In accordance with the requirements of current Russian legislation, all employers, including individual entrepreneurs, must pay compulsory insurance contributions on a timely basis. Ignoring this requirement entails prosecution, including within the framework of the Criminal Code of the Russian Federation. The proposed material examines what the fine for insurance premiums is provided for, and other options for penalties provided for by current regulations for late or incomplete payment of contributions.

Procedure for paying insurance premiums

Insurance premiums are regular payments that must be transferred to organizations, individual entrepreneurs and citizens using hired labor.

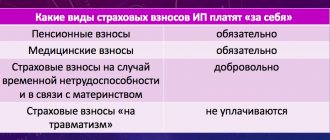

Payment of contributions must be made within the framework of the following types of compulsory insurance:

- pension;

- in connection with disability and maternity;

- medical.

These funds are accumulated in funds that provide material support for target categories of citizens deprived of the opportunity to earn money, on a temporary or permanent basis. Contributions are taken into account according to the billing period, which is determined by the calendar year. Provides for the preparation and submission of reports to the tax authorities, submitted based on the results of the first quarter, six, nine months and annual reports. Payment of contributions is made based on completed accruals for attracted personnel, services rendered and payment for author's orders.

The accounting exception for the calculation of these payments applies to the following amounts:

- government benefits;

- compensation accruals paid to dismissed employees for compensation of damage, payment for accommodation and food, purchase of work clothing, etc.;

- one-time payments accrued for the purpose of providing assistance to victims of a natural disaster, for a born or adopted child, etc.;

- income received from the sale of trade goods of individual nationalities;

- insurance payments for compulsory and voluntary personal insurance;

- other charges and compensations included in the relevant list approved by law.

The amounts of insurance premiums make up the following part of the income received by employers (indicated as a percentage):

- to the Pension Fund – 22;

- for compulsory health insurance – 5.1;

- in the Social Insurance Fund, due to temporary disability and maternity – 2.9.

It is also necessary to pay contributions for injuries, the amount of which ranges from 0.2 to 8.5 percent, depending on the degree of risk of the professional activities of the involved personnel.

Article on the topic: Insurance premiums for individual entrepreneurs for incomes over 300,000 rubles

For the payer’s income amount not exceeding 300 thousand rubles, funds are transferred monthly, no later than the 15th day of the month following the reporting month. Additional payments for contributions for exceeding the specified limit must be paid before the beginning of July of the following reporting year.

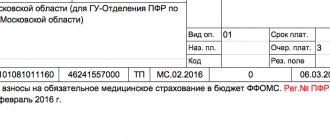

Contributions are transferred according to the appropriate code to the tax department. Payment can be made on the tax service website, through the State Services portal or by contacting a banking institution.

Fines for non-payment of contributions

Until 2021, the procedure for calculating fines for non-payment or late transfer of compulsory insurance contributions was determined by Law No. 212, adopted at the federal level in July 2009. But after the noted period, in 2021 and later, control of the timely transfer of insurance premiums is entrusted to the tax department. At this time, the scale of penalties against violators is determined by the current Tax Code of the Russian Federation, and if non-payment is associated with serious violations of the law - by the Criminal Code of the Russian Federation.

In the FSS

The amount of the fine imposed for late contributions to the Social Insurance Fund is regulated by the provisions of Art. 122 of the Tax Code of the Russian Federation. According to this regulatory act, failure to pay insurance premiums to the Social Insurance Fund threatens the violator with a fine amounting to 20 percent of the accumulated debt. And if the defaulter’s intent is proven, the fine doubles – up to 40 percent.

Additionally, it is possible to punish an official who has committed gross violations of maintaining accounting records, due to which the enterprise has not paid or lately transferred the required contributions.

In accordance with Art. 15.11 of the Code of Administrative Offenses of the Russian Federation, such a violator may be subject to an administrative fine in the amount of 5,000 to 10,000 rubles upon initial detection of a violation of legal requirements. If a similar violation is repeated, a fine of 10,000 to 20,000 rubles may be imposed, as well as removal from office for a period of one to two years.

Individual entrepreneur for himself

For individual entrepreneurs found to have failed to pay or untimely deduct contributions, similar disciplinary sanctions are imposed in the form of fines. An individual entrepreneur is obliged to pay statutory contributions for pension and compulsory health insurance even during the period when business activities are not carried out.

Exemption from these payments is allowed for the following time periods:

- army conscription service;

- caring for the baby until he reaches the age of one and a half years (within six years in total);

- caring for a child with a disability or an elderly relative with a disability;

- living with a husband or wife in a place of military contract service or working in a diplomatic mission in the territory of another state, without the possibility of employment for this period.

Related article: Peculiarities of taxing sick leave with insurance premiums

To avoid a fine for non-payment of insurance premiums, an individual entrepreneur must document the existence of the listed grounds.

IN INFS

Art. 122 provides for the following grounds for imposing a fine for non-payment or partial transfer, late repayment of compulsory insurance contributions:

- reducing the tax base by eliminating charges that must be taken into account when calculating contributions;

- errors in the calculation, including the use of reduced tariffs or inaccuracies in the applied methodology for calculating the tax base;

- other actions of the payer that are unlawful in nature, if this is not related to controlled transactions with foreign companies.

If arrears are identified due to partial or complete non-payment, untimely transfer of the provided insurance contributions, the payer will be presented with a demand from the tax authorities to repay the debt. Additionally, penalties and fines provided by law will be assessed.

But if the policyholder takes into account the required amounts in a timely manner and submits the documentation, and the non-payment is caused by late payment, fines can be avoided. In this case, punishment will follow only in the form of a penalty.

How to pay a fine

The fine is paid in three parts, because insurance contributions include pension, social and medical (proportional to each type). This explanation is given by the Federal Tax Service in letter dated May 5, 2021 No. PA-4-11/8641.

For example, organizations were assessed a fine of 10,000 rubles. Of these, for compulsory pension insurance (10,000: 30 x 22) - 7,333.33, social (10,000: 30 x 2.9) - 966.66 and medical (10,000: 30 x 5.1) - 1,700.

KBC for making fine payments

:

Penalties for late payment of insurance premiums

When calculating the amount of penalties for late insurance payments, three hundredth of the Central Bank refinancing rate for each day of delay is taken into account. If the key rate changes during the period of non-payment, the calculation is carried out separately, depending on the conditions on the day the debt was formed.

The specified key rate measure is applied if the period of late payment of insurance premiums is within 30 days. For each day in excess of the marked time limit, this indicator doubles, amounting to 1/150 of the Central Regional Bank rate.

Amounts of fines

Failure to pay or only partial payment of insurance premiums is grounds for increasing the amount of debt due to penalties and fines. Moreover, their size and applicability depend on the characteristics of the situation. Thus, legally, the amount of the fine can have the following values:

- 20% of the amount of the debt – if we are talking about unintentional non-payment (i.e. the situations listed above, when the individual entrepreneur himself did not realize that the error had occurred);

- 40% of the amount of arrears - if the contribution was not made or was not paid in full by the entrepreneur intentionally.

For example, if the amount of debt on insurance premiums for an entrepreneur is 2,000 rubles, he will be required to pay a fine of 400 rubles. – if the arrears arose unintentionally, 800 rubles. - if he deliberately did not pay this money.

If we are talking about non-payment of contributions for injuries, then the amount of the fine is not determined by tax legislation, since contributions are made to the Social Insurance Fund. And the amount of financial liability is determined by a completely different regulatory act -. At the same time, the size of the fine will not change; they will also be 20 and 40% for unintentional and intentional failure to transfer funds, respectively.

Read: Illegal entrepreneurship - features of prosecution

Criminal penalties for non-payment of insurance premiums (if insurance premiums are not paid on time)

After changes made to the criminal law in August 2021, only violations of tax payments were subject to criminal liability. But after changes in legislation and the transfer of control of insurance contributions to the tax service, the situation has changed.

After the adopted amendments to the Criminal Code, Art. 199 of this document provides for the following punishment options for managers of enterprises and companies, specialists responsible for maintaining accounting records, if a violation of insurance deductions is committed on a large scale:

- penalties from 100,000 to 300,000 rubles. (or deduction of official salary for a period of 1 – 3 years);

- two-year forced labor with the inability to hold a position (indefinitely or for a period determined by the court);

- six-month detention;

- imprisonment for two years or less, without possibility of further appointment.

Article on the topic: Insurance administration of premiums

If the court determines that the violation caused particularly large damage to the state, the penalties provided for the specified categories of violators are tightened:

- the fine increases to 500,000 with a minimum amount of 200,000 rubles;

- In addition to the impossibility of holding relevant positions, the perpetrator may be sentenced to forced labor for a period of five years or less, or imprisonment for up to 6 years.

Major damage is understood as arrears for a three-year period or more, if the amount of non-payment of contributions was from 5 million rubles. For particularly large losses, a similar period of non-payment is noted, with the accumulation of a debt amount of 13 million rubles.

In relation to individual entrepreneurs, the penalty is established by Art. 198 of the Criminal Code of the Russian Federation, providing for the possibility of assigning in case of major damage:

- fine from 100,000 to 300,000 rubles. (or earnings for 1 – 2 years);

- forced labor for up to 12 months;

- six-month arrest;

- three years' imprisonment.

If the amount of non-payment is particularly large, the possible fine increases from 200,000 rubles. up to half a million, duration of forced labor - up to 3 years, imprisonment - up to a similar period (the term of arrest remains unchanged).

When can criminal punishment be avoided?

The policyholder can avoid criminal liability for non-payment or late transfer of insurance premiums if the following circumstances are noted:

- the violation was committed for the first time;

- fully repaid debt;

- paid fines provided for by law;

- paid penalties.

But if a violation that threatens criminal liability is recorded again, punishment cannot be avoided.

To avoid undesirable consequences in the form of fines, penalties or prosecution under the current Criminal Code for late payment of insurance premiums, employers need to carefully and in the manner prescribed by law maintain reporting documentation. And payments for these deductions must be made within the prescribed time frame.

Nuances that accountants and managers should know about

The legislation clearly states what penalties can be imposed for non-payment of insurance premiums. It is also mentioned here that payers are exempt from criminal liability if they committed violations for the first time and paid in full, including penalties and fines issued on the basis of the Tax Code of the Russian Federation.

However, accountants and managers who may be punished for late and incorrect payment of insurance contributions to the budget need to know a few more things:

- a payer who has not transferred correctly calculated contributions to the budget and reflected in the statements faces only penalties (clause 19 of the Resolution of the Plenum of the Supreme Arbitration Court of the Russian Federation dated July 30, 2013 No. 57);

- In case of non-payment or incomplete payment of insurance premiums based on the results of reporting periods (quarter, half-year, 9 months), the payer cannot be charged a fine provided for in Art. 122 of the Tax Code of the Russian Federation (Determination of the Judicial Collegium for Economic Disputes of the Supreme Court of the Russian Federation dated April 18, 2018 No. 305-KG17-20241 in case No. A41-306/2017, Letter of the Federal Tax Service dated July 26, 2018 No. SA-4-7 / [email protected] );

- on the basis of Part 1 of Art. 199 of the Criminal Code of the Russian Federation, to determine the amount of debt of the policyholder, debts for all obligatory payments - taxes, fees and insurance premiums - can be summed up;

- liability under Art. 122 of the Tax Code of the Russian Federation will not occur if the payer has an overpayment, which, when making a decision based on the results of a tax audit, is not offset against other debts (Letter of the Ministry of Finance dated October 24, 2017 No. 03-02-07/1/69682).

Legal documents

- Tax Code of the Russian Federation

- Federal Law of July 24, 1998 No. 125-FZ “On compulsory social insurance against industrial accidents and occupational diseases”

- Art. 122 Tax Code of the Russian Federation

- Art. 199 of the Criminal Code of the Russian Federation

- 199.4

- Resolution of the Plenum of the Supreme Arbitration Court of the Russian Federation dated July 30, 2013 No. 57