Is it necessary to lead?

Form KM-6 is an important reporting document for the cashier, which indicates the amount of daily revenue. These report certificates are of great importance when carrying out inspections by supervisory authorities.

Based on them, a complete picture of the completeness of the reflection of the enterprise’s revenue is compiled. Certificates are also required when drawing up a summary report.

The question of whether to fill out a report is ambiguous.

The absence of this form does not entail the application of penalties; in many organizations it is simply not needed; private entrepreneurs, as a rule, do without it.

If the supervisory authorities, when carrying out control activities, discover the absence of a certificate-report, then this fact will be considered an aggravating circumstance.

The director of the company will be in trouble, and he, in turn, will transfer all the blame to the cashier.

In addition to the KM-6 report, the KM-7 form can be drawn up - information about cash register counter readings and revenue must be filled out if the enterprise has two or more cash registers.

Purpose of the report

Based on this report, the organization’s consolidated reporting is generated on the performance of cash registers, as well as on the amount of revenue received for a certain time. This reporting is necessary for the company to report to tax and government authorities on its activities.

The certificate is generated in one copy per work shift or per full working day. At the end of the document, the cashier puts his signature, thereby confirming that he is fully responsible for the information provided in the certificate.

The cashier submits his report to the senior cashier or company manager along with all proceeds. If the organization is small, the cashier can hand over the proceeds directly to the bank's collector. This action is reflected in special reporting.

Revenue is determined based on information from special cash register counters. It must be determined at the beginning and end of each working day. In this case, it is necessary to take into account the money returned by customers back to the cash register. The amount of these funds is subtracted from the total amount of revenue received, then checked and confirmed by responsible employees.

Rules of conduct

One of the norms for maintaining a report is its daily (at the end of the shift) execution.

The cashier signs his autograph on it and hands over the form, along with all proceeds, to the senior (chief) cashier or directly to the head of the company.

If the organization is small (one or two cash desks), then all the money is handed over to the collector of the credit institution.

How to fill?

To prevent errors when filling out the certificate form, you must follow the general rules. The help report is presented in the form of 3 blocks: line, table and summary.

The first line of the document indicates the name of the company, its address (must be identical in all documentation), and telephone number. The name of the individual unit is also indicated.

For individual entrepreneurs, similar rules apply as for legal entities. In a number of situations, individual entrepreneurs mistakenly assume the use of a similar form, but this report is drawn up only on the approved form.

Below is the TIN of the enterprise, structural unit (if any). In the field intended for entering information about cash register equipment, enter its brand (type, model) and serial number in accordance with the available cash register documentation.

The “Application program” line is not filled in if it is not used in the work. Next, the surname and initials of the cashier are entered in the appropriate line; if there are several cashiers, then the field remains blank.

The “shift” cell records the report number, which, as a rule, begins with the letter “Z”.

The next field contains the document details: number, date, start and completion time of work. Don't forget to fill out this information.

The tabular part of the help report is divided into 10 columns:

- 1 — serial number of the control counter;

- 2, 3 — department and section number, respectively;

- 4 - remains empty when using modern cash registers;

- 5 - readings of the cash counter at the beginning of the shift, day (the amount from column 9 of the cashier’s journal of the last shift, a similar amount is written in the morning X-report, in the GROSS TOTAL line;

- 6 - meter readings at the end of the working day, GROSS TOTAL line of the Z-report;

- 7 - enter the revenue for the shift, the sum of all punched checks, the difference between columns 5 and 6;

- 8 - the amount of all refunds and erroneously issued checks, information is displayed in the KM-3 act, to which all checks confirming the return are attached, the information must match the amount from column 15 of the KM-4 journal;

- 9 - cashier's surname;

- 10 – cashier’s signature.

The total expressions of columns 7 and 8 are recorded in the resulting field.

The cashier generates a Z-report from cash register equipment at the end of the working day (shift). It displays information about all cash transactions. Based on the balance recorded in the Z-report, the cashier reconciles the available cash and then transfers it to the responsible persons, the bank.

The cashier removes the X-report from the cash register to determine the cash in the cash register during the work shift (day). An unlimited number of it can be generated, information about such actions is not displayed, and revenue is not reset.

You can put dashes in the empty lines of the KM-6 certificate so that supervisory authorities do not have questions about the document being unfilled.

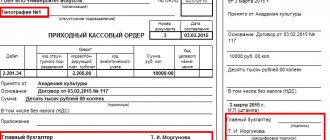

In the final block, the amount of revenue is written down in words. The “accepted” line contains the details of the receipt order.

If the report is handed over to the collector, then information about the transfer of proceeds to the bank is entered; when transferring it to the chief cashier, this line is not filled in.

Next, the cashier, senior cashier and head of the company put their signatures; if these positions are combined by one employee, then the signature is affixed three times.

and a sample of filling out the unified form KM-6

certificate-report KM-6 – word, excel.

filling out the KM-6 form - example.

Other forms of cash documents:

- KO-4 - cash book;

- KO-5 - certificate-report of the cashier-operator.

How to stitch a cash book?

When maintaining a cash book, an important point is not only its correct filling, but also compliance with all requirements for registration of accounting documentation. First of all, this concerns stitching sheets and fastening them.

The order of stitching the sheets of the cash book also depends on how it is maintained:

1. A book purchased from a printing house is bound immediately. Before you start filling it out you must:

- number all sheets;

- sew all sheets;

- on the last page indicate the total number of sheets;

- put a seal (wax or mastic);

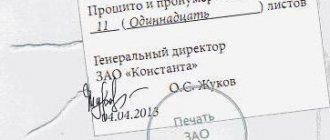

- sign (this must be done by the head of the enterprise and the chief accountant).

2. The book, printed on a computer, is stitched at the end of the year. During the year, the cashier or accountant fills out the printed sheets and stores them in a separate folder, and then staples them according to the same rules as the finished book (indicating the number of pages, the seal and signatures of the manager and chief accountant).

When maintaining and registering a cash book, it is worth remembering several important points:

- Having a book is necessary for those organizations and entrepreneurs who deal with cash in their activities.

- For use, you can either buy a ready-made cash book or print it yourself on your computer.

- A special responsible person is responsible for maintaining the cash book: the chief accountant or cashier.

- In the paper version, the book can be kept either by hand or using technical means (that is, filled out on a computer and printed).

Watch also the video on how to fill out the cash book correctly:

How do I make corrections?

Cashiers with little work experience allow, when filling out the cashier-operator's certificate-report form, sometimes they write their own number instead of the company's TIN.

This is, of course, not true. The identification number is always recorded by the company.

Columns 5 and 6 should be carefully filled out; information from the GROSS TOTAL X-report cannot be entered into column 6.

This error occurs due to negligence and inattention.

There are also errors in the numerical value of writing revenue amounts.

The cashier or cashier-operator must carefully check each digit in KM-6.

If typos occur on the form, penalties can be avoided; a fine is issued for errors in the numbers personally recorded by the operator.

Certificate-report of cashier-operator (filling sample)

The cash document in question is a unified form with a single accepted procedure for filling it out. Each form is numbered and the date and time of operation of the cash register are indicated.

At the beginning and at the end of the working period, the total meter readings must be entered. Information is recorded on the amount of revenue and the amount of cash that was returned to customers according to completed acts in the KM-3 form. Next, the revenue minus returns is recorded, the PKO data or bank details are indicated, depending on where the cash was deposited. After which the document is signed by management, the cashier-operator himself and the person who received the funds.

A sample of filling out the certificate can be downloaded on our website - see the material “Unified Form No. KM-6 - Form and Sample”.

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

Is it necessary for online checkouts?

Explanations of the tax authority dated September 26, 2021 No. ED-4-20/ [email protected] in connection with the use of online cash registers allows legal entities to refuse to maintain a certificate report; all information about transactions performed on cash registers is stored in the taxpayer’s personal account.

If no cash transactions were carried out throughout the working day (shift), then a certificate report is not issued.

Payment is displayed in the KM-6 form:

- In cash;

- bank cards.

Non-cash transfers to the company's current account are not recorded in the report.

Maintaining cash discipline for LLCs and individual entrepreneurs. List of documents

One of the requirements of cash discipline is the presence of a cashier , and his duties can be performed by the director of the enterprise or (in the case of individual entrepreneurs) by the individual entrepreneur himself. In a situation where there is more than one cashier, a senior cashier must be appointed.

In addition to the cashier, the company must have a person who is responsible for generating cash documents. Most often, this responsibility is assigned to the chief accountant. However, as in the situation with a cashier, the role of this person can be played by the cashier or directly undertaken by the individual himself. Responsibilities for generating cash documents can be delegated to an organization that maintains accounting records.

Documents that need to be completed for cash transactions:

- A cash receipt order (PKO) is issued for each receipt of cash at the cash desk. When cash is accepted using a cash register or BSO, then one such order can be issued for the total amount per shift.

- An expense cash order (RKO) is issued for each expense transaction, i.e. for any withdrawal of money from the cash register. It is imperative to check the correctness of filling out such orders and verify the identity of the employee to whom the money is issued.

- Cash book (form KO-4) – records of all income and expense transactions are kept here, i.e. the data of each PKO and RKO must be reflected in it. The cashier's responsibilities include daily reconciliation of cash amounts with balances on cash documents. This may not be done if there were no operations during the shift.

- The accounting book (form KO-5) must be filled out if the enterprise has more than one cashier. This book reflects all movements of money between cashiers and the senior cashier. They must be certified with personal signatures.

- Payroll and payroll must be prepared and signed by employees when payments are made to them.

Maintaining cash documents is acceptable both in paper and electronic form

When completed manually, documents must be certified by original signatures.

Documents in electronic form are drawn up using a computer (other equipment) ensuring their protection from unauthorized access and signed with electronic signatures.

Important! Cash discipline does not include books of income and expenses, BSO, as well as the report and journal of the cashier-operator.

Maintaining a cash book in a separate department

The responsibility for maintaining a cash book is assigned to all separate divisions of the organization in which cash transactions are carried out. Such clarifications were given by the cash circulation department of the Bank of Russia in letter dated May 4, 2012 No. 29-1-1-6/3255. The Federal Tax Service of Russia adheres to a similar position in its letter dated May 17, 2013 No. AS-4-2/8827.

What is a cash balance limit?

The cash register limit or carryover balance is the maximum possible amount of cash that can be left in the cash register at the end of the shift. Anything in excess of this amount must be deposited in the bank. True, small deviations are acceptable on days when a large amount of cash is expected to be issued (paydays) or on holidays.

Setting a cash register limit should be approached extremely responsibly, since if the limit is not set at the end of the work shift, there should not be a single ruble in the cash register. Otherwise, there will be a violation for which administrative liability and a fine are provided.

An order to set a cash limit.

The limit must be calculated and fixed in an internal order, which can set a limit both for a specific period of time and for an unlimited period, i.e. until a new order is issued.

Simplified procedure.

For small enterprises (less than 100 employees and revenue for the previous year less than 800 million rubles) and individual entrepreneurs, from June 1, 2014, establishing a cash balance limit is not mandatory. However, to cancel it, it is necessary to issue an appropriate order based on the Directive of the Bank of Russia dated March 11, 2014 No. 3210-U, which must certainly contain the following wording: “Keep cash in the cash register without setting a limit on the cash balance.”

Important points

If the cash register operator's journal is lost, a specialist from the cash register technical service center is called, he takes down a fiscal report (or a report from the EKLZ unit, if the company has a modern cash register with the letter “K”) from the cash register for the entire period from which the journal was lost.

But it would be better to check the dates with the tax inspector; the procedure for restoring the cashier-operator’s journal is not recorded anywhere, each department may present its own requirements.

Then a free form application is written to the tax office about the loss of the cashier-operator’s journal, a power of attorney is issued with a seal for the registration of the cashier-operator’s journal (for the organization), a new journal is purchased and with the fiscal report removed (or with a report from the EKLZ unit).

Then you should contact the Federal Tax Service again (the date the fiscal report was taken), where, based on the documents submitted, they will issue a new cashier-operator journal.