When and what errors occur

Errors in payments between counterparties are made by the compilers of payment orders, i.e. employees of accounting departments. In this case, incorrect data can be in a variety of points in the document: for example, the number of the agreement under which funds are transferred is incorrectly indicated, the purpose of the payment is incorrectly written, or, sometimes, VAT is allocated where it is not necessary, etc.

This can be corrected unilaterally by sending a letter to the partner to clarify the purpose of the payment.

In this case, the other party is not obliged to send a notification of receipt of this message, but it will not be superfluous to make sure that the letter has been received.

What errors can be corrected?

The variety of fiscal taxes and fees often leads to the fact that the taxpayer makes typos in payment documents. If the error is not corrected, the payment may be lost, and the tax authorities will recognize the debt and apply penalties.

If an inaccuracy was identified before the payment document was executed by the bank or Federal Treasury authorities, the payment order can be recalled. But what to do if the payment order (PO) has already been posted and the funds have been debited from the current account in favor of the Federal Tax Service. You can correct a payment order from 01/01/2019 due to any errors, but subject to three conditions:

- The statute of limitations has not expired, that is, three years have not yet passed since the transfers were made to the Federal Tax Service.

- When adjusting payment, no arrears are created for a specific tax liability.

- The money was credited to the budget, that is, it went to the personal account of the Federal Treasury.

In this case, you will have to prepare a sample: an application to the tax office to clarify the payment.

However, not all errors can be corrected. Let's define the key conditions. It is impossible to correct the PP for insurance contributions to the Federal Tax Service, as well as for contributions for injuries to the Social Insurance Fund, if:

- an error was made in the KBK (the first three digits of the budget classification code are incorrectly indicated) in field 104;

- payment of the contribution to compulsory pension insurance was credited to the individual pension account of the employee (insured person), that is, contributions already credited cannot be clarified (clause 9).

- the money has not been received to the appropriate account of the Federal Treasury, that is, fields 13 and 17 (bank and beneficiary account) are filled in incorrectly in the payment order;

In other cases, the taxpayer can correct any errors and inaccuracies in the following fields of the PP: Field number Name 101 Payer status 60 INN of the payer 102 KPP of the payer 61 INN of the recipient 103 KPP of the recipient 104 KBK, but only if the first three digits are indicated correctly 105 OKTMO 106 Basis of payment 107 Payment period 108 Base document number 109 Document date 24 Purpose of payment

Is it possible to challenge a new payment assignment?

Typically, changing the “Purpose of payment” parameter occurs by mutual agreement and without any special consequences. But in some cases complications are possible. For example, if the tax inspectorate during an audit discovers such a correction and considers it a way to evade taxes, sanctions from the regulatory authority can be considered inevitable. It happens that friction regarding the purpose of payment arises between counterparties, especially in terms of payments on debts and interest. In most cases, in order to challenge the correction, the party protesting it will have to go to court, and no one will give guarantees of winning the case, since such stories always have many nuances.

An important condition necessary in order to avoid possible problems is that information about changes in the purpose of the payment must be transmitted to the banks through which the payment was made. To do this, you just need to write similar letters in a simple notification form.

Methods of sending a letter

You can send a clarification letter in one of several ways:

- Bring it in person to the territorial office of the authority;

- Send with a courier service employee;

- Via the Internet;

- By post with acknowledgment of delivery.

If sending is carried out via the Internet, the company’s digital signature must be affixed to the clarification letter about the purpose of payment.

Similar articles

- How to fill out the payment purpose in a payment order?

- Field 107 in the payment order

- How to revoke a payment order

- Payment order fields

- Payment for a third party payment purpose

How to write a letter correctly

A letter to clarify the purpose of payment does not have a unified template that is mandatory for use; accordingly, it can be written in any form or according to a template approved in the company’s accounting policy. At the same time, there is a number of information that must be indicated in it. This:

- name of the sending company,

- his legal address,

- information about the addressee: company name and position, full name of the manager.

- a link to the payment order in which the error was made (its number and date of preparation),

- the essence of the admitted inaccuracy

- corrected version.

If there is several incorrectly entered information, then they must be entered in separate paragraphs.

All amounts must be entered on the form in both numbers and words.

When writing a letter, it is important to adhere to a business style. This means that the wording of the message should be extremely clear and correct, and the content should be quite brief - strictly to the point.

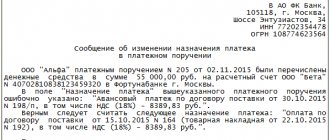

STATEMENT about an error in the execution of a payment order

Moscow 04/06/2017

In accordance with paragraphs 7 and 8 of Article 45 of the Tax Code of the Russian Federation, Gazprom LLC requests a decision to clarify the payment to the Social Insurance Fund. In field 105 of the payment order dated January 13, 2021 No. 415 for the transfer of contributions for insurance against accidents and occupational diseases in the amount of 5,000 (Five thousand) rubles. OKTMO was incorrectly indicated - 43914000.

This error did not entail the failure to transfer the amount of insurance contributions to the budget of the Social Insurance Fund of the Russian Federation to the corresponding account of the Federal Treasury.

General Director ______________ A.V. Ivanov

Chief accountant _________ A.S. Glebova

Download Application to the Social Insurance Fund for clarification of OKTMO in the payment slip for contributions for injuries

If necessary, check with the fund. Please attach a copy of the payment order to your application.

If the payment order was drawn up on paper, the FSS of Russia has the right to demand a copy of such order from the bank. The bank is obliged to provide the fund with a copy of such payment within five days from the date on which they received the request from the FSS of Russia. Then, within five days, the FSS of Russia will issue a decision to clarify the payment (by order of the FSS of Russia dated February 13, 2021 No. 40). This follows from paragraphs 9–12 of Article 26.1 of the Law of July 24, 1998 No. 125-FZ.

to menu

How to format a letter

The law makes absolutely no requirements for both the informational part of the letter and its design, so you can write it on a simple blank sheet or on the organization’s letterhead, and both printed and handwritten versions are acceptable.

The only rule that must be strictly followed: the letter must be signed by the director of the company or a person authorized to endorse such documentation.

It is not necessary to stamp the message, since since 2021 legal entities are legally exempt from the need to do this (provided that this requirement is not specified in the company’s internal regulations).

The letter must be written in at least four copies :

- you should keep one for yourself,

- transfer the second to the counterparty,

- the third to the payer's bank,

- the fourth to the recipient's bank.

All copies must be identical and properly certified.

Sample application for clarification of payment

| To the head of the Federal Tax Service No. your tax office for the Vladimir region (what is your region) From the name of your legal entity INN 330812300601/ KPP 3301001 Address: your legal address | ||

| APPLICATION for clarification of payment | ||

| By payment order No. 10 dated 02.02.2017, Progress LLC paid pension insurance contributions for January 2021 in the amount of 10,000 rubles. By mistake, the company reflected the KBK for 2021 in the payment. Payment of pension insurance contributions was made in 2021. Therefore, the code should be 182 1 0210 160. We ask: – consider the payment order No. 10 dated 02.02.2017 as correct KBK 182 1 0210 160 (clauses 7 and 8 of Article 45 of the Tax Code of the Russian Federation); – clarify the payment and not charge penalties, since the company fulfilled its obligation to pay insurance premiums for January 2021 on time. In addition, the error in the BCC did not result in non-transfer of contributions to the budget. | ||

How and for how long to store a letter

After sending, all letters about clarification of the purpose of payment must be registered in the journal of outgoing documentation, and one copy must be placed in the folder of the current “primary” company. Here it must remain for the period established for such documents by law or internal regulations of the company, but not less than three years . After losing its relevance and expiration of the storage period, the letter can be transferred to the archive of the enterprise or disposed of in the manner prescribed by law.

Documents for offset and return of overpayments for contributions “for injuries” in Social Insurance, 21-FSS, 23-FSS

From 01/01/2017, you will need to apply for a refund or credit for overpaid (collected) premiums for “accident” insurance using new forms.

Social Insurance has approved seven forms used to offset (return) excess contributions. In particular:

- act of joint verification of calculations for contributions “for injuries”, penalties and fines (21-FSS of the Russian Federation);

- forms of decisions on offset and return of amounts of overpaid (or collected) “unfortunate” contributions;

- forms of applications for the return (offset) of overpaid (collected) contributions for insurance against accidents and occupational diseases, as well as penalties and fines ( 23-FSS ).

How to fill out form 23-FSS

As for the forms in force in 2021 for the return (offset) of contributions, approved by the order of the Social Insurance Fund dated February 17, 2015 No. 49, from 2021 they will not be applied to contributions “for injuries”. At the same time, they will continue to be used to return (offset) contributions in case of temporary disability and in connection with maternity for reporting periods that expired before 01/01/2017 (FSS Order No. 458 dated 11/17/2016).

- 4-FSS 2021 new form form download Information is provided on downloading the new 4-FSS form for 2021, which can be downloaded for free. Excel format – Excel. Policyholder code. Example of filling. A link is provided to download the new form 4-FSS.

- Reporting to the Social Insurance Fund according to Form 4-FSS, example of filling out A simple example of filling out reporting to the Social Insurance Fund with comments and explanations is given based on the Procedure for filling out Form 4-FSS and the requirements of current legislation.

According to what principle are maternity leavers assigned and in what time frame are they transferred?

The employer must assign “maternity leave” within 10 calendar days from the date the insured person applies for them with the necessary documents. Payment of benefits is carried out by the employer on the day closest to the assignment of benefits, established for the payment of wages.

Source of the article: https://www.assessor.ru/notebook/fss/utochnit_vznosy_fss/

Instructions: prepare an application to the tax office to clarify the payment

What errors occur

Any organization is a payer of taxes, fees, and contributions. At least some tax payment is credited to the state treasury. For the transfer of budget payments, separate rules for filling out payment orders are provided. A mistake will result in penalties and fines. To correct a shortcoming in a payment, send a special application for clarification to the Federal Tax Service with a request to eliminate the inaccuracy.

All payment deficiencies are divided into three categories:

- critical blots in which the defect cannot be corrected;

- non-critical, in which it is enough to contact the Federal Tax Service to clarify the tranche;

- minor defects that do not require correction at all.

What errors cannot be corrected?

If a critical flaw is found in the payment order, then contacting the Federal Tax Service is pointless. You will have to find the money through the bank, then apply for a refund. There is no guarantee that the funds will be returned to the account. Please note that the return procedure takes a long period of time.

What errors are considered critical:

- The money did not enter the budget system of the Russian Federation. The situation is possible if the taxpayer indicated an incorrect Federal Treasury account in the payment order. If there is no money in the budget, then it is impossible to clarify it. Contact your banking organization to find out the unknown payment.

- The recipient's bank is incorrect. The essence is similar to the first point. If the details and name of the recipient's bank are entered incorrectly, the money will not be credited to the budget. They will remain in unclear tranches or get lost in the bank’s payment system. Contact the bank to find out the erroneous transfer.

Federal Tax Service requirements: what errors are allowed to be corrected

From 01/01/2020, it is allowed to correct a defect in a payment order only if three conditions are simultaneously met (clauses 7, 9 of Article 45 of the Tax Code of the Russian Federation):

The limitation period for the transfer has not expired. That is, no more than three years have passed since the completion of the erroneous tranche.

The adjustment will not lead to arrears in fiscal payments. This means that if, during the correction, the taxpayer incurs arrears in taxes, fees, and contributions, the adjustment will be refused.

What errors may not be corrected?

Minor typos, spelling and punctuation errors in the “Purpose of payment” field do not require correction. For example, if the payer missed a comma or abbreviated words incorrectly, this will not affect the flow of funds to the budget. It is not necessary to contact the Federal Tax Service for clarification.

We invite you to familiarize yourself with the Preliminary medical examination when hiring: for whom it is required

Check whether the error distorts the essence of the payment. For example, if the assignment incorrectly indicates the reporting or tax period, there is a typo in the registration number of the policyholder, etc. Similar shortcomings will have to be corrected by the Federal Tax Service.

How to fix it correctly

To correct the shortcomings, you must contact the Federal Tax Service to clarify the payment. Adjustments are made exclusively on an application basis. This means that the payer will be required to draw up a special application.

[1]

Since there are quite a lot of errors, a unified example of a letter to the tax office about payment clarification is not provided. Compose it in any form. The application is certified by the manager. The signature of the chief accountant is not required, but is desirable.

Prepare a letter to the tax office about clarification of payment in two copies at once if you submit documents in person. One copy of the application will remain with the Federal Tax Service, and the second copy will be marked as accepted by the receiving inspector. It is possible to submit papers by mail, through an authorized representative or electronically (via TKS or through the taxpayer’s personal account).

How to make an application

When drawing up a letter about payment clarification, we take into account the important recommendations of the Federal Tax Service:

Registration requirements

Prepare a letter of clarification on the organization's letterhead. Or, in the header of the form, indicate all the details of the applicant’s company (name, tax identification number, checkpoint and address). This information is necessary to identify the applicant in the Federal Tax Service database.

Structure requirements

We indicate the name of the position of the head and the Federal Tax Service itself to which we are submitting the application. Below we write down the address of the inspection location.

We disclose information about the applicant. Be sure to indicate the name, tax identification number, checkpoint and address. Enter contact information for communication.

We indicate the date of compilation and registration number in the journal of outgoing documentation.

Application for clarification of payment

We must indicate:

- information about the payment order in which an error was detected;

- information about the error itself;

- correct payment details;

- grounds for making corrections (clause 7 of article 45 of the Tax Code of the Russian Federation).

It is not necessary to indicate the reasons for which the deficiency was made.

Make a separate list of attachments to the letter. Be sure to enter the payment details with an error here. It is allowed to attach other documents confirming the circumstances. For example, a bank statement, a copy of a receipt, etc.

Please attach copies of supporting documents to your application.

What to do if the bank made a mistake

If the fiscal tranche was not received by the Federal Tax Service due to the fault of a bank employee, the payer will only learn about this from the Federal Tax Service. The inspectorate will send a demand to pay the arrears and accrued penalties. The procedure for the payer is as follows:

- Check your payment slip and bank statement. Make sure there are no errors in the papers.

- Contact your bank to clarify the payment. Take copies of your payment and statements with you.

- Having solved the problem with the banking error, contact the Federal Tax Service. Prepare a petition in any form with a request to cancel the accrual of penalties. Indicate that the flaw was made by bank employees. Attach documents confirming the correction of the banking error to the application. For example, this is an explanatory bank and a receipt for transferring money to the budget.

The Federal Tax Service will consider the application. If the payer is not at fault, then the accrual of penalties will be canceled.

Sample application to the Federal Tax Service

Use the current sample letter to the tax office to clarify payment. The example is suitable for a situation where an error was made in the KBK.

Inspectorate of the Federal Tax Service of Russia No. 27 for Moscow

Address: st. Novocheremushkinskaya, 58, bldg. 1,

from GBOU DOD SDYUSSHOR "ALLUR"

Address: st. Primarynaya, 12, bldg. 9,

Ref. No. 144 from 09/12/2020

about payment clarification

In the payment order No. 505 dated July 20, 2020 for the transfer of VAT for the 2nd quarter of 2021, in field 104 the code 18210301000012100110 is erroneously indicated as a BCC.

The correct value for field 104 is 18210301000011000110.

Please clarify the erroneous payment based on clause 7 of Art. 45 of the Tax Code of the Russian Federation.

Copy of payment order dated July 20, 2020 No. 505.

Director of the State Budget Educational Institution of Children's and Youth Sports School "ALLUR" IVANOV I.I. Ivanov

https://gosuchetnik.ru/bukhgalteriya/instruktsiya-sostavlyaem-zayavlenie-v-nalogovuyu-ob-utochnenii-platezha

Errors in payment and how to correct them?

| Error | What to do |

| Incorrect Russian Treasury account number and recipient bank details | Tax inspectors will consider insurance premiums unpaid. The Federal Tax Service will demand payment of the arrears with penalties and fines and will block the account (clauses 4, 6 and 8 of Article 45 of the Tax Code of the Russian Federation). You will have to pay the fees again using the correct details. Return the erroneous payment. To do this, contact:

|

Incorrect details:

| The money arrived as intended. Check your payment by submitting an application to the tax office with the correct details |

| You transferred an excess amount of insurance premiums to the budget | You can offset the overpayment against future payments. Another option is to return the overpayment. To do this, submit an application. Before offset or return, the Federal Tax Service of Russia may order a reconciliation of settlements |

| Confused FSS, PF and IFTS | The situation when you sent contributions to the funds to the old details, and not to the Federal Tax Service, is not dangerous. In this case, tax authorities will recode the payment to the correct details automatically. |