Estimate

| Reviews: | 0 | Views: | 4776 |

| Votes: | 0 | Updated: | n/a |

File type Text document

Document type: Statement

?

Ask a question Remember: Contract-Yurist.Ru - there are a bunch of sample documents here

Working balance (turnover sheet) for synthetic accounts +——————————————————————-+ ¦Name¦Balance at the beginning¦Turnover for the month¦ Balance at the beginning ¦ ¦ bills ¦ of the month ¦ ¦ of the next month ¦ +————+—————-+—————-+———————¦ ¦ ¦ D ¦ K ¦ D ¦ K ¦ D ¦ K ¦ +————+——-+———+——-+———+———-+———¦ ¦Cashier ¦ ¦ ¦ ¦ ¦ ¦ ¦ +————+——-+ ———+——-+———+———-+———¦ ¦Products ¦ ¦ ¦ ¦ ¦ ¦ ¦ +————+——-+———+——-+—— —+———-+———¦ ¦Profits and ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦losses ¦ ¦ ¦ ¦ ¦ ¦ ¦ +————+——-+———+——-+—— —+———-+———¦ ¦Reserve ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦fund ¦ ¦ ¦ ¦ ¦ ¦ ¦ +————+——-+———+——-+——— +———-+———¦ ¦Settlements with ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦founders¦ ¦ ¦ ¦ ¦ ¦ ¦ +————+——-+———+——-+——— +———-+———¦ ¦Charter ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦capital ¦ ¦ ¦ ¦ ¦ ¦ ¦ +————+——-+———+——-+———+ ———-+———¦ ¦Calculation ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦account ¦ ¦ ¦ ¦ ¦ ¦ ¦ +————+——-+———+——-+———+— ——-+———¦ ¦Loans ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦banks ¦ ¦ ¦ ¦ ¦ ¦ ¦ +————+——-+———+——-+———+—— —-+———¦ ¦Creditors ¦ ¦ ¦ ¦ ¦ ¦ ¦ +————+——-+———+——-+———+———-+———¦ ¦ Total ¦ ¦ ¦ ¦ ¦ ¦ ¦ +———————————————————————-+

Download the document “Current balance (turnover sheet) for synthetic accounts"

How a beginner can understand accounting

Not all accounting rules are regulated by regulations. Most operations are based on primary accounting documents: acts, certificates, invoices, checks, orders, etc. For primary documents, unified forms and recommended samples are provided. The form of the unified document is approved by the relevant instructions and can only be changed by entering additional details. A list of most of these forms with design examples can be found at this link.

How do unified documents differ from ordinary documents?

Ordinary documents can be modified taking into account the specifics of the enterprise or filled out in any form. Unified forms cannot be changed. This is regulated by Federal Law No. “On Accounting” dated December 6, 2011, which entered into force on January 1, 2013, and Government Decree No. dated July 8, 1996. The forms of primary documents are included in the “Album of unified forms of primary documents”, agreed upon by the Ministry of Finance and approved by the State Statistics Committee of the Russian Federation. The latest amendments to Law 402-FZ were made on May 23, 2016 on the basis of Federal Law No. 149-FZ. Changes have affected the activities of accounting departments of state organizations.

Correct accounting in an organization begins with studying regulatory documents

Download the balance sheet blank form

The basis for the use of reporting is Art. 10 Federal Law No. 402. The document provides the following positions:

- Accounting objects and the values of monetary changes for each parameter are grouped inside the register.

- The data recorded in the primary documentation is registered with subsequent accumulation in accounting registers.

- Forms and types of registers for private companies are approved by the state, and for government agencies - budget legal acts.

SALT is used as a primary document, being an accounting register.

A significant advantage of the document is the visibility of data during an audit.

Info Form The reverse balance sheet can be downloaded for free directly from us. In the regulatory legal acts of the Russian Federation, such a term as “turnover balance sheet” does not exist. We can say that it exists unofficially. This has remained since the times of the Soviet Union, when the “turnover balance sheet” was used as an accounting register.

You can download a blank form of this document for free directly from our website.

The use of the reverse balance sheet is described in some way in the provisions of Art. 10 Federal Law “On Accounting” dated December 6, 2011 No. 402-FZ. This regulatory legal act (LLA) provides that:

- all information that is reflected in primary documents must be registered and accumulated in accounting registers (clause 1 of Art.

The following is the “Balance at the end of the month.”

This indicator is determined by the formula Account balance at the beginning + / - Account turnover = Account balance at the end Accounting statements, calculations, declarations, account cards, balance sheets and other registers are usually stored in paper form. But they can also be stored in electronic format. To do this, certify the documents with an electronic signature.

If it is not there, you will have to print the papers. The document always indicates

- specific amounts.

- whose accounting department generates the document,

- account numbers (sometimes with their decoding),

- name of the enterprise or organization,

An important condition: if compiled correctly, the final numbers in all columns of the statement must match.

But in any case, you have the right to store those registers that are not listed in your accounting policy exclusively on your computer. Keep primary documents such as invoices or receipts for at least five years.

The balance sheet belongs to the category of regular documents and is compiled, as a rule, once a month in a single copy.

We recommend reading: Should you punish a person for what he paid?

It is not necessary to sign the document, but if necessary, it must be certified by the employee who was involved in its preparation or verification (for example, the chief accountant).

According to Order of the Federal Tax Service of the Russian Federation No. ММВ-7-15/184, the taxpayer must provide a balance sheet for monitoring. The analysis can be carried out using different accounts: analytical, chess, synthetic, depending on production needs.

Drawing up balance sheets and posting transactions

The first job that a novice accountant learns is posting transactions and agreements carried out by the company. It is carried out by double entry, in which a debit for one item will necessarily be a credit for another. For example, withdrawing money from a current account and transferring it to the cash desk of an enterprise for the payment of wages to employees is carried out according to section 5: article 51 - current account (credit for the amount withdrawn), 50 - cash register (debit for the same amount). In this way, all transactions are reflected in accounting.

As a result, for any period, the amount of the entire debit must equal the entire credit. This is balance - the ultimate goal of an accountant in a specific period of time. It cannot be otherwise, because money does not just appear and disappear without a trace. But between posting and balance there is a very important intermediate operation - compiling SALT.

Drawing up a balance sheet

Open accounting registers (order journals) for synthetic accounts and record the balance in them as of October 1, 2013, using the data in Table 14.

Table 14 Balance on synthetic accounts as of October 1, 2013

| Account Code | Account name | Amount, rub. |

| 1 | 2 | 3 |

| 01 | Fixed assets | 7578730 |

| 02 | Depreciation of fixed assets | 2400693 |

| 04 | Intangible assets | 145000 |

| 05 | Amortization of intangible assets | 25000 |

| 09 | Deferred tax assets | 50000 |

| 10 | Materials | 1623550 |

| 10/9 | Inventory and household supplies | 60000 |

| 16 | Deviations in the cost of materials | 71000 |

| 19/3 | VAT on purchased assets | 113700 |

| 20 | Main production (including product A - 33,140 rubles) | 33140 |

| 43 | Finished products | 375830 |

| 50 | Cash register | 5670 |

| 51 | Current accounts | 415710 |

| 58 | Financial investments | 140000 |

| 60 | Settlements with suppliers and contractors (Tekhnika LLC) | 682000 |

| 62 | Settlements with buyers and customers | 27970 |

| 66 | Calculations for short-term loans and borrowings | 351870 |

| 68 | Calculations for taxes and fees | 289600 |

| 69 | Calculations for social insurance and security | 51700 |

| 70 | Payments to personnel regarding wages | 180095 |

| 71 | Settlements with accountable persons (accounts receivable from Frolov S.I.) | 4300 |

| 73 | Settlements with personnel for other operations | 68000 |

| 77 | Deferred tax liabilities | 151920 |

| 80 | Authorized capital | 4000000 |

| 83/1 | Increase in property value due to revaluation | 372000 |

| 84 | retained earnings | 1575322 |

| 99/1 | Profit before tax | 900000 |

| 99/2 | Conditional income tax expense | 216000 |

| 99/3 | Permanent tax liability | 10000 |

| 97 | Future expenses | 41600 |

Based on the compiled accounting registers (order journals of a unified form), we will make entries in the general ledger.

Based on the general ledger data, we will draw up a turnover sheet for synthetic accounts (Table 15).

Table 15 Turnover sheet for synthetic accounts for the fourth quarter

| Sh-r accounts | Account name | Balance as of 01.10. | Turnover for the 4th quarter | Balance as of 01.01. | |||

| Debit | Credit | Debit | Credit | Debit | Credit | ||

| 01 | Fixed assets | 7578730 | 133000 | 206000 | 7505730 | ||

| 02 | Depreciation of fixed assets | – | 2400693 | 47000 | 58345 | – | 2412038 |

| 04 | Intangible assets | 145000 | – | – | – | 145000 | |

| 05 | Amortization of intangible assets | – | 25000 | – | 604 | – | 25604 |

| 08 | Investments in non-current assets | – | – | 40000 | 30000 | 10000 | – |

| 09 | Deferred tax assets | 50000 | – | 1000 | – | 51000 | |

| 10 | Materials | 1623550 | – | 63130 | 292580 | 1394100 | – |

| 10/9 | Inventory and household supplies | 60000 | – | – | – | 60000 | |

| 15 | Procurement and acquisition of material assets | – | – | 65000 | 65000 | – | |

| 16 | Deviations in the cost of materials | 71000 | – | 2000 | 11946 | 61054 | – |

| 19/3 | VAT on purchased assets | 113700 | – | 24750 | 138450 | – | – |

| 20 | Primary production | 33140 | – | 702858 | 675844 | 60154 | – |

| 23 | Auxiliary production | – | – | 95979 | 95979 | – | – |

| 25 | General production expenses | – | – | 185578 | 185578 | – | – |

| 26 | General running costs | – | – | 49737 | 49737 | – | |

| 28 | Defects in production | – | – | 2780 | 2780 | – | – |

| 43 | Finished products | 375830 | – | 673064 | 493367 | 555527 | – |

| 44 | Sales expenses | – | – | 32500 | 32500 | – | – |

| 50 | Cash register | 5670 | – | 350495 | 350495 | 5670 | – |

| 51 | Checking account | 415710 | – | 1356356 | 1456745 | 315321 | – |

| 58 | Financial investments | 140000 | – | – | – | 140000 | – |

| 60 | Settlements with suppliers and contractors | – | 682000 | 736050 | 163750 | – | 109700 |

| 62 | Settlements with buyers and customers | 27970 | – | 835676 | 718856 | 144790 | – |

| 66 | Calculations for short-term loans and borrowings | – | 351870 | 320000 | 666000 | – | 697870 |

| 68 | Calculations for taxes and fees | – | 289600 | 141250 | 161612 | – | 309962 |

| 69 | Calculations for social insurance and security | – | 51700 | 63800 | 87870 | – | 75770 |

| 70 | Payments to personnel regarding wages | – | 180095 | 330024 | 305000 | – | 155071 |

| 71 | Calculations with accountable persons | 4300 | – | 15400 | 6000 | 13700 | – |

| 73 | Settlements with personnel for other operations | 68000 | – | 300 | 300 | 68000 | – |

| 76 | Settlements with various debtors and creditors | – | – | 25000 | 2600 | 22400 | – |

| 77 | Deferred tax liabilities | – | 151920 | – | 2800 | – | 154720 |

| 80 | Authorized capital | – | 4000000 | – | – | – | 4000000 |

| 83/1 | Increase in property value due to revaluation | – | 372000 | – | – | – | 372000 |

| 84 | Retained earnings (loss) | – | 1575322 | – | 705989 | – | 2281311 |

| 90 | Sales | – | – | 777620 | 777620 | – | – |

| 91 | Other income and expenses | – | – | 100456 | 100456 | – | – |

| 99/1 | Profit before tax | – | 900000 | 983396 | 83396 | – | – |

| 99/2 | Conditional income tax expense | 216000 | – | 8499 | 224499 | – | – |

| 99/3 | Permanent tax liability | 10000 | – | 2008 | 12008 | – | – |

| 97 | Future expenses | 41600 | – | – | – | 41600 | |

| Total | 10980150 | 10980150 | 8164706 | 8164706 | 10594046 | 10594046 |

Found documents on the topic “turnover sheet for accounting accounts sample”

- Working balance ( turnover sheet ) for synthetic accounts Accounting statements, accounting → Working balance (turnover sheet) for synthetic accounts

working balance ( turnover sheet ) for synthetic accounts +-+ namebalance at the beginningturnovers for the month balance at the beginning... - Sample. Statement accounting sales of products for shipment (No. 16/1)

Accounting statements, accounting → Sample. Product sales accounting sheet for shipment (No. 16/1)statement no. 16/1 accounting for sales of products for shipment for 20 +-+ line-settlement buyer, according to invoices (other documents) shipped...

- Sample. Statement No. 7 in Analytical accounting

Accounting statements, accounting → Sample. Statement No. 7 on analytical accountingstatement no. 7 on analytical accounting to accounts no. 06 “long-term financial investments”, no. 09 “lease obligations due...

- Sample. Statement accounting remaining materials in the warehouse. Form No. m-14

Accounting statements, accounting → Sample. A list of remaining materials in the warehouse. Form No. m-14…2.89 no. 241 sample of the 1st page of the form +-+ (enterprise, organization) code for okud warehouse (storeroom) +-+ statement of balance of materials in the warehouse for 20 financially responsible person (position, acting, last name) ...

- Statement accounting accounts, issued by a branch of a foreign legal entity to buyers of products (works, services). Form No. 5-vpp (instruction of the State Tax Service of the Russian Federation dated June 16, 1995 No. 34 (as amended dated December 29, 1995 No. vz-6-06-672))

Accounting statements, accounting → Statement of invoices issued by a branch of a foreign legal entity to buyers of products (works, services). Form No. 5-vpp (instruction of the State Tax Service of the Russian Federation dated June 16, 1995 No. 34 (as amended dated December 29, 1995 No. vz-6-06-672))...no. 3 to the instructions of the state tax service of the Russian Federation dated June 16, 1995 no. 34 form no. 5-vpp statement of invoices issued by the department (full name of the foreign legal entity) to buyers of products (work...

- Sample. Statement accounting intangible assets and depreciation (No. 17)

Accounting statements, accounting → Sample. Statement of accounting for intangible assets and depreciation (No. 17)statement no. 17 accounting for intangible assets and depreciation for 20 +-+ line type non-short balance for movement...

- Statement accounting accounts suppliers accepted for payment by a branch of a foreign legal entity. Form No. 6-vpp (instruction of the State Tax Service of the Russian Federation dated June 16, 1995 No. 34 (as amended dated December 29, 1995 No. vz-6-06-672))

Accounting statements, accounting → Statement of accounts of suppliers accepted for payment by a branch of a foreign legal entity. Form No. 6-vpp (instruction of the State Tax Service of the Russian Federation dated June 16, 1995 No. 34 (as amended dated December 29, 1995 No. vz-6-06-672))...no. 3 to the instructions of the state tax service of the Russian Federation dated June 16, 1995 no. 34 form no. 6-vpp statement of accounting invoices accepted for payment by the department (full name of the foreign legal entity) for (...

- Accounting statements, accounting statements

, accounting - Sample. Statement accounting issuance (return) of workwear, safety footwear and safety equipment. Form No. MB-7

Accounting statements, accounting → Sample. Record sheet for the issuance (return) of workwear, safety footwear and safety equipment. Form No. MB-7form no. MB-7 was approved by the Decree of the State Statistics Committee of the USSR dated December 28, 1989 no. 241 +-+ okud code +-+ record sheet for the issue (return) of work clothes, safety shoes and safety equipment +-+ month number, type workshop code, department...

- Sample. Statement accounting financing a branch of a foreign legal entity. Form No. 1-vop (simplified) (instruction of the State Tax Service of the Russian Federation dated June 16, 1995 No. 34 (as amended on December 29, 1995 No. vz-6-06-672))

Accounting statements, accounting → Sample. Statement of financing of a branch of a foreign legal entity. Form No. 1-vop (simplified) (instruction of the State Tax Service of the Russian Federation dated June 16, 1995 No. 34 (as amended on December 29, 1995 No. vz-6-06-672))...no. 4 to the instructions of the state tax service of the Russian Federation dated June 16, 1995 no. 34 form no. 1st statement of accounting for the financing of the branch (full name of the foreign legal entity) for (month, quarter, year) +…

- Sample. Statement accounting expenses of a branch of a foreign legal entity. Form No. 2-vop (simplified) (instruction of the State Tax Service of the Russian Federation dated June 16, 1995 No. 34 (as amended on December 29, 1995 No. vz-6-06-672))

Accounting statements, accounting → Sample. Statement of accounting of expenses of a branch of a foreign legal entity. Form No. 2-vop (simplified) (instruction of the State Tax Service of the Russian Federation dated June 16, 1995 No. 34 (as amended on December 29, 1995 No. vz-6-06-672))...no. 4 to the instructions of the state tax service of the Russian Federation dated June 16, 1995 no. 34 form no. 2nd statement of accounting of expenses of the department (full name of the foreign legal entity) for (month, quarter, year) +-+ n...

- Sample. Statement accounting salaries of branch employees in the Russian Federation. Form No. 3-pp (instruction of the State Tax Service of the Russian Federation dated June 16, 1995 No. 34 (as amended on December 29, 1995 No. vz-6-06-672))

Accounting statements, accounting → Sample. Payroll records for branch employees in the Russian Federation. Form No. 3-pp (instruction of the State Tax Service of the Russian Federation dated June 16, 1995 No. 34 (as amended on December 29, 1995 No. vz-6-06-672))…no. 3 to the instructions of the state tax service of the Russian Federation dated June 16, 1995 no. 34 form no. 3-pp statement salary accounting

- Analytical card accounting To account No. 52 "currency" check«

Accounting statements, accounting → Analytical accounting card for account No. 52 “currency account”analytical accounting for account no. 52 “currency account ” name of currency +-+ balance at the beginning of the month currency at the rate +- bank statement...

- Statement accounting results identified by inventory (Unified form N INV-26)

Enterprise records management documents → Statement of results identified by inventory (Unified Form N INV-26)The document “ Statement of accounting of results identified by inventory (unified form n inv-26)” in excel format can be obtained from the link...

- Record sheet for the issuance of workwear, safety footwear and safety devices (Standard interindustry form N MB-7)

Enterprise records → Record sheet for the issuance of workwear, safety footwear and safety devices (Standard interindustry form N MB-7)

Balance sheet as of December 31, 2006

| Name of synthetic accounts | Balances at the beginning of the month | Monthly turnover | Balances at the end of the month | |||

| debit | credit | debit | Credit | debit | Credit | |

| 01 "Fixed assets" | 100000 | 104000 | 204000 | |||

| 02 “Depreciation of fixed assets” | 10000 | 1000 | 11000 | |||

| 08 “Investments in non-current assets” | 104000 | 104000 | ||||

| 10 "Materials" | 130000 | 16000 | 40000 | 106000 | ||

| 19 “Value added tax on acquired assets” | 22600 | 21600 | 1000 | |||

| 20 "Main production" | 153000 | 153000 | ||||

| 43 “Finished products” | 153000 | 153000 | ||||

| 44 “Sales expenses” | 5000 | 5000 | ||||

| 50 "Cashier" | 10000 | 89600 | 69600 | 30000 | ||

| 51 “Current accounts” | 270000 | 310000 | 272000 | 308000 | ||

| 60 “Settlements with suppliers and contractors” | 190000 | 141600 | 147600 | 196000 | ||

| 62 “Settlements with buyers and customers” | 100000 | 240000 | 60000 | 280000 | ||

| 68 “Calculations for taxes and fees” total, including: | 50400 | 50400 | ||||

| 68-1 “Calculations for personal income tax” | 10400 | 10400 | ||||

| 68-2 “Calculations for VAT” | 40000 | 40000 | ||||

| 69 “Calculations for social insurance and security” | 32000 | 32000 | ||||

| 70 “Settlements with personnel for wages” | 80000 | 80000 | ||||

| 75 “Settlements with founders” | 50000 | 50000 | ||||

| 76 “Settlements with various debtors and creditors” | 2200 | 2200 | ||||

| 80 “Authorized capital” | 200000 | 50000 | 250000 | |||

| 84 “Retained earnings (uncovered loss)” | 102200 | 42000 | 144200 | |||

| 90 “Sales” in total, including: | 678000 | 678000 | ||||

| 90-1 “Revenue” | 240000 | 240000 | ||||

| 90-2 “Cost of sales” | 153000 | 153000 | ||||

| 90-3 "VAT" | 40000 | 40000 | ||||

| 90-7 “Business expenses” | 5000 | 5000 | ||||

| 90-9 “Profit (loss) from sales” | 240000 | 240000 | ||||

| 99 "Profits and losses" | 110000 | 42000 | 42000 | 110000 | ||

| Total: | 612 200 | 612200 | 2999600 | 2999600 | 711200 | 711200 |

| Appendix to the order of the Ministry of Finance of the Russian Federation dated July 2, 2010 No. 66n Table 5. Form No. 1 OKUD BALANCE SHEET | |||

| on | 201 | G. | |

| CODES | |||

| Form No. 1 according to OKUD | 0710001 | ||

| Date (year, month, date) | |||

| Organization | according to OKPO | ||

| Taxpayer identification number | TIN | ||

| Kind of activity | according to OKVED | ||

| Organizational and legal form / form of ownership | |||

| according to OKOPF / OKFS | |||

| Unit of measurement: thousand rubles. / million rubles (cross out what is not necessary) | according to OKEI | 384/385 | |

| Location (address) | |||

| Approval date | |||

| Date sent (accepted) | |||

| ASSETS | Indicator code | At the beginning of the reporting year | At the end of the reporting period |

| 1 | 2 | 3 | 4 |

| I. NON-CURRENT ASSETS | |||

| Intangible assets | 110 | – | – |

| Fixed assets | 120 | 90000 | 193000 |

| Construction in progress | 130 | – | – |

| Profitable investments in material assets | 135 | – | – |

| Long-term financial investments | 140 | – | – |

| Deferred financial assets | 145 | – | – |

| Other noncurrent assets | 150 | – | – |

| TOTAL for section I | 190 | 90000 | 193000 |

| II. CURRENT ASSETS | |||

| Reserves | 210 | 130000 | 106000 |

| including: | |||

| raw materials, supplies and other similar assets | 211 | 130000 | 106000 |

| animals for growing and fattening | 212 | – | – |

| costs in work in progress | 213 | – | – |

| finished products and goods for resale | 214 | – | – |

| goods shipped | 215 | – | – |

| Future expenses | 216 | – | – |

| other inventories and costs | 217 | – | – |

| Value added tax on purchased assets | 220 | – | 1000 |

| Accounts receivable (payments for which are expected more than 12 months after the reporting date) | 230 | 2200 | 2200 |

| including buyers and customers | – | – | |

| Accounts receivable (payments for which are expected within 12 months after the reporting date) | 240 | 100000 | 60000 |

| including buyers and customers | 100000 | 60000 | |

| Short-term financial investments | 250 | – | – |

| Cash | 260 | 280000 | 338000 |

| Other current assets | 270 | – | – |

| TOTAL for section II | 290 | 512200 | 507200 |

| BALANCE | 300 | 602200 | 700200 |

urist-consultant.ru

Any errors and incorrectly indicated indicators can lead to blocking of accounts and penalties, which means disruption to the smooth running of business. Therefore, special attention is paid to the correctness of document management and filling out accounting reports.

We recommend reading: Negative value of the amount in section 3 of the RSV

One of the important documents is the balance sheet (TCS), which shows changes in the main parameters of the enterprise’s activities during the reporting period. Anyone who needs a balance sheet can download a blank form for free from various Internet portals in the form of an Excel or Word document. According to Order of the Federal Tax Service of the Russian Federation No. ММВ-7-15/184, the taxpayer must provide a balance sheet for monitoring.

The analysis can be carried out using different accounts: analytical, chess, synthetic, depending on production needs. If the document is drawn up correctly, the debit and credit will coincide in pairs. If there is a discrepancy in the data, you will have to double-check everything.

Mandatory information included in the SALT:

- profit, expenses, amounts for transactions;

- reporting period;

- Company name;

- document's name;

- signatures of management persons.

- indication of the responsible persons who fill out the statement;

- accounts for which the statement is compiled;

The accounting document can be prepared in paper form or electronically, certified by an electronic signature. The provisions of this legal regulation use 2 concepts:

- turnover sheet - a source that records the amounts of income and expenses that correlate with the movement of goods or materials in the warehouse, balances at the beginning and end of the reporting month, as well as the corresponding amounts in synthetic accounts and sub-accounts;

- balance sheet - a document that generally corresponds to the turnover sheet, but it does not record the receipt and consumption of goods or materials.

Due to the availability of these legal regulations, as well as in the course of document management practices in the business and accounting community of the Russian Federation, more or less generally accepted formats of balance sheets gradually became widespread, the structure of which we will consider further.

There is another significant factor for the compilation of turnover by Russian enterprises.

The balance sheet shows the balances of all accounting accounts, credit and debit turnover, and displays the balances at the end of the reporting period. The classic turnover sheet consists of four columns:

- monthly turnover (debit and credit);

- balance at the beginning of the month (debit and credit);

- account name;

- balance at the end of the month (debit and credit).

The “turnover” form is not approved by law.

The balance sheet is intended for drawing up financial reporting forms. Based on this document, a balance sheet is formed.

SHARE

Indicators

“Turnover” allows you to

conduct a detailed analysis of information collected on accounting accounts.

Before you begin to consider SALT, you need to study the structure of accounting accounts (NU)

.

There are three groups of accounts

: active, passive and active-passive. The procedure for collecting and systematizing for a particular group is individual. To correctly understand the information from the statement, you need to know the parameters for maintaining accounts, which of them may have a balance, and which must certainly be closed within a certain period. For example, account 20 must be closed monthly, accounts 90 and 91 do not require this procedure in the context of subaccounts, and, meanwhile, the final balance is not formed for them.

Timely verification of the correctness of the reflection of information makes it possible to eliminate errors and create a balance sheet that reflects the real picture of the organization’s financial position.

The main benefit of SALT is to speed up the reporting process

, as well as in

the efficiency of providing information to external users

.

What is OSV intended for?

The basis for the records are invoices, acts, cash receipts and debit orders, payment receipts, reports on advances issued, salary slips, bank statements with details of calculations. Records are divided into: incoming and outgoing.

Sample journal of business transactions

| date | Contents of a business transaction | Debit | Credit | Amount, rub. |

| 21.04.2011 | A management company has been formed | 75.01 | 80.09 | 10 000 |

| 22.04.2011 | Founder Mokeenko A.V. contributed a share to the management company with materials | 10.09 | 75.01 | 10 000 |

Each such entry is reflected in an accounting entry, which consists of three components: Debit, Credit, Transaction Amount. The journal is compiled in chronological order and may have a significant number of entries.

In this case, it is necessary to leave a comment on each operation. To whom, when, for what goods/services payment was made. Incoming transactions are commented in the same order: from whom, when, how much and for what.

OSV helps to collect all movements on inventory, cash and other assets in a compact form. Allows you to track balances and their changes. The information, in turn, is reflected in the balance sheet.

Important! The report is used by tax officials during audits. SALT will be required by the bank if the organization applies for a loan

Analysis of the statement provides information about the financial reliability and solvency of the organization.

Why do we need regulation of the document flow of an enterprise?

The economic life of a company consists of a sequence of actions that are recorded in a journal (book). The form of the journal is established by the enterprise independently (Part 5, Article 10 of the Federal Law of December 6, 2011 N 402-FZ). Each transaction is recorded by accounting entries using the chart of accounts (Order of the Ministry of Finance N94n dated October 31, 2000).

Entries are reflected in two accounts. The number on the left is a debit (D), and the number on the right is a credit (K). The “primary” items are entered into the journal: invoices, forms of completed work, receipts, invoices, and so on. The enterprise establishes the principles and procedure for recording transactions in its accounting policy (Parts 5, 6, Article 10 of Federal Law N 402-F3 06.11.2011).

Analysis of turnover for account 51

Externally, the back looks like a table consisting of rows and columns. Movements in debit increase the balance, and movements in credit reduce it.

Figure 2. SALT for 51 accounts

In the table you can read which bank the organization works with. The balance at the beginning of the month was 322,327 rubles. During the month, 9,191,259.75 rubles were received. After paying current expenses, the organization had 779,525.84 rubles left at its disposal. It moves to a future period.

If the data is stored on paper, then for detailed analysis you need to refer to the transaction log. Select the desired payment day and amount. Automation allows you to quickly and error-free generate reports for any periods and monetary transactions.

The video will tell you more about this

Revolving balance sheet for accounts: what is it, form, examples

Now let's look at how to fill out a document using a specific situation as an example.

Therefore, the company must develop it independently.

The following information is known about Zheleznaya Volya LLC:

- 80 thousand rubles. the company borrowed (cash);

- 35 thousand rubles. The organization returned the debt (cash).

- 40 thousand rubles. — amount of payment for the goods (cash);

- 40 thousand rubles. the company spent on the purchase of goods from Yurveda LLC;

When the company borrowed money in cash, it increased the amount on hand.

At the same time, the amount of arrears of the company to third parties also increased. The transaction is reflected by the following posting: Debit 50 Credit 66 – a cash loan was received. For the second operation (purchase of goods), the organization needs to show the increase in account 41 “Goods” and the debt to the supplier: Debit 41 Credit 60 - the costs of purchasing goods are reflected.

Subsequently, the company reduced the debt to the supplier; the change must be shown in account 60.

If, as in our situation, the organization took money from the cash register, the posting will be as follows: Debit 60 Credit 50 - the debt to the supplier is repaid. The last operation - the company returned the money it borrowed (account 66).

The posting must show that the debt has been repaid and the amount on hand has decreased: Debit 66 Credit 50 – the debt under the loan agreement has been repaid. Download for free How to calculate profit and loss according to the tax return balance sheet there is an account 99.

It is to him that an organization needs to turn if it wants to calculate profits and losses.

Subaccounts are usually opened to this account, for example, subaccount 99.1 “Profits and losses from ordinary activities.”

Subaccounts 99.1 – 99.7 will have more detailed information. To analyze the data, you need to remember the following information. The debit balance on account 99 is the company’s final loss, and the credit balance is its net profit. We said earlier that the turnover sheet can be compiled separately for each account.

Using the example of a specific organization, let's look at how to fill out a balance sheet for three main accounts. Namely:

- (count 60);

- .

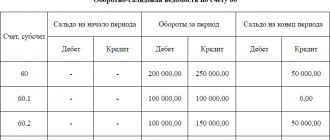

Status LLC transferred to its partner, Runa LLC, 150 thousand rubles in advance payment under the service agreement.

The company reflected this operation in the balance sheet table as an increase in receivable assets in subaccount 60.1. A month later, the organization received inventory from the counterparty totaling 210 thousand rubles. Due to this amount, the company's credit liability in subaccount 60.2 increased.

After another two weeks, “Status” transfers the partial cost of the goods in the amount of 150 thousand rubles to the partner. The company shows the operation in the document as a decrease in liabilities in subaccount 60.2 (in debit) and a decrease in assets in subaccount 60.1 (in credit). As a result, the company owed the counterparty 60 thousand.

rub. She showed the amount of debt under the loan of subaccount 60.2 (on credit). In line 60, the company entered the same numbers as in the “Result” column. In the “balance at the beginning of the period” field, due to the lack of indicators, the organization put dashes.

Account/sub-account

Basic rules for drawing up SALT

Today, there is no standardized, obligatory sample of this document, so it can be drawn up in free form or using special templates. Sometimes companies develop their own statement forms (based on their own needs) and subsequently print them in a printing house.

At first glance, SALT may seem like a simple set of numbers divided into different columns. However, in fact, it is a clearly structured summary table into which information is entered on various transfers, economic and financial operations of the enterprise, including such as writing off production costs, calculating taxes, calculating depreciation, generating reports, etc. .

Balance sheet: sample filling, example and basic details

Although the regulatory requirements for this report are not fixed in legislative acts due to the fact that it plays rather a technical role, it is an official document that must have the following details:

- Title (where the actual name of the report is indicated)

- Details of the company composing it

- Compilation period

- Units of accounting for objects of analysis

- Details of the persons responsible for the correct formation of the document

How to correctly fill out a balance sheet?

Basic rules for filling out the document

- The informative component of the document consists of: account number, account description, account balances (active or passive) at the beginning and end of the reporting period, account turnover for the reporting period.

- Each type of balance sheet has its own characteristics. When drawing up a document on synthetic accounts, you need to know that a correctly compiled statement of this type has three mandatory equalities.

- The amount of debit funds at the beginning of the reporting period must be equal to the amount of credit funds of the same reporting date. This equality follows from the fact that the funds of an enterprise are both its assets and the sources of their formation.

- The turnover on debit accounts must be equal to the turnover on credit. This equality follows from the principle of double entry: for example, wages are both production costs and the enterprise’s debt to employees.

- The third equality is expressed in the fact that the value of the company's assets must be equal to the amount of the company's liabilities. This equality also follows from the principle of double entry.

- A statement compiled from analytical accounts allows you to obtain information in the context of the necessary factors (assortment, types of counterparties, quantity).

- A chess sheet is compiled to record turnover in the debit and credit of accounts. The principle of double entry means that the assets of an enterprise are simultaneously its liabilities to counterparties.

What is better for a novice businessman to open: an individual entrepreneur or an LLC? The answer is contained in this article.

Accounting principles included in the Accounting Regulations “Accounting Policy of the Organization” (PBU 1/98):

- property isolation;

- going concern;

- consistency of accounting policies;

- temporary certainty of the facts of economic life;

- completeness of reflection of accounting information;

- timely reflection of the facts of economic life;

- the identity of analytical accounting data with turnovers and balances on synthetic accounting accounts on the last calendar day of each month;

- rationality of accounting.

An accounting method is a set of techniques by which accounting records are maintained. Such techniques include:

- documentation;

- accounts;

- double entry;

- inventory;

- evaluation and costing;

- balance;

- reporting.

Documentation is a set of documents that provides a continuous and continuous reflection of the economic activities of the enterprise. Each separate document is written evidence of the fact of a business transaction. The following mandatory details give the document legal force: name of the document, date of preparation, name of the organization on behalf of which the document is drawn up, content of the business transaction, measures of the business transaction in kind and monetary terms, names of positions of persons responsible for the execution of the business transaction, personal signatures of these persons. Accounts are a tool for coding, accounting and grouping economic assets and transactions. We will look at the account in more detail in the corresponding chapters. Double entry - recording a business transaction on the debit of one account and on the credit of another - provides an interconnected and controlled reflection of the transaction. Coding a business transaction using double entry is called an accounting entry. Inventory – checking the availability of inventory, cash and financial obligations. Valuation and calculation are methods of determining the cost of economic assets, the costs of their acquisition and construction, production costs, costs of selling products, etc. Balance sheet is a way of summarizing and grouping economic assets and their sources as of a certain date. We have already looked at an example of a balance sheet above; we will look at it further. Accounting statements are a general picture of the property and financial condition of an enterprise, as well as a reflection of its economic activities for the reporting period.

see also Functions and tasks of an accountant

* * *

So, we looked at why a balance sheet , as well as how it is compiled using the example of a specific account.

The balance sheet is maintained for internal accounting and is provided upon request to the tax authorities. It indicates the movement of goods, materials and cash, other assets, as well as the liabilities of the company, its capital, reflected in the accounting accounts. In addition, it reflects the balances at the beginning and end of the specified period for these accounts.

We hope that our article will help you in the process of accounting and in preparing the specified statement.

Similar articles

- How to correctly prepare a balance sheet?

- How to read the balance sheet?

- How to check the balance sheet?

- How is the balance sheet for account 01 formed and used?

- How is the balance sheet formed for account 70?

Synthetic and analytical accounting

Accounts that are intended for a generalized reflection of economic assets and their sources are considered synthetic. This type is used to account for company funds in a single monetary value.

Synthetic accounting is used:

- to fill out reports,

- to fill the balance,

- analysis of the financial and economic activities of the company.

To control the safety of valuables, you need to know not only their total value, but also other data necessary for identification. If a company has accumulated debt, along with finding out its total volume, it is necessary to determine the reason for its occurrence.

Analytical accounts allow you to keep records in both physical and monetary terms. They open in addition to synthetic ones. Recording transactions with category accounts is called analytical accounting. Its implementation is necessary to control and ensure the safety of inventory items.

Filling example

Let's look at an example of filling out 71 accounts. One of the company’s employees, for example Ivanov, received funds in the amount of 200,000 rubles for business needs. And Petrov, an employee of the same organization, received 20,000 rubles for business trips.

Accordingly, both employees will need to report on their expenses and provide relevant documents.

A week later, employee Ivanov, confirming his actions, brought an advance report containing 9,000 rubles. Petrov brought the same document, but only for 19,000 rubles.

This raises the question - how to compile SALT for account 71, where business transactions will be indicated?

Such a document will be compiled in the form of a table, where the columns will be designated as follows:

| Account (sub-account) / Analytical characteristics of a sub-account | Balance at the beginning of the period | Period transactions | balance at the end of period | ||

| Debit | Credit | Debit | Credit | Debit | Credit |

Moreover, in the first column the following will be recorded:

- Synthetic account.

- A subaccount on which transactions were also carried out, but only if it is included in the chart of accounts that will be used by the organization.

- Analytical features by which this subaccount can be determined. Here the signs can be anything, but most often they represent the initials of those employees to whom the cash was entrusted.

Next, you should record in the document the fact that two employees were actually given funds in the specified amount. Such transactions will correspond to the following transactions:

- Dt.71.01 Kt.50 - 10000;

- Dt.71.01 Kt.50 - 20000.

The following data should be reflected in the SALT:

- First, we enter two amounts in the Debit column opposite the corresponding account characteristics (in this case, these will be the names of employees).

- Next, we sum up the two numbers that will help form a debit, and indicate the resulting figure of 30,000 rubles in the Debit column opposite the account.

- If there were no other transactions on the account, then the resulting amount is duplicated again opposite the 71 account.

When employees present checks and reports, the following entries are made:

- Dt.10 Kt.71.01 - 9000;

- Dt.26 Kt.71.01 - 19000.

In the OCB we additionally indicate the following data:

- We enter checks for 9000 and 19000 opposite the initials of the employees in the Credit column.

- We sum up the data on credit transactions to get the amount of 28,000.

If the initial balance is zero, then in order to calculate the balance at the end of the month and duplicate it in SALT, you need to subtract smaller amounts from the large amounts listed in the columns under the Turnover cell at the end of the month.

If the former are recorded in the Debit section, and the latter in the Credit section, then the results of the calculations are indicated in the Debit section, located under the Balance cell at the end of the month. Here it will consist of:

- 1000 rubles according to the reports of employee Ivanov (this amount will be written opposite his last name);

- 1000 rubles according to the reports of employee Petrov (also recorded opposite the corresponding surname).

After entering the data in the Debit column, located under the End of Period Balance cell, opposite the account itself, you should sum up all the analytical characteristics of the account (in this example, it is 2000 rubles). The same value should be duplicated opposite account 71 under the Balance at the end of the month cell.

As a result, based on the results of operations, a debit balance calculated for 71 accounts is recorded in the SALT. And the total amount of such balance will be 2000 rubles.

And here is an example of what the result of all the above operations will look like:

| Account (sub-account) / Analytical characteristics of a sub-account | Balance at the beginning of the period | Period transactions | balance at the end of period | ||

| Debit | Credit | Debit | Credit | Debit | Credit |

| 71 | 30000 | 28000 | 2000 | ||

| 71.01 | 30000 | 28000 | 2000 | ||

| Ivanov | 10000 | 9000 | 1000 | ||

| Petrov | 20000 | 19000 | 1000 |

Reverse balance sheet blank form free download in Word

The absence of a statement or errors when filling out the “turnover” are classified as a gross violation of the rules for accounting for expenses and income. The tax inspectorate fines for such violations 10,000 rubles.

And for long-term violations of the turnover, the fine is 30,000 rubles. You can maintain a balance sheet on paper, as before, or in electronic form using an accounting program.

In the latter case, the “turnover” is printed at the end of each reporting period, at the end of the year, and also for presentation at the request of the tax authorities. The balance sheet shows the balances of all accounting accounts, credit and debit turnover, and displays the balances at the end of the reporting period. The balance sheet is intended for drawing up financial reporting forms.

https://www.youtube.com/watch?v=FUAp8FeeAu4

The classic turnover sheet consists of four columns:

Revolving balance sheet for accounts: what is it, form, examples

There are three main types of balance sheet:

- combined (include elements of synthetic and analytical calculations).

- according to analytical accounts (formed by quantity, category and nomenclature);

- according to synthetic accounts (takes into account the totality of different values);

There are at least five reasons why an accountant cannot do without drawing up the SALT.

There are no errors in the calculations if:

- the amount of debit funds at the beginning of the reporting period is equal to the amount of credit funds of the same reporting date;

Reverse balance sheet: blank form free download

Drawing up a balance sheet is mandatory if it is approved as an accounting register for a company or entrepreneur.

An order for approval of accounting policies may be as follows: . The persons who compiled and signed it are responsible for the correct preparation of the balance sheet. The absence of a statement or errors when filling out the “turnover” are classified as a gross violation of the rules for accounting for expenses and income.

The tax inspectorate fines for such violations 10,000 rubles. And for long-term violations of the turnover, the fine is 30,000 rubles. You can maintain a balance sheet on paper, as before, or in electronic form using an accounting program.

In the latter case, the “turnover” is printed at the end of each reporting period, at the end of the year, and also for presentation at the request of the tax authorities.

The balances are shown in the balance sheet

An example of filling out and a balance sheet form

But at the same time, this law provides that primary information should be grouped in accounting registers in monetary terms. And therefore, the use of the balance sheet has spread in practice.

In addition, the specified accounting register is given much attention by the tax authorities, who request and study it during each audit.

Also, the Federal Tax Service, as part of the innovation in the form of tax monitoring, has provided for the mandatory submission of balance sheets for analysis and control in the document flow with taxpayers.

The balance sheet is compiled using synthetic and analytical accounts, and can also be mixed.

The structure of the balance sheet includes 7 columns: account name; balance at the beginning of the period for Dt and Kt; turnover according to Dt and Kt; balance at the end of the period according to Dt and Kt.

Form reverse balance sheet

How to stitch documents correctly with thread? Photos and step-by-step instructions are contained in our new publication here.

The peculiarity of this type of report is that it can be compiled in the context of individual accounts, or even subaccounts, and also that it is compiled on any date, without waiting for the end of the reporting period.

Depending on what is the object of research, the document is formed using synthetic accounts, analytical accounts, or a chessboard pattern.

Is it possible to get a loan to open a small business from scratch and what needs to be done for this - find out by following the link.

A document compiled on the basis of an analysis of analytical accounts makes it possible to track cash flows and reserves in the context of a specific account in the Chart of Accounts. The main purpose of the chess statement is to provide information on business transactions for the reporting period.

It does not indicate balances, it contains data only on cash flows.

Turnover balance sheet - sample filling 2021 - 2020

; the structure of the accounting register must contain a grouping of accounting objects, as well as the monetary value of the corresponding objects; the forms of the corresponding registers for private economic entities are approved by management, for state ones - by budgetary legal acts. The fact that the balance sheet is used as an accounting register can be associated, first of all, with the legal tradition that was formed in the Soviet Union.

Another significant factor predetermining the use of turnover by modern enterprises is the publication by the Ministry of Finance of Russia of Order No. 119n dated December 28, 2001, by which

How to fill out the turnover sheet (form, sample)?

It will contain:

- debit turnover;

- balance at the end of period.

- balance at the beginning of the period;

- loan turnover;

It is more convenient to consider the algorithm for compiling the turnover sheet using the example of a separate synthetic account.

A week later, Ivanov reported on the use of funds, providing an advance report with supporting documents in the amount of 9,000 rubles. Petrov brought the employer a similar set worth 19,000 rubles.

What will the turnover sheet look like?

Rules for filling out the balance sheet for account 50 - form and sample in excel

This requirement applies to both incoming and outgoing transactions that determine the dynamics of the organization’s cash balance.

The following settlement actions involving the movement of cash are required to be reflected on the 50-account:

- collection, transfer of cash to the servicing bank;

- providing employees with cash on account (for example, for business needs, for business trips);

- issuing wages to employees of the organization.

- cash receipts for goods sold, services provided, work performed;

- return to the buyer (client) of previously paid money;

Account 50 clearly belongs to the category of active accounting accounts. As mentioned earlier, you can open and maintain separate sub-accounts using it. Debit always records any receipts (receipts) of cash issued by PKO orders.

Features of the balance sheet

They are similar, but have a number of significant differences that you need to familiarize yourself with in advance. The company has the right to independently develop a statement form or use a ready-made sample.

Having chosen the first option, you need to remember the need to include mandatory data in the paper. An analysis of current information on the topic will help identify their list.

A balance sheet is a document that reflects the state of current accounts at the beginning of a certain period. In addition, the paper records the amount of funds remaining in the account at the end of the period, the amount of income and expenses. The following types of document are distinguished:

- monthly;

- annual.

- quarterly;

The balance sheet is one of the main accounting documents.

The paper reflects all the actions that were performed with the company’s funds for a certain period. The statement cannot be compiled arbitrarily.

Why is this document needed?

Such a document is appropriate for analytical work; when compiling it, only data from the necessary transactions, presented in a generalized form, is used. That is, such a statement is needed for systematization, as well as control of the correct reflection of the facts of economic activity on accounting accounts

. Based on the results of this document, a balance sheet of the enterprise is formed, referring to the corresponding account balances.

Accounting for data specifically on this statement is required if it is necessary to analyze indicators that cannot be calculated on the basis of aggregated data from the balance sheet or income statement.

Also, the analysis based on this document is relevant when it is necessary to keep records on any date, without waiting for the end of the reporting period. This advantage is especially relevant for management accounting.

Summing up the results of the reporting period, information about the origin of an account may be useful for an accountant in this register. An in-depth analysis of the financial condition of an organization, including an assessment of the structure and dynamics of indicators, makes it possible to track their qualitative changes, identify the causes and factors of these processes.

Formation of turnover sheet using MS Excel

The mechanism for compiling the balance sheet in the traditional way is carried out in several stages:

1. A group of objects is selected for which it is necessary to draw up a balance sheet.

2. For each element of this group, a selection of transactions within a certain period is made sequentially. In this case, receipt transactions are entered in the incoming column, disposal (issue) transactions are entered in the expense column. After this, the summation is made according to the columns “ Income ” and “ Expense ”.

3. Aggregated (summed) data for each element is written out in a separate table.

4. If there are no incoming balances, then you must complete steps 1-3 for the period - .

When changing the period, this sequence of operations must be performed again and again, which greatly increases the labor costs for drawing up this type of report. Thus, the process of preparing a balance sheet in the traditional way is an extremely labor-intensive task. Let's consider automating this process using MS Excel.

Automated information technology involves the use of special tools to perform data processing operations. The source of data for the balance sheet is a data set, implemented in the form of an Excel table and representing a transaction log. For example, on the sheet Sheet1 .

TRANSACTION LOG

From the specified source data on Sheet2 , you need to obtain a table of the form:

TURNOVER SHEET FOR THE MOVEMENT OF MATERIALS IN THE WAREHOUSE

from 03/15/2001 to 03/20/2001

Warehouse: WAREHOUSE No. 1

Product group: Miscellaneous

Moreover, this form should be automatically recalculated when the calculation period changes.

1. You need to create a form (create an Excel workbook and type a table) in accordance with the option on the sheet Sheet1 of the new Excel workbook.

2. It is necessary to name (assign names) the ranges of cells in all columns of the table containing any information:

— select a range of cell values of a certain column;

— Insert ® Name ® Assign... ® In the name field, enter a name (for example, NameItem ) ® Ok .

— Hotkey for assigning names to cells: Ctrl+F3 .

- Thus, we will receive the names NumberP , DataReg , NameItem , Unit , ReceiptQuantity , ExpenseQuantity

.

3. Go to Sheet2 and create a balance sheet form in accordance with the task.

4. Assign names to the cells in which the start date of the period and the end date of the reporting period are stored.

— Select the cell that contains the start date of the period;

— Ctrl + F3 ® Name: StartDate ® Ok .

— Select the cell that contains the end date of the period;

— Ctrl + F3 ® Name: ConData ® Ok .

Enter the following formula in the first line, after the header of the balance sheet in the column Balance at the beginning

=SUM((IF($B8= NameItem ;1,0)) * (IF( DateReg =StartDate,1,0)) * (IF( DateReg =StartDate,1,0)) * (IF( DateReg

4. The result of completing the task option should be saved under the name Full Name_Work No._Option No. (for example, “ IvanovNN_Work8 _Option1.xls ”) on the hard drive in the folder “ My Documents IT in Economics ” and on a floppy disk - in two copies (two copies of the same information in different folders on a floppy disk).

5. Presentation of the results of the work (report and files on a floppy disk) for verification by the teacher.

6. Defense of the completed work: answering test questions on the theoretical material of the lesson and responding to the teacher’s comments on the completed work.

7. Teacher’s assessment of completed work.

1. What is an array formula?

2. What are array formulas used for?

3. Describe the composition and procedure for using array formulas in calculations?

4. How to set curly braces that delimit an array formula.

5. Describe the mechanism that underlies array formula technology. What does an array formula do?

6. Why do you need to name cell ranges when using array formulas?

7. How can I create array formulas that use cell ranges in other Excel workbooks?

8. What is a balance sheet? Describe its purpose. Why do these types of calculations need to be done using array formulas?

9. Describe the procedure for performing the work. How should the work be formatted? How should the results of the work done be presented?

Prepayment for goods and services has been made:

Receipt of products to the warehouse:

It is required, using array processing technology, to determine the composition of receivables (we owe) and payables (we owe) to suppliers (for each organization) for the period and summarize them in the following table.

COMPOSITION OF RECEIVABLES AND ACCOUNTS PAYABLE

from "___" __________ 2001 according to "___" __________ 2001

The compiled form should be automatically recalculated when the calculation period and the composition of the source data change.

The background information is presented in the table below. Using array formula technology, create a balance sheet of quantitative accounting.

The background information is presented in the table below. Cells marked with a question mark need to be calculated (Qty * Price). It is required to use array formula technology based on the initial data to compose:

— balance sheet of quantitative accounting;

- a form for determining profit from sales (method for assessing inventories - “by average”).

RECEIPT AND SALE OF GOODS OJSC "Torgovlya+"

Practical use of hypertext technology to solve the problem of organizing document flow and effective access to information.

A document flow system is a system for organizing the movement of documents, the main purpose of which is to control the location of documents and their movement. Any document flow system is based on the registration of documents - recording the receipt, disposal, and movement of documents in special ledger books. The electronic document management system provides for recording the movement of documents in a database.

When registering documents, it is necessary to assign the document to any group:

— by the time the document was created (for a certain period);

— by document type (letters, orders, instructions, etc.);

— at the place of origin of the document (division, department, external organization);

- based on other characteristics (performer, structural unit, additional information).

Large flows of information in the form of various kinds of documents (letters, orders, instructions, contracts, instructions, reports, business plans, proposals, technical documentation, various calculations, price lists, etc.) pass through modern organizations every day. The number of electronic documents is constantly growing and today accounts for at least 50% of all documents. This is explained by the widespread introduction of information technologies into various spheres of society.

Under these conditions, it is extremely important to quickly navigate information flows: quickly find and process any information.

Often, a lot depends on how quickly a particular document is found and processed.

Traditionally, the issue of organizing electronic document management in most enterprises is limited, at best, to scattering documents in folders. Needless to say, the contents of the directory, for example, “ c:My DocumentsLetters” with 150 files, is extremely uninformative: in order to find a specific letter on a specific topic after some time, you will need to look through this entire list.

Let's complicate the situation . Let's assume that there are several secretaries in an organization. In this case, finding some document from six months ago becomes a problem. We often see how some organization feverishly spends hours searching for the required document and often never finds it. In modern conditions, this must be done in a few seconds.

Attention! To complete the work of this lesson, you need to create a document registration file of the established form on the server in a network folder and register documents from different machines in the computer class.

Registering a document means the process of creating a separate record (line) in an Excel spreadsheet file, indicating all the necessary details of the document. The specified document details later become criteria for searching a document in the information base as the number of registered documents increases. Therefore, it is strictly necessary to fill in all details.

Example of a registration table based on MS Excel:

Users of the turnover sheet for account 51

Accountants rarely use such a list in their work. In most cases, a turnover is required to disclose specific transactions for the required transaction. If money is received from the buyer, then the amount is reflected in the journal of settlements with customers. There, work is already underway on the generation of primary documents: invoice, delivery note or act.

The financier works with a statement and a detailed list of transactions by counterparties. In particular, when planning expenses and assessing income for the required period. Credit organizations also analyze cash flow movements if an application for lending or leasing is received.

Why do we need turnover sheets for synthetic and analytical accounts?

Turnover balance sheets are a way of summarizing accounting information on the operating accounts of an enterprise, and more specifically those for which business operations were carried out. Compilation of the register is possible for any time period: from one month to a year. The table consists of indicators of the opening balance, turnover and values of the closing balance, as well as total amounts. The breakdown is given in terms of debit and credit.

The turnover sheet for synthetic accounting accounts is a single set of data in the context of synthetic accounting accounts. The correctness of filling out the table is checked by observing the following pairs of equalities:

- Incoming Debit Balance = Incoming Credit Balance.

- Debit turnover = Credit turnover.

- Outgoing Debit Balance = Outgoing Credit Balance.

The equality of balances and turnover is explained by the capabilities of accounting, that is, the practical implementation of double entry and the principle of correspondence in accounting - the amount of property (asset) is equal to the amount of the source (liability). If the above equalities are not observed, it means that inaccuracies/errors were made during the formation of the “turnover”, which require appropriate correction of the data.

The turnover sheet for analytical accounting accounts is a single set of data in the context of analytical accounting for verification, adjustment, information analysis, and control. They are divided into calculated, using monetary meters, and material, using natural meters. An example of the former is the “revolutions” on, 76, count; second - on , 04, , count. The balance sheet for analytical accounts is compiled to analyze the receipt and disposal of assets, manage settlements with partners (suppliers), accountants, contractors or clients. Unlike “turnovers” for synthetic accounting accounts, analytical tabular statements may not have internal equalities, but must coincide with the accounting account considered in detail.