Types of standardized expenses used

When an enterprise incurs expenses related to normalization, accounting is carried out especially carefully. The accuracy of the calculations prevents underestimation of income taxes. A number of expenses are found in almost all businesses.

| Type of expenses | Consumption rate size |

| Pension and personal insurance of employees | 12% of the wage fund |

| Employee health insurance | 6% of the wage fund |

| Replacement of defective periodicals | 7% of the circulation cost |

| Loss of printed products | 10% of the circulation cost |

| Certain types of advertising | 1% of revenue |

| Representation needs | 4% of the wage fund |

| Provisions for doubtful debts | Art. 266 Tax Code of the Russian Federation |

Certain types of expenses are taken into account in a special manner:

- Paid for notarization of documents, taken into account in the amount of tariffs established by law.

- Spent on R&D in the form of other expenses depending on wages and amounts allocated for the formation of funds from the sales amount.

- Sent for the maintenance of transport in the amount of standards established by the Government.

- Arising in the form of losses from natural loss within the limits determined by the Government.

The standards established by the Tax Code of the Russian Federation, departmental acts or Government resolutions are regularly reviewed. Before applying standards, their relevance is determined.

Accounting for standardized expenses for tax purposes

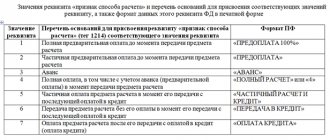

Not all expenses of an organization can be taken into account when calculating the tax base for income tax in full. There are costs that reduce the base partially, within the established norms. Accounting for such expenses has its own peculiarities.

Picture 1.

When talking about accounting for accepted standard expenses for tax purposes, we should dwell on the problem of VAT deduction. Value added tax can be deducted if the following conditions are met:

- goods, works or services purchased for further transactions subject to VAT;

- goods, works, services are capitalized;

- availability of an invoice from the supplier.

Note 1

Since $2015, the second paragraph has been excluded from paragraph $7$ of Article $171$ of the NKRF, according to which VAT on standardized expenses taken into account when calculating income tax is subject to deduction within the limits of the standards. Today, within the limits of the standards, VAT is deductible only on entertainment expenses that are classified as regulated.

The norms for expenses are specified in the Tax Code and in regulations of the Government of the Russian Federation. It is possible to establish standards in a special manner.

Too lazy to read?

Ask a question to the experts and get an answer within 15 minutes!

Ask a Question

Expenses regulated in accordance with the Tax Code include:

- advertising costs,

- voluntary insurance of employees,

- creating a reserve for doubtful debts,

- entertainment expenses,

- interest on borrowed funds,

- costs associated with the sale of media products and books.

Subparagraph $28$ of paragraph one of Article $264$ of the NKRF states that enterprises include advertising costs in other expenses that reduce the income tax base. Paragraph four of the same article determines that advertising expenses can reduce the tax base only within one percent of sales revenue. But this does not apply to all advertising costs. The following expenses are not standardized for tax purposes:

- for advertising through the media and telecommunications networks;

- illuminated and other outdoor advertising, including the production of advertising stands and billboards;

- participation in exhibitions, expositions, fairs;

- design of shop windows, sample rooms, sales exhibitions, showrooms;

- production of advertising brochures and catalogues;

- discounting of goods that have completely or partially lost their quality during exhibition.

Too lazy to read?

Ask a question to the experts and get an answer within 15 minutes!

Ask a Question

All other advertising costs are standardized. These costs cannot be written off until the amount of sales revenue is determined. Standardized advertising expenses are written off after the end of the quarter or month, depending on the reporting period. Costs within the established norm are included in the tax base.

The chart below will help you understand how to account for media advertising for tax purposes.

Figure 2.

Expenses incurred in excess of the norms and not taken into account in one reporting period can be recognized in the next reporting period (during the year). According to paragraphs. $22$ points $1$ st. $264$ NCRF, entertainment expenses are included in other expenses. These include costs associated with holding official receptions and servicing representatives of third-party enterprises participating in the negotiations. An official reception is a breakfast, lunch or other similar event. Entertainment expenses also include costs associated with receiving and servicing participants in meetings of the company’s governing body and officials of the receiving party. Costs for transporting participants to the meeting place and back, services during negotiations, payment for the services of a third-party translator - all these are entertainment expenses. As part of expenses for entertainment purposes, you can take into account the cost of alcoholic beverages purchased for an official event, but only if they are documented and economically justified. Payment for hotel accommodation for meeting participants cannot be included in entertainment expenses for income tax purposes. Expenses for entertainment, recreation, prevention or treatment of diseases are also not considered entertainment expenses.

Note 2

According to paragraph $2$ of article $264$ of the NKRF, all types of entertainment expenses are standardized. Their cost is included in the tax base in an amount not exceeding $4\%$ of the amount of labor costs for the reporting period. Expenses for entertainment purposes are taken into account in the following order. Labor costs are calculated on an accrual basis from the beginning of the year and multiplied by four percent. The result obtained is compared with the amount of entertainment expenses for the same period. Entertainment expenses within four percent of labor costs for the reporting period are included in the tax base.

A calculation certificate for standard expenses may look like this:

Figure 3.

Accounting for interest on borrowed funds is defined in article $269$ of the NKRF. To account for interest in the tax base, it is necessary to determine the method for calculating the amount of interest included in expenses. There are two ways:

- based on the average interest rate,

- based on the refinancing rate of the Bank of Russia.

The first method can be used by taxpayers who intend to take out several loans at the same time. All taxpayers have the right to use the second method. The chosen method of accounting for interest must be reflected in the accounting policy.

In accordance with paragraph $16$ of Art. $255$ NKRF costs for voluntary pension, health insurance and personal insurance of employees are taken into account in the tax base as part of labor costs. Voluntary insurance premiums are included in expenses only for the following contracts:

- long-term life insurance, with a contract term of at least five years;

- non-state pension provision, if accounting of pension contributions is kept on the personal accounts of participants of non-state pension funds, with the payment of pensions until the funds in the participant’s personal account expire, but for at least $5$ years;

- voluntary pension insurance, if lifelong payment of pensions is provided;

- voluntary personal insurance for employees, with a validity period of at least $1$ year and if the insurers provide for payment of medical expenses;

- voluntary personal insurance in case of death or disability as a result of the performance of work duties.

There are certain conditions for including designated contributions in expenses:

- the insurance organization must have licenses to conduct relevant types of activities;

- expenses for voluntary insurance may reduce the tax base in an amount not exceeding twelve percent of the amount of labor expenses.

- for contributions under health insurance contracts included in expenses, the limit is only six percent of the amount of labor costs;

- contributions under insurance contracts concluded in the event of death or disability, expenses cannot exceed fifteen thousand rubles per employee.

In addition to actual expenses, taxpayers have the right to reduce the tax base by the amount of accrued reserves. The rules for accounting for these expenses are defined in article $266$ of the NKRF.

Note 3

Doubtful debt is considered to be receivables that arose as a result of the sale of goods, works or services and were not repaid within the time limits established in the contract, and were not secured by a pledge, surety or bank guarantee. Deductions to reserves for doubtful debts are included in non-operating expenses. The reserve for doubtful debts can only be used to cover losses from bad debts, that is, those debts for which the statute of limitations has expired or there is no way to collect them.

Companies that sell printed periodicals take into account the costs of defective, out-of-marketable or missing copies as part of other expenses. But such expenses cannot exceed seven percent of the cost of the entire circulation of a certain issue of a periodical. Periodicals can be written off if they are not sold before the next issue is published, non-periodic publications only after two years from the date of publication, calendars only after April 1 of the year to which they relate. These costs are standardized and cannot exceed 10% of the cost of printing a given issue of a periodical or book product.

Too lazy to read?

Ask a question to the experts and get an answer within 15 minutes!

Ask a Question

Normalization of thermal energy consumption

Thermal energy consumption is used for the production and management needs of the enterprise. The amount of energy supplied is determined by the technical requirements of the equipment of boiler houses and servicing utility networks. The cost of consumption is determined by the volume of supply and tariffs of the energy producer, fixed by contractual terms.

When concluding a contract, the planned need of the enterprise is calculated, the amount of supply is determined by actual consumption. In the accounting of an enterprise, energy losses may occur during transportation and storage. Losses are taken into account in the amount of natural loss norms determined by government decree (clause 7 of article 254 of the Tax Code of the Russian Federation).

Cost accounting when using a car

Operating transport requires incurring operating costs and costs associated with equipment repairs. Expenses are taken into account for transport owned by the organization, received under a rental or leasing agreement, subject to the acceptance of the equipment into operation or off-balance sheet accounting. In the accounting of individual entrepreneurs, personal vehicles are used, the expenses for which are taken into account in expenses provided that they are used to generate income.

| Type of consumption | How is it determined |

| Fuel | The standards are established by order of the Ministry of Transport. Consumption is determined depending on seasonality, city scale and increasing factors taking into account the year of manufacture |

| fuels and lubricants | The standards are determined by the Ministry of Transport and the enterprise depending on the intensity of operation. |

Accounting for business travel expenses

The relationships of enterprises with partners in other regions require negotiations, personal discussion of contracts and other reasons for business trips. When performing an official task, the enterprise incurs costs, some of which are regulated. The costs take into account:

- Cost of travel to the place of execution of the official assignment.

- Payment for hotel accommodation, registration of additional documents.

- Per diem and field expenses. Payments to employees are not standardized and are taken into account for tax purposes in full (clause 12, clause 1, article 264 of the Tax Code of the Russian Federation).

When calculating daily allowances, the provisions of clause 3 of Art. 217 Tax Code of the Russian Federation. Amounts accrued over 700 rubles per day for business trips within the country do not apply to compensation payments, are considered the employee’s income and are subject to taxes.

Standardized costs

Standardized expenses in tax accounting - such expenses are not included in the current classification, but they also occur. Thus, expenses in this category include those transactions that can be combined according to a general principle: standards have been approved for their recognition in tax accounting. In other words, costs can only be taken into account in a certain amount, but not more than the regulatory limit.

For example, entertainment expenses can be taken into account in the amount of 4% of labor costs for the same period. The costs of voluntary personnel insurance are no more than 12% of labor costs. Some advertising costs are up to 1% of sales revenue.

Legal documents

- Tax Code of the Russian Federation

- Article 253 of the Tax Code of the Russian Federation

- 254

- 264 Tax Code of the Russian Federation

- Ch. 34 Tax Code of the Russian Federation

- Law No. 125-FZ

- Tax Code of the Russian Federation

- Article 265 of the Tax Code of the Russian Federation

Rationing of interest on loans and credits

Interest on debt obligations of ordinary transactions is taken into account in full. Expense rationing is provided for controlled transactions and agreements between related parties. Expenses include the actual interest rate under the contract or the key rate of the Central Bank of the Russian Federation if the standard value is exceeded. The accounting procedure is defined in Art. 269 of the Tax Code of the Russian Federation.

If an enterprise has controlled or uncontrolled transactions, the procedure for writing off expenses is determined independently. Accounting for expenses in taxation depends on the accounting method. With the cash method, inclusion in the composition is made at the time of payment, with accrual - on the last day of the reporting period.

Rationing of advertising events of the enterprise

Costs of advertising the company's activities and attracting customers are written off in full or within normal limits, depending on the type of advertising. Non-standardized types of advertising include:

- Advertising events in the form of information alerts through the media and communication systems.

- Outdoor illuminated advertising, installation of billboards and stands.

- Providing exhibitions, showrooms, printing advertising products, participation in exhibitions and similar forms.

Types of advertising not specified in clause 4 of Art. 264 of the Tax Code of the Russian Federation and spent on the purchase of prizes during promotional events must be taken into account as part of the standardized costs. The limit amount is set at 1% of the amount received from sales in the reporting or tax period.

Cost calculation example

The "Visit" company held an advertising campaign to promote its products in the form of an exhibition. The total cost of expenses was 250,000 rubles. During the event, prizes were awarded for a competition on knowledge of the history of product creation in the amount of 10,000 rubles. Revenue in the accounting period amounted to 150,000 rubles. In the accounting of the enterprise "Visit" the following operations are performed:

- We determined the amount of non-standardized costs: 250,000 – 10,000 = 240,000 rubles;

- We calculated the allowable rate of expenses: 150,000 x 1% = 1,500 rubles.

- Conclusion: the amount of expenses accepted for accounting was 241,500 rubles.

Posting promotional videos

Another controversial cost item is the creation and placement of advertising videos. During inspections, inspectors tend to regard them as “expenses for other types of advertising,” which, according to paragraph 4 of Article 264 of the Tax Code of the Russian Federation, are subject to rationing.

But in practice, the question of whether it is necessary to normalize the cost of an advertising film is not always resolved positively. It all depends on where the video is posted and who provided the services for its placement.

If the video is shown on television, then the costs are fully included in the reduction of taxable profit. This is explained by the fact that, according to the Tax Code, expenses for advertising events through the media are not standardized. And although employees of the Federal Tax Service insist that the showing of a film on TV is taken into account within 1 percent of revenue, taxpayers invariably win in the courts (see, for example, the resolution of the Federal Antimonopoly Service of the North-Western District dated July 10, 2014 No. A44-4952/2013).

The situation is similar with videos that are shown on screens located on the facades of buildings. The cost of such displays can be written off entirely as expenses, since the Code directly states that any outdoor advertising is exempt from rationing. The Ministry of Finance of Russia also agrees with this (letter dated 04/07/10 No. 03-11-06/2/52).

But if the video is placed inside a building (InDoorTV technology), costs generally have to be normalized. This fully applies to the demonstration of advertising films in store sales areas, as the Ministry of Finance of Russia recalled in letter dated 12/06/12 No. 03-03-06/1/631 (see “The Ministry of Finance recognized the costs of showing advertising videos in stores as regulated” ).

An exception is provided for the case when services for placing an advertising video are provided by a company registered as a mass media outlet. In such a situation, the taxpayer has the right to take into account the full amount of expenses, even if the video is shown indoors. Specialists from the Russian Ministry of Finance also agreed with this in a letter dated May 17, 2013 No. 03-03-06/1/17267 (see “The Ministry of Finance explained the procedure for accounting for the costs of advertising using InDoorTV technology (indoor television)”).

Rationing of entertainment expenses

Enterprises bear the costs of negotiations with partners or potential partners, reception, delivery of persons and their accommodation. The list of allowable expenses is established in clause 2 of Art. 264 Tax Code of the Russian Federation. Detailed accounting must be provided to support expenses.

| Accounting transaction | Documenting |

| Approval of the list of costs used to represent the interests of the company | Appendix to the order on accounting policies |

| Issuance of an order | For each reception or negotiation, an order is drawn up separately |

| Approval of the list of costs | An estimate is being drawn up |

| Conclusion of an agreement with a supplier of works and services | The document contains a detailed description of the services or work provided. |

| Confirmation of contract execution | A deed, invoice and other forms are drawn up |

| Submitting the report for approval to the manager | The report on the event includes the purpose, time, location, program, composition of persons, cost item by item |

| Calculation of standardized costs | Produced in accordance with the wage fund |

The size of the norm is limited to 4% of the payroll. Write-off of expenses is carried out during the tax period for calculating profit - a calendar year in proportion to the norm.

Example of calculating the cost rate

The Krona enterprise has prepared a conference meeting with partners to negotiate the terms of contracts. The cost of expenses amounted to 20,000 (including VAT 3050.85) rubles for the event. The company submits quarterly income tax reports. The wage fund for the 1st quarter of 2016 amounted to 200,000 rubles. In the accounting of the Krona enterprise:

- We determined the size of the expense norm: 200,000 x 4% = 8,000 rubles;

- We calculated the amount not taken into account in expenses: 20,000 – 8,000 = 12,000 rubles;

- We determined the amount of VAT to apply the deduction: 8,000 x 18/118 = 1,220.34 rubles.

- Conclusion: the expenses of the 1st quarter of 2021 include the amount of 8,000 rubles, the VAT deduction for the 1st quarter is 1,220.34 rubles.

Direct costs and indirect

This grouping of costs is provided for income tax payers who determine income and expenses on an accrual basis. Let us recall that those entities that have the right to keep records of income and expenses using the cash method should not allocate indirect costs.

If it is necessary to split production costs, the procedure for classifying an operation as a specific type must be determined by the taxpayer independently. That is, the company itself decides what type of expense a particular payment should be classified as. Such a decision to divide expenses into direct and indirect must be enshrined in the accounting policy.

So, direct costs should be attributed to the sale of goods, works, and services within the framework of production in which they were directly involved. These include material costs, wage costs and insurance premiums for key personnel. If an enterprise uses fixed assets in the production (sales) process, then accrued depreciation on these objects can also be taken into account as part of direct costs.

All other types of expense transactions, except non-operating ones, should be classified as indirect. Let us remind you that indirect expenses are recognized when forming the tax base for income tax upon the fact of occurrence, provided there are supporting primary documents.