Use of bill transactions by enterprises

Recently, modern enterprises are increasingly using bill transactions.

A bill of exchange can act both as a promissory note and as a means of payment. Also, enterprises can use a bill of exchange as an object of sale, in which case the bill of exchange will be one of the types of movable property. Also, increasingly, lenders, when issuing a loan, require the debtor to provide his own bill of exchange as confirmation of the borrowing relationship.

The bill, in turn, can be of two types - interest-bearing or discount:

- An interest-bearing note has a fixed interest rate. It is issued for the purpose of accumulating income.

- A discount bill is interest-free; the discount will be formed in the form of the difference between the amount received by the borrower and the face value of the bill, that is, the amount that he is obliged to return.

Finished works on a similar topic

- Course work Taxation of bills 480 rub.

- Abstract Taxation of bills 270 rub.

- Test work Taxation of bills 240 rub.

Receive completed work or specialist advice on your educational project Find out the cost

Taxation of transactions with bills of exchange (page 1 of 3)

Introduction

Taxes are the main source of revenue generation for the budget of the Russian Federation. Among the wide variety of taxation objects, I would like to highlight transactions with securities. In the economic activities of legal entities, the most common are bills of exchange, which act as a means of payment, a guarantee of payment or as a security. Due to different approaches to the nature of bills of exchange, problems arise in accounting and, as a consequence, in the taxation of transactions with bills of exchange. For correct taxation and accounting of transactions with bills of exchange, it is necessary to be based on the agreement that served as the basis for the issuance or transfer of a bill of exchange. Another thing is that the terms of the transaction are not reflected in the circulation of the bill of exchange, this is precisely the reason and meaning of the abstractness of the bill of exchange. The agreement still remains the main primary document.

Since 1991, enterprises, organizations, institutions and entrepreneurs have again been allowed to supply products (perform work, provide services) on credit, charging interest to buyers (consumers, customers), using promissory notes to formalize such transactions, i.e. provide each other with commercial credit. This problem is covered in the first part of this work.

The second part of the work is devoted to the taxation of individuals. Since the tax base is determined only from the income received, differences in taxation exist depending on the type of securities, therefore, when describing the taxation of individuals, transactions with various securities are considered.

1. Taxation of transactions with bills of exchange applied

in settlements between enterprises for the supply of goods

In the practice of enterprises, there are often cases when payments for shipped goods are carried out by bills of exchange. When making payments between enterprises using bills of exchange, one should be guided by the Federal Law of March 11, 1997. N 48-FZ “On bills of exchange and promissory notes”, the provisions of Articles 142-149 of the Civil Code of the Russian Federation.

A bill of exchange is a written promissory note drawn up in the prescribed form and giving its owner the unconditional right to demand, upon maturity, from the person who issued the bill, payment of the amount specified in it. The person who issued the bill is the drawer; the person who accepted the bill is the holder of the bill. Bills of exchange can be simple or transferable.

A promissory note is a written document containing a simple and unconditional obligation of the drawer (debtor) to pay a certain amount of money at a certain time and in a certain place to the holder of the bill or, on his order, to another person. With a promissory note, the drawer himself undertakes to pay the issued bill. The holder of the bill has the right to receive payment on the bill.

A bill of exchange (draft) is a written document containing an unconditional order from the drawer to the payer to pay a certain amount of money at a certain time and in a certain place to the holder of the bill or, on his order, to another person.

It is necessary to distinguish between two types of bills, the accounting of transactions for which has fundamental differences:

a) Bills of exchange issued directly by the buyer of the products (goods). Such bills of exchange are accounted for by the bill holder (supplier) as the buyer's debt secured by the bill of exchange.

b) All other bills, i.e. bills of exchange of other persons (and not the buyer of products, goods) transferred in payment for goods (products) received. In this case, the accounting records of the bill holder (supplier) at the time of receipt of such a bill reflect the repayment of receivables for the delivered products, i.e. there is no debt owed by the buyer of the products. Therefore, the bill holder (supplier) accounts for such bills in the “Short-term financial investments” account.

1.1. Taxation of the organization-drawer of the bill

The drawer organization, instead of paying for the received inventory (work, services), issues a bill with the obligation to pay it after a certain period of time.

When reflecting in accounting bills of exchange received by an enterprise as a means of payment for the supply of goods, it is necessary to be guided by the letter of the Ministry of Finance of the Russian Federation dated October 31, 1994 N 142 “On the procedure for reflecting in accounting and reporting transactions with bills of exchange used in settlements between enterprises for the supply of goods and work performed and provided with" clause 2 of the Regulations on the composition of costs, approved by the Decree of the Government of the Russian Federation of 05.08.92. N 552 (as amended and supplemented), income paid to the holder of a bill as “interest for deferred payment (commercial loan)” is subject to attribution to the cost of products (works, services) and is fully taken into account for tax purposes (not limited by the marginal rates established by law , including the discount rate of the Central Bank of Russia).

Often, payment of a bill of exchange with “live” money does not occur at all, and the bill of exchange is repaid by offsetting mutual claims upon shipment (fulfillment) by the organization-bill-issuer of products (works, services) of the organization that is the holder of the bills issued by the organization-issuer of the bill.

For the drawer (buyer), an important question is the moment of assigning value added tax on received material assets to settlements with the budget (in the debit of account 68).

When the buyer uses his own bill of exchange in payments for the supply of goods, VAT is considered to be actually paid to the supplier at the time of repayment of the bill. In this regard, the drawer (buyer) has the right to attribute VAT to settlements with the budget only upon payment of his own bill. In this case, the fact of transferring one’s own bill of exchange to the supplier cannot be considered as payment for the goods (work, services) supplied. This is due to the fact that in the analyzed case, the debt of the drawer (buyer) for the goods supplied remains until the bill is paid.

1.2. Taxation of the bill holder organization

The organization-bill holder records the bills received on account of the supply of goods, products (work performed, services rendered) in the debit of account 62 “Settlements with buyers and customers”, subaccount “Bills received” in correspondence with the credit of account 46 “Sales of products (work, profit and losses”, subaccount “Income on bills”.

Income from bills of exchange (interest or positive difference) is included in non-operating income taken into account for tax purposes. In accordance with Instruction of the State Tax Service of the Russian Federation dated August 10, 1995 No. 37 “On the procedure for calculating and paying income tax of enterprises and organizations to the budget,” these incomes for tax purposes are accepted in the amounts taken into account when determining financial results according to accounting rules, i.e. according to accrual, regardless of their actual receipt (Appendix No. 11 to the instructions).

It should be taken into account that in accordance with sub. “g”, Article 5 of the Law of the Russian Federation “On Value Added Tax”, income received from the circulation of securities (including bills), both in the form of interest and in the form of a discount, is exempt from VAT.

If the organization holder of the bill, for tax purposes, determines the proceeds from the sale “on payment”, then after receiving funds under the bill, organization B has obligations to calculate taxes, the necessary indicator of which is revenue (VAT, tax on highway users, etc.). In addition, organization B is obliged to determine the financial result from the sale of products (works, services).

If the bill holder organization, for tax purposes, determines the proceeds from sales “by shipment”, then the proceeds (and all relevant taxes) arise from the bill holder organization after shipment of the products and presentation of settlement documents to the buyer, regardless of the receipt of funds to the account of the bill holder organization or receipt of the bill in payment for goods.

The bill holder organization can, without waiting for the bill to be paid, transfer (sell) the bill to another organization, for which purpose a record is made about the new owner of the bill on the back of the bill, which is called an endorsement. Endorsed bills of exchange, after their transfer, are accounted for by the endorsing organizations in off-balance sheet account 009 “Securities for obligations and payments issued” until the expiration of the deadline for filing claims on the said bills in accordance with the established procedure, receiving notice of their payment, or their payment by the endorsing organization.

Reflection in the accounting records of the bill holder of transactions on the early transfer (sale) of bills is similar to the reflection of transactions on the redemption of bills.

If, upon early transfer (sale) of a bill of exchange, the amount of money or other funds actually received by the bill holder organization turns out to be less than what is due to the bill holder (supplier) for the shipped products (goods), then this difference is repaid at the expense of the bill holder’s own funds.

When transferring a bill of exchange to a third party to pay off accounts payable for received material assets, the holder of the bill of exchange, who determines the proceeds for tax purposes based on “payment”, at the time of transfer of the bill of exchange must reflect for tax purposes the sale of products for which he actually received the bill of exchange from the buyer, and calculate all necessary taxes from it. This is due to the fact that in the situation under consideration there will be no receipt of funds at all to pay for the bill, and therefore for the shipped products.

Features of accounting for your own bill

Accounting for transactions related to a bill of exchange is one of the most complex and controversial from a tax point of view. For the purpose of correct accounting, it is necessary to correctly use a fairly large volume of articles of the Tax Code.

Note 1

Regardless of the type of bill, the participants in the relationship will have income and expenses in the form of interest, which must be reflected in tax accounting. The discount on the own bill will be considered non-operating income or expense and will be distributed evenly. The amount of income or expense in the form of interest on debts is taken into account based on the profitability of the obligation and its duration in the reporting period as of the date of recognition of income/expenses. The discount will be recognized as received and included in expenses/income at the end of the relevant reporting periods, regardless of the date from which interest is accrued.

Looking for ideas for study work on this subject? Ask a question to the teacher and get an answer in 15 minutes! Ask a Question

How to get tax savings when using bills of exchange in calculations

Recently, most experts characterize any financial schemes using their own bills of exchange or bills of exchange of third parties as transactions with a high tax risk. Since inspectors believe that the use of such forms of payment is often associated with tax evasion. At the same time, a more convenient and reliable financial instrument simply does not exist.

According to its legal nature, a bill of exchange can be used both as an independent object of purchase and sale, and as a way to attract borrowed funds, and as a means of payment. Using a bill of exchange as a means of payment provides companies with the opportunity to increase their turnover, obtain the necessary raw materials from suppliers, and expand the circle of buyers. Only by performing these direct functions can a bill of exchange simultaneously bring some tax savings to the company.

The settlement function of bills of exchange accompanies the tax savings of the supplier

The settlement function of a bill of exchange is used for tax optimization, mainly when the tax base is calculated on a cash basis. For example, for companies using the simplified tax system. Since when using the cash method, income is recognized on the date of receipt of funds or when repaying debt in another way (clause 2 of Article 273 of the Tax Code of the Russian Federation). Consequently, a company can save a single tax (income tax) by receiving the buyer’s own bill of exchange as payment for goods, works, and services sold. Revenue from sales from a cash basis supplier arises on the date the bill is repaid by the buyer or on the date it is transferred to a third party.

For suppliers operating on an accrual basis, receiving a bill of exchange in payment does not entail any tax consequences. The tax base for income tax and VAT does not depend on payment (clause 1 of Article 249, clause 1 of Article 248, clause 3 of Article 271 of the Tax Code of the Russian Federation). However, such companies can also receive tax savings from settlements with bills of exchange.

The fact is that the supplier can take into account the face value of bills of exchange from third parties when forming a reserve for doubtful debts (Article 266 of the Tax Code of the Russian Federation). Since the transfer of a bill of exchange does not lead to receipt of actual payment for goods sold (resolution of the Federal Arbitration Court of the West Siberian District dated May 4, 2012 No. A45-13579/2011). Until the bills are repaid by the drawer or transferred to third parties.

From the analysis of the provisions of Article 815 of the Civil Code of the Russian Federation, it follows that the bill certifies the obligations under the loan agreement. It turns out that the loan is related to the sale. Therefore, the company has the right to create a reserve for debt in payment of which a third party bill of exchange was received. Moreover, bills of exchange are not mentioned in the list of collateral that does not allow the formation of a reserve for doubtful debts (clause 1 of Article 266 of the Tax Code of the Russian Federation).

It is also beneficial for the buyer to pay with bills of exchange

A buyer who has transferred a third party bill of exchange as an advance payment to the supplier may accept the advance VAT as a deduction. This approach is shared by arbitration courts. For example, in the resolution of the Federal Arbitration Court of the North-Western District dated January 19, 2012 No. A05-5313/2011, the company transferred promissory notes to the seller for future deliveries of goods. The organization deducted tax from the amount of the prepayment.

Of course, the tax authorities considered that the company had no right to a deduction. Since she does not have documents confirming the actual transfer of the advance payment to the supplier (clause 9 of Article 172 of the Tax Code of the Russian Federation). According to the inspectors, such documents can only be payment orders. However, the judges noted that the parties to the transaction have the right to independently determine the form and method of mutual settlements. In particular, they may provide in the contract for both payment in money and the transfer of a bill of exchange or another form of payment.

Thus, the arbitrators came to the conclusion that the controllers’ requirement to submit a payment order for the amount of the advance payment unreasonably infringes on the rights of the taxpayer who uses other means of settlement with counterparties. As the Federal Arbitration Court of the Ural District indicated, the main thing is to stipulate in the supply agreement that advance payment can be made by bill of exchange (resolution dated September 14, 2011 No. F09-5136/11). Indeed, within the meaning of paragraph 9 of Article 172 of the Tax Code of the Russian Federation, the payment document only confirms the fact of prepayment. When transferring a bill of exchange, such confirmation is the act of acceptance and transfer of the security.

In addition, the buyer can transfer his own bill of exchange as an advance. True, in this case, in order to reduce tax risks, it is advisable to draw up an additional agreement to the supply agreement, which will indicate that prepayment can be made by the buyer’s own bill of exchange. This tax saving method will allow you to receive a VAT deduction without diverting funds from the company’s turnover.

Paying dividends in bills will allow you to defer the payment of personal income tax

Payment of dividends using bills of exchange from third parties will allow deferring the payment of personal income tax for a period acceptable to the founder. Because if the recipient of the bill is an individual, then at the time the bill is received, he does not have any income. After all, a company that acts as a payer of dividends does not have the opportunity to withhold personal income tax, as prescribed by paragraph 3 of Article 214 of the Tax Code of the Russian Federation. The bill in this case is considered not as property, but as a debt security. Therefore it is not income in kind.

In addition, the Presidium of the Supreme Arbitration Court of the Russian Federation indicated back in 2000 that upon receipt of a bill of exchange, income subject to personal income tax arises for an individual only at the time of actual receipt of funds under the bill of exchange (Resolution No. 440/99 dated April 11, 2000). The Federal Tax Service of Russia also believes that until an individual exercises the right to claim under a bill of exchange, this person does not have actual income either in cash or in kind (letter dated April 26, 2006 No. 04-2-02/ [email protected] ).

This approach is also shared by the courts (for example, Resolution of the Federal Arbitration Court of the Volga District dated September 14, 2012 No. A12-22935/2011). However, the Russian Ministry of Finance still believes that the date of recognition of income is the day the bill is transferred to the taxpayer (letter dated December 25, 2012 No. 03-04-05/4-1435).

When selling a bill of exchange to another individual, the founder must pay personal income tax at a rate of 13 percent. Of course, if he declares income. The final holder of the bill also independently pays tax, but only on the amount of the discount or interest (letter of the Ministry of Finance of Russia dated March 22, 2010 No. 03-04-05/2-118).

If the founder has the status of an individual entrepreneur and conducts business activities, then he may not present the bill for redemption, but use it in settlements as a means of payment. If a simplified individual entrepreneur decides to sell a bill of exchange, he will have to pay tax at a rate of 6 percent. With the object “income minus expenses”, both income from the sale of a security and expenses for its acquisition will arise. Consequently, the tax base for the single tax will be zero.

Meanwhile, transferring your own promissory note to the founder in payment of dividends is quite risky. Since tax authorities may claim that at the time of its transfer dividends were paid. Consequently, then it was necessary to keep the PFDL. Moreover, judges may agree with this approach (resolution of the Federal Arbitration Court of the Volga District dated September 21, 2009 No. A55-20239/2008).

Although paying dividends using their own bills makes no economic sense, some companies allow such behavior. Motivating this by the presence of balance sheet profit, which is not supported by the availability of free cash.

A promissory note will help you receive money tax-free

With the help of a promissory note, a company can receive money from a third party or dependent organization without paying income tax. That is, to receive funds not from the founder or from a subsidiary (subclause 11, clause 1, article 251 of the Tax Code of the Russian Federation). For example, a company receives a bill of exchange to a third party free of charge from a company that is eligible for the specified benefit. If the presentation of a bill of exchange for payment or its other disposal occurs no earlier than in a year, then the funds received by the company are exempt from income tax.

In addition, the organization can receive its own promissory note from the company entitled to the specified benefit. The organization can then use this bill of exchange in settlements or sell it. The main thing is that the disposal of the bill should occur no earlier than a year after its gratuitous receipt.

According to the Ministry of Finance of Russia, repayment during the year of a bill received from the sole founder is also not income of the company (letters dated 02.15.13 No. 03-03-10/4006, dated 05.05.10 No. 03-03-06/1/313 ). Officials point out that, taking into account the provisions of Articles 128 and 130 of the Civil Code of the Russian Federation, a bill of exchange for profit tax purposes is recognized as property. Therefore, income from the gratuitous receipt of a third party’s bill of exchange from the main founder is not taken into account for tax purposes as income in the form of property received gratuitously (subclause 11, clause 1, article 251 of the Tax Code of the Russian Federation).

In addition, when a bill of exchange is redeemed, the corresponding debt obligation is terminated, and therefore the redemption of a bill of exchange cannot be considered as a transfer of the security to third parties. Consequently, if the bill is repaid within a year from the date of its receipt, income in the form of property received free of charge does not arise. That is, in this situation, the Ministry of Finance also recognizes that this operation with a bill of exchange falls under subclause 11 of clause 1 of Article 251 of the Tax Code of the Russian Federation.

It is noteworthy that if there is a later repayment of the note, the same rules will apply as for the disposal of securities. That is, income will arise that is taken into account in the tax base for profits. Moreover, if the bill was received free of charge, then there is no reason to reduce income for expenses.

In practice, a scheme is often encountered when a group of companies includes several legal entities and an individual entrepreneur, who at the same time is the sole founder of these companies (see diagram). One company provides a loan to another, and in return receives promissory notes from the borrower. The lender then transfers the notes to its sole participant to pay dividends. At the same time, the entrepreneur does not have income from which personal income tax must be withheld at a rate of 9 percent (Resolution of the Presidium of the Supreme Arbitration Court of the Russian Federation dated April 11, 2000 No. 440/99). According to this resolution, the date of inclusion in the entrepreneur’s income of the amounts of proceeds from the sale of goods, works, services paid for by a bill of exchange is determined by the earliest of the following dates: the day of repayment of the bill of exchange or the day of its alienation in any other way.

Tax-free transfer of money within a group of companies

Next, the founder makes a decision to increase the authorized capital of the drawer. Moreover, payment of the contribution to the authorized capital occurs through the transfer of bills. Then the borrower does not have taxable income (subclause 3, clause 1, article 251 of the Tax Code of the Russian Federation). You can also make bills as a contribution to the property of the borrowing company (Article 23 of Federal Law No. 14FZ dated 02/08/98), then the company does not generate income due to subparagraph 11 of paragraph 1 of Article 251 of the Tax Code of the Russian Federation.

As a result of any of these operations, the borrower will have his own bills of exchange at his disposal, which can either be repaid by order of the manager or put back into circulation. In any case, the drawer will not have to return the funds to the lender. And at the same time he will not have taxable income.

The cost of bills of a liquidated issuer reduces profit

The company may obtain tax savings by expensing the value of the liquidated issuer's notes. However, the Ministry of Finance believes that if the drawer was liquidated, then the resulting losses do not reduce taxable profit.

In letter dated 06/03/11 No. 03-03-06/3/3, officials explain that the company does not have the right to take into account losses associated with the acquisition of securities on the basis of subparagraph 2 of paragraph 2 of Article 265 of the Tax Code of the Russian Federation. Since Article 280 of the Tax Code of the Russian Federation does not provide for the inclusion in expenses of the cost of securities, the debt for which is recognized as bad, if the issuer is liquidated.

Paradoxical is the fact that Moscow tax officials express the opposite opinion (letter from the Federal Tax Service for Moscow dated May 19, 2011 No. 16-03/ [email protected] ). Indicating that the company can take into account a loss in the form of expenses for the acquisition of a security on the basis of subparagraph 2 of paragraph 2 of Article 265 of the Tax Code of the Russian Federation upon the liquidation of the issuer as a bad debt. In addition, in Resolution No. 15706/07 dated April 15, 2008, the Presidium of the Supreme Arbitration Court of the Russian Federation indicated that a bill of exchange is a way for the drawer to formalize his debt to repay borrowed funds. Such judgments led senior judges to the opinion that such a debt can be considered hopeless due to the liquidation of the debtor (clause 2 of Article 265 and clause 2 of Article 266 of the Tax Code of the Russian Federation).

Most likely, the company will have to defend the possibility of recognizing losses from writing off bills of exchange of a liquidated debtor in court. Especially if the controllers manage to prove that the organization deliberately linked its activities with dishonest contractors. Indeed, companies often artificially create such losses for themselves in order to save on income taxes.

Selling your own bill does not form a tax base

A company selling its own bills may not pay income tax. Since the funds received by the seller are essentially borrowed and are not subject to accounting as part of the issuer’s income on the basis of subparagraph 10 of paragraph 1 of Article 251 of the Tax Code of the Russian Federation. Let us remind you that, according to this norm, funds received under loan agreements are not subject to accounting when determining the tax base.

In one of the similar disputes, the organization sold its own promissory notes under a purchase and sale agreement. The funds received were not taken into account when determining the tax base for profits. Of course, the controllers considered this to be unlawful and assessed additional income taxes on the company. Having analyzed the purchase and sale agreements, the inspection came to the conclusion that when these transactions were carried out, the bill of exchange acted as a commodity. Therefore, the taxpayer should have taken into account the funds received from the sale of bills of exchange as income (Articles 280, 329 of the Tax Code of the Russian Federation).

However, the Presidium of the Supreme Arbitration Court of the Russian Federation sided with the company (resolution No. 9995/09 dated November 24, 2009). At the same time, pointing out that the sale of own bills is not the sale of securities. Because by selling them, the organization actually attracts borrowed funds. The sale of your own bill of exchange under a purchase and sale agreement does not change the content of the loan transaction. Therefore, funds received as a result of the placement of bills of exchange are not taken into account when determining the income tax base.

Similar conclusions are contained in the letter of the Ministry of Finance of Russia dated March 21, 2006 No. 03-03-04/1/268. This approach is also shared by arbitration courts (resolutions of the Federal Arbitration Court of the Moscow District dated April 29, 2009 No. KA-A41/2434-09, dated October 29, 2008 No. KA-A40/10239-08).

Simplifyers can speed up the recognition of expenses for the purchase of goods

By issuing his own bill of exchange, a simplified buyer can quickly recognize the cost of purchased goods, works, and services for which he paid with his own bill of exchange as expenses (Clause 2 of Article 346.17 of the Tax Code of the Russian Federation). To do this, it is necessary to novate (Article 414 of the Civil Code of the Russian Federation) the obligation under the bill of exchange for a loan. The legality of this approach is confirmed by arbitration practice (for example, resolution of the Federal Arbitration Court of the Central District dated March 27, 2012 No. A14-1209/2010). Thus, in one of these disputes, the Federal Arbitration Court of the Volga District confirmed that obligations under a bill of exchange purchase and sale agreement can be replaced by a loan obligation (resolution dated January 23, 2013 No. A65-15293/2011).

In practice, a simplified seller may not recognize income upon receipt of a friendly buyer’s own bill of exchange in payment for goods sold. To do this, it is necessary to obtain a loan secured by this bill without making an endorsement. In this case, the seller has the right not to recognize income from the sale of goods, works, services, and property rights. In addition, the seller receives additional working capital at his disposal.

At the same time, there are situations when judges recognize innovation as an illegal operation. For example, the Federal Arbitration Court of the North Caucasus District, in its resolution dated November 13, 2012 No. A22-1685/2011, came to the conclusion that the buyer’s obligation under the purchase and sale agreement was not terminated by novation. Since in the disputed loan agreement the parties did not provide that the buyer’s obligations in connection with the conclusion of the contract are terminated.

The judges indicated that the essence of novation is the termination and replacement of the original obligation that previously existed between the parties with another obligation. In this case, innovation occurs only when the actions of the parties are aimed at ensuring that it is novated. If the parties intend to make a novation, then they must document this fact.

We also note that, according to Article 414 of the Civil Code of the Russian Federation, as a result of novation, the original obligation is terminated and a new one arises, providing for a different subject or method of fulfillment. At the same time, the Civil Code does not specify what is meant by another subject and method of execution.

The opinion of the Russian Ministry of Finance, set out in letter No. 03-03-06/2/76 dated July 10, 2008, allows us to take a broader look at this issue. From this clarification it follows that it is possible to nominate a bill of exchange by replacing a previously issued promissory note with two new bills of exchange. This situation occurs when the buyer of goods cannot repay the amount of his debt on time and essentially restructures it.

In this case, according to officials, interest on the original bill should accrue until the novation agreement is signed. And after this point, interest must be accrued on two new bills. The person who issued the original bill accounts for interest on it as an expense, based on the initial yield and the length of time the borrowed funds were used.

In this case, accounting for expenses in the form of interest on new bills is carried out based on the new yield established when issuing such debt obligations and the period of their circulation. And the lender will count interest on the original note and new notes in income.

This situation is possible when the buyer is an intermediary and himself receives bills of exchange from third parties in payment for the delivered goods. Then the intermediary can agree with the seller to exchange bills. That is, the buyer’s own bill of exchange held by the seller is exchanged for a bill of exchange of a third party held by the buyer. In this case, the difference in the denominations of the bills can be issued as an advance payment against upcoming deliveries of goods. Or issue the seller’s own bill of exchange, which the company can either sell or use to pay for subsequent deliveries. It turns out that the buyer will be able to recognize the expense, since as a result of the exchange, the obligation under his own bill was terminated.

Accounting for early repayment of bills

In case of early repayment of the promissory note, income will be recognized as received and included in income on the date of repayment of the debt obligation. The remaining difference will be taken into account by the holder of the bill at a time between the entire amount of the discount and that already accrued as income in tax accounting. The borrower who paid for the security ahead of schedule similarly accrues additional expenses in the form of the difference between the actually paid discount amount for early repayment and the already calculated amount in tax accounting.

Note 2

If the bill is repaid before the end of its validity period, then income is accrued in the same way, since the discount is distributed evenly over periods and will not be fully taken into account by the time the bill expires.

When calculating expenses, it is important to remember that they are standardized. There are two ways to normalize interest expenses. The first method is rationing based on the refinancing rate of the Central Bank. The procedure is established by Article 269 of the Tax Code of the Russian Federation.

A comparison of data with other loans can also be used - used in the case where the company has other debt obligations on similar terms. The maximum amount of interest by which taxable profit can be reduced will be determined based on the average level of interest on similar obligations. When choosing this method, it is necessary to have a clear procedure for determining comparable loans in the accounting policies of the organization. Loans are considered comparable if the following conditions are met: the same currency and term, comparable amounts and similar collateral.

Income tax: Payments by bills of exchange of third parties: taxation features

Income tax: Payments by bills of exchange of third parties: taxation features

Payments for the supply of goods (performance of work, provision of services) can be made not only in money. Enterprises often use bills of exchange as a means of payment. However, bill circulation raises many questions among its participants related to the registration of these transactions in accounting and taxation. We will try to answer some of them in this article.

Definition and mandatory details of third party bills of exchange

In paragraph 1 of Art. 142 Civil Code of the Russian Federation

a definition of a security is given as a document having legal force.

The main features of a security are:

- This is a document certifying property rights, the exercise or transfer of which is possible only upon presentation. Property rights may include requirements for payment of a certain amount of money, transfer of property, as well as other requirements in the field of civil law relations;

- this document must be executed in compliance with the requirements for its form and contain the required details;

- securities are classified as objects of civil rights ( Article 128 of the Civil Code of the Russian Federation

) and are movable property (

Article 130 of the Civil Code of the Russian Federation

).

With regard to a third party bill of exchange, the following can be said: this is a bill of exchange, the drawer of which is neither the organization that issued it nor the seller of the bill.

Third party bills of exchange used in settlements between the supplier and the buyer can be of two types:

- previously received by the buyer from his counterparties as payment for goods shipped to him (work performed for him, services provided to him);

- previously acquired by the buyer for money when making financial investments (financial bills).

Bill circulation in the Russian Federation is regulated by Federal Law No. 48-FZ

[1] and

the Regulations on bills of exchange and promissory notes

[2]. It should be noted that bills of exchange are practically not circulated on the territory of the Russian Federation, therefore, in the future, the word “bill” will mean only a promissory note.

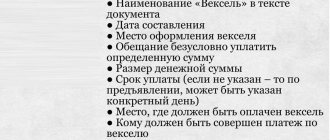

To recognize a document as a promissory note, clause 75 of the said provision establishes the following mandatory details:

- name "bill";

- a simple and unconditional promise to pay a certain amount;

- indication of the payment term;

- indication of the place where payment should be made;

- the name of the person to whom or on whose order the payment should be made;

- indication of the date and place of drawing up the bill of exchange;

- the signature of the person issuing the bill (the drawer).

A document that does not contain any of the indicated designations does not have the force of a promissory note ( clause 2 of article 144 of the Civil Code of the Russian Federation, clause 76 of the Regulations on bills of exchange and promissory notes

) except in the following cases:

- if the bill does not indicate a payment term, then it is payable upon presentation;

- if the place of payment is not directly indicated in the bill, then it should be presented at the place of issue;

- If a promissory note does not indicate the place of its preparation, then it is recognized as signed in the place indicated next to the name of the drawer.

I would like to draw your attention to such a mandatory detail of the bill as “Payment Date”. Clause 33 of the Regulations on bills of exchange and promissory notes

states that it can be assigned in one of the following ways:

- upon presentation;

- in such and such a time from presentation;

- in so much time from compilation;

- on a certain day.

A note due date that is worded in a manner different from the options listed above, or contains consecutive due dates for payment, may result in the security being invalidated.

Payments with bills of exchange from third parties: reflection of transactions in accounting

Accounting for bills of exchange of third parties is carried out in accordance with PBU 19/02

[3] and

the Instructions for the Application of the Chart of Accounts for Accounting Financial and Economic Activities of Organizations

[4], on the basis of which such securities are classified as financial investments (

clause 3 of PBU 19/02

), are reflected in the same name account 58 “Financial investments” sub-account 2 “Debt securities”.

All business transactions, as is known, must be confirmed by primary accounting documents ( Article 9 of Federal Law No. 129-FZ

[5]). Auditing practice shows that when making bill payments, enterprises often make mistakes related to documenting transactions with securities. A specific example will help you understand what primary documents are needed to complete such operations.

Example 1.

Organization “A” in March 2004, under a purchase and sale agreement, purchased from the bank for 570,000 rubles. financial bill with a nominal value of RUB 590,000. with a payment deadline of “five months from the date of preparation,” which was subsequently transferred as payment for materials purchased from organization “B” in the amount of 590,000 rubles. (including VAT at the rate of 18% - 90,000 rubles).

In the accounting records of organization “A”, business transactions were reflected as follows:

| Contents of operation | Debit | Credit | Amount, rub. |

| Funds transferred as payment for a financial bill | 76 | 51 | 570 000 |

| The bill is accounted for as a financial investment | 58-2 | 76 | 570 000 |

| As of the date of purchase, supplies of materials | |||

| The debt to organization “B” for materials is reflected | 10 | 60 | 500 000 |

| VAT on materials included | 19 | 60 | 90 000 |

| A financial bill was transferred to pay off the debt under the supply agreement | 60 | 91-1 | 590 000 |

| The book value of the bill is written off | 91-2 | 58-1 | 570 000 |

| Submitted for VAT refund on purchased materials (570,000 x 18 / 118) | 68 | 19 | 86 949 |

| A non-deductible amount of VAT has been written off (90,000 – 86,949) | 91-2 | 19 | 3 051 |

The supplier (organization “B”) will reflect the business transaction as follows:

| Contents of operation | Debit | Credit | Amount, rub. |

| Products shipped to buyer | 62-1 | 90-1 | 590 000 |

| Debt to the budget for deferred VAT was accrued on the cost of products sold | 90-3 | 76 | 90 000 |

| Received a third party bill of exchange in payment for products | 58-2 | 62-1 | 590 000 |

| Debt to the budget for deferred VAT is included in tax liabilities | 76 | 68 | 90 000 |

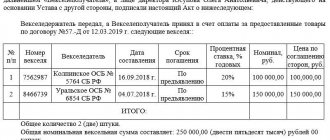

The operation to acquire ownership of a bill of exchange must be carried out on the basis of a securities purchase and sale agreement, which defines the main essential terms of the transferred property (bill) and its price, as well as an act of acceptance and transfer of securities, in which the parties must clearly indicate what kind of bill of exchange is being transferred (form number, all its details, purpose of transfer and the moment of transfer of ownership of this bill).

The operation of transferring a bill of exchange as payment for goods can be formalized in two ways: either as an offset, or as a provision of compensation, as a result of which the contract for the sale of goods from the moment of transfer of the bill of exchange is considered executed.

In the first option, the offset of counter homogeneous claims must be confirmed by acts of reconciliation of settlements and an application for offset.

In the second option, the organization fulfills its obligations to pay for the goods by transferring a bill of exchange. The primary documents in this case will be the compensation agreement and the act of acceptance and transfer of the bill. In the act of acceptance and transfer of the bill of exchange, in addition to the details of the security, it must be indicated in payment for what goods (work, services) the bill of exchange is being transferred; on the basis of which (number, date) agreement the goods and materials (services) were received; the total amount of repayable obligations (may differ from the face value of the bill). The VAT amount should be highlighted separately in the act. If the person accepting the bill acts on the basis of a power of attorney, then its details (date of issue, number) must be indicated in the act.

Typically, in practice, the buyer transfers in payment for goods a bill of exchange whose denomination exceeds the contract price, or a bill of exchange providing for the payment of interest upon its repayment. We will discuss below what tax consequences arise.

Income tax

The procedure for taxation of income from securities, as well as operations on their sale and other disposal, including redemption, is determined by Chapter 25 of the Tax Code of the Russian Federation

. This takes into account the dual nature of securities, which is as follows.

Initially, during the entire period of stay with the organization, the security is considered as a debt obligation, the assessment of which is subject to the rules of clause 6 of Art. 250 Tax Code of the Russian Federation

.

And only at the stage of sale (redemption) of a security, the result of its disposal is assessed in a special manner based on the norms of Art.

280 Tax Code of the Russian Federation .

These features of taxation of securities, which will be discussed in more detail below, fully apply to bills of exchange of third parties.

Procedure for taxation of income on bills of exchange of third parties

If an organization has a third party bill of exchange, tax consequences for accruing interest arise in two cases:

- if the bill is interest-bearing;

- if the bill has a discount.

According to paragraph 3 of Art. 43 Tax Code of the Russian Federation

any pre-declared (established) income, including in the form of a discount (the difference between the face value and the purchase price of the bill or the amount of the transaction for the sale of products (works, services) as a settlement for which the security was received), is recognized as interest.

Therefore, in both the first and second cases, based on paragraphs.

6 tbsp. 250 of the Tax Code of the Russian Federation , the amount of interest is non-operating income for the recipient of the bill and, accordingly, non-operating expenses for the payer (subject to the restrictions listed in

paragraph 2 of paragraph 1 of Article 265 of the Tax Code of the Russian Federation and Article 269 of the Tax Code of the Russian Federation

). It should be noted that the amount of interest on bills can only be established in relation to bills with a payment period of “at sight” and “at such and such a time from sight”. In all other cases, bills must be issued as discount bills. Therefore, as soon as an organization has a non-interest bearing security, it must analyze it for the presence of a discount.

For organizations operating on the accrual basis, in accordance with the requirements of clause 6 of Art. 271

and

art.

328 of the Tax Code of the Russian Federation , interest on securities is recognized as income and included in non-sales at the end of the corresponding reporting period (provided that the term of the bill falls on more than one reporting period). If securities are sold or disposed of (including redeemed) before the expiration of the reporting period, then the income is included in the corresponding income on the date of termination of the agreement (repayment of the debt obligation).

In accounting, based on clause 16 of PBU 9/99

[6], interest is accrued for each expired reporting period only if the bill of exchange received by the seller indicates the interest rate.

If a discount bill is received from the buyer (that is, the interest rate is not specified), then income on such a security is revealed only upon the sale (redemption) of the bill.

Thus, the procedure for accounting for income on bills of exchange of third parties in accounting and tax accounting using the accrual method may be different. When in accounting income on securities is accrued not at the end of the reporting period, but on another date or is not accrued at all in a given reporting period, then for tax purposes it is necessary to specifically calculate its amount attributable to the reporting period. If interest in accounting is accrued at the end of each reporting period, then these amounts are recognized for tax accounting purposes.

Organizations using the cash method recognize income (expense) regardless of the period of the bill at the time of payment or repayment in another way ( clauses 2, 3 of Article 273 of the Tax Code of the Russian Federation

).

It should be noted that organizations must reflect the amount of interest income separately for each debt obligation.

based on certificates from the person responsible for accounting for income and expenses on debt obligations. Let's look at the above using examples.

Example 2.

OJSC Lada pays income tax using the accrual method based on the results of quarterly calculations. On February 17, 2004, the organization acquired an interest-bearing note from a third party at a nominal value of RUB 130,000. with a term “at sight”, providing for payment of 20% per annum of the nominal value at the end of each month. Let’s assume that the organization did not repay the bill in the first quarter.

The bill of exchange received by the organization indicates the interest rate, which gives grounds for accounting purposes to accrue interest for each expired reporting period. Thus, for tax purposes, interest on a bill of exchange is recognized according to accounting data, since they are accrued in the same manner as for tax accounting.

Reflection of the interest calculation operation is presented in the following table:

| Contents of operation | Debit | Credit | Amount, rub. |

| February 17, 2004 The interest-bearing bill was accepted for accounting | 58-2 | 76 | 130 000 |

| The accrual of income on the bill is reflected: February 29, 2004 (RUB 130,000 x 0.20 / 366 days x 12 days) | 76 | 91-1 | 852 |

| March 31, 2004 (RUB 130,000 x 0.20 / 366 days x 31 days) | 76 | 91-1 | 2 202 |

In the income tax return

[7] for the first quarter of 2004, the organization must reflect “accrual” the calculated amount of interest income - 3,054 rubles. (852 + 2,202) due to her during the period of ownership of the bill (from February 17 to March 31, 2004), on line 030 “Non-operating income” of Sheet 02 of the Declaration (on line 030 of Appendix No. 6 to Sheet 02 of the Declaration) in that case , if at the end of the reporting period this security has not been sold by the organization. The costs of purchasing a bill of exchange are taken into account in the tax base only when it is sold.

As already noted, if the acquisition and sale of a bill of exchange were carried out in the same reporting period, then the organization would not have the obligation to reflect “on an accrual basis” the amount of interest income attributable to the period of ownership of the security, since it would be included in the sales price bills.

Example 3.

Organization on January 10, 2004 as payment for shipped products in the amount of 150,000 rubles. received a bill of exchange from a third party, the nominal value of which is RUB 200,000. The maturity date of the bill is April 10, 2004.

In accounting for a discount bill, an organization is not required to accrue interest evenly over the period of its existence. Income will be reflected when the bill is repaid, that is, on April 10, 2004 (of course, provided that the organization does not repay the bill earlier than the specified date).

For tax purposes, a special calculation must be made. Since until the end of the first quarter of 2004 the bill was owned by the organization, then as of the last day of the reporting period the organization must determine the amount of interest income based on the discount amount equal to 50,000 rubles. (200,000 – 150,000), and the time of holding the security from January 10 to March 31, 2004 inclusive, which is 82 days.

The total number of days from the date of purchase of the bill to the date of its repayment is 92 days.

Income in the first quarter will be calculated as follows: (50,000 / 92 x 82) = 44,565 rubles. The organization must include this amount as non-operating income in the tax base when calculating income tax on line 030 of Sheet 02 of the Declaration (on line 030 of Appendix No. 6 to Sheet 02 of the Declaration).

We will consider the reflection of transactions for the sale (repayment) of bills of exchange of third parties in the next section of the article.

Procedure for taxation of transactions with bills of exchange of third parties

The concept of “transactions with securities” includes operations for the sale, other disposal, and redemption of securities. Chapter 25 of the Tax Code of the Russian Federation

a separate procedure has been established for taxation of income and expenses for such transactions, according to which the tax base is formed separately, broken down into two categories of securities: securities traded on the organized securities market and not traded on the organized securities market.

Bills of exchange from third parties do not meet the criteria of clause 3 of Art.

280 of the Tax Code of the Russian Federation , therefore they belong to the second category - securities that are not traded on the organized securities market.

The specifics of determining the tax base for transactions with securities are established by Art. 280 Tax Code of the Russian Federation

, in accordance with

clause 2

of which

income from operations on the sale or other disposal of securities (including redemption) is determined based on the sale price (other disposal), as well as the amount of accumulated interest income paid by the buyer to the taxpayer, and the amount of interest income, paid to the taxpayer by the drawer.

At the same time, the taxpayer’s income from the sale (other disposal) of securities does not include amounts of interest income previously taken into account for tax purposes. Let's illustrate the above with an example.

Example 4.

Let's continue the condition of example 3. Let's assume that the organization presents the bill for redemption on the appointed date (April 10, 2004) and receives 200,000 rubles.

When filling out the Declaration for the six months, the organization will reflect the amount received (200,000 rubles) on line 010 of Sheet 06 “Calculation of the tax base for income tax on transactions with securities not traded on the organized securities market” of the Declaration. Expenses associated with the acquisition and sale of a bill of exchange (150,000 rubles) are reflected on line 030 of Sheet 06. Thus, the tax base on Sheet 06 of the Declaration includes an amount of 50,000 rubles. (lines 040, 070, 120). It (provided that the organization has not carried out other transactions for the sale (disposal) of securities) is transferred to the main Sheet 02 (on lines 180 - 200).

It is necessary to take into account that interest income for the first quarter of 2004 (44,565 rubles) has already been taken into account in the tax base for the corresponding period (line 030 of Sheet 02 of the Declaration for the first quarter of 2004), therefore, in order to avoid double taxation, the organization must reduce the amount of income on repayment of the bill by 44,565 rubles. ( clause 2 of article 280 of the Tax Code of the Russian Federation

) on line 040 of Sheet 02 (line 020 of Appendix No. 7 to Sheet 02).

Peculiarities of accrual of income on bills with a maturity date of “at sight, but not earlier”

Previously, readers' attention was drawn to such a mandatory requisite of a bill as “payment period”. It should be noted that quite often a payment deadline may be indicated on the form of a bill with the following clause: “upon presentation, but not earlier.”

For tax accounting purposes in accordance with paragraphs. "g" section 5.4.1 Methodological recommendations for the application of Chapter 25 “Income Tax”

[8] “

for calculating a discount on bills of exchange with the clause “upon sight, but not earlier”, the estimated maturity of the bill

of exchange , determined in accordance with bill of exchange legislation (365 (366) ) days plus the period from the date of drawing up the bill of exchange to the minimum date of presentation of the bill of exchange for payment)

.”

This procedure applies not only to discount bills, but also to interest-bearing bills. It should be noted that in relation to bills with indicated interest on the form, the provisions of clause 19 of the Resolution of the Plenum of the Supreme Arbitration Court of the Russian Federation and the Plenum of the Supreme Arbitration Court of the Russian Federation No. 33/14

[9], according to which, if there is a direct clause on the start date of interest accrual, the latter is accrued from the date specified in the clause until the date of repayment. In this case, the day from which the term begins to flow is not included in the interest calculation period.

Example 5.

On January 20, 2004, OJSC Lada acquired an interest-bearing note from a third party at a nominal value of RUB 80,000. with a period of “upon presentation, but not earlier than March 20, 2004”, providing for payment of 10% per annum.

For tax accounting purposes, with such a clause on the bill of exchange, its circulation period is extended until March 20, 2005. Since interest is indicated on the form of the bill of exchange, the minimum date

, from which income on the bill will be accrued, is established in accordance with the requirements

of the Resolution of the Plenum of the Supreme Arbitration Court of the Russian Federation.

Thus, if the holder of the bill (the Lada organization) presents the bill for redemption on March 20, 2004, then the drawer has the right to pay him only the face value of the bill (RUB 80,000). If an organization presents a bill of exchange for redemption after the specified date (for example, April 20, 2004), then it will receive the bill amount and interest due to it for 31 days (inclusive from March 21 to April 20), at the rate of 10% per annum:

80,000 + (80,000 rub. x 0.10 / 366 days x 31 days) = 80,678 rub.

Let's assume that an organization charges income tax quarterly. When presenting a bill of exchange for redemption on April 20, 2004, the organization for the first quarter of 2004 in the Declaration of Profit on line 030 “Non-operating income” of Sheet 02 (on line 030 of Appendix 6 to Sheet 02 of the Declaration) must reflect “accrued” interest on existing security in the amount formed from March 21 inclusive to March 31 (the last day of the quarter), that is, for 11 days, namely 80,000 rubles. x 0.1 / 366 days. x 11 days = 240 rub.

On April 20, 2004, the organization repaid the bill. In the Declaration for the first half of 2004, the organization will reflect:

- on line 010 of Sheet 06: income received - 80,678 rubles.

- on line 030 of Sheet 06: expenses associated with the acquisition and sale of the bill - 80,000 rubles.

Thus, the tax base according to Sheet 06 of the Declaration includes the amount of 678 rubles. Provided that the organization has not carried out other transactions for the sale (disposal) of securities, this amount is transferred to the main Sheet 02 (on lines 180 - 200).

It is necessary to take into account that interest income for the first quarter of 2004 (240 rubles) has already been taken into account in the tax base for the corresponding period (line 030 of Sheet 02 of the Declaration for the first quarter of 2004), therefore the organization must reduce the amount of income on repayment of the bill for this amount, reflecting the “withdrawal of interest” on line 040 of Sheet 02 “Non-operating expenses” (line 020 of Appendix No. 7 to Sheet 02 of the Income Tax Declaration).

Example 6.

Organization "Lada" on February 10, 2004, as payment for shipped products in the amount of 236,000 rubles. received a bill of exchange from a third party, the nominal value of which is RUB 300,000. The bill contains the clause “upon sight, but not earlier than March 10, 2004.”

Under such conditions, the maturity date of the bill, as in the previous example, is extended until March 10, 2005.

In this example, we are dealing with a discount bill (discount amount - 64,000 rubles) with the clause “upon sight, but not earlier”, on which no interest is charged

.

Therefore, income in the form of a declared discount must be accrued in a way different from the previous Example 5

(based on the amount of income and the maturity of the bill). The concept of a minimum date from which interest will accrue on the bill amount is applicable only for bills with interest indicated on the bill form.

If there is a clause “upon sight, but not earlier,” the discount bill is considered negotiable within 365 (366) days plus the time from the date of issuance of the bill (in our case, February 10, 2004) to the date specified in the bill (March 10, 2004) . Thus, in our case: 366 + (19 + 10) = 395 days (assuming that the bill was repaid on March 10, 2004). In this case, income on the bill must be accrued from the day following the day the bill is issued,

that is, from February 11, 2004.

According to the example, the organization repaid the bill on March 10, 2004, that is, in the same quarter when the bill was purchased. Since the acquisition and sale of the bill of exchange were carried out in the same reporting period, the organization does not have the obligation to reflect “on accrual basis” the amount of interest income attributable to the period of ownership of the security.

If we change the conditions of the example and assume that the bill was repaid in another quarter (for example, April 25, 2004), then when filling out the Income Tax Return, you must keep the following in mind.

Since until the end of the first quarter of 2004. the bill was owned by the organization, then as of the last day of the reporting period the organization must determine the amount of interest income based on the discount amount equal to 64,000 rubles. (300,000 – 236,000) and the time of holding the security – from February 11 to March 31, 2004 inclusive, which is 50 days.

Income in the first quarter of 2004 was calculated as follows: (64,000 rubles / 395 days x 50 days) = 8,101 rubles. The organization must include this amount as non-operating income in the tax base when calculating income tax on line 030 of Sheet 02 (on line 030 of Appendix No. 6 to Sheet 02) of the Declaration.

When the bill is repaid on April 25, 2004, the organization will receive 300,000 rubles. When filling out the Declaration for the half-year, the organization must reflect the amount received on line 010 of Sheet 06. Expenses associated with the purchase of a bill (236,000 rubles) are reflected on line 030 of Sheet 06. Thus, the tax base on Sheet 06 of the Declaration includes an amount of 64 000 rub. It (provided that the organization has not carried out other transactions for the sale (disposal) of securities) is transferred to the main Sheet 02 (on lines 180 - 200).

It is necessary to take into account that interest income for the first quarter of 2004 (RUB 8,101) has already been taken into account in the tax base for the corresponding period. To avoid double taxation, when repaying a bill, an adjustment to income is made: the income previously reflected in the Declaration must be shown in line 040 of Sheet 02 as part of non-operating expenses.

Determination of the transaction price when paying with bills of exchange of third parties

Before calculating income and expenses on a bill, it is necessary to find out whether the amount received from the payer corresponds to the market value of the bill

.

This requirement is enshrined in paragraph 6 of Art.

280 of the Tax Code of the Russian Federation , according to which for tax purposes the actual price of sale or other disposal of these securities is accepted if at least one of the following conditions is met:

- if the actual price of the corresponding transaction is within the range of prices for a similar (identical, homogeneous) security registered by the organizer of trading on the securities market on the date of the transaction or on the date of the nearest trading before the corresponding transaction was completed at least once during the last 12 months;

- if the deviation of the actual price of the relevant transaction is within 20% upward or downward from the weighted average price of a similar (identical, homogeneous) security either on the date of the transaction or on the date of the closest trading before the relevant transaction at least once during the last 12 months.

Definitions of similar, identical, homogeneous securities are given in the Methodological recommendations for calculating income tax (clause 6.3.1 subsection “Taxation of securities”), as well as in clause 1.2.6 of Bank of Russia Regulation No. 89-P

[10]. Identical (similar) means securities of the same type, having the same basic characteristics (type of security, payment currency, par value, type of declared income, term and conditions of circulation).

It should be noted that it seems unlikely to obtain information on the prices of a similar bill of exchange for which trading was carried out on the stock exchange (unless, of course, the taxpayer is dealing, for example, with bills of Lukoil, Gazprom and similar, information on the selling prices of which is published in special financial publications). In the absence of the necessary information about the market price of a specific bill, it is recommended to compare the amount received with a certain estimated price of the bill

.

The difference between these amounts should not exceed 20% of the estimated price. If the selling price of a bill of exchange deviates from the estimated price by less than 20%

, then for profit tax purposes the selling price of the bill of exchange is accepted.

If the selling price of a bill deviates from the estimated price by more than 20%

, then it cannot be accepted for tax purposes. In such cases, the estimated price of the bill is accepted, and the following is taken into account.

For interest-bearing bills, the settlement price can be determined by adding the amount payable on the bill and the interest on this amount, calculated at the refinancing rate of the Central Bank of the Russian Federation for the period when the bill was held by the organization.

For discount bills, according to the Methodological Recommendations for the Application of Chapter 25 of the Tax Code of the Russian Federation

, it is recommended to use the following formula for calculating the accrued (accumulated) amounts of interest payments:

Rts = (N – K) / T x D + K, where Rts is the estimated price; N – nominal value of the purchased security; K – purchase price of the security; T – number of days from acquisition to maturity of the security; D – the number of days that passed after the acquisition of the security until the sale (other disposal) of the bill.

Please note:

When a debt security is repaid on time, the settlement price is not determined.

Example 7.

Vlada LLC for previously completed work in the amount of RUB 500,000. receives from ZAO Svetlana an interest-free promissory note from a third party with a nominal value of RUB 530,000, which matures in 183 days. Vlada LLC, without waiting for the maturity date, sold the bill after 13 days for 520,000 rubles.

Let's determine the settlement price of the bill using the above formula: Rts = (530,000 rubles - 500,000 rubles) x 13 days. / 183 days + 500,000 rubles = 502,131 rubles. Let's determine the percentage deviation of the transaction price from the estimated price: (520,000 rubles – 502,131 rubles) / 502,131 rubles. x 100% = 3.6%.

That is, the selling price of the bill deviates from the estimated price by less than 20%, so it can be accepted for tax purposes.

Let's change the conditions of example 7 and assume that Vlada LLC sold the bill for 390,000 rubles.

The settlement price of the bill remains the same - 502,131 rubles.

Let's determine by how many percent the bill's selling price deviates from the estimated selling price: (390,000 rubles – 502,131 rubles) / 502,131 rubles. x 100% = 22.33%.

Thus, the selling price of the bill deviates from the calculated price by more than 20% and, therefore, cannot be accepted for tax purposes. In this case, the actual sale price of the bill is adjusted to the settlement price equal to RUB 502,131.

Example 8.

On March 12, 2004, the organization sells an interest-bearing bill of exchange to a third party, the nominal value of which is RUB 100,000. The date of its preparation (stamped on the bill) is February 12, 2004. The maturity date of the bill is September 12, 2004. The refinancing rate of the Central Bank of the Russian Federation at the time of sale of the bill is 14%.

At the time of sale of the bill, 184 days remained until its maturity.

The amount of daily increase in the value of the bill, calculated at the refinancing rate, amounted to: 100,000 rubles. x 14% / 366 days. = 38.25 rub. / day.

The organization can determine the estimated price of the bill, which is necessary to calculate the 20% deviation from the transaction price in the direction of both downward and upward, in the amount of 92,962 rubles. (100,000 rubles – (38.25 rubles/day x 184 days). The transaction price, which is within the limits of such deviation, will be recognized as actual and does not require additional adjustment.

It should be noted that if bringing the proceeds to the settlement price (adjustment) is made by the enterprise, then its amount must be indicated on line 020 of Sheet 06 “Calculation of the tax base for income tax on transactions with securities not traded on the organized securities market.”

A loss was incurred on transactions with third party bills

An enterprise that has a bill of exchange from a third party on its balance sheet can wait until the end of the bill period and present the bill to the debtor for payment, or it can transfer the bill by endorsement (either for cash, or as payment for goods (work, services), or in advance, etc.) at an earlier date. In this case, the company may incur losses on transactions with securities. The question arises: how is such a loss taken into account for the purpose of calculating income tax?

The procedure for recognizing losses from transactions with securities is defined in Art. 280 of the Tax Code of the Russian Federation, in paragraph 10

which states the following:

“Taxpayers who received a loss (losses) from transactions with securities in the previous tax period or in previous tax periods have the right to reduce the tax base received from transactions with securities in the reporting (tax) period (carry forward these losses to the future) in the manner and under the conditions established by Art. 283 Tax Code of the Russian Federation.

In this case, losses from transactions with securities not traded on the organized securities market, received in the previous tax period (previous tax periods), can be attributed to the reduction of the tax base from transactions with such securities, determined in the reporting (tax) period.” .

In addition, when determining the loss from the sale of a bill of exchange, the taxpayer should remember the rules for determining the amount of income and expenses from the sale of securities established by paragraph 2 and paragraph 6 of Art. 280 Tax Code of the Russian Federation

, as well as the dates of recognition for the purposes of calculating income tax of income (

clause 3 of Article 271, Article 279 of the Tax Code of the Russian Federation

) and expenses (

clause 7 of clause 7 of Article 272 of the Tax Code of the Russian Federation

).

Example 9.

On March 1, 2004, Aurora LLC shipped goods to Strela CJSC in the amount of 236,000 rubles. (including VAT - 36,000 rubles). The purchase price of the goods is 120,000 rubles. The buyer paid for the goods with a promissory note from Sberbank of the Russian Federation in the amount of 236,000 rubles. with a payment term “on sight, but not earlier than April 1, 2004. Aurora LLC presented the bill for payment on March 15, 2004. According to the agreement between the SB RF and Aurora LLC “On early payment of a promissory note of the SB RF” to the bank account The organization received 233,000 rubles.

The following entries were made in the accounting records of the enterprise:

| Contents of operations | Debit | Credit | Amount, rub. |

| March 1, 2004 | |||

| Sales of goods reflected | 62 | 90-1 | 236 000 |

| VAT debt accrued | 90-3 | 76/vat | 36 000 |

| Purchase price written off | 90-2 | 41 | 120 000 |

| Received a bank bill in payment for goods sold | 58-2 | 62 | 236 000 |

| VAT added to the budget | 76/vat | 68 | 36 000 |

| March 15, 2004 | |||

| The bank's debt on the bill is reflected | 76 | 91-1 | 233 000 |

| The book value of the bill is written off | 91-2 | 58-2 | 236 000 |

| Cash received on a bill of exchange | 51 | 76 | 233 000 |

| The loss from the sale of the bill is reflected (RUB 236,000 – RUB 233,000) | 99 | 91-9 | 3 000 |

Calculations in the example under consideration show that the amount received on the bill does not deviate from the estimated transaction price by more than 20%, therefore, the transaction price is recognized as actual and does not require additional adjustments. This means that if the above conditions are met, the amount of 3,000 rubles will be taken at a loss.

[1] Federal Law dated March 11, 1997 No. 48-FZ “On bills of exchange and promissory notes.” [2] Resolution of the Central Executive Committee of the USSR and the Council of People's Commissars of the USSR dated 08/07/37 No. 104/1341 “On the implementation of the Regulations on bills of exchange and promissory notes.” [3] Accounting Regulations “Accounting for Financial Investments” PBU 19/02, approved. By Order of the Ministry of Finance of the Russian Federation dated December 10, 2002 No. 126n. [4] Order of the Ministry of Finance of the Russian Federation dated October 31, 2000 No. 94n. [5] Federal Law of November 21, 1996 No. 129-FZ “On Accounting”. [6] Accounting Regulations “Income of the Organization” PBU 9/99, approved. By order of the Ministry of Finance of the Russian Federation dated 06.05.99 No. 32n. [7] The form of the Organization's Profit Tax Declaration was approved by Order of the Ministry of Taxes and Taxes of the Russian Federation dated November 11, 2003 No. BG-3-02/614. [8] Methodological recommendations for the application of Chapter 25 “Organizational Profit Tax”, Part Two of the Tax Code of the Russian Federation, approved. By order of the Ministry of Taxes and Taxes of the Russian Federation dated December 20, 2002 No. BG-3-02/729. [9] Resolution of the Plenum of the Supreme Court of the Russian Federation and the Plenum of the Supreme Arbitration Court of the Russian Federation dated December 4, 2000 No. 33/14 “On some issues in the practice of considering disputes related to the circulation of bills of exchange.” [10] Regulation of the Central Bank of Russia dated September 24, 1999 No. 89-P “On the procedure for credit institutions to calculate the amount of market risks.”

Bill of exchange for payment of goods

If an enterprise uses the method of determining revenue as funds are received when calculating the tax base (to the account of the enterprise or bank), then upon receipt of a bill of exchange as payment for products, tax settlements with the budget will be made in the reporting period in which the bill of exchange becomes due (if the bill is received from a third party - then settlement is made at the time of its receipt). If revenue is determined upon shipment, then taxable profit will be taken into account immediately, regardless of the actual receipt of funds.

Do you need to select material for your study work? Ask a question to the teacher and get an answer in 15 minutes! Ask a Question

VAT on interest on a bill

As a rule, the buyer pays the seller with a bill of exchange, which provides additional income in the form of interest or a discount.

If the goods (work, services) for which the bill of exchange is received are subject to VAT, the interest (discount) on the bill of exchange increases the tax base (subclause 3 of clause 1 of Article 162 of the Tax Code of the Russian Federation). However, VAT does not need to be charged on the entire amount of interest (discount). But only from that part of it that exceeds the amount of interest calculated at the refinancing rates in force in the periods for which the calculation is made (subclause 3, clause 1, article 162 of the Tax Code of the Russian Federation).

Calculate the amount of VAT when receiving interest (discount) on a bill depending on the applicable tax rate as follows.

If the goods (work, services) in payment for which the bill of exchange was received and with which the receipt of interest (discount) on the bill of exchange is associated are subject to VAT at a rate of 18 percent, use the formula:

| VAT | = | Amount of interest (discount) on the bill | – | Interest amount calculated based on the refinancing rate | × | 18/118 |

If the goods (work, services) in payment for which the bill of exchange was received and with which the receipt of interest (discount) on the bill of exchange is associated are subject to VAT at a rate of 10 percent, use the formula:

| VAT | = | Amount of interest (discount) on the bill | – | Interest amount calculated based on the refinancing rate | × | 10/110 |

Such rules are established in subparagraph 3 of paragraph 1 of Article 162 and paragraph 4 of Article 164 of the Tax Code of the Russian Federation.

In accounting, reflect the accrual of VAT on interest (discount) on bills of exchange of buyers (customers) by posting:

Debit 91-2 Credit 68 subaccount “VAT calculations”

– VAT is charged on interest (discount) on the bill.

This procedure is provided for in the Instructions for the chart of accounts.