Expenses for a business trip abroad differ from expenses for business trips within Russia. discuss how to correctly prepare an advance report for a business trip abroad with the 2020 sample in this consultation.

Also see:

- Nuances of organizing and processing a business trip

- How to arrange a business trip correctly

What you need to know about the trip report

Upon returning from a business trip, including a foreign one, the employee is obliged to report on it and submit an advance report to the accounting department.

The form of the advance report can be approved by the local act of the company. Or, the old-fashioned way, they use a report in form AO-1.

Regardless of the form, you must comply with the deadline for submitting the report - 3 business days after the end of the business trip.

The employee attaches all documents confirming expenses to the advance report for a business trip abroad. Namely:

- travel tickets and boarding passes (if tickets are electronic, you need to print them);

- receipts for the use of bed linen;

- hotel invoices and receipts (residential rental agreement), receipts;

- receipts of fees (agent's commission for purchasing a ticket, receipt for baggage transportation, etc.);

- documents confirming payment of visa or consular fees;

- other supporting documents.

ADVICE

For the convenience of preparing and conducting an advance report, supporting documents can be pasted onto blank A4 sheets with a field for filing documents on the left.

If the employer purchases tickets and books a hotel through an agency or directly from the contractor, documents for travel and accommodation (boarding pass or voucher, hotel bill or certificate of accommodation) must be attached to the report.

We take into account travel expenses

how the main business trip expenses are recognized for tax purposes .

| Type of expenses | Income tax | Personal income tax | Insurance contributions to the Pension Fund, Social Insurance Fund, Compulsory Compulsory Medical Insurance and Compulsory Compulsory Compulsory Medical Insurance | |

| Daily allowance in the amounts provided for by local regulations or collective agreement | Fully included in expenses | Not withheld from amounts not exceeding: (or) 700 rubles. per day - for business trips around Russia; (or) 2500 rub. per day - for business trips abroad. If the daily allowance was paid in a larger amount, then the excess amounts are subject to personal income tax | Not credited | |

| Daily allowances for the day of arrival from a business trip abroad must be paid according to the norm established for business trips in Russia (in rubles). And even if the regulations on business trips adopted by your company state that daily allowances for the last day of a business trip are paid in the same amount as for all days of a business trip abroad (for example, 2,500 rubles), only 700 rubles will not be subject to personal income tax. If daily allowances were paid in foreign currency, then in order to compare the amount of daily allowances with the established ruble standard for the purpose of calculating personal income tax, you need to convert them into rubles at the official exchange rate in effect on the date of payment of daily allowances (and not on the date of approval of the advance report) | ||||

| Travel expenses: — to the place of business trip and back (including business class or in SV carriages); — to the airport, train station, pier (including by taxi) and back | Counted into expenses without restrictions | Doesn't hold | Not credited | |

| Expenses for renting residential premises - subject to availability of supporting documents | Counted into expenses without restrictions | The entire hotel payment amount is not deducted. If there are no supporting documents, then personal income tax is imposed on amounts in excess of: (or) 700 rubles. per day - for business trips around Russia; (or) 2500 rub. per day - for foreign business trips | Not credited. If there are no supporting documents, then the amount reimbursed to the employee is not subject to contributions within the limits established in the local regulations. If you have not established such standards, then urgently supplement your business travel regulations with a procedure for reimbursing employees for unconfirmed expenses in order to avoid paying contributions | |

| Expenses for service in bars, restaurants, in the room, as well as fees for the use of recreational and health facilities (for example, a fitness room, sauna, etc.) are not taken into account for profit tax purposes. | ||||

| Costs for processing and issuing visas, international passports, vouchers, invitations, etc. | Counted into expenses without restrictions | Doesn't hold | Not credited | |

| Payment for communication services | ||||

| Payment for services of VIP lounges (superior lounges) at airports | ||||

| You can justify the cost of paying for VIP rooms, for example, like this: service in the VIP room provides access to telephone and other types of communications, as well as access to the Internet, which allows a business trip employee to quickly solve production problems that require his participation | ||||

Currency conversion

Let's consider a situation where an employee received an advance payment for a business trip in rubles, and the expenses were incurred in foreign currency.

An employee can independently exchange rubles for foreign currency at an exchange office in the Russian Federation or while already on a business trip abroad. In this case, the rate is taken on the date the employee purchased the currency, if he attached a certificate from the exchange office to the advance report.

It often happens that an employee cannot confirm the fact of purchasing currency. For example, due to the loss of a certificate from the bank about the completed exchange. It may also be that when exchanging currency in another country, the exchange office did not issue the employee with a conversion document.

In this case, for recalculation, they take the official exchange rate of the Central Bank on the date of approval of the advance report by the head of the company. This position is confirmed by letters from the Federal Tax Service dated March 21, 2011 No. KE-4-3/4408 and the Ministry of Finance dated March 31, 2011 No. 03-03-06/1/193.

For an example of recalculating daily allowances issued in foreign currency, see our article “Taxes and contributions on daily allowances abroad: calculation examples.”

The advance was issued in the same foreign currency in which the expenses were paid

This is the simplest situation from the point of view of drawing up an expense report. In Form N AO-1, you only need to record the amounts in foreign currency from the documents and convert them into rubles. We have already discussed above at what rate this should be done. Let's consider an example when an organization determines the ruble amount of travel expenses paid in advance at the exchange rate on the date the advance was issued.

Example. Filling out a report on a foreign business trip, when the accountable amount is issued and spent in euros

Condition

LLC "Major" sends deputy director S.I. Zvezdochkin. on a business trip to conduct negotiations with a French company. The duration of the business trip is from 09/02/2010 to 09/14/2010. The travel tickets were purchased by the organization by bank transfer.

The organization established daily allowance rates at LLC Major, including for foreign business trips, in rubles (so as not to exceed the standard not subject to personal income tax).

The daily allowance standard for France is 2100 rubles. per day.

The daily allowance standard for Russia is 500 rubles. per day.

From the cash register of LLC "Major" to Deputy Director S.I. Zvezdochkin. 09/01/2010 2,000 euros (to pay cash expenses) and 25,700 rubles were issued for travel expenses. (daily allowance). The Central Bank exchange rate as of September 1, 2010 is 39.01 rubles/euro.

09/14/2010 Zvezdochkin paid for hotel services in the amount of 2340 euros.

He prepared the advance report on 09/15/2010. On the same day, the director approved it.

The Central Bank exchange rate as of September 15, 2010 is 39.53 rubles/euro.

And on the same day, the employee was given 340 euros from the cash register (as repayment of overexpenditure).

Solution

Amount of expenses in rubles (per diem) - 25,700 rubles:

— for days spent in France — 25,200 rubles. (2100 rub. x 12 days);

— for business trip days spent in Russia — 500 rubles. (1 day - day of arrival in Russia from France - 09/14/2010).

The total amount of travel expenses in foreign currency is 2340 euros. This amount is more than the advance payment given to the employee.

Part of the amount of travel expenses within the limits of the advance payment issued (2000 euros) must be converted into rubles at the exchange rate on the date of issue of the advance payment (as of 09/01/2010 - 39.01 rubles/euro). And the remaining part (340 euros) must be converted into rubles at the Central Bank exchange rate on the date of approval of the advance report (39.53 rubles/euro).

As a result, the amount of foreign currency travel expenses in rubles will be 91,460.20 rubles.

(EUR 2,000 x RUB 39.01/EUR + EUR 340 x RUB 39.53/EUR).

The following entries will be made in accounting.

| Contents of operation | Dt | CT | Sum |

| On the date of advance payment (09/01/2010) | |||

| Currency issued from the cash register for travel expenses (2000 euros x 39.01 rubles/euro) | 71 “Settlements with accountable persons” | 50, subaccount 2 “Cashier in euros” | 78 020,00 |

| Rubles issued from the cash register as daily allowance | 71 “Settlements with accountable persons” | 50, subaccount 1 “Cashier in rubles” | 25 700,00 |

| As of the date of approval of the advance report (09/15/2010) | |||

| Travel expenses reflected (RUB 78,020 + EUR 340 x RUB 39.53/EUR) | 26 “General business expenses” | 71 “Settlements with accountable persons” | 91 460,20 |

| Daily allowances reflected | 26 “General business expenses” | 71 “Settlements with accountable persons” | 25 700,00 |

| There is no need to withhold personal income tax from daily allowances, since they do not exceed non-taxable norms (2100 rubles/day < standard 2500 rubles/day, 500 rubles/day < standard 700 rubles/day). Daily allowances are also not subject to insurance premiums. | |||

| The issue of overexpenditure to the employee in euros is reflected (340 euros x 39.53 rubles/euro) | 50, subaccount 2 “Cashier in euros” | 71 “Settlements with accountable persons” | 13 440,20 |

Reverse side of form N AO-1

| Number in order | Document confirming production costs | Name of document (expense) | Expense amount | Debit account, sub-account | ||||

| according to the report | accepted for accounting | |||||||

| date | number | in rub. cop. | in currency (in euros) | in rub. cop. | in foreign currency | |||

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 |

| 1 | 14.09.2010 | 85646 | hotel bill | 91 460,20 | 2 340 | 91 460,20 | 2 340 | 26 |

| 2 | 15.09.2010 | a/o N 63 | per diem abroad | 25 200,00 | 25 200,00 | 26 | ||

| 3 | 15.09.2010 | a/o N 63 | daily allowance Russian. | 500,00 | 500,00 | 26 | ||

| Total: | 117 160,20 | 2 340 | 117 160,20 | 2 340 | ||||

Advance report

You can see how to correctly fill out an advance report for a foreign business trip here:

As a general rule, the employee must independently fill out the advance report.

In the advance report, it is important to indicate all expenses incurred by the employee during a business trip abroad.

If an employee has incurred any expenses that are not provided for in the company’s organizational and administrative document, it is necessary to attach to the report a memo with a positive resolution from the manager.

On a business trip abroad, unexpected expenses may arise - taxis, dry cleaning, expenses for cellular communications or the Internet, buying a laptop, etc., etc. Each situation must be considered separately.

You can learn about the specifics of work while constantly on business trips abroad from our article “Work related to business trips abroad: what you need to know.”

Currency advance report if a corporate card is issued

The expense report has two tasks: to make payments to the employee and to reflect travel expenses in accounting. However, to perform each of these tasks, different currency translation rules are applied. These rules depend, among other things, on the method of issuing and the currency of the advance, the currency of the established amounts of travel expenses and the currency of the actual expenses incurred.

Transferring an advance payment to a corporate card is gaining popularity: firstly, non-cash payments are convenient, and secondly, with regard to hiring expenses, you can focus on the actual expenses of the employee without complying with a number of restrictions of Regulation No. 176.

Let’s figure out how to correctly make currency conversions using this method of issuing an advance, and also, for convenience, implement them in the advance report form. As a result, we will offer an optimal example of filling out an advance report with step-by-step explanations.

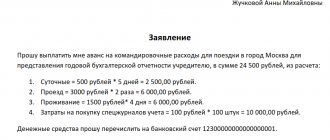

Situation. The production organization Zlato LLC (Gomel) sends Deputy Director Ivan Aleksandrovich Chikunov on a business trip regarding the conclusion of an agreement for the supply of raw materials (order No. 154 of 09.09.2019).

Place of business trip: Moscow. The duration of the business trip is from September 10, 2019 to September 13, 2019 (for 4 days). The start and end dates of the business trip are the dates of arrival in Moscow and departure from it, respectively.

Air travel to and from the place of business trip is paid for by the organization in a non-cash manner.

To provide the employee with an advance payment, a corporate card was issued to the organization’s account in US dollars, to which USD 680 was credited.

The employee returned from a business trip on September 13, 2019. The advance report was submitted on September 16, 2019. Attached to it is the invoice of the Orion Hotel N 1196/7 dated 09/13/2019 (check-in - 09/10/2019, check-out - 09/13/2019) in the amount of 18,535 Russian. rub.

The bank statement for the account to which the specified corporate card was issued contains the following information:

- cash withdrawal:

transaction 09/10/2019 - 7500 Russian. rub.;

debit from the account on September 12, 2019 - 120.04 US dollars (at the exchange rate - 62.4766 Russian rubles per 1 US dollar (conditionally));

— payment of the hotel bill for accommodation:

transaction 09.13.2019 — 18535 RUR. rub.;

debit from the account on September 16, 2019 - 297.15 US dollars (at the exchange rate - 62.3753 Russian rubles per 1 US dollar (conditionally)).

For settlements with employees, the organization uses the rate established by the international payment system on the date of each transaction - the exchange rate.

Official exchange rate of the Belarusian ruble:

— as of September 12, 2019 — RUB 2.0845. for $1;

— as of September 16, 2019 — 2.0511 rub. for 1 US dollar.

Algorithm for filling out an advance report

For the purposes of SETTLEMENTS WITH THE EMPLOYEE

Step 1. Reflection of travel expenses subject to reimbursement in the CURRENCY OF OPERATIONS COMPLETED.

Expenses subject to reimbursement on the basis of supporting documents are reflected in the advance report in the currency of these documents <*>. Daily allowances do not require the submission of such documents <*>, so it is logical to reflect them in the currency of the established amounts (hereinafter referred to as the currency of the norms).

When issuing a corporate card to an employee, hiring expenses are reflected in actual amounts based on supporting documents, and not in the amounts established by Appendix 2 to Regulation No. 176 <*>.

In our case, the following are subject to compensation:

- daily allowance - 120 US dollars (30 US dollars x 4 days);

— hiring costs — 18535 Russian. rub.

Expenses for air travel to the place of business trip and back are not reflected to the employee, since they were paid by the organization by bank transfer <*>.

Step 2. Recalculation of travel expenses reflected in the advance report into the ADVANCE CURRENCY.

Since daily allowances are initially reflected in the standard currency, which corresponds to the currency of the advance (the currency of the account for which the corporate card was issued), there is no need to recalculate them <*>.

Hiring expenses were incurred in Russia. rubles, and the advance currency is US dollars, so they need to be recalculated. When recalculating, the following may be used as a conversion rate <*>:

— exchange rate on the date of each transaction;

— National Bank exchange rate on the date of the advance report.

Since on the date of the report (as of September 16, 2019) the organization has an account statement for which the corporate card was issued, and it contains the necessary information, the exchange rate can be used for recalculation.

Accordingly, the amount of hiring costs, recalculated into the advance currency, will be 297.15 US dollars (18,535 Russian rubles / 62.3753).

The amount of travel expenses in the advance currency will be USD 417.15 (USD 120 + USD 297.15).

Step 3. Determination of DEBT according to the advance report.

When issuing a corporate card to an employee with credited funds, the actual transfer of these amounts does not occur, since these funds remain in the organization’s account until they are written off. Accordingly, funds are considered received on account as they are debited from the account, that is, they are recognized as an advance issued on the dates of their debit from the account.

In this situation, the amount of the advance received by the employee will be $417.19 ($120.04 + $297.15).

The difference between the advance amount and the travel reimbursement amount is $0.04 ($417.19 - $417.15). This employee debt is reflected in the advance report in the following currency:

For reference, the employee must repay the debt within 15 working days from the date of return from a business trip, excluding the day of arrival, in our case - no later than 10/04/2019 <*>. In this case, the employee’s return of 0.04 US dollars (an amount less than the established denomination of the US dollar banknote) is made in Belarusian rubles at the official rate to the corresponding foreign currency on the date of preparation of the advance report <*>. On the date of repayment, the employee’s debt for the advance payment is subject to revaluation <*>. Exchange differences arising when revaluing debt are reflected in account 91 “Other income and expenses” as part of income (expenses) for financial activities <*>.

For COST ACCOUNTING purposes

Step 4. Conversion of travel expenses reflected in the advance currency into BELARUSIAN rubles <*>.