Accounting Methods

The main concepts used by accountants are “debit” and “credit”. These terms are quite abstract, can be used interchangeably, and both can be interpreted as methods of describing a decrease or increase in funds in an account.

The concepts of debit and credit are opposite. Translated from Latin, debit means “he owes” and credit “I owe.”

In simple words, debit is savings available or funds received into an account. In relation to a company, a debit is the amount in the cash register or in the current account . In addition to cash, property is also debited.

A loan is an expense for a company or individual.

Accounting statements of income and expenses

To assess the activities of an enterprise or income and expenses in the home budget, the concepts of debit and credit are recorded in a table with two columns. The debit is recorded on the left and the credit on the right. Analysis of all incoming and outgoing transactions allows you to see the real picture of the movement of finances.

Ideally, debit and credit should match; even better, if debit exceeds credit, this means that you are in profit.

If the credit amount is greater than the debit amount, this indicates that the organization is unprofitable. There is a budget deficit. A table of income and expenses helps to identify unnecessary expenses and maintain balance.

When does a debit become an income and when does it become an expense?

In the accounting posting system, there is a division of accounts into active and passive:

- Active accounts reflect information about the receipt, debit and current state of the enterprise’s funds. Debit on such accounts shows the receipt of funds, investments and repayment of debt to the company. A loan shows the expenditure of funds and a decrease in the organization’s property.

- Passive accounts reflect the sources of economic funds and changes. Here, debit reflects the expenditure of profits and funds, and credit reflects income (debt repayment, profit growth).

On active accounts, debit is an income, and credit is an expense, but on liabilities, the functions of the methods are opposite. The movement of funds occurs from credit to debit in the case of assets, and from debit to credit in liabilities.

Debit reflects the balances of property in active and passive accounts, and credit reflects sources. To connect the two concepts, the term “ balance ” is used.

If the debit on active accounts increases, this indicates an increase in the organization's ownership. As the debit on the passive account increases, the company's funds decrease.

Account 68 in accounting: postings:

Account 68 in accounting serves to collect information about mandatory payments to the budget, deducted both at the expense of the enterprise and employees. The amount and procedure for paying tax amounts are reflected in the Tax Code of the Russian Federation, according to which calculations must be made. The accountant records all obligations to the state, which are then transferred to him at a certain period and at the same time written off from the account.

What is taken into account in account 68?

According to the Standard Chart of Accounts, the 68th is called “Calculations for taxes and fees”. It quite obviously follows from this that it is created to account for settlements with the state budget.

All commercial organizations in one way or another encounter the concept of taxes. What it is? Taxes are a fixed amount that must be paid by an individual or legal entity to finance the state.

A full description of each payment is contained in the Tax Code of the Russian Federation.

If everything is more or less clear with taxes, then what is meant by the concept of “collection”? This is a contribution for which an obligation arises when an individual or business needs to obtain legal services from the government or other authorities. The fee may also be established for commercial companies as a mandatory condition for conducting business activities in a certain territory.

Tax obligations of organizations

Payments for taxes and fees can be sent to the federal, regional or local budget. It depends on the type of obligation. Federal taxes include VAT, excise taxes, and income taxes. Local and regional taxes consist mainly of amounts assessed for the use of land and property.

When considering the tax obligations of an enterprise, it would be correct to systematize payments in the context of this economic entity. Let's group the main types of taxes and fees, data on which are entered into account 68 in accounting, according to the method of their payment:

- from the amount of sales proceeds - excise taxes, VAT, customs costs;

- write-off to the cost of products (works, services) - taxes on land, water resources, mining, on property and transport of an enterprise, gambling business;

- from net profit - corporate income tax.

In addition, account 68 is also used to pay personal income tax levied on the income of individuals (employees of the enterprise).

Depending on the tax regime under which the enterprise operates, payment rates and their total number change. For example, organizations using the simplified tax system may be exempt from paying VAT, property and profit tax, and personal income tax.

Account characteristics

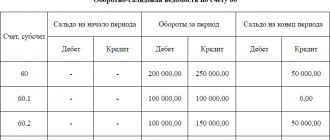

Account 68 in accounting is active-passive. At the end of the period, both a debit and a credit balance can be formed. In this case, the amounts in credit indicate the size of the enterprise’s obligations to the state, and in debit - vice versa. It turns out that any accrual occurs on credit, and write-off occurs on debit. Most often, of course, the organization has a credit ending balance on account 68.

Debit turnover indicates either the payment of taxes and fees, or the amount of VAT to be reimbursed when purchasing goods from suppliers. Credit turnover arises when obligations are formed and VAT is payable according to the invoice.

Analytical accounting

As can be seen from the characteristics of the enterprise’s obligations to the state, the number of taxes is enough to turn account 68 into confusion. To systematize the data, sub-accounts are created for a group of tax payments and fees: this way you can always view the necessary information.

https://www.youtube.com/watch?v=wrFTIL6tK00

Let's consider an example of analytical accounts for the main types of tax payments and fees from a legal entity:

- 68/01 – personal income tax;

- 68/02 – VAT;

- 68/03 – excise taxes;

- 68/04 – income tax;

- 68/05 – tax on vehicles;

- 68/06 – property tax;

- 68/07 – other fees and taxes;

- 68/08 – single tax (under the simplified tax system).

The established list of codes for subaccounts of synthetic account 68 is reflected in the accounting policy of the enterprise. The data is grouped into turnover sheets. The sum of the final results for analytical accounts should converge with the data of synthetic accounting of account 68.

Application of debit and credit in practice

Accounting statements are always balanced. Any purchase or transaction entails the simultaneous appearance of a debit and a credit in the accounts. The accounting department usually writes off funds coming into the company. As assets grow, debit accounts increase; when purchasing furniture and inventory, assets also increase.

- The purchase of new equipment for a business increases the debit account (assets), but also increases the credit, showing the amount of funds in the current account.

- A bank loan for the development of an organization is recorded as a debit account, and the amount of debt to the financial institution goes to the credit account. This procedure is called the double counting system.

Thus, accounts decrease and increase when comparing debits and credits. Money constantly moves across accounts, and debits and credits show the redistribution of funds as they are received and spent in the enterprise.

Revenue accounting, or it's not that simple

According to tax accounting rules, sales revenue does not include:

- amount differences;

- interest on commercial loans;

- interest (discount) on bills.

Let's look at these types of income in more detail.

Amount differences

You can set the selling price for goods (work, services) in conventional units or foreign currency (for example, US dollars, euros). The price set in conventional units must be converted into rubles.

If from the date of sale of goods (work, services) to the date of payment, the foreign currency exchange rate has increased, after such recalculation the buyer’s ruble debt will increase. The amount he will have to pay extra is called the positive amount difference.

If from the date of sale of goods (work, services) to the buyer to the date of payment, the foreign currency exchange rate has decreased, then the buyer’s debt will decrease. The amount by which the debt will be reduced is called the negative amount difference.

In accounting, positive amount differences increase revenue from the sale of goods (works, services), and negative ones reduce it. In tax accounting, positive amount differences are taken into account as non-operating income, and negative differences as non-operating expenses. They do not affect sales revenue.

Please note: if a company accounts for revenue using the cash method, then the amount differences are not taken into account when taxing profits.

Example

Passive LLC sells goods. Under the purchase and sale agreement, the cost of goods is expressed in US dollars and amounts to 1000 US dollars (excluding VAT). “Liability” takes into account revenue when calculating income tax on an accrual basis.

Situation 1

The official US dollar exchange rate was:

– on the date of shipment of goods to the buyer – 30 rubles/USD;

– on the date of payment for goods – 33 rubles/USD.

The Passiv accountant made notes:

Debit 62 Credit 90-1

– 30,000 rub. (30 rubles/USD x 1000 USD) – the buyer’s debt is reflected;

Debit 51 Credit 62

– 33,000 rub. (33 rubles/USD x 1000 USD) – money received from the buyer;

Debit 62 Credit 90-1

– 3000 rub. ((33 rub./USD – 30 rub./USD) xx 1000 USD) – a positive amount difference is reflected.

The company received 33,000 rubles from the buyer, including:

– 30,000 rub. – price of goods;

– 3000 rub. – positive total difference.

Revenue from the sale of goods is reflected as follows:

– in accounting – in the amount of 33,000 rubles;

– in tax accounting – in the amount of 30,000 rubles. The positive amount difference (3,000 rubles) is taken into account as non-operating income.

Situation 2

The official dollar exchange rate was:

– on the date of shipment of goods to the buyer – 33 rubles/USD;

– on the date of payment for goods – 30 rubles/USD.

The Passiv accountant made notes:

DEBIT 62 Credit 90-1

– 33,000 rub. (33 rubles/USD x 1000 USD) – the buyer’s debt is reflected;

DEBIT 51 Credit 62

– 30,000 rub. (30 rubles/USD x 1000 USD) – money received from the buyer;

DEBIT 62 Credit 90-1

– 3000 rub. ((33 rub./USD – 30 rub./USD) x 1000 USD) – the buyer’s debt is reduced by a negative amount difference.

The company received 30,000 rubles from the buyer. At the same time, the negative amount difference amounted to 3,000 rubles.

Revenue from the sale of goods is reflected as follows:

– in accounting – in the amount of 30,000 rubles;

– in tax accounting – in the amount of 33,000 rubles. The negative amount difference (RUB 3,000) is taken into account as a non-operating expense.

Interest on commercial loans and bills

In the contract for the sale and purchase of goods (works, services), your company may provide that the buyer is provided with a deferred or installment payment plan (in other words, the buyer is provided with a commercial loan). Typically, under such contract conditions, the buyer must pay both the cost of goods (work, services) and interest for deferring their payment.

In accounting, interest on deferral increases sales revenue. In tax accounting, interest received on any debt obligations (including commercial loans) is taken into account as non-operating income. They do not affect revenue from the sale of goods (works, services). The procedure for reflecting interest on loans in tax accounting does not depend on the method of determining revenue (accrual method or cash method).

Example

CJSC Aktiv sells goods, the price of which, according to the contract, is 12,000 rubles. (without VAT). According to the terms of the contract, the buyer must pay for the goods 60 days after receiving them. In this case, the buyer must pay 0.1% of the cost of goods for each day of deferred payment.

The total amount of interest for deferred payment for goods will be:

12,000 rub. x 0.1% x 60 days = 720 rub.

The Aktiva accountant must make the following entries:

Debit 62 Credit 90-1

– 12,000 rub. – revenue from the sale of goods is reflected;

Debit 62 Credit 90-1

– 720 rub. – additional revenue from the sale of goods has been accrued in the amount of interest;

Debit 51 Credit 62

– 12,720 rub. (12,000 + 720) – money has been received from the buyer.

Revenue from the sale of goods is reflected as follows:

– in accounting – in the amount of 12,720 rubles;

– in tax accounting – in the amount of 12,000 rubles. Interest on a commercial loan (720 rubles) is taken into account as non-operating income.

Interest (discount) on commercial bills issued in payment for goods (work, services) is reflected in a similar manner.

Example

CJSC Aktiv sells goods whose price is 25,000 rubles. (without VAT). In payment for the goods, the buyer issued his own promissory note to Aktiv. The nominal value of the bill is 30,000 rubles.

The Aktiva accountant must make the following entries:

Debit 62 subaccount “Settlements with customers” Credit 90-1

– 25,000 rub. – revenue from the sale of goods is reflected;

Debit 62 subaccount “Settlements with customers” Credit 90-1

– 5000 rub. (30,000 – 25,000) – additional revenue from the sale of goods was accrued by the amount of the discount on the bill;

Debit 62 subaccount “Bills received” Credit 62 subaccount “Settlements with customers”

– 30,000 rub. – the bill received from the buyer is taken into account;

Debit 51 Credit 62 subaccount “Bills received”

– 30,000 rub. – money was received from the buyer to repay the bill.

Revenue from the sale of goods is reflected as follows:

– in accounting – in the amount of 30,000 rubles;

– in tax accounting – in the amount of 25,000 rubles. The discount on the bill (5,000 rubles) is taken into account as non-operating income.

Recalculation of revenue at market prices

In general, revenue from the sale of goods (work, services) is calculated based on the prices established in the agreement with the buyer (customer). It is believed that these prices correspond to market prices. However, in some cases, the tax office has the right to check whether the prices established in the contract really correspond to market prices.

Tax authorities can do this in the following cases (Article 40 of the Tax Code):

- the company transfers goods (work, services) under a commodity exchange (barter) agreement;

- the buyer and seller are considered interdependent persons;

- the company sells goods (works, services) under a foreign trade transaction;

- for a short period of time, the transaction price differs from other transactions with the same goods (works, services) by more than 20 percent.

If, as a result of such an audit, it is determined that the price established by the contract deviates from the market price by more than 20 percent, the tax authorities are given the right to recalculate the proceeds (and therefore charge income tax) based on the market price. Therefore, in these situations, revenue is reflected in tax accounting based on the market price of goods (work, services) sold.

If the accountant does not do this himself, then the tax authorities will accrue additional revenue during a documentary audit. Then, in addition to income tax, the company will also have to pay penalties for late payment.

Vladimir MESHCHERYAKOV “Annual Report – 2004” (selected)

Stay up to date with the latest changes in accounting and taxation! Subscribe to Our news in Yandex Zen!

Subscribe