What regulatory document regulates the mechanism for submitting 6-NDFL during reorganization

A document that describes in detail the algorithm of actions of a tax agent when submitting 6-NDFL in the conditions of reorganization does not currently exist.

However, this does not mean that there is no regulatory regulation on this issue, and companies undergoing reorganization can act at their own discretion. The process of submitting 6-NDFL in such a situation is regulated by the following regulations:

- Tax Code of the Russian Federation (Articles 50, 55, 230).

- The procedure for filling out 6-personal income tax, approved by order of the Federal Tax Service of Russia dated October 14, 2015 No. ММВ-7-11/ [email protected] , taking into account changes made by order of the Federal Tax Service of Russia dated January 17, 2018 No. ММВ-7-11/ [email protected]

In addition, the “tax” aspects of the reorganization are based on “civil” ones - clause 4 of Art. 57 of the Civil Code of the Russian Federation, which outlines the key rules of reorganization:

- the company is considered reorganized (except for cases of merger) from the moment of state registration of the companies created during the reorganization;

- the merged company is considered reorganized from the moment information about its liquidation is reflected in the Unified State Register of Legal Entities.

This article of the Civil Code of the Russian Federation defines an important aspect for tax reporting - the date from which responsibility for the preparation and transmission of reporting to tax authorities passes to the newly formed person after the reorganization.

The second important nuance for tax reporting, which includes 6-NDFL, is determining the duration of the last tax period for the reorganized company for which it must report. The algorithm described in paragraph 2 of Art. applies here. 55 of the Tax Code of the Russian Federation: the last tax period for a reorganized company is the period of time from the beginning of the current year to the date of reorganization.

Liquidation of a legal entity

[reklama2]

Liquidation of a legal entity is a method of terminating its activities in the absence of universal succession in its rights and obligations (only partial succession is possible - certain rights of the terminated legal entity are transferred to its creditors)

Types of liquidation of a legal entity

There are 2 liquidation procedures:

- Voluntary – carried out by decision of the founders or an authorized body of a legal entity.

- Compulsory - occurs in accordance with a court decision.

Voluntary liquidation of a legal entity

- The founders or body must report their decision on liquidation to the authorized state body in order to make an appropriate entry in the state register of legal entities. The founders or the body for the liquidation of a legal entity appoint a liquidation commission and establish the procedure and timing of liquidation.

- The main task of the liquidation commission is to identify all debts of a legal entity and carry out settlements with its creditors. To do this, it publishes a notice of liquidation of a legal entity, as well as the procedure and deadlines for submitting claims by its creditors, and also notifies all creditors in writing about the liquidation. Then, after the deadline for submitting claims, an interim liquidation balance sheet is drawn up (it reflects information about the composition of the legal entity’s property, the list of stated claims of creditors and the results of their consideration)

- If a legal entity does not have enough interim balance to satisfy the claims of creditors, then the legal entity’s property is sold at public auction. faces. If there is a shortage of this property, in some cases a claim for satisfaction of the remaining claims may be brought against persons bearing subsidiary liability for the debts of the legal entity. If it is discovered that there are insufficient funds to satisfy the claims of creditors, then liquidation must be carried out in the manner prescribed by bankruptcy legislation.

- Settlements are made with the creditors of the legal entity in order of priority

- Begins after completion of all settlements with creditors. The liquidation commission draws up the final liquidation balance sheet; the remainder of the property is transferred to the founders or participants of the legal entity.

- Liquidation is considered completed from the moment the corresponding entry is made in the state register.

[advertisement3]

Special case (bankruptcy)

Bankruptcy (insolvency) - occurs when a legal entity is unable to fully satisfy the claims of its creditors for monetary obligations. They can only count on partial satisfaction of their demands.

The main feature of liquidation in bankruptcy is the mandatory compliance with the competitive procedure for distributing the property of the liquidated legal entity among creditors.

A person can be declared bankrupt only in court - by decision of an arbitration court.

Forced liquidation of a legal entity

Compulsory liquidation is carried out in accordance with a court decision. The grounds may be, for example, carrying out activities prohibited by law or without a license

How to fill out 6-NDFL during reorganization (liquidation)

6-NDFL during reorganization must be drawn up taking into account the following nuances:

- in the column “Submission period (code)” of the title page, indicate 2 numbers from Appendix 1 to the procedure approved by Order of the Federal Tax Service No. ММВ-7-11/450 - 51, 52, 53 or 90, meaning respectively 1 quarter, half a year, 9 months or year (these codes are used only when registering 6-NDFL in a situation of reorganization or liquidation);

- the data in section 1 is filled in on an accrual basis from the beginning of the year until the date of reorganization;

- section 2 reflects calendar dates and total values for the last reporting period (from the 1st day of the first month of the reporting period to the date of reorganization, but not more than 3 months);

- The data for filling out 6-NDFL must be taken from the tax registers for personal income tax (their maintenance is mandatory).

The material “Sample of filling out a tax register for 6-NDFL” will tell you what the personal income tax register looks like and how it is filled out.

How and when to transfer 6-NDFL to the tax authorities during reorganization

6-NDFL can be received from the reorganized company to the tax authorities in two ways (they are described in the manner approved by the order of the Federal Tax Service No. MMV-7-11/450):

- a representative of a company or individual entrepreneur can bring a paper 6-NDFL to the tax authorities or send it by mail - these methods are possible for companies that have paid income to no more than 25 individuals from the beginning of the year until the moment of reorganization;

- electronically (via TKS using an electronic digital signature) - this method can be used by all tax agents without exception to submit 6-NDFL.

The reorganized company must complete the latest 6-NDFL report for the last tax period - the period of time from the beginning of the year until the day the reorganization is completed. It must also be submitted before the reorganization (closure) is completed. This follows from the letter of the Federal Tax Service of Russia dated March 30, 2016 No. BS-3-11/ [email protected]

If the reorganized company did not have time to submit a report in Form 6-NDFL, then the obligation to submit reports passes to the legal successor (clause 5 of Article 230 of the Tax Code of the Russian Federation).

Package of necessary documents

The main point when carrying out any legal procedure is the preparation of the necessary package of documents. In this case it should include:

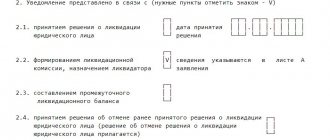

- application to the Federal Tax Service in form No. Р16003 (on exclusion from the Unified State Register of Legal Entities);

- decision to carry out reorganization (with a sole founder), or minutes of the general meeting (drawn up by both the reorganized company and the legal successor);

- affiliation agreement, which specifies the conditions for the procedure;

- deed of transfer.

Even at the preparatory stage, it is necessary to send a notification to the Federal Tax Service about the start of the process (within 3 days). Additionally, it is required to publish an advertisement twice in the “Vestnik GR” in order to inform creditors.

Application to the tax authorities

The application form in form No. Р16003 is available for download on the Federal Tax Service website. The document consists of the following subsections:

- information about the affiliated legal entity;

- information about the legal successor;

- information about publications in the media;

- information about the applicant.

The first two subsections are filled out based on data on companies contained in the Unified State Register of Legal Entities. It indicates the names, details, information about the numbers and dates of entries in the state register. Next, you must indicate the dates of publication of the announcement of the reorganization in the press.

The subsection “information about the applicant” records information about the representative submitting documents to the Federal Tax Service. Here your full name, information about the date and place of birth, details of your identity document, and place of residence are indicated. If a legal entity acts as a representative, its name and details are indicated.

you can here.

Making a decision

Reorganization of a legal entity can begin only after a unanimous decision is made by all founders in favor of this event (Clause 1, Article 57 of the Civil Code of the Russian Federation). This decision is made at an extraordinary meeting of the founders (each of the parties), where the affiliation agreement and other organizational issues are also approved. If there is only one owner, he simply needs to draw up the appropriate document.

The decision must reflect:

- method of reorganization;

- the basis for the procedure (contract details);

- details of both parties;

- responsible person.

For clarity, let’s look at a sample decision of a sole founder.

Sole participant of Aqua LLC

The sole participant of Aqua LLC, represented by director Nikolai Petrovich Pavlov, acting on the basis of the Charter, decided:

- Reorganize Aqua LLC (OGRN, INN, KPP, location) in the form of merger with Soyuz LLC (OGRN, INN, KPP, location).

- Approve the accession agreement No. 1/RO/09 dated July 12, 2017. between Aqua LLC and Soyuz LLC.

- Authorize Aqua LLC to sign and submit documents of affiliation to the tax authorities, as well as make publications in the printed publication “Vestnik GR”.

Director of Aqua LLC N.P. Pavlov

Treaty of accession

The agreement of accession does not act as a constituent document; it only prescribes the procedure for carrying out the reorganization.

The contract stipulates the following points:

- appointment of a person responsible for carrying out the procedure;

- description of the stages of reorganization;

- the size of the future authorized capital of the legal successor;

- timing and scope of succession;

- changes made to the Charter of the legal successor.

document can be found here.

Agreement on merger during reorganization (sample)

As for changing the size of the authorized capital, several options are acceptable:

- Summation of the authorized capital of all participants in the reorganization.

- Maintaining the previous size of the authorized capital of the legal successor with the repurchase of shares of the acquired companies.

- Approval of the new size of the authorized capital and distribution of its shares at the general meeting of all participants.

Whatever method is chosen, it should be reflected in the accession agreement. A sample agreement can be downloaded here.

Order on reorganization

Another important organizational point is drawing up a reorganization order. The order must reflect that from a certain date the employees of the reorganized company will be transferred to the staff of the legal successor. This order must be familiarized with the signature of all employees, because some of them may not agree to move to a new company.

On the reorganization of Aqua LLC

In connection with the reorganization of Aqua LLC in the form of merger with Soyuz LLC,

- All employees of Aqua LLC from September 13, 2017. considered to be working for Soyuz LLC.

- Head of Human Resources Lavrova E.V. add new information to employment contracts and employee work books.

- Secretary Voronina N.A. inform Lavrova E.V. with the text of the order until September 14, 2017.

- I reserve control over the execution of the order.

Reason: certificate of termination of activity dated September 13, 2017.

Director Pavlov N.P.

How to fill out 6-NDFL for a legal successor

The successor company submits the 6-NDFL calculation to the tax office at its location or at the place of registration, if it is the largest taxpayer. When filling out the calculation, the corresponding code is recorded in the column “at location (accounting (code))” of the title page:

- 215 - at the location of the legal successor who is not the largest taxpayer;

- 216 - at the place of registration of the legal successor, who is the largest taxpayer.

The Federal Tax Service, by order dated January 17, 2018 No. ММВ-7-11/ [email protected], updated the 6-NDFL calculation form, which officially comes into force on March 26, 2018.

The updated form can be downloaded here.

Fields have been added to the title page of the form that can only be filled in by legal successors:

- Form of reorganization (liquidation) - indicate the code given in Appendix No. 4 to the procedure for filling out the calculation:

- 1 – transformation;

- 2 – merger;

- 3 – separation;

- 5 – connection;

- 6 – separation with simultaneous addition.

- TIN/KPP of the reorganized organization - the codes of the reorganized company are indicated.

The “tax agent” column indicates the name of the reorganized company or its separate division.

The accuracy and completeness of the data in the calculation is confirmed by the assignee by indicating code 1 in the appropriate cell.

Reorganization of a legal entity

Reorganization is one of the forms of termination of a legal entity (merger)

Reorganization is one of the forms of emergence of a legal entity (spin-off)

Reorganization is one of the forms of termination and emergence of a legal entity (merger, division, transformation)

Forms of reorganization

- Merger of several legal entities

- Merger of a legal entity with another

- Division of a legal entity into several independent legal entities

- Separation of one or more legal entities from a legal entity

- Transformation of a legal entity from one legal form to another

Types of reorganization

- Voluntary – carried out by decision of the founders or an authorized body of a legal entity with the consent of state bodies

- Compulsory - carried out by court decision, for example, in case of a monopoly

The reorganization is formalized using a transfer deed . It must contain provisions on all matters of succession.