Transportation expenses in accounting: entries and examples – Business Ideas

Transport costs are the costs of an enterprise directly related to the delivery of purchased goods to the counterparty.

The procedure for accounting for transportation costs for delivery in accounting is reflected in the accounting policy. The amount of transportation costs may be included in the price of the goods or issued as a separately provided service.

Depending on the method of accounting for transportation costs, the corresponding transactions are generated.

Features of accounting for transportation costs

Transportation costs (otherwise known as transportation and procurement costs) include the following costs:

- Payment of transportation costs for delivery of goods;

- Payment for loading and unloading operations;

- Temporary storage fee.

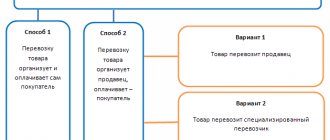

Payment options for the cost of goods delivery services:

- The company includes the cost of delivery in the price of the goods;

- Refund of the amount spent by the seller in accordance with the concluded agreement with the buyer;

- The buyer pays transport costs separately;

- They pay for services in accordance with the concluded agreement for the delivery of goods with the transport company.

Example 1. The amount of transportation costs is included in the price of the goods

The organization VESNA LLC purchased equipment for a total amount of 531,000.00 rubles, incl. VAT - RUB 81,000.00 Transport costs amounted to RUB 29,500.00, VAT RUB 4,500.00. According to the accounting policy of the enterprise, transportation costs are included in the cost of goods. Account 15 is used to form the cost price.

According to paragraph 6 of PBU 5/01, delivery costs may be included in their actual cost. The actual cost is written off to account 41 “Goods”.

The accounting records reflect transportation costs for delivery; we make the following entries:

| Debit Account | Credit Account | Transaction amount, rub. | Description of transaction posting | A document base |

| 15 | 60 | 450 000,00 | The purchase price of purchased equipment is taken into account | Consignment note (TORG-12), Invoice received |

| 19 | 60 | 81 000,00 | VAT on purchased equipment has been taken into account | |

| 15 | 60 | 25 000,00 | Transport costs included | |

| 19 | 60 | 4 500,00 | VAT on transport costs included | |

| 41 | 15 | 475 000,00 | The actual cost of purchased equipment is taken into account |

Example 2. The amount of transportation costs is included in sales expenses

VESNA LLC purchased goods for a total amount of RUB 413,000.00, incl. VAT 63,000.00 rub. Transportation costs amounted to RUB 20,060.00, incl. VAT RUB 3,060.00 According to the accounting policy, transportation costs are included in selling expenses. The cost price is formed on account 41.

Get 267 video lessons on 1C for free:

- Free video tutorial on 1C Accounting 8.3 and 8.2;

- Tutorial on the new version of 1C ZUP 3.0;

- Good course on 1C Trade Management 11.

According to paragraph 13 of PBU 5/01, transportation costs are included in sales costs.

https://www.youtube.com/watch?v=Ng4Ifp0Mgog

In accounting, entries for transportation expenses are generated:

| Debit Account | Credit Account | Transaction amount, rub. | Wiring Description | A document base |

| 41 | 60 | 350 000,00 | The purchase price of goods is taken into account | Consignment note (TORG-12), Invoice received |

| 19 | 60 | 63 000,00 | VAT on purchased goods has been taken into account | |

| 44.01 | 60 | 17 000,00 | Transport costs included | |

| 19 | 60 | 3 060,00 | VAT on transport taxes included |

Example 3. Delivery of goods by transport services sells goods to the buyer for a total amount of 885,000.00 rubles, incl. VAT RUB 135,000.00 According to the accounting policy, the cost of transport services is included in the price of the goods.

According to the terms of the contract, VESNA LLC must deliver the goods to the buyer. An agreement has been concluded with a transport company for the delivery of goods.

According to the terms of the agreement, the cost of services for delivering goods to the buyer is RUB 35,400.00, incl. VAT RUB 5,400.00

The accounting records reflect transportation costs under the service agreement; we make the following entries:

| Debit Account | Credit Account | Transaction amount, rub. | Wiring Description | A document base |

| 62 | 90.01 | 885 000,00 | Accounting for revenue from sales of goods | Consignment note (TORG-12), Invoice issued, Consignment note (form 1-T) |

| 90.03 | 68.02 | 135 000,00 | VAT charged on sales of goods | |

| 90.02 | 41 | 885 000,00 | Write-off of goods sold | |

| 44.01 | 60 | 30 000,00 | Accounting for the costs of delivering goods to the buyer by a transport company | Delivery agreement, Certificate of provision of transport services, Bill of lading, Bill of lading (form 1-T), Bill of lading (TORG-12) |

| 19.04 | 60 | 5 400,00 | Accounting for input VAT claimed by the transport company | Invoice received |

| 51 | 62 | 885 000,00 | Buyer payment for goods sold | Bank statement |

| 60 | 51 | 35 400,00 | Payment to the transport company for delivery of goods | Bank statement |

| 90.07.01 | 44.01 | 30 000,00 | Costs for delivery of sold goods are written off | Accounting information |

| 68 | 19 | 5 400,00 | VAT is accepted for deduction | Book of purchases |

Primary documents confirming transportation costs

Source: https://bzkey.ru/transportnye-rasxody-v-buxgalterskom-uchete-provodki-i-primery/

Transport costs associated with the delivery of purchased goods:

If the delivery cost is reflected separately in the supplier’s documents, then the TZR should be included in the cost of goods.

Methods for accounting for material and equipment in the cost of goods:

- include TZR in the cost of goods;

- reflect TZR on account 44

as a separate item of sales expenses.

Method 1: include TZR in the cost of goods.

It should be noted that this method is quite labor-intensive and often contradicts the requirement of rationality, however, it is used in some organizations. Its essence is that the purchased goods are delivered to the warehouse taking into account the cost of the goods and materials, for this purpose the total value of the goods and materials is distributed proportionally between the cost of the received batches of goods. Subsequently, the accounting of goods is carried out in an assessment that includes TZR.

Example 1.

The organization received:

1st batch: Executive table 100 pcs. at a price of 1000 rubles, batch cost 100,000 rubles.

2nd batch: Computer stool 50 pcs. at a price of 800 rubles, batch cost 40,000 rubles.

The total cost of goods received is 140,000 rubles.

Transport and procurement costs = 10,000 rubles.

How to accept this product into the warehouse?

We calculate the delivery costs of each batch in proportion to its cost:

Costs for the supply of the 1st batch: 10,000 * 100,000 / 140,000 = 7,143 rubles.

The cost of the 1st batch, taking into account delivery = 107,143 rubles, this batch will be accounted for at this cost, while the price of one manager’s desk, taking into account the TZR: (100,000 + 7143) / 100 = 1,071.43 rubles.

We carry out similar calculations for the second batch:

Costs for the supply of the 2nd batch: 10,000 * 40,000 / 140,000 = 2857 rubles.

Cost of the 2nd batch including delivery = 42,857 rubles.

Price of a computer table including TZR: (40000 + 2857) / 50 = 857.14 rubles.

Postings for accounting for goods received, taking into account delivery:

| Sum | Debit | Credit | Contents of operation |

| 107143 | 41.1 | 60 | A batch of executive tables has been received |

| 43857 | 41.2 | 60 | A batch of computer tables has been received |

If the supplier has allocated VAT and issued an invoice (together with shipping documents), then we subtract the amount of VAT from the cost of consignments of goods and set it for deduction (d19 d60 and d68.VAT d19).

Next, when selling a product, its cost is written off: d90.2 k41.1(2

). In this case, the cost of transportation costs will be included in the cost of goods sent for sale.

Method 2: reflect TZR on account 44 as a separate item of sales expenses

TZR can be accounted for separately on account 44 “Sales expenses”, for which a separate sub-account is opened on this account; for example, it can be called “44/TR”. At the end of the month, transportation costs accumulated on account 44/TR are written off in proportion to the cost of goods sold for the month.

An example of accounting for goods and materials on account 44:

Within a month, goods were purchased. At the same time, the supplier allocated the cost of technical and equipment separately.

1st batch: Executive table 100 pcs. at a price of 1,000 rubles, batch cost: 100,000 rubles.

2nd batch: Computer stool 50 pcs. at a price of 800 rubles, batch cost: 40,000 rubles.

Total cost of goods received: RUB 140,000.

Transport and procurement costs: 10,000 rubles.

In addition, the organization itself purchased goods and delivered them to its warehouse.

Inventory for independent procurement (per month):

Gasoline: 2,000 rub.

Car repair: 4,000 rub.

Driver's salary: RUB 15,000.

Accrued insurance premiums for the driver's salary (30%): RUB 5,000.

Car depreciation: RUB 1,000.

Postings for accounting of goods and materials for the month:

| Sum | Debit | Credit | Contents of operation |

| 100000 | 41.1 | 60 | A batch of executive tables has been received |

| 40000 | 41.2 | 60 | A batch of computer tables has been received |

| 10000 | 44/TR | 60 | Delivery costs included |

| 2000 | 44/TR | 10 | Gasoline expenses written off |

| 4000 | 44/TR | 76 | Costs for car repairs at a service station are taken into account |

| 15000 | 44/TR | 70 | Driver's wages paid |

| 5000 | 44/TR | 69 | Insurance premiums are calculated on the driver's salary |

| 1000 | 44/TR | 02 | Vehicle depreciation reflected |

It is important to remember that at the end of the month, not all inventory items are written off, but only a part of them, proportional to the goods shipped.

The procedure for determining the amount of inventory items subject to write-off

To determine the amount of inventory items subject to write-off, it is necessary to analyze account 41

“Goods” and

account 44/TR

“Sales expenses”.

Analysis of account 41:

For example, at the beginning of the month the organization had goods worth 300,000 rubles. (initial account balance 41), within a month more goods were received for a total amount of 700,000 rubles. (debit turnover of account 41), goods were sold within a month for a total amount of 500,000 rubles. (credit turnover of account 41).

Analysis of account 44/TR:

For example, the opening debit balance is RUB 30,000. During the month, expenses in the amount of 70,000 rubles were reflected in the debit of account 44/TR.

Thus, goods worth 1,000,000 rubles. (opening balance plus turnover for the month in the debit of account 41) corresponds to transport and procurement expenses in the amount of 100,000 rubles. (opening balance plus expenses for the month in the debit of account 44/TZR).

The amount of TZR that needs to be written off from the credit of account 44/TR

(corresponding to goods sold) will be:

TZR for goods sold = 100,000 * 500,000 / 1,000,000 = 50,000 rubles.

Shipped goods in the amount of 500,000 rubles correspond to transportation costs in the amount of 50,000 rubles. It is this amount that will need to be written off at the end of the month in one transaction.

| Sum | Debit | Credit | Contents of operation |

| 50000 | 90.2 | 44/TR | The amount of expenses for the delivery of purchased goods in connection with its sale has been written off. |

The general formula for calculating TZR subject to write-off for a month = (opening balance on the debit of account 44/TR + turnover on the debit for the month of account 44/TR) * turnover on the credit of account 41 / (opening balance on the debit of account 41 + turnover on the debit for month of account 41).

The organization chooses one of the above methods of accounting for goods and materials (including goods and materials in the cost of goods or reflecting goods and materials as a separate expense item on account 44), reflects its choice in its accounting policy.

Transport costs in production to what account?

Transportation costs - posting to reflect them, types and accounting options. In this article you will find information on this topic.

Concept and types of transport costs

Tzr when purchasing materials

TZR when purchasing goods

Transport costs when selling goods or finished products

Results

Concept and types of transport costs

Most companies engaged in manufacturing or trading activities use the services of transport companies or have their own fleet of vehicles. When purchasing assets, the organization also incurs other associated costs, which, together with delivery costs, form transportation and procurement costs (TPC).

Each company is required to enter and approve in its accounting policy a list of expenses that should subsequently be attributed to TZR. To do this, you need to use legal acts from the following list:

- PBU 5/01 “Accounting for inventories” (approved by order of the Ministry of Finance of the Russian Federation dated 06/09/2001 No. 44n).

Clause 6 of this document shows the costs associated with the procurement and delivery of materials to the place of their use. This:

- costs associated with procurement and delivery;

- costs associated with maintaining enterprise personnel engaged in procurement and storage;

- transportation services for materials and equipment to the place of their use;

- interest accrued on loans from business partners;

- interest accrued as part of loans for the purchase of inventories, provided that these interests were formed before the accounting of inventories.

- Guidelines for accounting for inventories (approved by order of the Ministry of Finance of Russia dated December 28, 2001 No. 119n).

Clause 70 of the guidelines contains a list of material and equipment that can be included in the purchase of materials. This list includes the following types of expenses:

- for loading and transportation, if they are paid outside the basic cost of materials;

- for wages, social contributions and business trips of workers involved in the procurement and storage of materials;

- on the maintenance of actually used warehouse premises;

- payment for services of intermediary companies and individual entrepreneurs;

- to pay for storage services until the moment when the goods and materials arrive at the buyer;

- on interest accrued as part of loans for the purchase of inventories, if these interests were accrued before the moment of accounting for inventories;

- by the amount of losses en route, if their size is within the limits of the standards for natural loss;

- other expenses.

- All-Russian classifier of types of economic activity (approved by order of Rosstandart dated January 31, 2014 No. 14-st).

The classifier has a section “Transportation and storage”, it provides a list of transport services that you should focus on. The fact is that the Tax Code of the Russian Federation does not contain wording on what applies to this type of expense. Therefore, when organizing accounting and tax accounting, it is necessary to create and approve in the accounting policy an identical list of transport services.

It should be taken into account that the type of technical documentation is of great importance for accounting. Namely:

- Inventory related to the acquisition of materials;

- TZR due to the purchase of goods: in a trading company;

- non-trading company;

Let us note the features of accounting for each type.

Tzr when purchasing materials

PBU 5/01 determines that TZR are included in the actual cost of materials (clauses 6, 11). Paragraph 83 of the guidelines allows the use of three methods of recording TKR in terms of purchases. The company is instructed to choose one of the methods below and include it in the accounting policy of the enterprise.

- The 15th account “Procurement and acquisition of materials” is used for reflection.

In addition to the mentioned 15th account, with this method and when applying accounting prices, the 16th account “Deviation in the cost of material assets” is also used. Reference prices can be taken from the following categories:

- negotiated prices (they should not take into account associated costs for procurement and delivery);

- prices in force in previous periods;

- planned prices;

- average prices valid for a certain group of inventories.

In order to show what records are made when materials are received and written off, we will draw up the following table:

| The essence of the recording | Dt | CT |

| We record the cost of materials received based on the primary documents received from the partner (at purchase prices) | 15 | 60, 71, 76 |

| We record the technical requirements based on the primary documents received from the supplier (clause 85 of the guidelines) | 15 | 60, 71, 76 |

| We receive materials using discount prices | 10 | 15 |

| We write off the amount formed as a positive difference between the actual price and the accounting price | 16 | 15 |

| If a negative difference is formed, the entry will be reversed | 15 | 16 |

| We record the write-off of materials for production using the accounting price | 20, 23 | 10 |

| We record the difference between the actual and accounting value of the inventories transferred to the buyer, if this difference is positive. Otherwise, the same posting is reversed. | 20, 23 | 16 |

When forming the above table, in addition to those already described, the following accounts were used:

- 10th - “Materials”;

- 20th - “Main production”;

- 23rd - “Auxiliary production”;

- 60th - “Settlements with suppliers and contractors”;

- 71st - “Settlements with accountable persons”;

- 76th - “Settlements with various debtors and creditors.”

Paragraph 87 of the guidelines provides formulas used to calculate the percentage of write-offs of price deviations. The calculation procedure is as follows:

K = (Off0 + Off1) / (M0 + M1) × 100,

Where

K is the size of the deviation as a percentage;

Deviation0 - the size of the deviation at the beginning of the month (remainder);

Off1 - the size of the deviation accumulated during the month;

M0 - volume of materials at the beginning of the month in accounting prices;

M1 - volume of materials received during the month at accounting prices.

Off2 = K × M2,

Where

Off2 - the size of deviations that can be written off as expenses;

M2 is the volume of materials at accounting prices, which is written off as expenses.

- For reflection, a special sub-account is used on the 10th account “Materials”.

For such circumstances, we present the following tabular form for the records:

| The essence of the recording | Dt | CT |

| We reflect the cost of materials at purchase prices based on primary documents from the partner | 10 | 60, 71, 76 |

| We reflect the technical requirements on the basis of primary documents from the partner (clause 85 of the guidelines) | 10, sub-account “TZR” | 60, 71, 76 |

| We write off materials for production | 20, 23 | 10 |

| We write off inventory items in proportion to the cost of materials generated at the end of the month | 20, 23 | 10, sub-account “TZR” |

The above formulas can also be applied in this case. In this case, the selected calculation method should be approved in the accounting policy.

- TZR are directly included in the actual cost of materials.

This method is available only to those companies whose list of materials used is small and there are groups of materials that occupy a predominant volume in their total quantity. In other words, if the TRP falls on such inventories, then such expenses will be included in the cost of a unit of material.

Also look for information on materials accounting in the article “Accounting entries for materials accounting.”

TZR when purchasing goods

When purchasing goods, appropriate transportation costs can also be taken into account in different ways, which depend on what kind of activity the company is engaged in.

Thus, trading companies are allowed to choose an accounting method from the following list:

- TZR are included in the cost of goods (clause 6 of PBU 5/01): Dt 41, subaccount “TZR” Kt 60.

If account 15 “Procurement and acquisition of material assets” is used to record goods, then the entry will be as follows: Dt 15 Kt 60.

- TZR are included in the costs of selling goods (clause 13 of PBU 5/01), with the following costs:

- are scattered between those goods that are sold and those that remain in the warehouse (in the description of account 44, chart of accounts approved by order of the Ministry of Finance of the Russian Federation dated October 31, 2000 No. 94n),

- written off to cost in full: Dt 44 Kt 60.

At the end of the month, sales-related expenses can be written off to cost. The entry will be as follows: Dt 90, subaccount “Sale expenses” Kt 44.

The chosen accounting method must be included in the accounting policy of the enterprise.

In the above entries, in addition to those already mentioned, the following accounts are given:

- 02nd - “Depreciation”,

- 41st - “Goods”,

- 44th - “Sales expenses”,

- 70th - “Settlements with personnel regarding wages”,

- 69th - “Calculations for social insurance and security”,

- 90th - “Sales”.

If a partial write-off is used, then the accounting policy will need to include a method that the company will use when dividing inventory between goods sold and those that remained stored in the warehouse. The regulations do not provide guidance on which method to choose in different circumstances. That is, companies are free to choose it themselves.

However, you can get your bearings using the formula given in Art. 320 Tax Code of the Russian Federation:

K = (TP0 + TR1) / (T1 + T2) × 100,

Where

K is the average percentage of goods and materials that fell on inventory balances at the end of the month;

TP0 - transport costs, which correspond to unsold inventory balances at the beginning of the month;

TP1 - transport costs incurred in the current month;

T1 - the cost of goods that have already been purchased and sold in the current month;

T2 - the cost of goods that were purchased but not sold at the end of the month.

TP2 = K × T2,

Where

TP2 - transport costs that fell on unsold inventory balances at the end of the month;

T2 - the cost of goods that have already been purchased but not sold at the end of the month.

Non-trading organizations have the right to take into account transportation costs as sales expenses. This definition is contained in paragraph.

227 guidelines for accounting for inventories, approved by Order of the Ministry of Finance of Russia dated December 28, 2001 No. 119n.

Non-trading organizations should be considered those companies that, in addition to trading operations, carry out other types of economic activities.

Companies included in this category have the right to choose whether to spread costs between the cost of goods already sold and inventory balances. However, there are also some recommendations in this regard, contained in paragraph 228 of the guidelines. It is proposed to distribute expenses if:

- TZR exceed 10% of sales revenue,

- TZR is uneven throughout the year.

In addition, TZR are also taken into account in the actual cost of acquired fixed assets, as read in the article “Rules for keeping records of investments in non-current assets.”

Transport costs when selling goods or finished products

The following options for accounting for delivery costs are possible:

- If the delivery price is included in the price of the product.

Source: https://f-52.ru/transportnye-rashody-v-proizvodstve-na-kakoy-schet/

Accounting posting services

Many companies, when carrying out their activities, resort to the services of third-party organizations. Most often this is associated with activities related to the production or sale of products. Any services provided to your organization must be justified and reflected in the accounting entries.

Legislative regulation of registration of services rendered

The legal regulation of accounting for the provision of services is based on the agreement that you have drawn up with the counterparty. Regulation is also carried out on the basis of tax legislation and the Civil Code. In addition, additional regulations apply in educational, security and some other areas.

Since both legal entities and individuals can provide services, settlements with counterparties can be carried out in both non-cash and cash forms. Expenses for services are processed in the same way as all other expenses. The accounting accounts in which transactions are carried out depend on the division, type of production and other factors.

Documents for registering entries for services in accounting

- Invoice.

- Work completion certificate.

- Extract from current account.

- Extract from the payment order.

Tips for registering service entries in accounting

- Before recording service transactions in accounting, it is necessary to obtain documents confirming that the work was completed. Sign an agreement with the company you are working with. The document must be correctly drawn up and reflect all services provided.

- When performing work, it is necessary to fill out the appropriate report. There is no exact form for this document, so it is compiled by the company’s accountant. VAT will be deducted only if there is an invoice, which must be attached to the deed.

- An entry is made in accounting that reflects the amount of expenses for the service excluding VAT. Value added tax is reflected on the basis of the invoice.

- The following accounting entry is made on the basis of statements from the current account and payment order after payment for the work of the company that provided the services. If you paid the counterparty in cash through the cash register, the expenses are processed through an expense order.

- Next, you can deduct value added tax. The VAT amount must be entered in the purchase book under the exact date and number. Then the expenses are written off to cost, which also needs to be reflected in the accounting records using the appropriate entries.

Source: https://biznesanalitika.ru/article/buhgalterskij-uchet-uslug-provodki

Transport expenses in accounting: postings, reimbursement of expenses, write-off of expenses

Enterprises whose specialization is based on selling their own products not directly, but through contractors, must independently take care of how their goods will get to retail outlets or warehouses of partner companies.

In this case, the sale of the goods has already been completed, and ownership passes to the next owner, but the transportation or delivery of products must be agreed upon in advance and all requirements and conditions must be specified when preparing documents for the transaction.

So, if the supplier pays all transportation costs, then a special accounting account must be opened, which will keep track of all expenses for unloading work and costs for transporting products.

VAT: the buyer reimburses the seller for transportation costs

Commentary to the Letter of the Ministry of Finance of Russia dated August 15, 2012 N 03-07-11/299 “On the application of VAT deductions and issuing invoices for transport costs reimbursed by the buyer of goods to their seller”

Perhaps, in the vast majority of cases, goods, products or other valuables purchased by the buyer from the seller must be physically moved from one place to another, for example, transported from the supplier's warehouse to the buyer's warehouse. Moreover, often we are not talking about delivery of purchased goods to a neighboring street or within the same city, but about transportation to other localities or even to another country. How to correctly calculate VAT in one of the special cases arising during the transportation of goods is described in the commented Letter of the Ministry of Finance of Russia dated August 15, 2012 N 03-07-11/299.