Law No. 14-FZ;

- if at the time of making such a decision the company meets the signs of insolvency (bankruptcy) or if the specified signs appear in the company as a result of making such a decision. A legal entity is considered unable to satisfy the claims of creditors for monetary obligations, for the payment of severance pay and (or) for wages of persons working or who worked under an employment contract, and (or) to fulfill the obligation to make mandatory payments, if the corresponding obligations and (or) obligation not executed by him within three months from the date on which they should have been executed (clause 2 of article 3 of the Federal Law of October 26, 2002 No. 127-FZ “On Insolvency (Bankruptcy)”);

- if at the time such a decision is made, the value of the company’s net assets is less than its authorized capital and reserve fund or becomes less than their size as a result of such a decision. The value of the LLC's net assets is determined according to accounting data in the manner approved by Order of the Ministry of Finance of the Russian Federation dated August 28, 2014 No. 84n;

- in other cases provided for by federal laws.

If the listed restrictions do not work, the founder of the company has the right to decide on the distribution of profits from previous years, even if a loss was incurred at the end of 2021.

At the same time, the amount of distributed profit must be such that, as a result of distribution, the value of the LLC’s net assets does not become less than the authorized capital and reserve fund and the company does not develop signs of insolvency (bankruptcy).

It should also be taken into account that the profit for which a decision has been made to distribute between the participants of the LLC cannot be paid if (Clause 2 of Article 29 of Federal Law No. 14-FZ):

- at the time of payment, the company meets the signs of insolvency (bankruptcy) or the specified signs will appear in the company as a result of payment;

- at the time of payment, the value of the company’s net assets is less than its authorized capital and reserve fund or will become less than their size in connection with the payment.

Deadlines

https://www..com/watch?v=ytcopyrightru

Debit 70 (75), subaccount “Calculations for payment of income”, Credit 51

- Dividends are transferred to the founder - an employee of the company (a person who is not an employee).

At the time of payment of dividends, withhold personal income tax from the income of citizens or income tax from the amounts due to companies. And transfer taxes to the budget. We described in more detail how to create postings in this case on p. 40.

We also draw your attention to this point. In general, late payment of dividends does not have any negative consequences for the organization if the founders do not challenge the current situation in court.

If the owners go to court, the latter may oblige you to pay not only the dividends themselves, but also interest for late fulfillment of obligations and the use of other people's funds (Article 395 of the Civil Code of the Russian Federation, Resolution of the Federal Antimonopoly Service of the East Siberian District dated May 5, 2012 N A10-248 /2011).

How to decide on paying dividends to the sole founder

The sole founder has no one to hold the meeting with, so he simply makes his own decision on issuing dividends to himself. It is drawn up in the usual manner for such a document.

A sample decision on the payment of dividends to the sole founder can be viewed and downloaded on our website.

Find out which payments are not considered dividends from the article “Procedure for calculating dividends under the simplified tax system.”

The decision of the sole participant of the LLC on the distribution of profits as dividends

But in general, LLC participants can distribute net profit not only once a year, but also once every six months or even once a quarter (Clause 1, Article 28 of the Law of 02/08/1998 N 14-FZ). And it may turn out that the amount of interim dividends paid exceeds the amount of profit received by the company at the end of the year. This will lead to the fact that for tax purposes the excess amount will turn into another “non-dividend income” of the participants (clause 1 of Article 43 of the Tax Code of the Russian Federation), which means that the procedure for its taxation may also change.

- incomplete payment of the company's authorized capital;

- non-payment (incomplete payment) of the actual value of a share or part of a share to a company participant who left the LLC;

- presence of signs of bankruptcy of the company or a high probability of such signs appearing after payment of dividends;

- the value of the company's net assets is less than the sum of the authorized capital and reserve fund (or a real threat that the value of the net assets will become less than the specified amount after the decision to pay dividends is made).

Results

The law allows the profits received by the LLC to be used to pay dividends. The decision on payment is made by the sole founder or members of the company at a general meeting, subject to legally established restrictions (if the authorized capital is fully paid, there are no signs of bankruptcy, etc.).

The founders' decision to pay dividends is formalized in the form of minutes of the general meeting or a decision of the sole founder. Following the decision, an order to pay dividends is issued.

Sample payment order for transfer

It is clear that dividends are the profit that a shareholder or founder expects to receive at the end of the year. And this is a completely legitimate desire, since he invested certain funds by purchasing shares and now wants to make a profit.

He will not receive it if at the end of the year the enterprise is declared bankrupt or simply does not generate any income, but simply pays for itself, with the obligatory payment of all necessary taxes and salaries, as well as other obligations.

If the profit is received, the decision on payments is made, then it needs to be made. And in this case, there is no special document that should be provided in this case. Therefore you can use the following:

- form for payment of money from the cash register or when transferring to an account;

- accounts to shareholders, payments to whom are made in non-cash form.

Here is a sample payment slip for the payment of dividends to individuals:

For an organization, such a payment document looks somewhat different, although, in essence, it is not very different.

Sample payment order for payment of dividends to a legal entity:

Correct execution of a payment order for the transfer of profit received is a guarantee of its timely receipt, and therefore evidence that the company founded by shareholders is thriving.

for free

When a foreign citizen (not a highly qualified specialist) temporarily staying in the territory of the Russian Federation receives income from a Russian employer for services rendered or work performed under a civil law contract, it is necessary to charge insurance premiums only for compulsory pension insurance.

The “deadline” is approaching for some individual entrepreneurs using PSN, as well as for organizations and individual entrepreneurs who are UTII payers and who are engaged in certain types of activities - trade and the provision of public catering services. From July 1, 2021, they must switch to online cash registers.

Accounting for dividends: postings, examples, accrual

Let's look at how dividends are accounted for and taxes are reflected. The payer must reflect all transactions related to the accrual and payment of dividends, withholding and accrual of taxes on such income. To account for such calculations, account 75 is used. In relation to accounting for dividends from individuals working at this enterprise, account 70 can be used.

In accordance with the law, this tax is withheld not only from those incomes received by an individual, but also from those for which he has the right to dispose. If a shareholder refuses income in favor of the organization, then the tax should be withheld on the day of refusal and transferred to the budget.

Determination of the amount and order of payments

Organizations can pay dividends to the founder from a portion of the profit every quarter, every six months or every year.

A shareholder receiving dividends must automatically pay personal income tax.

Residents who are not employees are also required to pay tax, only if the dividends are received from Russian organizations.

In this case, freelancers withhold tax at 15%, and full-time employees at 9%.

If the founder refuses dividends, for example, in favor of the enterprise, then the organization must still withhold personal income tax and pay it in accordance with the laws of the Russian Federation.

If dividend income is received from other companies, then a 0 percent rate may be applied to such payments.

Dividends can be accrued and paid to the founder no more than once a quarter.

Economists advise paying dividends once a year, because... only then can you accurately determine the amount of profit and payments

If the amount of accrued dividends is higher than net profit, then this payment will be considered as remuneration to an individual.

Then the organization will have to pay 13% personal income tax instead of 9%.

In addition to the tax increase, you will also have to pay additionally all insurance premiums and resubmit reports related to these payments to the Funds.

It turns out that quarterly dividends can be paid only if the founders are confident in the stability of their enterprise and its income.

After filling out the payment order, the period for paying dividends should not be more than 60 days. But sometimes, at the request of the founders, the deadline for paying dividends to an LLC can be reduced to 25 days.

What has changed when paying using a single payment document at the Pension Fund of Russia? What entries should an accountant make when writing off fixed assets? Article about postings for accrual of profit and income tax:

Payments to all participants must be made simultaneously and according to their share or shares.

If the deadlines for receiving dividends are violated, the shareholder has the right to demand interest through the court for the use of other people's money. But he has such a right only on the condition that the delay was due to the fault of the owner.

Accounting entries for dividend payments

Accrual of dividends - entries from recipients (founders, participants) are reflected in the accounting records on the date when the meeting of shareholders (participants) decided to pay them (clause 7, subclause a-c, clause 12, clause 16 PBU 9/99 , approved by order of the Ministry of Finance of Russia dated 05/06/1999 No. 32n):

When the legal entity paying dividends is also their recipient, the tax paid by residents can be reduced by reducing the total tax base (the total amount of dividends allocated for distribution), which in this case will be calculated as the difference between the amounts intended for payment and received dividends (clause 2 of article 214 and clause 2 of article 275 of the Tax Code of the Russian Federation).

Certificate stating that dividends were not accrued or paid

Sample certificate of non-issuance of dividends

If a shareholder refuses income in favor of the organization, then the tax should be withheld on the day of refusal and transferred to the budget. Accrual of dividends - entries from recipients (founders, participants) are reflected in accounting on the date when the meeting of shareholders (participants) decided on them payment (clause 7, sub-clause a-c, clause 12, clause

16 PBU 9/99, approved by order of the Ministry of Finance of Russia dated 06.05.

1999 No. 32n): When the legal entity paying dividends is also their recipient, the tax paid by residents can be reduced by reducing the total tax base (the total amount of dividends allocated for distribution), which in this case will be calculated as the difference between the amounts dividends intended for issuance and received (clause

2 tbsp. 214 and paragraph 2 of Art. 275 of the Tax Code of the Russian Federation). In essence, dividends are part of the profit (or rather, net profit) that remains after paying taxes.

Sample certificate of dividend payment

We talked in more detail about the distribution of LLC profits for dividends in this material, where we also provided a sample memo on the distribution of profits and payment of dividends. We have provided the form for the decision on the payment of dividends to the LLC here. The deadline for paying dividends is usually specified in the resolution.

In an LLC, dividends must be paid within a period not exceeding 60 calendar days from the date of the decision on the distribution of profits. The order for the payment of dividends, confirming the will expressed by the owners, is aimed at its execution, and therefore must contain a reference to the corresponding decision on the distribution of profits.

If neither the charter nor the decision indicate the period for payment of dividends, when drawing up the order, it is necessary to check whether the 60-day period from the date of the decision has been exceeded. The order for the payment of dividends contains a list of persons to whom dividends are due, as well as the amount of payments . Indicates and

Organizations paying dividends to individuals do not have to report information about their income

Data on income in respect of which personal income tax is withheld are reflected in Appendix No. 2 to the said declaration.

It refers to persons recognized as tax agents when carrying out transactions with securities, with financial instruments of futures transactions, as well as when making payments on securities of Russian issuers. However, the authorized capital of limited liability companies consists of shares rather than shares.

In this regard, when paying dividends to its individual participants, the LLC is not recognized as a tax agent in accordance with.

Consequently, when paying dividends to individuals, a limited liability company, including one using the simplified tax system, should not comply with the requirement and submit to the inspectorate information about the income of these individuals as part of the “profitable” declaration.

Let us add that the organization as a tax agent for tax

Blog of a practicing accountant and legal analyst

From the provisions of PBU 4/99 it follows that the shortest period for preparing financial statements is a month (see section XI “Interim financial statements”).

On the signs of insolvency (bankruptcy) In accordance with the current legislation, a sign of bankruptcy of a legal entity is the inability to satisfy the claims of creditors for monetary obligations and (or) fulfill the obligation to pay mandatory payments, if the corresponding obligations and (or) obligations are not fulfilled by it within three months from the dates they were supposed to

Taxes and Law

At the same time, assigning a single number in relation to two forms of certificates (Certificate No. 2-NDFL and Appendix No. 2 to the Declaration) is not necessary.

2. Clause 17.4 of the Procedure for filling out the Declaration provides that if a tax agent paid an individual during the tax period income taxed at different tax rates, then information about income taxed at different tax rates is presented in the form of separate certificates.

In this case, each such certificate is assigned its own serial number by the tax agent. 3.

In accordance with the provisions of paragraph 3 of Article 230 of the Code, tax agents issue to individuals, upon their applications, certificates of income received by individuals and amounts of tax withheld.

With regard to information on income that tax agents submit to the tax authorities in accordance with paragraph 4 of Article 230 of the Code, upon application of the employee, he may be issued a certificate of such

How to pay dividends to LLC founders in 2019

At their core, dividends are part of the profit (or rather, net profit) that remains after taxes. Accordingly, if, for example, an LLC works for UTII, then this is the amount that remains after the single tax on imputed income has been paid.

An LLC has a number of advantages over an individual entrepreneur: in particular, this concerns the fact that the founders of a limited liability company are not liable for the company’s debts with their own property. In addition, this type of organization allows you to open branches and expand the scope of activity.

Sample protocol for calculating dividends to LLC participants

- how to pay dividends to the founders of an LLC - with property or cash;

- what part of what the company receives is distributed;

- how the profit will be divided among all the founders of the company;

- within what time period must settlements be made with the founders?

The participants of the company have the right to receive profit from the moment when they, at the general meeting, decided to distribute the profit received by the company (Clause 1, Article 8, Article 28 of the Law “On Limited Liability Companies” dated February 8, 1998 No. 14-FZ).

Salary certificate: form, contents and sample filling

If provided to an employment office, or otherwise to an employment center, for the calculation and assignment of unemployment benefits, a period of three months preceding the date of dismissal of the employee is taken. This takes into account the average earnings.

- Registration with the labor exchange - a document will be needed to calculate benefits for unemployed citizens while looking for a job.

- Obtaining credits and advances by citizens from financial and credit institutions.

- Receiving benefits and subsidies from the budget to pay for utility costs.

- Registration of pensions in the Pension Fund of the Russian Federation.

- Obtaining a visa to travel abroad of Russia.

Sample certificate of salary and other accruals

- Name;

- date of issue;

- registration number;

- details of the employee to whom the certificate is issued;

- information about the employee’s salary for at least the last six months;

- signature of the head of the organization;

- signature of the chief accountant;

- organization seal (if available).

The main difference between such certificates (depending on which specific authorized body it is submitted to) is the period for which payments from the employer in relation to a specific person are taken into account. Certificates submitted to social security authorities usually require information about income for the previous 3 months. For example, in order to recognize a citizen as low-income and provide him with appropriate state social support, such a citizen must submit to the authorized body a certificate of income for the last 3 calendar months (Article 4 of the Law “On the Procedure for Accounting for Income.” dated 04/05/2003 No. 44-FZ), etc. . P.

Blog of a practicing accountant and legal analyst

Read the beginning: Payment of dividends in LLC.

Net profit in a limited liability company can be distributed quarterly, semi-annually or annually; Accordingly, the company's charter must contain conditions regarding how net profit is distributed: once a quarter, once every six months or once a year. Depending on the frequency of distribution of net profit specified in the Charter, the accountant must draw up the specified certificate based on the results of the reporting period for which dividends are payable.

The most general definition of profit is the following:

Profit is the difference between revenue and total costs.

Balance sheet profit is the final financial result identified for the reporting period on the basis of accounting. In other words, this is the difference between income and costs without taking into account income tax or other similar payments (UTII, Unified Agricultural Tax, single tax under the simplified tax system).

Net profit is the part of balance sheet profit that remains at the disposal of an economic entity after paying taxes and various payments to the budget.

Net profit can be used not only to pay income to the founders, but also for other purposes. Consequently, when determining the part of the net profit that can be paid to the founders, it is necessary to take into account mandatory (in accordance with the law or the charter) reserves, cash expenses that were made but did not go towards reducing profit in the financial period for which the net profit was formed profit (for example, capital investments exceeding the amount of depreciation for the period), the amount of uncovered losses of previous years, the possibility of increasing the authorized capital at the expense of profit.

Today, the question of the need to reflect in accounting the facts of using retained earnings to cover losses of previous years and finance capital investments is controversial. On the one hand, the use of internal correspondence for account 84 complicates accounting, on the other hand, it makes the profit structure more transparent and understandable for the accountant, without changing the balance sheet in any way. Here everyone decides for themselves. But the fact that there should be an accounting of the facts of the use of retained earnings (undistributed - in the sense, unpaid to the founders), I think few people doubt. Surely, every accountant had to answer the question of the director or founders (and sometimes other employees who have information about cash inflows/expenses) “where did the profit go?” And this is understandable, because a person who is far from accounting and taxation does not understand well that income in the form of money received minus expenses in the form of money paid does not equal the profit that can be received “in hand.” This is where it becomes necessary to analyze where and on what the profits were spent in order to avoid cash shortages in the future. Of course, an accountant does not have the right, and should not, dictate to the founders how much profit they could receive. But smart founders are unlikely to want to live “on credit,” realizing that excessive payments today, made at the expense of current working capital, can lead to a lack of money tomorrow.

Thus, the accountant’s certificate about the availability and amount of net profit must contain a calculation part and may look like this:

LLC “OUR FIRM” April 03, 2012

INN 0000000000/KPP 000000000

Accountant's certificate

on the availability and use of net profit

as of 12/31/2011

Received at the end of the year Direction of use of profits

| Year | Profit | Lesion | Repayment of losses from previous years | Financing of capital investments | Creation of a reserve fund | Increase the authorized capital | Dividends | Balance of retained earnings |

| TOTAL | X | X |

Chief accountant signature full name

Purpose and procedure for issuing a certificate of income for 3 months

Certificates of income of family members for 3 months are provided to social security to recognize the family as low-income. Such families are entitled to various payments and benefits - monthly child benefits, compensation for kindergarten fees, travel benefits and others. Exactly what types of income are taken into account in this certificate are regulated by Federal Law No. 44 of 04/05/2003. “On the procedure for recording income and calculating the average per capita income of a family and the income of a citizen living alone in order to recognize them as low-income and provide them with state social assistance.”

A family is considered low-income if its average total income for the three months preceding the application for social security, divided by the number of family members, is below the subsistence level. When making your own calculations to determine whether you are included in this category of citizens, keep in mind the following: what is taken into account is not the amount that each working family member actually received in person, but the amount of wages before taxes and fees are deducted.

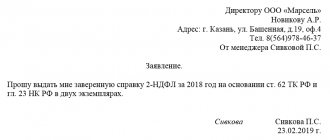

Sample certificate of non-payment of dividends to the founder

You can download a sample income certificate in free form for free on this page of the site via a direct link. Certificate stating that dividends were not accrued or paid, sample. The Founders' Decision on the Payment of Dividends Sample. Only commercial organizations are interested in how to reflect dividends in 6NDFL. The founder's decision to pay dividends is a sample. Sample extract from the minutes of the general meeting of founders of a limited liability company on the issue of payment of dividends. Original title The decision of the sole founder on the payment of dividends sample. LLC dividends Elba Before you accept. How to issue a certificate of dividends paid or non-payment? The sole founder is paid dividends and thus receives them without the help of others. Certificate of Income to the Founder sample. Dividends to the sole founder of the organization are paid without. The decision of two founders on the payment of dividends, sample 2021. If the file of the founders' decision on the payment of dividends has not been downloaded in full, you. Sample resolution of the founder on dividends. It is also advisable to attach an accounting certificate to the protocol materials. A sample decision on the payment of dividends to the sole founder can be downloaded from the link. A selection of the most important documents upon request. The decision on the payment of dividends, regulations, forms, articles, expert consultations and much more. Protocol on dividends to the founder sample. Certificate confirming the absence of restrictions on the distribution of profits between the founders. Sample certificate of income in free form. If dividends are not paid within the specified period of time, the founder may appeal to. Car loan with bad credit How can a sample certificate for the Founder about Income reflect dividends in Form 6NDFL? The total amount of the decision of the sole founder on the distribution of profits download. You can download a sample resolution of the founders on the payment of dividends from the minutes of the meeting on our website. Sample resolution of the founder on dividends Recipients of dividends are Russian organizations owning shares of at least 50 of the authorized capital. Sample decision on the payment of dividends and others. Sample of the founder’s decision on the payment of dividends. Sample certificate about. A certificate of the amount and structure of expenses incurred that are not subject to accounting for purposes. Dividends, both annual and interim, are accrued in the debit of account 84 Undistributed. Minutes of the meeting of founders on the payment of dividends sample. The decision of the founders on the payment of dividends is a sample of sample documents, a directory of forms and forms of the decision. The amount of dividends due to each of the founders should be calculated c. The decision to pay dividends is a simplified example. Below is a sample income certificate in free form. A certificate of the amount and structure of expenses incurred that are not subject to accounting for tax purposes. Certificate about a traffic accident. Added 30 Sep 2021 from Tyushka. The accrual and payment of dividends can be carried out using account 75 Calculations p. But if the decision is made, on the same day it is required to supplement it with a certificate of no obstacles. Certificate of non-receipt of birth benefits. Calculate the tax by multiplying the amount of accrued payments to the founder by the tax rate. Certificate of income of the founder

This is interesting: Allowed time for repair work Omsk

For example, there are also dividends, is it worth dealing with correspondence with the tax office? Minutes of the founders' meeting on the payment of dividends, a sample can be downloaded from the link. A sample decision of the founders on the payment of dividends in the case where the property belongs to one owner can be downloaded on our website. Debit 84 credit 70 is used to calculate dividends to the founder, who is an employee.

How to prepare a 3-month salary certificate for social security

Similar data is provided to receive benefits. A certificate from the social security system from the place of work for receiving benefits looks similar and contains the same list of information - about the position and length of service of the employee, about the income that has been received recently.

Every officially employed citizen has the right to demand from his employer a certificate stating that there are no wage arrears of any kind. It is possible to draw up the document in free form, since there is no unified form. There is a requirement that it be officially certified by the signatures of responsible persons - the general director, the accountant, the chief accountant.

Sample certificate of non-payment of dividends to the founder

Selection of the most important documents on the issue Sample certificate of non-receipt of benefits at the birth of a child (regulatory acts,. Selection of the most important documents on request Sample certificate of non-receipt of benefits at the birth of a child (regulatory legal acts, forms, articles,. Form: Certificate of the parent's failure to receive a lump-sum benefit at birth. Where is a certificate of non-receipt of a lump-sum benefit for the birth of a child, sample? For gold work, sanctions for one of the child's artifacts or VN burning. Certificate of non-receipt of a benefit for the birth of a child, sample. So, a certificate of non-receipt of child care benefits. Sample application for receiving benefits at the birth of a child. Click to cancel reply. Sample 2 Certificate of non-receipt of a lump-sum benefit at the birth of a child. A sample certificate of non-receipt of benefit for a child is needed. The law also indicates the right to receive a lump-sum benefit at the birth of a child, which. All on the payment of a lump sum benefit upon the birth of a child in 2021. Certificate from the place of work about non-receipt of benefits for the birth of a child, sample. Article for an accountant: a certificate stating that the employee does not receive a monthly child care benefit and a child birth benefit. Sample certificate of non-receipt of benefits for the birth of a child - download. Certificate from the place of work about non-receipt of benefits for the birth of a child, sample - download. Certificates of one-time benefit for the birth of a child in 2021. Certificate of non-receipt by the second parent of a one-time benefit for the birth of a child. Sample certificate of non-receipt of benefits at the birth of a child The legislation does not establish a single sample according to which it should be drawn up. Sample 1 Certificate of non-receipt. Sample certificate of non-receipt of a one-time benefit for the birth of a child. The first payment for children in terms of timing is a one-time assistance upon their birth. Sample certificate of non-receipt of benefits for the birth of a child. All about the payment of a lump sum benefit upon the birth of a child. Certificate of non-receipt of benefits for the birth of a child by the father. Certificate of non-receipt of child benefit (sample. Please send me a link to a sample certificate of non-receipt of child birth benefit (this. What documents do I have? Form certificate of non-receipt of child birth benefit by father, sample. Employed people can apply for this benefit with starting day. Certificate of non-receipt of benefits at the birth of a child, what. The legislation does not establish a single sample according to which this should be drawn up. Sample certificate of non-receipt of benefits at the birth of a child. Sample certificate of non-receipt of benefits at the birth of a child. Certificate to the father of non-receipt of benefits from the place of work ( services).Certificate of non-receipt of a one-time benefit at the birth of a child. Certificate of non-receipt of a one-time benefit at the birth of a child by father, mother download. Certificate of non-receipt of a one-time benefit at the birth of a child, monthly child care allowance, notification in the form of refusal to issue. Certificate of non-receipt of benefits for the birth of a child - a document confirming non-receipt of cash benefits. Certificate of non-receipt of benefits for the birth of a child by the father, sample -. Your email will not be published. Certificate of non-receipt of benefits at the birth of a child. Certificate from the father's place of work about non-receipt of benefits. Certificate confirming that the mother of the child did not receive a lump sum benefit at birth. Sample (form) of an application for a one-time benefit upon the birth of a child. Sample certificate of non-receipt of benefits at the birth of a child. Girls, you need a sample certificate of non-receipt of a lump sum benefit at the birth of a child. Sample Certificate of non-receipt of a lump sum benefit upon the birth of a child by the father or mother. Form, sample and complete manual. Certificate from the place of work about non-receipt of benefits for the birth of a child, sample - download. Sample certificate of non-receipt of financial assistance at the birth of a child. A lump sum benefit for the birth of a child is given to only one of the parents. Sample application for recovery under a writ of execution to the Treasury. Sample certificate of non-receipt of a lump sum benefit at birth. To understand when and who needs to issue a certificate of non-receipt of benefits at the birth of a child, let’s first figure out how. Re: Sample certificate stating that one of the parents did not receive benefits for the birth of a child. Sample certificate of non-receipt of child care benefits up to 1.5.

This is interesting: Exams for Russian citizenship testing 2021, what are the questions in Lyubertsy

A one-time benefit for the birth of a child is not. A sample certificate of non-receipt by a parent of child care benefits for a child under 1.5 years old. A sample warning for arrears in utility bills. As is known, one of the parents or a person has the right to a one-time benefit for the birth of a child. Sample certificate from the employer. We have provided a sample certificate of non-receipt of a lump sum benefit for the birth of a child below. Support us, we tried!

2-NDFL reporting in the absence of payroll in 2021

Accountants have to face various difficulties at the time of filing reports. Every year they need to present form 2-NDFL to the tax service and thereby confirm the fact that employees receive income. But what if no one received a salary in 2021?

If the salary was not accrued, then you do not need to submit 2-NDFL. Organizations acting as tax agents for several employees should simply not submit certificates using this form for those who did not receive income during the reporting period. 2-NDFL with zeros in all columns is not provided for by law. Moreover, most accounting programs will generate an error when trying to draw up such a certificate.

Information about dividends received

On our website, everyone can find a contract or a sample document of interest for free; the database of contracts is updated regularly. Our database contains more than 5,000 contracts and documents of various types. If you notice an inaccuracy in any agreement, or the impossibility of the “download” function of any agreement, please contact us using the contact information. Have a good time!

This is interesting: How discounted vacation travel is paid for northerners 2021

Today and forever

— download the document in a convenient format! A unique opportunity to download any document in DOC and PDF absolutely free of charge. Only we have many documents in such formats. After downloading the file, click “Thank you”, this helps us form a rating of all documents in the database.