What is personal income tax

In essence, this fee is an income tax that is levied on residents of the Russian Federation. Foreigners also pay it if they earn money within the country. Tax residents are considered to be people with any citizenship or without it who are in Russia for more than 183 days over a 12-consecutive month period.

Individuals can pay taxes on their own. But the responsibility for calculating personal income tax and its payment is assigned to tax agents - legal entities or individual entrepreneurs, who are required to calculate and calculate the tax according to the law and concluded agreements.

By hiring personnel, the employer becomes a tax agent. He, independently or through the accounting department, calculates the tax, deducts it from the employee’s salary and sends it to the budget.

When working in special modes

If an entrepreneur conducts his business by switching to the simplified tax system or PSN before the start of the reporting period, then personal income tax is not paid on income from the activities specified in the Unified State Register of Entrepreneurs or a patent. When using UTII, a businessman also does not make contributions to the budget from the profit received in the course of conducting his main work. Also see “Who pays personal income tax”.

But there are a number of exceptions that provide for the payment of personal income tax for individual entrepreneurs in 2021 and under these special regimes. These include the following situations (see table).

| Action | Explanation |

| Obtaining a loan from another entrepreneur or legal entity at 0%. | Personal income tax is calculated based on the amount of savings received based on the difference between the percentages. |

| Receiving dividends as an individual while being a member of a joint stock company. | The entire procedure for calculating and paying tax in this case falls on the shoulders of the organization paying income to the individual entrepreneur. The tax agent withholds personal income tax from the profit received by the entrepreneur and sends it to the state treasury. |

| Receiving income from the sale of your own property. | The individual entrepreneur here acts as an ordinary individual. |

Should an individual entrepreneur pay this tax?

The rules for paying income tax for individual entrepreneurs depend on the taxation scheme that he applies. Merchants have access to a general and several special regimes that have their own characteristics, including regarding the payment of fees.

In general mode

Businessmen operating under the general tax scheme are required to pay personal income tax. In this case, income is recorded using the cash method, i.e., in accordance with the receipt of funds at the cash desk or to the current account, and not at the time of registration of documentation. This has nothing to do with receiving an advance and final payment. Income is recognized when mutual settlements are made and earnings are received.

Important! A merchant’s own finances aimed at replenishing working capital are not considered income. The same applies to loans, credits and erroneous receipts.

Special modes

Entrepreneurs do not pay personal income tax under the simplified tax system if they receive income from carrying out the activities provided for by their certificate. But there are several cases when you have to pay such a fee on a simplified basis.

Thus, when receiving income from sources unrelated to business activities, an individual entrepreneur pays a 13% fee, like any other individual. However, the payment can be reduced if you have rights to a tax deduction. Another case of paying tax is receiving income from dividends and certain types of earnings, defined in clause 3 of Article 346.11 of the Tax Code of the Russian Federation.

Individual entrepreneurs using a simplified system pay personal income tax when:

- receiving prizes in advertising and promotional events worth over 4,000 rubles;

- savings on interest on loans;

- receiving interest on foreign currency or ruble deposits;

- receiving royalties not related to the main work activity;

- receiving profit from the sale of your property.

The same applies to any financial receipts outside of professional activities from which tax is not withheld by the tax agent.

For other special modes the following rules apply:

- A businessman on UTII does not pay personal income tax on earnings from activities carried out under this taxation scheme.

- From earnings from any other activity, the individual entrepreneur pays personal income tax for himself.

- Working on a patent does not imply the payment of income tax for the types of activities in respect of which this patent is valid.

- When receiving profit from activities not covered by the PSN, the entrepreneur submits a declaration and pays personal income tax.

- On the Unified Agricultural Tax, merchants do not pay this tax, with the exception of earnings from dividends.

If an entrepreneur has not submitted an application for the application of a special regime, he is considered to be working for OSNO and pays taxes in accordance with the requirements for the general scheme. If a simplifier has violated the rules for applying the special regime, he is transferred to OSNO automatically and is obliged to make tax payments properly, taking into account the features of this system.

Important! No tax is charged on payment for a patent.

Personal income tax for individual entrepreneurs using the simplified tax system in 2021

Taxpayers who use the simplified tax system are exempt from paying personal income tax on profits generated as a result of business activities. This profit is subject to simplified taxation. At the same time, an individual entrepreneur using the simplified tax system is not exempt from paying personal income tax in the cases provided for in paragraphs 2, 4, 5 of Article 226 of the Tax Code of the Russian Federation.

Funds that an individual entrepreneur received from performing those types of activities that are specified during registration and entered into the Unified State Register of Individual Entrepreneurs are not subject to fees.

The profit that an individual entrepreneur receives using the simplified tax system from transactions not listed in the Unified State Register of Individual Entrepreneurs is, by law, considered a transaction made by an individual and is subject to taxation at a rate of 13%.

An individual entrepreneur using the simplified tax system can exercise his right to a tax deduction and reduce his taxable income.

An individual entrepreneur using the simplified tax system is a personal income tax payer in the following cases:

- from profits in the form of cash (material) prizes as a result of participation in various promotions that are carried out by sellers (manufacturers) of products for winnings that exceed 4,000 rubles;

- from the profit generated in the case of receiving loans (from loans in rubles - an amount calculated as 2/3 of the refinancing rate minus the cash equivalent of interest under the loan agreement; from loans in foreign currency - the monetary benefit is calculated at a rate of 9% per annum minus the interest specified in terms of the agreement - in accordance with Articles 212 and 224 of the Tax Code of the Russian Federation);

- from profits generated as a result of receiving interest on bank deposits (deposits in rubles are calculated as the sum of the refinancing rate of the Central Bank of the Russian Federation and 5 percentage points; deposits in foreign currency are calculated at a rate of 9% per annum);

- from profits from foreign sources;

- in the form of dividends (from participation in third-party organizations);

- from funds received for which it was not previously transferred and withheld in accordance with Article 228 of the Tax Code of the Russian Federation.

Thus, an individual entrepreneur using the simplified tax system who needs to pay personal income tax must report to the tax authorities (by filing a declaration) before April 30 of the year following the year of profit formation and pay the tax no later than July 15.

If an individual entrepreneur on the simplified tax system is an employer, he is recognized as a tax agent regarding income paid to his employees. In accordance with the law, individual entrepreneurs are obliged to deduct 13% from their earnings (or 30% for foreigners), transfer them to the budget and submit the relevant certificates to the tax office.

Update 10/19/2019: for foreigners, the Russian government plans to reduce the personal income tax rate from 30% to 13%, making it equal to the rate for residents of the Russian Federation.

How and how much to pay

The peculiarities of paying personal income tax for individual entrepreneurs are related not only to the applied taxation regime, but also to the presence of hired personnel at the businessman’s disposal. Depending on the chosen system, the merchant acts as a tax agent in relation to employees and must withhold personal income tax from the payments he makes. At the same time, the entrepreneur pays tax on his earnings received as an individual.

Without employees

An entrepreneur without employees using the simplified tax system is not considered a tax agent and does not pay personal income tax. But when hiring people under civil agreements, he is obliged to make tax payments on their earnings. In the general mode, a businessman submits reports and pays this tax for himself.

Important! If a businessman combines several taxation schemes, then he must calculate taxes and pay them, as well as provide reporting, in accordance with the requirements for each regime.

With employees

When hiring people, individual entrepreneurs under any regime pay personal income tax for them. This means that a businessman is obliged to submit appropriate reports on time, calculate, withhold and transfer taxes for each employee in accordance with current legislation.

How to calculate and pay taxes correctly?

Moscow Accounting offers to try an extremely convenient service - comprehensive outsourcing services for individual entrepreneurs. We will assign you a professional accountant who works in our office. The specialist will calculate taxes and fees, control the document flow, calculate the salaries of your employees, prepare and submit reports to the tax authorities - and all this in remote work mode, without rush jobs and deadlines.

You will save up to 80% on a full-time accountant and protect yourself from financial risks associated with accounting errors. Leave a request and a consultant will call you back within 5 minutes.

Payment rules

The tax is paid at the place of tax registration. If a tax agent has separate divisions, personal income tax for employees working in them is paid at the location of such divisions.

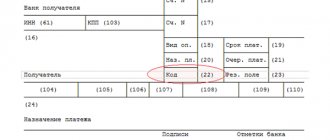

When filling out a payment order, you must provide the following details:

- Payer status in field 101 - for individual entrepreneur 09, for tax agent 02;

- Budget Classification Code (BCC).

KBK Personal Income Tax 2021 for employees for individual entrepreneurs - 182 1 0100 110. For the entrepreneur himself, the code 182 1 0100 110 is indicated.

When specifying the KBK personal income tax for employees in 2021 for individual entrepreneurs, it is better to check the regulatory documentation to avoid making a mistake.

Calculation examples

To calculate personal income tax, you need:

- Determine all income subject to this tax for the reporting period.

- Find out the correct rate for each type of income.

- Calculate the tax base.

- Calculate the payout using the formula.

The formula looks like this: Personal income tax = tax base x tax rate

For example, for an employee with a monthly salary of 58,000 rubles. Personal income tax will be 58,000 x 13% = 7,540 rubles.

If the same employee is entitled to a tax deduction, for example, for a mortgage, its amount is deducted from the tax base.

Advance payments for personal income tax

For individual entrepreneurs, OSNO provides for payment of personal income tax in two ways. The first is an advance payment, which is made upon notification from the tax authorities. This payment is made:

- Six months before July 15th.

- For the third quarter - until October 15.

- For the fourth quarter - until January 15.

Advance payments are calculated based on the information reflected in the declaration in the previous period, taking into account deductions. If the merchant has not received a notification, he has the right not to make advance payments. However, at the end of the year, personal income tax should be calculated and paid in full.

The second option is an adjustment after submitting the declaration to the tax authorities. The businessman needs to return the extra transferred money from the budget or make additional payments as needed. When the payer's income has changed by more than 50% within the tax period, he needs to submit a return to adjust the advance payments. For this purpose, fill out form 4-NDFL.

Important! If an advance is credited with a delay, a penalty will be charged on the resulting debt.

Procedure and deadline for personal income tax payment for individual entrepreneurs

If you use OSNO, then the following procedure for paying personal income tax is provided for you:

- Based on the results of each quarter of the current year, you should calculate the amount of tax to be paid to the budget in the form of advances. Data for calculation - income and expenses for the quarter. The advance must be paid by the 15th day of the month following the quarter (for the 3rd quarter of 2021 - by 10/15/17).

- At the end of the reporting year, calculate the tax amount for the year. Data for calculation - income and expenses for the past year.

- Prepare and submit a tax return indicating the amount of personal income tax for the year. The deadline for submission is April 30 of the next year (for 2021 – until April 30, 2018). See → “Filling out the 3-NDFL declaration for individual entrepreneurs on OSNO in 2021.”

- By April 30, make the final tax calculation (the amount according to the declaration minus advances).

Payment period

Personal income tax for the year is transferred by the entrepreneur until July 15 of the following year. Other deadlines are provided for tax agents:

- From employee salaries - no later than the next day after payment of income to employees.

- For sick leave and vacation pay - no later than the last day of the month in which these payments were made.

- From dividends paid by LLC - no later than the next day after the funds are transferred.

- From dividends paid by JSC - no later than one month after the date of payment.

In addition to penalties for violating the deadlines for paying personal income tax, an entrepreneur faces a fine of 20%.

Personal income tax is paid by every citizen who receives income in the Russian Federation. This obligation also applies to individual entrepreneurs. If an entrepreneur does not have hired personnel, he pays the fee for himself. If there are employees, the businessman acquires the status of a tax agent and makes payments for each hired employee. The specifics of payments depend on the taxation scheme applied. Thus, for individual entrepreneurs, the general scheme provides for advance payments with subsequent adjustments.

Tax amounts may be reduced if you are eligible for appropriate deductions. There are certain deadlines for paying the fee, and in case of violation, penalties and fines will apply.

General information about this tax

There are two main taxes on OSNO: income tax and VAT. Individual entrepreneurs and legal entities pay different taxes on income received. The former pay personal income tax, the latter pay income tax.

The specifics of personal income tax payment to individual entrepreneurs are varied. It is believed that personal income tax is a tax that the employer deducts from the salaries of his employees. However, the individual entrepreneur still calculates and pays taxes on income earned in the course of business.

The tax is calculated based on the profit received as a result of business activities for a specific time period subject to tax.

It consists of:

- income from sales;

- amounts received without payment (discovered during inventory).

Profit accounting is carried out on the day the amount of money is credited to the entrepreneur’s account.

When an individual entrepreneur receives an advance payment for the future provision of services or delivery of goods, this advance also represents a tax basis from the moment it is credited to the current account. The formula for calculating personal income tax is as follows:

Personal income tax = (Income received – Tax deductions – Advance payments) x Rate

For a newly registered individual entrepreneur, there is a certain procedure:

- An activity is being carried out that will lead to the receipt of the first income.

- Based on the first profit, the expected amount for 365 days is calculated (the calculation takes into account the income and expenses of the individual entrepreneur on OSNO for personal income tax, namely, the applicable tax base for 365 days is determined).

- Then this figure is entered into 4-NDFL and the declaration is submitted to the tax office (one month and 5 days are given for submission from the date of receipt of the first profit).

- Taxpayers are sent 4-NDFL, service employees calculate the advance payment according to the tax and send a notification.

- Advances are paid throughout the year according to these notifications.

- At the end of the year, 3-NDFL is filled out and the final calculation of personal income tax for individual entrepreneurs is carried out on OSNO.

Personal income tax reporting for individual entrepreneurs whose work experience is more than a year and who have already submitted tax form 3-NDFL has a different form. From the above list of individual entrepreneurs, you do not need to perform actions from the first to third points. Federal Tax Service employees will calculate the advance according to data from 3-NDFL for the previous year.

If an individual entrepreneur hires employees, then payment of personal income tax for the employees is mandatory. However, in this case, the entrepreneur acts as a tax agent, and the employee acts as a payer. At the same time, it is necessary to submit a 2-NDFL certificate for each employee to the Federal Tax Service. A businessman must pay personal income tax on the next day after his salary is paid to the taxpayer. Transferring personal income tax in advance is prohibited; this payment will be considered incorrect and will be returned.

Personal income tax deducted from vacation and sick leave is credited in the allotted period ending on the last day of the month in which the payment was received. Personal income tax is not collected from the advance payment.

We recommend you study! Follow the link:

Does an individual entrepreneur pay personal income tax for himself and for his employees?