Which are included in other expenses?

The basic composition of other expenses of an organization in accounting is regulated by the third section of PBU 10/99.

Thus, other expenses are included in accounting (if these are not expenses for ordinary activities in accordance with clause 5 of PBU 10/99):

- expenses associated with the provision for a fee for temporary use (temporary possession and use) of the organization’s assets;

- costs associated with the provision for a fee of rights arising from patents for inventions, industrial designs and other types of intellectual property;

- expenses associated with participation in the authorized capitals of other organizations;

- expenses associated with the sale, disposal and other write-off of fixed assets and other assets other than money (except foreign currency), goods, products;

- interest paid for the provision of funds (credits, borrowings) for use;

- expenses related to payment for services provided by credit institutions;

- contributions to valuation reserves created in accordance with accounting rules (reserves for doubtful debts, for depreciation of investments in securities, etc.), as well as reserves created in connection with the recognition of contingent facts of economic activity;

- fines, penalties, penalties for violation of contract terms;

- compensation for losses caused by the organization;

- losses of previous years recognized in the reporting year;

- amounts of receivables for which the statute of limitations has expired, and other debts that are unrealistic for collection;

- exchange differences;

- the amount of asset depreciation;

- transfer of funds (contributions, payments, etc.) to charity, expenses for sporting events, recreation, entertainment, cultural and educational events and other similar events;

- other expenses.

Please note that other expenses also include expenses arising as a consequence of emergency circumstances of economic activity - natural disaster, fire, accident, nationalization of property, etc.

Also see “How expenses are recognized in accounting.”

Read also

18.07.2019

Other expenses. Line 2350

This line reflects information about other expenses of the organization not mentioned above (clause 21 of PBU 10/99).

What are other expenses of the organization?

With the exception of interest payable, other expenses include (clauses 11, 13 PBU 10/99, paragraph 2, paragraph 20, paragraph 22, paragraph 4, paragraph 38 PBU 19/02, paragraph 13, paragraph 3 paragraph 19 PBU 3/2006, paragraph 7 PBU 17/02, paragraph 25 PBU 5/01, paragraph 20 Guidelines for accounting of inventories, paragraph 6 paragraph 15 PBU 6/01, clauses 21, 41 PBU 14/2007, clause 16 PBU 24/2011, clause 70 Regulations on accounting and financial reporting, Instructions for using the Chart of Accounts, clause 21 PBU 13/2000, clauses 3, 7 PBU 15/2008, paragraph 15 PBU 2/2008, paragraph 14 PBU 20/03, paragraph 14, paragraph 6, paragraph 9 PBU 22/2010):

- expenses associated with the provision for a fee for temporary use (temporary possession and use) of the organization’s assets (if these expenses are not recognized by the organization as expenses for ordinary activities);

- expenses associated with the provision of rights to use intellectual property objects for a fee (if these expenses are not recognized by the organization as part of expenses for ordinary activities);

- expenses associated with participation in the authorized capital of other organizations (if these expenses are not recognized by the organization as expenses for ordinary activities);

— expenses associated with the sale, disposal and other write-off of fixed assets and other assets other than cash (except foreign currency), goods, products;

— the residual value of assets for which depreciation is charged, and the actual cost of other assets written off by the organization;

— expenses associated with payment for services provided by credit institutions;

— contributions to valuation reserves;

— fines, penalties, penalties for violation of contract terms;

— compensation for losses caused by the organization;

- losses of previous years recognized in the reporting year when correcting an insignificant error of the previous reporting year after signing the financial statements for this year or when correcting a significant error of the previous year after signing the financial statements for this year by an organization - a small business entity;

- the amount of receivables for which the statute of limitations has expired, and other debts that are unrealistic for collection;

— negative exchange rate differences;

— part of the additional capital corresponding to the amount of negative exchange rate differences related to the discontinued activities of the organization outside the Russian Federation;

— the amount of depreciation of fixed assets in excess of the amount of its revaluation credited to additional capital during revaluation in previous reporting periods;

— the amount of depreciation of intangible assets in excess of the amount of its revaluation credited to additional capital during revaluation in previous reporting periods;

— the amount of depreciation of the exploration asset in excess of the amount of its revaluation credited to additional capital during revaluation in previous reporting periods;

— loss from impairment of intangible assets;

— loss from impairment of a exploration asset;

— the amount of depreciation of financial investments;

— transfer of funds (contributions, payments, etc.) related to charitable activities;

— expenses for sporting events, recreation, entertainment, cultural and educational events and other similar events;

— expenses for operations with containers;

— expenses for maintaining capacities and facilities that are mothballed;

— costs associated with the consideration of cases in courts;

— R&D expenses that did not produce a positive result;

- amounts of budget funds received in previous years and subject to return in connection with violation of the conditions for their provision;

— expenses arising as a consequence of extraordinary facts of economic activity;

— additional borrowing costs;

— expenses associated with the preparation and signing of a construction contract (if there is no likelihood of its conclusion in the reporting period);

- loss from joint activities distributed among partners;

— other expenses qualified by the organization as other.

Other expenses are recognized when the conditions established by clause 16 of PBU 10/99 are met in the reporting period to which they relate (clause 18 of PBU 10/99).

The rules for recognizing expenses in the Statement of Financial Results are defined in paragraph 19 of PBU 10/99. In particular, the Financial Results Report shows:

— expenses recognized in the reporting period when the non-receipt of economic benefits (income) or receipt of assets becomes certain;

— arising liabilities not caused by the recognition of the corresponding assets.

Other expenses are accounted for in the debit of account 91 “Other income and expenses”, subaccount 91-2 “Other expenses”.

Note!

Organizations are small businesses, with the exception of issuers of publicly placed securities, that recognize revenue not upon the transfer of rights of ownership, use and disposal of products supplied, goods sold, work performed, services rendered, but after receipt of funds and other forms of payment, expenses also recognized after repayment of the debt (paragraph 2, paragraph 18 of PBU 10/99).

From November 16, 2014, simplified methods of accounting, including simplified financial statements, are not entitled to be used by commercial organizations - small businesses if they are microfinance organizations or their accounting statements are subject to mandatory audit (clause 1, 4, part 5 Article 6 of Law No. 402-FZ).

What accounting data is used when filling out line 2350 “Other expenses”?

The value of the indicator of this line (for the reporting period) is determined on the basis of data on the total debit turnover for the reporting period in subaccount 91-2 of account 91 (with the exception of analytical accounts for accounting for interest payable and accounting for VAT, excise taxes and other similar obligatory payments to be received from other legal entities and individuals). The amount of other expenses is indicated in the Statement of Financial Results in parentheses.

Other expenses may not be shown in the Financial Results Statement in detail in relation to the corresponding income if (clause 21.2 of PBU 10/99, clause 18.2 of PBU 9/99, clause 34 of PBU 4/99):

1) accounting rules provide for or do not prohibit such reflection of expenses;

2) income and related expenses arising as a result of the same or similar fact of economic activity are not significant for characterizing the financial position of the organization.

Note!

If types of income are identified in the Financial Results Report, each of which individually constitutes five or more percent of the organization’s total income for the reporting period, it shows the portion of expenses corresponding to each type of income. To do this, the organization can enter additional lines into the Financial Results Report (clause 21.1 of PBU 10/99).

Option 1. If the organization reflects the amounts of other income and other expenses in detail, then:

Line 2350 “Other expenses” = Turnover on the debit of subaccount 91/2 (except for interest payable, as well as VAT, excise taxes and other similar mandatory payments to be received from other legal entities and individuals and reflected in subaccount 91-2)

Option 2. If the organization reflects the amounts of other income and expenses in a collapsed manner, then:

Line 2350 “Other expenses” = Turnover on the debit of subaccount 91/2 in terms of other expenses that are not balanced (except for interest payable) + Negative balance of other income (credit turnover on account 91/1) and other expenses (debit turnover on subaccount 91/2) in terms of income and expenses that are balanced (except for income and expenses included in lines 2310 “Income from participation in other organizations”, 2320 “Interest receivable” and 2330 “Interest payable”, as well as VAT , excise taxes and other similar mandatory payments).

The indicator for line 2350 “Other expenses” (for the same reporting period of the previous year) is transferred from the Statement of Financial Results for this reporting period of the previous year.

Example of filling out line 2350 “Other expenses”

Let’s use the conditions of the previous example, supplementing them with data on line 2350 “Other expenses” of the Financial Results Report for 2013.

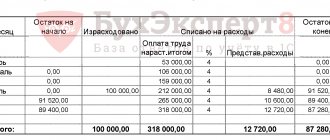

Indicators for subaccounts 91-1 and 91-2 of account 91 in accounting (with the exception of analytical accounts for interest receivable, interest payable, income from participation in the authorized capital of other organizations): rub.

| Turnover for the reporting period (2014) | Sum |

| 1 | 2 |

| 1. For the loan of subaccount 91-1 (according to relevant analytics) | 4 508 120 |

| 1.1. Income in the form of fines, penalties, penalties for violation of the terms of contracts, as well as amounts received in compensation for losses (damage) | 250 000 |

| 1.2. Positive exchange rate differences | 280 635 |

| 1.3. Adjustment of valuation allowances | 900 000 |

| 1.4. Income from the sale of non-current assets | 1 770 000 |

| 1.5. Income from the provision of property for rent | 826 000 |

| 1.6. Assets received free of charge | 150 000 |

| 1.7. Reversal of loss from impairment of intangible assets | 300 000 |

| 1.8. Other other income | 31 485 |

| 2. By debit of subaccount 91-2 (according to relevant analytics) | 6 347 314 |

| 2.1. Expenses in the form of fines, penalties, penalties for violation of the terms of contracts, as well as amounts paid in compensation for losses (damage) | 680 000 |

| 2.2. Negative exchange rate differences | 346 120 |

| 2.3. Contributions to valuation reserves | 1 800 000 |

| 2.4. Expenses associated with the sale of non-current assets | 1 250 000 |

| 2.5. Expenses associated with the provision of property for rent | 550 000 |

| 2.6. Loss from previous years identified in the reporting year (insignificant error) | 260 000 |

| 2.7. Damage caused to the organization (in the absence of perpetrators) | 600 000 |

| 2.8. Other miscellaneous expenses | 465 194 |

| 2.9. Analytical account for accounting for VAT on income from the sale of non-current assets | 270 000 |

| 2.10. Analytical account for accounting for VAT on rent | 126 000 |

Fragment of the Financial Results Report for 2013

Option 1. The organization shows other income and expenses in detail in the Statement of Financial Results.

| Explanations | Indicator name | Code | For 2013 | For 2012 |

| 1 | 2 | 3 | 4 | 5 |

| other expenses | 2350 | (5826) | (4615) |

Option 2. The organization shows other income and expenses collapsed in the Income Statement.

| Explanations | Indicator name | Code | For 2013 | For 2012 |

| 1 | 2 | 3 | 4 | 5 |

| other expenses | 2350 | (3425) | (3642) |

Solution

Option 1. The organization shows other income and expenses in detail in the Statement of Financial Results.

The amount of other expenses is 5951 thousand rubles. (RUB 6,347,314 - RUB 270,000 - RUB 126,000).

A fragment of the Income Statement in Example 6.11 will look like this.

| Explanations | Indicator name | Code | For 2014 | For 2013 |

| 1 | 2 | 3 | 4 | 5 |

| other expenses | 2350 | (5951) | (5826) |

Option 2. The organization shows other income and expenses collapsed in the Income Statement.

1

Let's determine the balance of other income and expenses, which are shown in the Statement of Financial Results on a collapsed basis:

- income (net of VAT) and expenses from renting out property - 150,000 rubles. (RUB 826,000 - RUB 126,000 - RUB 550,000);

- income (net of VAT) and expenses associated with the sale of non-current assets - 250,000 rubles. (RUB 1,770,000 - RUB 270,000 - RUB 1,250,000);

— positive and negative exchange rate differences — (-65,485) rub. (RUB 280,635 - RUB 346,120);

— the amount of created valuation reserves (including adjustments) — (-900,000) rub. (900,000 rub. - 1,800,000 rub.).

2

Let's determine the indicator for line 2350 “Other expenses”.

The amount of other expenses is 2971 thousand rubles. (RUB 680,000 + RUB 65,485 + RUB 900,000 + RUB 260,000 + RUB 600,000 + RUB 465,194).

A fragment of the Income Statement will look like this.

| Explanations | Indicator name | Code | For 2014 | For 2013 |

| 1 | 2 | 3 | 4 | 5 |

| other expenses | 2350 | (2971) | (3425) |

Identification of violations in the accounting of traffic and work permits

If, as a result of inspection actions, violations are identified at any stage, it is necessary to clarify their essence, determine their features and outline corrective measures (most often complex).

The most frequently detected violations are:

- the procedure for recognizing other income and expenses is not reflected in the accounting policy;

- methods for assessing PD&R are not fully established;

- in the working chart of accounts, any subaccount is forgotten to account for P&R (three are required - 91.1 “Other income”, 91.2 “Other expenses”, 91.9 “Balance of other income and expenses”);

- the procedure for reflecting PD&R in accounting documentation is not formalized;

- There are no acts on the inventory of certain types of development work.

If these and other shortcomings are discovered, this indicates that in certain aspects the accounting for other income and expenses is reflected incorrectly and/or incompletely.

Significance of the identified violations

Not all detected inconsistencies have the same meaning. When conducting an audit of development and documentation measures, an assessment of their materiality is carried out - that is, a critical level, upon reaching which accounting data ceases to be reliable and no longer provides data for forecasting and planning. To do this, they evaluate data on shortages and excess amounts and compare the indicators of previous checks and the current state. If the discrepancies are significant, conclusions are drawn:

- about errors in primary documentation, as a result of improper organization of its maintenance;

- about violations of the reflection of financial data for other types of economic activities.

What does an audit of other income and expenses check?

In relation to the P&R audit, a set of verification activities is applied, which includes the following aspects:

- whether, from the point of view of accounting policy, financial resources are distributed between fixed and other;

- whether the feasibility and validity of classifying finances as other income and expenses has been observed;

- whether distributed finances are correctly reflected in the accounting of basic and other income and expenses;

- how correctly the provisions of the accounting policy regarding P&R are formulated;

- whether the choice of a particular accounting policy option is justified under Article 91 (where the law allows for variability);

- whether other costs incurred and income received are accurately posted over time relative to the reporting period;

- how can you evaluate operations related to the DPIR regarding their completeness, timeliness, and reliability of reflection;

- whether appropriate records are maintained in accordance with current requirements and rules;

- whether the internal accounting and audit systems adopted at the enterprise are effective;

- Are there any violations on the part of the P&R regarding the formation of the tax base?

Why are PD&Rs checked separately?

Other income and expenses by their nature have functional differences from other financial income and expenses, especially from those carried out in the main type of activity. P&R accounting indicators have a significant impact on the formation of the organization’s accounting policy, the correct display of financial results, and the formation of rating indicators of the economic activity of the entire organization.

Therefore, verification of PD&R accounting can be carried out by:

- as a separate unit within the general audit;

- as an audit of individual transactions - specifically for account 91.

What transfers determine income

After familiarizing yourself with the list of what other expenses are in accounting, you need to decide on income items and calculations in this direction based on the results of the activities of different institutions. Economists have determined that analytical accounting should be carried out on account 91. It is necessary to organize it in such a way that it is convenient for execution and inspection specialists to use, so that business processes become visible, and the financial result after postings is revealed. To do this, they introduced distinctions into sub-accounts: highlighting the number 1 - the revenue part, while expenses are designated by the number 2 . Income is regulated by a list, according to PBU 9, paragraph 7.

Based on the functionality of the institution, cash equivalents are received. They do not belong to finances earned based on the completed volumes of commercial products of the main production, but come from calculations for:

- rental payments resulting from the temporary provision of premises;

- license fees for the right to own intellectual property;

- payment provided for participation in the authorized capital from another company. This includes interest rates, receipt of income from securities;

- transfer of profits due to joint work under various contracts;

- receiving money from sales of products, commercial products;

- dividends received as accruals for a loan provided to another company;

- bank interest payments, since they have the capital of the enterprise;

- penalties for violation of contracts, debts incurred for late repayment, penalties and interest;

- gratuitous donation of assets;

- compensation for damages by violators of contracts;

- crediting past profits discovered by the audit;

- overdue debts;

- differences in currency rates;

- after revaluation of the asset, the identified profitable amount.

There is a special point where resources obtained from the consequences of natural disasters, accidents, epidemics. Income is considered to be the material assets remaining after unusable assets have been written off.

Tax accounting

According to paragraphs. 17 clause 1 art. 264 of the Tax Code of the Russian Federation, an organization’s expenses for audit services are classified as other expenses associated with production and (or) sales. This rule does not contain any restrictions or exceptions. Thus, the expenses of organizations for conducting mandatory and initiative (voluntary) audits are taken into account when taxing profits.

It should be noted that the issue of accounting for the costs of preparing and auditing reporting according to international standards for organizations that are not required to maintain such reporting is controversial. The Tax Code of the Russian Federation does not contain clarifications on this issue. The official position is that taxpayers can take into account the costs of maintaining reports under IFRS, as well as auditing such reports, if this is a necessary condition for carrying out activities aimed at generating income (Letter of the Ministry of Finance of Russia dated September 4, 2012 N 03- 03-06/1/462).

In accordance with paragraphs. 3 paragraph 7 art. 272 of the Tax Code of the Russian Federation, the date of incurring other expenses (in the form of expenses for payment to third parties for work performed (services provided)) is recognized as one of the following dates:

- settlement date in accordance with the terms of concluded agreements;

- date of presentation of documents serving as the basis for making settlements (for example, an act of provision of services);

- the last date of the reporting (tax) period to which the expenses relate.

In accordance with Art. 313 of the Tax Code of the Russian Federation, an organization has the right to establish a specific date for recognizing expenses in its accounting policies for tax purposes.

As a rule, in accordance with their accounting policies, most organizations reflect the costs of an audit in tax accounting as of the date of the act.

Accounting for auditing costs

Companies often use the services of auditors. Their price is quite high. Therefore, it is important to properly account for such services.

The purpose of the audit is to express an independent opinion on the reliability of the financial (accounting) statements of companies and their compliance with the accounting procedures. This is stated in paragraph 3 of Article 1 of the Law of August 7, 2001 No. 119-FZ “On Auditing Activities” (hereinafter referred to as the Audit Law).

Accounting statements allow its users (for example, owners) to draw conclusions about the results of economic activities, the financial and property position of the company and make decisions.

An audit can be carried out by both audit firms and individual auditors. He can be obligatory and proactive.

Compulsory audits are carried out by companies specified in paragraph 1 of Article 7 of the Audit Law. For example, it cannot be avoided: