The concept of revenue in accounting

Based on PBU 9/99 “Income of the organization”, revenue in accounting can be recognized only if: (click to expand)

- the enterprise has the right to receive this revenue, that is, this right must be confirmed either by a concluded agreement or in another way;

- the amount of revenue can be determined;

- after receiving the proceeds, the organization will receive economic benefits;

- the goods have been transferred to the buyer, or the service has been provided (work accepted);

- It is possible to determine the expenses that an organization incurred to obtain specific revenue.

Revenue recognition

As a general rule, revenue from the sale of goods is recognized in accounting only if the following conditions are met:

- the organization has the right to receive this revenue, which is confirmed by an agreement or other document;

- the amount of revenue can be determined;

- the organization has received payment for the goods or there is no uncertainty regarding receipt of payment (there is confidence that as a result of this transaction there will be an increase in economic benefits). For example, an organization has documents (agreement, invoice, letter of guarantee, receipt, etc.) on the basis of which it can demand payment for the goods;

- ownership of the goods has passed to the buyer;

- the expenses that have been or will be incurred in connection with this operation can be determined.

If at least one of the listed conditions is not met, recognize in accounting not revenue, but accounts payable. An advance received on account of future deliveries is also not considered revenue (clause 3 of PBU 9/99).

Such rules are established by paragraphs 3 and 12 of PBU 9/99.

For organizations that have the right to conduct accounting in a simplified form, a special procedure for accounting for income is provided (Parts 4, 5, Article 6 of the Law of December 6, 2011 No. 402-FZ).

Situation: how to determine the moment of transfer of ownership when selling purchased goods (own products)?

In general, ownership of the goods (own products) passes to the buyer at the time of transfer. However, the law or contract may provide for another moment of transfer of ownership. Such rules are established in paragraph 1 of Article 223 of the Civil Code of the Russian Federation.

The moment of transfer of goods (own products) may be:

- the moment of delivery to the buyer (that is, the moment of actual receipt of the goods (own products) at the disposal of the buyer or the person indicated by him);

- delivery by the seller to the carrier (or to a communication organization);

- delivery of a bill of lading or other document of title.

Such rules are provided for in Article 224 of the Civil Code of the Russian Federation.

In addition, in some cases, legislation establishes specifics for determining the moment of transfer of ownership. For example, ownership passes:

- when selling real estate - at the time of state registration of the transfer of ownership (clause 2 of Article 223 and Article 551 of the Civil Code of the Russian Federation). For more information about at what point the real estate seller should reflect taxable income, see How to take into account income and expenses from the sale of depreciable property for income tax purposes;

- when concluding a rental-sale agreement - at the time of payment for the goods (Article 501 of the Civil Code of the Russian Federation);

- when concluding an exchange agreement - at the time the organization receives goods (products) under a commodity exchange transaction (Article 570 of the Civil Code of the Russian Federation).

Reflection of revenue in accounting

In order to reflect revenue in accounting, you need to rely on supporting documents. That is, on such documents that can confirm that the right to the goods has transferred to the buyer, for example, a deed or invoice, as well as other primary documents. There are a certain number of requirements for these primary documents. They, for example, must be drawn up either according to standard forms of accounting documentation, or according to a form approved by the organization.

The procedure for determining revenue, according to PBU 9/99, revenue is taken to be those amounts that are equal to receipts of money and property in monetary terms, as well as accounts receivable. At the same time, revenue is recognized in accounting taking into account VAT and excise duties, but they are not revenue.

In cases where the buyer does not fully pay his debt to the company, revenue should be recognized in the accounting of the supplier organization as the amount of payment received, as well as receivables from this buyer.

Revenue. Profit. Income. What is the difference

The table below examines the relationship between three related economic concepts ↓

| Revenue | Income | Profit |

| Cash received by the company from sales of its main activity | Revenue + cash from other operations | Income – expenses and losses |

| The effectiveness of core activities is assessed | The effectiveness of the company as a whole is assessed | Final effectiveness is assessed |

| Value is always > 0 | Value is always > 0 | Maybe <0 |

As you can see from the table, income differs from revenue in that it represents any positive financial result for a company. Regardless, it was obtained through the sale of goods/services, as the main source of cash flow to the company, or through additional actions.

Income can be received by a company from: the sale of part of its assets (real estate, machines, inventories, etc.), dividend payments (due to ownership of shares in other companies), rental payments (for premises, land, equipment), patents and intellectual property. , gratuitously received assets and expired accounts payable.

Income is a more comprehensive economic term than revenue, because includes not only money from the company's main activities. So, for example, if a company is engaged in leasing premises, then the funds received will be classified as revenue. Conversely, if a company is engaged in coal mining and received cash for the sale of its equipment, then this will be classified as other income.

Profit differs from income in that it includes accounting for expenses (costs). These include: fixed and variable costs. Revenue always takes a positive value, unlike profit.

Fixed costs are a class of enterprise expenses not related to production volume.

Variable costs are a class of enterprise expenses that depend on production volume.

The table below discusses which costs are classified as fixed and variable.

| Fixed costs | Variable costs |

| Costs for salaries of management personnel (salaries), rental of premises, machines, unified social tax, depreciation using the straight-line method, taxes on enterprise property, interest on obligations, marketing , see → Fixed costs. Formula. Example calculation in Excel | Costs of raw materials, fuel, materials, electricity, sales taxes, bonus part of the payment of working personnel, telephone use , see → Variable costs. Formula. Example calculation in Excel |

Methods of revenue recognition in accounting

There are two methods for recording revenue in accounting:

- Accrual method - is a generally accepted method, revenue is recorded as shipment;

- Cash method - revenue with this method is taken into account when payment is received.

The accrual method is used by all organizations to account for all revenue, with the exception of revenue under contracts with a special right to transfer ownership.

By the way, small businesses are given the right to choose; they can use both the accrual method and the cash method. This possibility is provided for in clause 20 of the Standard Accounting Recommendations. But when using the cash accrual method, the following requirement must be taken into account: expenses are recognized only after the debt is repaid.

The chosen method of revenue recognition is necessarily recorded in the accounting policies of the organization. The cash method is more convenient to use only for those small businesses that do not have many business transactions. Since, under the cash method, a company recognizes expenses only after they have been paid, then with a large number of such expenses, it is very difficult to track which of them are reflected in accounting and which are not yet.

When the cash method is used, costs that are related to the sale of products should be reflected in account 20 “Main production”.

IFRS, Dipifr

In 2014, the IASB approved a new revenue accounting standard, IFRS 15 “Revenue from Contracts with Customers”. This standard introduces the so-called “five-step” revenue recognition model. In other words, 5 specific actions must be taken to recognize revenue. To understand how this works, let's look at a simple example of accounting for revenue from the supply of equipment with service. This example was created by Dipifr examiner Paul Robins and submitted to the exam in December 2015.

Five-step revenue recognition model in IFRS

Step 1. Identify the contract

A contract is an agreement between two or more parties that creates enforceable rights and obligations. In some cases, IFRS 15 requires an entity to combine contracts and account for them as one contract. The standard also specifies accounting requirements for modifications to previously concluded contracts.

Step 2: Identify performance obligations.

A contract includes a promise to transfer goods or services. If the goods and services are distinct , these promises are performance obligations and must be accounted for separately.

Step 3. Determine the transaction price.

The transaction price is the amount of consideration under the contract that the company expects to receive for the goods or services transferred.

Step 4: Allocating the transaction price to the performance obligations.

Distribution occurs on the basis of stand alone prices for goods or services. If there is a discount, it can be allocated either to all obligations proportionately, or only to some obligations.

Step 5: Revenue Recognition

Revenue must be recognized either at a specific point in time or as the company satisfies its performance obligations.

Let's consider the application of this model using the example of revenue recognition for the supply of equipment with service. I have made small additions to the condition in bold italics.

Example 1. Sale of equipment with service.

annually prepares financial statements as of September 30.

On September 1, 2015, Kappa sold (and transferred) equipment (machine) . Kappa also agreed to service the equipment for a two-year period beginning September 1, 2015, at no additional charge. The total amount payable by the buyer for this transaction has been agreed upon as follows:

- $800 thousand if the buyer pays by December 31, 2015.

- $810 thousand if the buyer pays by January 31, 2016.

- $820 thousand if the buyer pays by February 28, 2016.

Kappa management believes that it is highly likely that the buyer will make payment under the contract in January 2021. If the equipment were sold separately without maintenance, then its price would be equal to 700 thousand dollars. For servicing the equipment for two years (without delivery), Kappa would have received compensation in the amount of $140,000. The alternative amounts receivable ($800,000, $810,000, $820,000) should be treated as variable consideration.

How should the revenue from this transaction be reported for the year ended September 30, 2015?

Step 1. Identify the contract

IFRS 15 sets out certain requirements for contracts that must be accounted for in accordance with the standard. This is done in order to filter out invalid or fictitious contracts that do not represent real transactions.

According to IFRS 15, clause 9, the contract is taken into account only if ALL conditions are met:

- 1) the contract has been approved, and each party undertakes to fulfill its obligations under the contract

- 2) the rights of the parties in relation to goods and services

- 3) payment terms

- 4) the contract must have commercial content

- 5) receipt of a refund is likely (the buyer is able and intends to pay a refund)

The requirement in paragraph 4 (clause 4) that the agreement has a commercial content is necessary to prevent artificially inflated revenue. Without this requirement, goods could be transferred back and forth.

Essentially, all of the above criteria require the seller to evaluate whether the contract is valid and represents a real transaction. Assessing the buyer's credit risk (clause 5) is also related to assessing the validity of the contract, since the transaction is real only if the buyer is able and intends to pay the promised remuneration. Companies tend to only enter into contracts where it is likely that they will receive consideration. And if not, then such an agreement will be a fictitious transaction.

The contract with the buyer must give rise to legally enforceable rights and obligations. A contract does not exist if each party has the right to terminate the contract unilaterally without fulfilling it and without paying compensation.

In this problem, we can assume that Kappa and the equipment buyer have entered into a contract for which all the criteria listed in IFRS 15 are met: the contract has a commercial substance, the terms of payment are defined, and Kappa is likely to receive reimbursement.

Step 2: Identify performance obligations.

The unit of account for revenue recognition is obligation . This term was implied in the old revenue standard, but there was no precise definition. I use the word obligation as a translation of the English word obligation, because this is the term contained in the Russian translation of IFRS 15. The word obligation can also be translated as obligation.

A performance obligation is a distinct good or service that the selling company promises to transfer to the buyer.

Essentially, the term "distinctive goods" means that a good can be separated from other goods: the seller supplies it separately, and the buyer can use (=benefit from) it separately from the seller's other goods. The same applies to services.

The standard says much more about this (standard clauses 27-30), but here for ease of explanation we will limit ourselves to this.

Goods and services that are not distinct are combined with other goods or services promised in the contract until a package of goods or services is obtained that is distinct. In some cases, this will cause the entity to account for all goods or services promised in the contract as one performance obligation.

In our example, Kappa has two responsibilities:

- provide equipment

- provide maintenance services.

This is a distinct product and service, since the buyer can benefit from the product or service separately, because the problem indicates the possibility of selling service by Kappa without supplying equipment (there is a separate price).

In IFRS 15 - transfer of control, in IFRS 18 - transfer of risks and benefits of ownership

Satisfying a performance obligation means transferring an asset (good or service) to the buyer. Goods and services are assets at the moment they are received and used (in the case of services, the asset exists for an instant - it is consumed immediately). An asset is transferred when (or as) the buyer obtains control of the asset.

Control over an asset is:

- 1) the ability to determine how the asset will be used

- 2) the ability to obtain substantially all of the remaining benefits from the asset.

- 3) the ability to prevent other parties from receiving benefits from the asset.

IMPORTANT: Under the new IFRS 15 standard, revenue is recognized when control is transferred from the seller to the buyer. In IFRS 18, revenue was recognized when the risks and rewards of ownership of the goods passed.

Why transfer control rather than risks and rewards as in the old revenue standard?

What is written in the Basis for Conclusions to IFRS 15 (Basis for Conclusions) BC.118 on this matter:

1) IFRS 15 defines revenue as income arising in the ordinary course of business of an entity. Revenue (see definition) arises from an increase in a contractual asset or a decrease in a contractual liability. And the current definition of an asset in the Conceptual Framework describes an asset as a resource controlled by a company. Therefore, it is methodologically more correct to associate an increase in assets with the transfer of control.

The definition of income in the standard is as follows:

Income* is an increase in economic benefits during the reporting period in the form of income or improvement in the quality of assets or a decrease in the amount of liabilities, which lead to an increase in equity capital not associated with contributions from capital participants.

2) Sometimes it can be difficult to determine the moment of transfer of risks and benefits if some of the risks and benefits remain with the seller (see point 3 of the list). Using the transfer of control criterion for revenue recognition in this case leads to more reasonable conclusions.

3) The risk-reward approach may conflict with the concept of performance obligations. If the product requires subsequent servicing by the seller, then part of the risks associated with the product remains with the seller. Based on the concept of transfer of risks and benefits, a company may conclude that it has only one performance obligation: selling the product along with service. In this case, revenue will be recognized only after all risks have been eliminated. When applying the concept of change of control, the seller will have two responsibilities identified: 1) delivery of goods and 2) provision of maintenance services. These performance obligations will be satisfied at different times and revenue will be recognized accordingly.

Step 3. Determine the transaction price.

The transaction price is the amount of consideration in exchange for the transfer of promised goods or services to the buyer.

In the simplest case, the amount of compensation is fixed and expressly stated in the contract, and this step is not difficult to complete. But, of course, in real life everything can be much more complicated. IFRS 15 discusses the following complications in detail:

- a) variable compensation;

- b) presence of a significant financing component in the contract

- c) non-monetary compensation;

- d) consideration payable to the buyer

In our case, we have variable compensation : the payment amount will be equal to 800,000, 810,000 or 820,000 dollars depending on the payment period.

Generally speaking, the amount of reimbursement may vary due to the provision of discounts, refunds, credits, price concessions, incentives, performance bonuses, penalties or other similar items. The promised consideration may also vary if the company's right to reimbursement depends on the occurrence or non-occurrence of a future event. For example, the amount of consideration will be variable if the product was sold with a right of return or if a fixed amount was promised as a performance bonus if a particular milestone was completed ahead of schedule.

Variable consideration must be assessed using one of two methods:

- expected value method is the expected compensation, weighted by the probability of possible values from the range.

- most likely amount method - the single most probable value of the expected compensation from the range of its possible values

To value variable consideration, a company should use the method that best predicts the amount to which the company will be entitled.

Important Note

The variable part of the reimbursement is included in the transaction price only in the amount that will not need to be reversed later (highly probable that a significant reversal of revenue will not occur) . That is, if the selling company is absolutely sure of the amount of compensation, this amount can be recognized as revenue. The remainder of the variable consideration can only be recognized once the uncertainty has been resolved.

Information from the problem statement allows you to use only the second method - the method of the most probable value. Because the:

“Kappa management believes that it is highly likely that the buyer will make payment under the contract in January 2021,”

then, in this case, the estimated recovery is $810,000. This is the amount agreed upon with the buyer according to the terms of the task for payment in January 2021.

Step 4: Allocating the transaction price to the performance obligations.

Distribution occurs on the basis of stand alone prices for goods or services. If there is a discount, it can be allocated either to all obligations proportionately, or only to some obligations.

Because Kappa has two performance obligations, it is necessary to determine how much of the $810,000 is attributable to each. To do this you need to create a proportion:

- 810 x 700/840 = 675 — revenue from equipment

- 810 x 140/840 = 135 - total revenue for services

| Duty to perform | Separate selling price | Allocation of transaction price to performance obligations | Share, % |

| Equipment | 700,000 | 675,000 | 83,333 |

| Service | 140,000 | 135,000 | 16,667 |

| Total | 840,000 | 810,000 | 100 |

Step 5: Revenue Recognition

Revenue must be recognized either over time or at a point in time. IFRS 15 defines the criteria for recognizing revenue over time. If none of the criteria are met, then revenue is recognized at a point in time (i.e. immediately).

The Company transfers control of a product or service and recognizes revenue during the period if ANY (ONE) of the following criteria is met:

- the buyer simultaneously receives and consumes benefits as the seller fulfills the performance obligation (an asset is a service);

- the seller creates or improves an asset (for example, work in progress), over which the buyer gains control as the asset is created or improved (a tangible asset);

- The seller's satisfaction of a performance obligation does not (a) create an asset that it can use for an alternative purpose (resell to another buyer), and ( b) the seller is entitled to receive payment for the portion of the contract work completed to date.

This topic is discussed in more detail in the article about construction contracts (differences between IFRS 11 and IFRS 15).

In our example, service revenue should be recognized over time because the first criterion listed is met. And the sale of equipment should be recognized immediately when control is transferred to the buyer.

Kappa recognizes all revenue from the sale of equipment on September 1, 2015, since control of the equipment was transferred on this date (the machine was delivered to the buyer's plant). The maintenance service is performed over a period of two years, 1/24 of this amount should be recognized at the reporting date.

Therefore, Kappa will make accounting entries:

At the time of transfer of control over the equipment:

- Dt Accounts receivable Kt Revenue (goods) - 675,000

- Dr Accounts receivable Kr Contractual obligation (service) - 135,000

On September 30, 2021, 1/24 of the service revenue will be recognized:

Dr Contractual obligation Kr Revenue - 5,625 (135,000/24 months = 5,625)

Extracts from Kappa's financial statements

Statement of financial position as at 30 September 2016

Accounts receivable - 810,000 Contractual obligation - 129,375 = 135,000 - 5,625

Statement of comprehensive income for the year ended 30 September 2021

Revenue from equipment sales - 675,000 Revenue from services - 5,625

This article is of an overview nature; IFRS 15 describes in much more detail many aspects of revenue accounting. The articles on this site are intended to arouse interest in an in-depth study of IFRS, but, of course, cannot replace a detailed independent analysis of the provisions of the standards. If you are building a career in international accounting standards, then, by and large, this requires reading the original texts of IFRS in English.

For more articles explaining the provisions of IFRS 15, please see the New IFRS 15 Revenue Standard section.

- 1. EPS indicator - calculation formula. Basic earnings per share

- 2. Exchange differences - examples of calculation and posting IFRS 21

- 3. Deposit capitalization - what is it? Interest capitalization formula: monthly, daily, continuous

- 4. Stock exchanges are places where stocks and other securities are traded.

- 5. IFRS what is it? Why do Russian accountants need them?

SPRING SALE!

Features that arise when determining revenue

- When the price is not determined. Sales of products, provision of services and other activities for which the company receives revenue occur on the basis of an agreement between the buyer and the customer. In this case, the contract, as a rule, provides for the establishment of a price. However, there are also contracts where the price is not provided and is determined based on the prices charged for similar types of goods. Revenue in this case is also determined by the price of similar goods.

- Transfer of ownership after receipt of funds. Revenue under this type of contract is determined on the date of receipt of money.

- When providing a commercial loan. When the buyer is granted a deferred payment, the proceeds are accepted in the full amount of the debt. The term of the so-called loan does not matter.

- When paying not in cash. The Civil Code of the Russian Federation allows the option of non-monetary payment only under an exchange agreement. Revenue under such contracts is taken into account at the cost of the goods that the organization receives. In this case, the cost of the goods is determined based on the cost of similar goods (works, services). When the cost of the goods received cannot be determined for some reason, the organization will determine revenue based on the cost of the goods transferred in exchange. The cost of your goods should be similar to the cost of usually shipped goods.

- When the obligation under the contract changes, when a discount is provided. There are situations when the price changes after the contract has been concluded. For example, it is possible to provide a discount. If the goods are transferred to the buyer already taking into account the discount, then there will be no need to adjust the revenue in this case. And if the discount is provided after the shipment has taken place and after the relevant documents have been issued, then the selling company will need to adjust the revenue by creating the posting: D62 K90-1 – REVERSE! Sales revenue is adjusted by the discount amount.

- When returning an item. If a situation arises when the buyer returns the goods, then an adjustment must be made in accounting for revenue, otherwise at the end of the period it will reflect an incorrect result. When the sale of goods and the return of goods occur in the same tax period, then it is necessary to adjust the 90 “Sales” account. But if the return occurs only next year, then the cost of this product will be reflected in non-operating expenses in the form of a loss from previous years and taken into account in account 91 “Other income and expenses.”

- When setting the price in USD There are also situations when settlement under an agreement occurs in rubles, but is equivalent to an amount in the currency of another country or in conventionally accepted units. In this case, the parties to the contract set the date for recalculating the price either from the foreign exchange rate at the time of payment or on the day of shipment. The peculiarity of such an agreement is that the final price is formed only after calculation. That is, the final cost of goods in Russian currency is determined at the time of final settlement and consists of partial payment for future deliveries, as well as other amounts transferred for the goods. The moment of determining revenue will be an earlier date, either the date of shipment or the moment of payment.

- When creating a reserve for doubtful debts. When creating a reserve for debts, the amount of revenue should not change.

Revenue recognition example

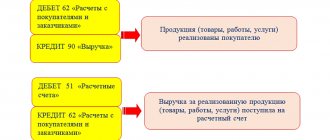

Continent LLC ships goods to the Counterparty on prepayment. On the date of transfer of the goods, ownership rights also pass. Revenue is accordingly recognized on the date of shipment. Let's reflect these transactions in accounting with the appropriate entries:

- D51 K62 – Prepayment received for future shipment

- D62 K68 – VAT accrued (as of the date the tax base was determined)

- D62 K90-1 – Products shipped

- D90-3 K68 – VAT charged

- D68 K62 – VAT calculated at the time of shipment is accepted for deduction

Revenue under the contract in foreign currency

If the agreement is concluded in a foreign currency, the procedure for determining the amount of revenue in accounting depends on whether the agreement provides for prepayment.

If an advance is not provided, determine revenue as follows:

| Revenue | = | Contract amount in foreign currency | × | Foreign currency exchange rate to the ruble on the date of revenue recognition |

If the contract provides for an advance form of payment, determine revenue using the following formula:

| Revenue | = | Advance amount in rubles | + | Contract amount in foreign currency | – | Advance amount in foreign currency | × | Foreign currency exchange rate to the ruble on the date of revenue recognition |

In this case, calculate the advance amount in rubles using the formula:

| Advance amount in rubles | = | Advance amount in foreign currency | × | Foreign currency exchange rate to the ruble on the date of acceptance of the advance for accounting |

This procedure follows from paragraphs 9 and 10 of PBU 3/2006.

An example of how revenue from the sale of goods is reflected in accounting, taking into account the advance received. The cost of the contract is expressed in foreign currency, payments are made in rubles

Torgovaya LLC entered into an agreement for the supply of goods in the amount of $5,500 (excluding VAT), payment is made in rubles at the official exchange rate of the Central Bank of the Russian Federation. The buyer made an advance payment of the equivalent of $2,500 on January 21, and shipment and full payment were made on February 20.

The US dollar exchange rate (notional) was: – on the day of receiving the advance (January 21) – 29.7 rubles/USD; – on the day of shipment and full payment (February 20) – 29.8 rubles/USD.

The organization's accountant made the following entries in the accounting records.

January 21:

Debit 51 Credit 62 – 74,250 rub. (2500 USD × 29.7 rubles/USD) – prepayment received.

On February 20, the day the goods were shipped, the accountant determined the amount of the buyer’s remaining obligations to the organization: 5500 USD – 2500 USD = 3000 USD.

Unpaid revenue is determined at the exchange rate on the date of final payment, that is, on February 20:

Debit 51 Credit 62 – 89,400 rub. (3000 USD × 29.8 rubles/USD) – final payment for the goods has been received.

The total amount of revenue will be: RUB 74,250. + 89,400 rub. = 163,650 rub.

Debit 62 Credit 90-1 – 163,650 rubles. – revenue from the sale of goods is reflected.

Revenue under the contract in conventional units

The amount of revenue depends on the procedure for determining the exchange rate of a conventional unit. If conventional units are strictly tied to the ruble (for example, one conventional unit is equal to 30 rubles regardless of changes in the official exchange rate), determine revenue using the formula:

| Revenue = Contract amount in conventional units × Value 1 cu. e. in rubles |

The exchange rate of a conventional unit can be tied to the foreign exchange rate, taking into account interest. Then the revenue will be equal to:

| Revenue | = | Contract amount in conventional units | × | Foreign currency exchange rate to the ruble on the date of revenue recognition | + | Percent |

If an advance payment is received under a contract whose value is expressed in conventional units, use the formulas provided for calculating revenue under a contract concluded in foreign currency. In this case, in your calculations, use the foreign currency exchange rate to the ruble, taking into account interest.

In all of these cases (both under an agreement expressed in foreign currency and under an agreement expressed in conventional units), the foreign currency exchange rate to the ruble is equal to the official exchange rate of the Central Bank of the Russian Federation on the date the transaction is reflected. However, the parties may, in an agreement expressed in conventional units, provide for a different rate (independent of changes in the official rate of the Central Bank of the Russian Federation). Then determine revenue in accounting taking into account this rate. This follows from paragraph 5 of PBU 3/2006.

If an organization carries out a large number of similar transactions in foreign currency, then it is possible to establish an average rate that will be used by the organization in accounting for a month or a shorter period. This is possible only if the official exchange rate of foreign currency to the ruble changes insignificantly. Such rules are specified in paragraph 6 of PBU 3/2006.

To establish an average exchange rate in an organization, write in the accounting policy for accounting purposes:

– which operations can be considered homogeneous (for example, recalculation of revenue under contracts whose value is determined in foreign currency);

– what is considered a minor change in the official exchange rate of the Central Bank of the Russian Federation (for example, within 1%);

– what document will set the average rate (for example, by order of the manager).

It is possible to include such conditions in the accounting policy, since PBU 3/2006 does not indicate in which specific cases the average rate is applied and what is considered an insignificant change in the official rate (clause 7 of PBU 1/2008).

This procedure is established in paragraphs 4–6 of PBU 3/2006.

Situation: when do exchange rate differences arise in accounting when selling goods?

Exchange rate differences in accounting arise in two cases:

- if the value of the contract is expressed in foreign currency and payment for it is received in foreign currency (differences arise when recalculating accounts receivable);

- if the value of the contract is expressed in foreign currency or conventional units linked to foreign currency, and payment for it is received in rubles. In accounting, the concept of “total differences” does not exist. However, in practice, when making payments under contracts expressed in foreign currency or conventional units linked to foreign currency, discrepancies arise between the ruble valuation of products (work, services) on the date of shipment and on the date of payment. Since the nature of the occurrence of such discrepancies is similar to the nature of exchange rate differences, a single procedure for their reflection is used in accounting: as part of other income or expenses (clause 7 of PBU 9/99, clause 11 of PBU 10/99).

Whether or not exchange differences arise when accounting for a specific business transaction for the sale of goods depends on the terms of the contract. Exchange differences arise if the buyer pays for the goods after shipment (transfer) and ownership of the goods passes on the date of shipment.

In this case, the exchange rate difference is formed at the time of payment for the goods: positive (if the ruble valuation of the debt on the date of shipment (transfer) is lower than on the date of payment), or negative (if the ruble valuation of the debt on the date of shipment (transfer) is higher than on the date of payment ).

Also, the exchange rate difference is formed on the reporting date (the last day of the month) when recalculating the liability if the payment and shipment dates fall on different months (clause 3 of PBU 3/2006).

The exchange rate difference is taken into account as part of other income or expenses on account 91 “Other income and expenses” (Instructions for the chart of accounts).

If the buyer makes an advance payment under the contract, no exchange rate difference arises (clauses 7, 9 of PBU 3/2006).

An example of the occurrence and reflection in accounting of exchange rate differences arising from the sale of goods. The cost of the contract is expressed in foreign currency, payments are made in rubles

Torgovaya LLC entered into a supply agreement. Hermes must deliver the goods on January 21, and the buyer pays for the goods on February 20. The contract amount is USD 5,000, payment is made in rubles at the official exchange rate of the Central Bank of the Russian Federation on the date of payment for the goods. Title passes to the buyer upon shipment.

The US dollar exchange rate (conditional) is: – January 21 – 29.7 rubles/USD; – January 31 – 29.6 rubles/USD; – February 20 – 29.8 rubles/USD.

The organization's accountant made the following entries in the accounting records.

January 21:

Debit 62 Credit 90-1 – 148,500 rub. (5000 USD × 29.7 rubles/USD) – revenue from the sale of goods is reflected.

January 31:

Debit 91-2 Credit 62 – 500 rub. – (5000 USD × (29.7 rubles/USD – 29.6 rubles/USD)) – reflects a negative exchange rate difference.

February 20th:

Debit 51 Credit 62 – 149,000 rub. (5000 USD × 29.8 rubles/USD) – payment for the goods has been received;

Debit 62 Credit 91-1 – 1000 rub. (5000 USD × (29.8 rubles/USD – 29.6 rubles/USD)) – positive exchange rate difference is taken into account.

Situation: how to determine the amount of revenue when selling goods with deferred (installment) payment?

The procedure for determining revenue when selling goods on a deferred basis (in installments) depends on whether interest is accrued under the contract or not.

A purchase and sale agreement may provide for payment for goods on a deferred or installment basis (Article 488 of the Civil Code of the Russian Federation, Article 489 of the Civil Code of the Russian Federation). Such a condition will mean the provision of a commercial loan (Article 823 of the Civil Code of the Russian Federation). The agreement may establish that the buyer must pay interest for the provision of a deferment or installment plan (clause 14 of the resolution of the Plenum of the Supreme Arbitration Court of the Russian Federation No. 13, Plenum of the Supreme Arbitration Court of the Russian Federation No. 14 of October 8 1998).

Thus, there are three possible options for providing a deferred (installment) payment to the buyer:

– no interest accrual;

– the initial cost of goods increases by the amount of interest, that is, the procedure for determining the price of goods depends on the terms of settlement under the contract (clause 1 of Article 424 of the Civil Code of the Russian Federation). For example, if the buyer is given a deferred payment (installment plan), the price of the product increases by 10 percent;

– with interest accrued on the balance of the buyer’s debt.

If the agreement does not provide for the payment of interest, then in accounting the proceeds from the sale of goods will be determined in the general manner. Also determine revenue if, under the terms of the contract, the initial cost of goods increases by the amount of interest in accordance with the payment schedule. Recognize revenue in the full amount of receivables, taking into account the interest provided for in the agreement (clause 6.2 of PBU 9/99). In this case, all conditions for recognition of revenue in accounting established in paragraph 12 of PBU 9/99 will be met.

If the agreement specifies only the right for the organization to receive interest for providing a commercial loan with the condition that the exact amount of interest is determined monthly based on the unpaid amount, then the interest will be recognized as revenue at the end of each month. This is explained by the fact that the organization has the right to receive a certain amount of interest only after the end of the month (clause 12 of PBU 9/99).

An example of how revenue is reflected in accounting, taking into account interest received for providing a commercial loan when selling goods

LLC "Torgovaya" enters into contracts for the retail purchase and sale of cars. The initial payment is 20 percent, interest under the contract is 24 percent per annum on the amount of unpaid goods. The organization sold a car worth 354,000 rubles on April 1. (including VAT – 54,000 rubles). The initial payment was 70,800 rubles. (RUB 354,000 × 20%). According to the agreement, the buyer makes deferred payment monthly on the 1st for three months in equal installments. The agreement does not provide for the possibility of recalculating interest in case of early repayment of debt.

The table shows the percentage calculation:

| date of payment | The amount of the opening balance as of the date of payment, rub. | Payment amount, rub. | Interest accrual | Total payment amount, rub. | ||

| During the period | Number of days in the period | Amount of interest, rub. | ||||

| 1 | 2 | 3 | 4 | 5 | 6 | 7 |

| 1st of May | 283 200 (354 000 – 70 800) | 93,363 (283,200 : 91 days × 30 days) | April | 30 | 5586 (283,200 × 24%: 365 days × 30 days) | 98 949 (93 363 + 5586) |

| June 1st | 189 837 (283 200 – 93 363) | 96,475 (283,200 : 91 days × 31 days) | May | 31 | 3870 (189,837 × 24%: 365 days × 31 days) | 100 345 (96 475 + 3870) |

| July 1 | 93 362 (283 200 – 93 363 – 96 475) | 93 362 | June | 30 | 1842 (93,362 × 24%: 365 days × 30 days) | 95 204 (93 362 + 1842) |

| Total | 283 200 | 91 | 11 298 | 294 498 | ||

The organization's accountant made the following entries in the accounting records.

April 1:

Debit 50 Credit 62 – 70,800 rub. – the down payment for the car has been received;

Debit 62 Credit 90-1 – RUB 365,298. (RUB 354,000 + RUB 11,298) – revenue from the sale of a car is reflected, including interest;

Debit 90-3 Credit 68 subaccount “VAT calculations” – 55,723 rubles. (RUB 300,000 × 18% + RUB 11,298 × 18/118) – VAT is charged on revenue.

1st of May:

Debit 50 Credit 62 – 98,949 rub. - money has been received from the buyer.

June 1st:

Debit 50 Credit 62 – 100,345 rub. - money has been received from the buyer.

July 1:

Debit 50 Credit 62 – 95,204 rub. - money has been received from the buyer.

Answers to common questions

Question No. 1. “To recognize revenue for the sale of goods, is a contract sufficient, or are some other documents required?”

In order to recognize revenue in accounting, one contract is not enough. Since we are dealing with the sale of goods, in addition to the contract, a TORG-12 invoice must be issued.

Question No. 2. “The date of recognition of revenue and the date of recognition of the tax base are the same?” (click to expand)

No, the tax base can be determined on the day of shipment, and revenue recognized on the day of payment. These dates may be the same or different. In any case, the moment of recognition of the tax base and the moment of recognition of revenue must be fixed in the company's accounting policies.