What is a penalty as an accounting object?

A penalty is a penalty determined by law or contract for failure to fulfill obligations by one party to the agreement to the other (others). From an accounting point of view, it is legitimate to consider a penalty:

- other income of the receiving party (clause 7 of PBU 9/99);

- other expenses of the obligated party (clause 11 of PBU 10/99).

Penalties as income are reflected in accounting in the reporting period in which the title documents on the basis of which the penalty was formed appeared. Such a document could be, for example, a court decision or a bilateral act of the parties to the agreement (clause 16 of PBU 9/99). The penalty as income or expense must be reflected in the balance sheet before the actual settlements of the parties (clause 76 of the regulations by order of the Ministry of Finance of Russia dated July 29, 1998 No. 34n).

The main accounting account for generating entries for penalties is 76. Let's study how it and its subaccounts are used to reflect transactions related to the payment of a penalty by a business entity (or its receipt of corresponding income from a counterparty).

Accounting records for court decisions

Rubric “Questions and Answers” Question No. 1.

Are the costs of obtaining legal assistance or paying a specialist compensation when using a full-time lawyer in court proceedings? The salary of a full-time lawyer when participating in the process does not relate to legal costs and is not a compensable expense.

Receiving compensation by the winning party is possible when concluding a civil contract with a lawyer. The job description of a lawyer does not indicate the obligation to represent interests in court. Question No. 2.

Is it possible to challenge the amount of expenses imposed on the debtor's manager during bankruptcy? It is possible, provided that they are clearly disproportional – the amount exceeds the value of the debtor’s property available to cover expenses. The debtor has the right to submit an application to the judicial authority that controls the procedure. Question No. 3.

Accounting for legal expenses in accounting

Punitive damages awarded or admitted have been paid. Payment order (0401060), Bank statement on current account. 76-2 51, 76 The amount of the claim was paid to suppliers and contractors, including offsetting mutual counterclaims.

Payment order (0401060), Bank statement on the current account, Certificate of offset of counter mutual claims. 91-2 76 Penalties payable to the bailiff service are reflected. Decision to award punitive damages, Accounting certificate (0504833).

76 51 Paid expenses associated with enforcement proceedings. Payment order (0401060), Bank statement on current account. 79-2 76-2 Settlements on claims have been transferred to separate divisions.

Advice 76-2 79-2 Reflects settlements of claims submitted by separate divisions.

Accounting for legal costs and penalties

Covering expenses is carried out at the expense of the debtor and is not compensated by third parties.

Expenses subject to judicial approval include:

- Manager's remuneration.

- Payment for current activities in the form of postal, office, and transportation expenses.

- Amounts required for publication of notifications about the start of the procedure in the Bulletin.

- Funds spent on holding public auctions of the debtor's property.

- Payments for the services of appraisers, auditors, experts and others.

When determining the amount of expenses, the validity of the expenses, reasonable amount and proportionality to the result are taken into account.

Accounting entries for court decisions

When covering expenses, several repayment options arise.

Procedure Compensation of expenses The fee is paid by the plaintiff, the application is not submitted to the court Refund is carried out by the territorial branch of the Federal Tax Service before the expiration of 3 years The fee is paid, the claim is satisfied in pre-trial order The amount of fees and costs in some cases is returned in a separate claim Claims are partially satisfied Expenses incurred by the plaintiff , are partially compensated, in terms of recognition of the claim or at the discretion of the court. The defendant has no obligation to pay the state duty. Only costs are subject to compensation; the amount of the state duty to the plaintiff is not covered. Expenses incurred by the plaintiff in the course of pre-trial consideration of claims are not covered. Expenses often include costs for the services of lawyers. The courts do not recognize such expenses and do not attribute them to the losing party.

Accounting entries for accounting for settlements of claims

PBU 10/99 compensation for losses caused by the organization is accepted for accounting in amounts awarded by the court or recognized by the organization. Moreover, in accordance with paragraph.

18 PBU 10/99 expenses are recognized in the reporting period in which they occurred, regardless of the time of actual payment of funds and other form of implementation (assuming the temporary certainty of the facts of economic activity). Therefore, the necessary entries in accounting must be reflected as of the date entry into force of the court decision: Debit 91, subaccount “Other expenses” Credit 76, subaccount “Settlements on claims” - 1,393,203.52 rubles. - an expense is recognized in the form of overdue rent. As the debt is repaid, the following entry will need to be made in the accounting: Debit 76, subaccount “Settlements of claims” Credit 51-100,000 rubles. — the amount was transferred (partially) to pay off the debt.

How are fines (penalties) paid by the obligated party to the contract reflected in accounting?

The party to the contract, which is obliged to compensate the counterparty for losses by paying a penalty, will generate the following entries:

- Dt 91.2 Kt 76 (the penalty was recognized on the basis of a title document);

- Dt 76 Kt 51 (the penalty is transferred within the time limits specified by law or contract).

If the penalty is paid to an individual in cash, this will be reflected by the posting: Dt 76 Kt 50.

In cases provided for by law, when making settlements with an individual, not only the penalties paid - fines (penalties) are reflected in the accounting records, but also the taxes and contributions accrued on them.

So, if the recipient of the penalty is an individual who is not registered as an individual entrepreneur, then the following correspondence may additionally be drawn up:

- When the penalty arose within the framework of legal relations under an agreement, payments under which are subject to insurance premiums (for example, under a civil process agreement for the performance of work by an individual):

- Dt 76 Kt 68 (personal income tax charged for a penalty);

- Dt 68 Kt 51 (NDFL paid);

- Dt 91.2 Kt 69 (contributions are calculated for the amount of the penalty - pension and medical, in accordance with subparagraph 1, paragraph 1, article 420 of the Tax Code of the Russian Federation);

- Dt 69 Kt 51 (dues paid).

- When the penalty arose within the framework of other legal relations:

- Dt 76 Kt 68 (personal income tax charged);

- Dt 68 Kt 51 (NDFL paid).

An example of such a penalty is compensation to an individual under a shared construction agreement (letter of the Ministry of Finance of Russia dated September 15, 2017 No. 03-04-06/59629). Contributions for this type of penalty are not charged.

In both of these cases, personal income tax must be paid no later than the next day after the calculations are made (clause 6 of Article 226 of the Tax Code of the Russian Federation). Contributions, if any, are made, as usual, by the 15th day of the month following the date in which the payments were made.

Accounting for penalties in accounting

In accordance with the Chart of Accounts (Order of the Ministry of Finance dated October 31, 2000 No. 94n), the amounts of tax penalties due are reflected in the debit of account 99 “Profits and losses” in correspondence with the account for accounting settlements with the budget for taxes.

Therefore, if an organization was assessed penalties on taxes, then the accounting entry will be as follows:

Debit account 99 – Credit account 68 “Calculations for taxes and fees”

Moreover, since analytical accounting for account 68 is carried out by type of tax, the credit of this account indicates the type of tax for which penalties were accrued.

So, when calculating penalties for value added tax, the posting will be as follows:

Debit account 99 – Credit account 68, sub-account “VAT”

Accordingly, the transfer of the amount of accrued penalties will be reflected in the accounting entry:

Debit account 68, sub-account “VAT” - Credit account 51, etc.

And when calculating penalties for tax under the simplified tax system, the accounting entry, accordingly, will be:

Debit of account 99 – Credit of account 68, subaccount “USN”

When calculating penalties on contributions, accounting entries will also consist of a debit to account 99, but for a loan you need to indicate account 69 “Calculations for social insurance and security”

Penalty under an employment contract: how to take into account personal income tax and contributions?

If we are talking about the payment of a penalty to an individual under an employment contract (in the general case - in connection with a delay in wages), then other entries will be reflected in the accounting records:

- Dt 91 Kt 73 (the employer's penalties to the employee for wages have been accrued);

- Dt 73 Kt 51 or 50 (penalties paid).

The use of entries, which in turn are associated with the calculation of personal income tax and social contributions for penalties under employment contracts, is characterized by certain nuances.

A penalty under an employment contract is not subject to personal income tax if it is accrued within the limits established by the provisions of Art. 236 Labor Code of the Russian Federation. This is stated in paragraph 3 of Art. 217 of the Tax Code of the Russian Federation and is confirmed by the Ministry of Finance of Russia in letter dated February 28, 2017 No. 03-04-05/11096.

If a collective agreement or a specific employment contract establishes higher standards, then personal income tax is also not charged on interest. But if such standards are not established at the enterprise, then when a higher compensation is actually paid, personal income tax is charged on the difference between this compensation and the standards prescribed in the Labor Code of the Russian Federation (letter of the Ministry of Finance of Russia dated November 28, 2008 No. 03-04-05-01/450).

Contributions for penalties under an employment contract are generally always accrued (letter of the Ministry of Labor of Russia dated April 27, 2016 No. 17-4-OOG-701). Although in judicial practice there are also opposing positions (for example, Resolution of the Presidium of the Supreme Arbitration Court of the Russian Federation dated December 10, 2013 No. 11031/13). But strictly speaking, according to the letter of the law, contributions must be calculated and, in order to avoid legal disputes, it is recommended.

If you need to reflect personal income tax on a contractual penalty, the following entries apply:

Subscribe to our newsletter

Yandex.Zen VKontakte Telegram

- Dt 73 Kt 68 (personal income tax withheld for a penalty);

- Dt 68 Kt 51 (NDFL paid).

Insurance premiums are reflected in the same entries as in the case of a civil contract.

How to reflect the accrual and payment of tax penalties and fines in accounting

The basis for making entries for penalties or fines assessed for payment to the budget are documents with the amounts of these payments issued by the tax authority:

- decisions based on the results of the audit;

- requirements for payment of taxes (contributions).

For the taxpayer, they represent an expense, which the Chart of Accounts recommends reflecting on account 99. However, it will not be a violation to use account 91 for this purpose (allowing for expansion of the list of other expenses listed in the Chart of Accounts) provided that they are separated in the analytics from penalties, accrued in favor of counterparties. The corresponding account for tax sanctions will be account 68, in which both penalties and fines should be allocated for each tax (contribution) in the analytics.

How to take into account the penalty for the entitled party?

In turn, the party that receives the counterparty’s penalty under the contract will reflect the following entries in the accounting records:

- Dt 76 Kt 91.1 (the penalty was recognized by the court or the parties in accordance with the supporting document);

- Dt 51 Kt 76 (the penalty is credited to the company’s current account).

Note that according to account 76, it makes sense for the authorized party (by the way, as well as the obligated party) to use a separate sub-account to account for penalties and other penalties under civil contracts - 76.2.

Separate nuances characterize the establishment of the company’s obligation to charge VAT on the received penalty (if the taxpayer works under the OSN). This issue is highly controversial. It will be useful to familiarize yourself with the arguments for and against the calculation of VAT in legal relations involving the formation of a penalty.

Write-off from the account by court decision

Accounting for state fees Legal expenses in the form of state fees, incurred by the plaintiff and subject to recovery by decision of the arbitration court from the defendant, on the date of entry into force of the court decision are attributed by the plaintiff to other income and are reflected by an entry on the credit of account 91 in correspondence with the debit of account 76 “Settlements with various debtors and creditors" (clause 7 of PBU 9/99 "Income of the organization"). Accordingly, in the defendant’s accounting, the amounts of compensation for legal costs paid to the plaintiff are classified as other expenses and are also reflected in the accounting on the date the court decision entered into force. The entries to reflect the amount of the reimbursed state duty will be similar to the entries made in the accounting to reflect the recognition of expenses in the form of overdue rent : Debit 91, subaccount “Other expenses” Credit 76, subaccount “Settlements on claims” - RUB 26,932.04.

And therefore they are faced with malicious debtors among them. When all attempts to resolve this situation have been exhausted, the company's management has no choice but to go to court to collect the debt.

Let's consider a situation where the court made a decision in favor of the creditor and, in addition to the debt, ordered the debtor to return legal costs and imposed a penalty.

Debt collection through court (postings)

The debt of accountable persons is reflected according to the article specified in the current legislation.

It must be remembered that the tax sphere is constantly being reformed. If not all amounts have been spent, then the remainder is returned to the company's cash desk.

If the amount was overspent, and there is evidence that it was necessary, then the overspending is returned to the employee.

The necessity of the expenses incurred is checked and certified by the company management.

If the employee received funds for travel expenses, then the advance report and the unspent amount should be submitted to the accounting department no later than 3 working days upon return.

Write-off from the current account by court decision

The following entries are made in accounting: Debit Credit Description of transaction Dt 68 Kt 50 (51) Payment of state duty Dt 91/2 Kt 68 Acceptance of state duty as part of expenses Dt 76/2 Kt 91/1 Confirmation of state duty expenses by the court Dt 51 Kt 76/2 Occurs reimbursement of expenses Now we need to deal with VAT. The fact is that it was accrued with the revenue. State duty is not subject to taxation.

What about penalties and interest? The fact is that these amounts are connected directly to payments for goods or services, therefore, they should make the VAT base larger.

This is stated in letters of the Ministry of Finance No. 03-07-08/204, No. 03-07-11/214, etc.

When a lawsuit is initiated to collect a debt from a debtor, the main burden falls on the shoulders of the plaintiff. It should be noted that judges have long had a different position on this issue, considering that the penalty is not subject to taxation.

Source: https://zakon52.ru/spisanie-so-scheta-po-resheniyu-suda-provodki/

Penalty and VAT: should tax be charged?

There are 2 opposing points of view regarding this issue:

- VAT must be charged because, in accordance with subparagraph. 2 p. 1 art. 162 of the Tax Code of the Russian Federation, the tax base for VAT is formed from any amounts that are associated with payment for goods sold (and there is no obvious reason to consider the amount of the penalty as an exception).

- There is no need to charge VAT, since the agreement on penalties in accordance with Art. 331 of the Civil Code of the Russian Federation is drawn up separately from the main agreement of the parties. Therefore, the penalty should not be associated with payment for goods (letter of the Ministry of Finance of Russia dated 06/08/2015 No. 03-07-11/33051).

If we talk about the type of penalty accrued on the basis of Art. 317.1 of the Civil Code of the Russian Federation (on interest for illegal withholding of funds), the Ministry of Finance allows VAT to be charged on the amount of such a penalty if there is a connection between it and payment for goods, without explaining the specific criteria for establishing the fact of such a connection (letter from the Ministry of Finance of Russia dated 03.08.2016 No. 03-03-06/1/45600).

Thus, the taxpayer determines whether or not to charge VAT. If there is objectively no reason to consider the penalty related to the receipt of payment for the goods, no tax is charged.

There are many types of penalties: for late payment, for downtime, for exceeding limits, etc. The Tax Guide ConsultantPlus will help you determine the calculation of VAT on the amounts of various types of penalties. You can take advantage of a free trial if you don't have K+ yet.

But if the company believes otherwise, then VAT transactions will be reflected (by the authorized party) in the accounting registers using the following entries:

- Dt 91.2 Kt 76 (sub-account “VAT”) - VAT is charged on the amount of the calculated penalty;

- Dt 76 Kt 68 - VAT is charged on the amount of the penalty received;

- Dt 68 Kt 51 - VAT on the penalty has been paid.

The penalty under the contract can be written off by the entitled party. Let's study which entries reflect this in accounting.

Accounting and taxation of fines, penalties, penalties under business contracts for the debtor organization

In accounting, fines, penalties, and penalties for violation of contractual obligations are included in non-operating expenses. This is determined by paragraph 12 of Order of the Ministry of Finance of the Russian Federation dated May 6, 1999 No. 33n “On approval of the accounting regulations for “organizational expenses” PBU 10/99″ (hereinafter referred to as PBU 10/99).

In accordance with clause 14.2 of PBU 10/99, fines, penalties, penalties are accepted for accounting in the amounts awarded by the court in the reporting period in which the court made a decision on their collection.

In accordance with the Chart of Accounts and the Instructions for its application, approved by Order of the Ministry of Finance of the Russian Federation dated October 31, 2000 No. 94n, in accounting for the reflection of fines, penalties, penalties, account 91 “Other income and expenses” is intended, subaccount 91-2 “Other expenses » in correspondence with accounts for settlements or cash.

| Account correspondence | ||

| Debit | Credit | |

| 91-2 "Other expenses" | Penalties for violation of contractual obligations awarded by the court are reflected | |

| Penalties paid for violation of contractual obligations | ||

Example 1.

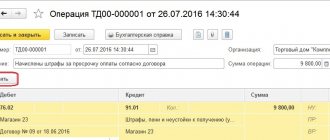

The Vega organization shipped a consignment of goods to the Delta organization in the amount of 236,000 rubles (excluding VAT). According to the terms of the agreement, for late payment for goods, a fine of 50,000 rubles and a penalty of 0.1% for each day of delay are provided. The Delta organization did not make the payment on time, thereby violating the terms of the contract. The Vega organization filed a claim for a fine in the amount of 50,000 rubles and penalties in the amount of 3,200 rubles. The Delta organization agreed with the claim made against them.

| Account correspondence | Sum | ||

| Debit | Credit | ||

| 236 000 | Goods accepted for accounting | ||

| 91-2 “Other expenses” | 53 200 | Received a complaint from the supplier | |

| 236 000 | Payment for goods reflected | ||

| 53 200 | Fines and penalties listed | ||

End of the example.

For the purpose of calculating income tax, the amount of the fine payable is taken into account as part of non-operating expenses not related to production and sales, in accordance with subparagraph 13 of paragraph 1 of Article 265 of the Tax Code of the Russian Federation (hereinafter referred to as the Tax Code of the Russian Federation).

The date of recognition of expenses in the form of a fine, penalty, or penalty for a taxpayer who determines income and expenses using the accrual method is the date the organization recognizes the fine. This follows from subparagraph 8 of paragraph 7 of Article 272 of the Tax Code of the Russian Federation:

“the date of recognition by the debtor or the date of entry into legal force of the court decision - for expenses in the form of amounts of fines, penalties and (or) other sanctions for violation of contractual or debt obligations, as well as in the form of amounts of compensation for losses (damage).”

For organizations that determine income and expenses on a cash basis, expenses in the form of fines, penalties and (or) other sanctions for profit tax purposes are recognized after their actual payment (clause 3 of Article 273 of the Tax Code of the Russian Federation).

Please note that in order to recognize fines, penalties, penalties as part of non-operating expenses, a document is required that confirms the fact of violation of contractual obligations by the debtor. That is, the requirement of Article 252 of the Tax Code of the Russian Federation must be met, expenses must be justified and documented.

Penalties are calculated based on the terms of the contract, or at the written request of the creditor, or by court decision. Do I need to issue an invoice for the amount of the penalty? In accordance with paragraph 1 of Article 168 of the Tax Code of the Russian Federation, when selling goods (work, services), the supplier issues the corresponding invoices to the buyer. But if a penalty is accrued, no shipment of goods, performance of work, or provision of services occurs, therefore, the supplier does not issue an invoice for the amount of penalties.

Please note that the payer of the penalty (buyer), calculated on the amount of the penalty, does not have the right to deduct VAT. Since Article 171 of the Tax Code of the Russian Federation does not provide for the possibility of accepting a tax deduction for VAT on this basis.

According to paragraph 2 of Article 171 of the Tax Code of the Russian Federation, tax amounts presented to an organization for goods, work, services, property rights acquired for the implementation of transactions recognized as objects of taxation and for goods (work, services) acquired for resale are subject to deduction.

As we can see, the organization has no grounds to offset the tax paid against penalties.

A similar point of view is reflected in the letter of the Ministry of Taxes and Taxes of the Russian Federation dated April 27, 2004 No. 03-1-08/1087/14.

Therefore, the organization attributes the total amount of sanctions, together with the tax, to non-operating expenses in its accounting as of the date of the letter of agreement to pay the sanctions under the contract.

For profit tax purposes, the organization takes into account the amounts on the claim without VAT, since all cases when VAT can be taken into account in expenses are listed in Article 170 of the Tax Code of the Russian Federation (Appendix No. 4).

Example 2.

The Vega organization shipped products to the Delta LLC organization in the amount of 295,000 rubles (including VAT 45,000 rubles). In accordance with the agreement, Delta LLC must pay for the products received within 15 days. For each day of delay, Delta LLC must pay a penalty in the amount of 0.5% of the cost of the products under the contract. Delta LLC delayed payment by 10 days. A claim was made to the organization. In response to the submitted claim, Delta LLC agreed to pay a penalty based on the terms of the contract.

| Account correspondence | Amount, rubles | ||

Answer

If your contract stipulates the possibility of withholding a penalty from the monetary security of the contract, then we recommend that you reflect the situation in your accounting with the following entries:

Debit 3.201.11.510 Credit 3.304.01.730 – Application security money received at the temporary disposal of the institution

Debit 1.209.40.560 Credit 1.401.10.140 – a penalty was imposed under the contract

Debit 3.304.01.830 Credit 3.304.06.730

Debit 1.304.06.830 Credit 1.209.40.660 – the penalty was offset against the application security

Debit 3.303.05.830 Credit 3.201.11.610 - Money transferred to budget revenue

These postings are made by analogy with the offset of penalties by securing a contract for budgetary institutions, therefore we recommend that this procedure for state-owned institutions be agreed upon with the founder or financial authority.

How to take into account money to secure an application or execution of a contract for procurement under Law No. 44-FZ

Situation:

How can the customer record the monetary security of the application and its return in accounting?

One way to secure an application is a cash deposit. The participant transfers it to the account:

- the customer, if there is a competition or request for proposals;

- operator of the electronic platform (EP), if the customer is holding an auction.

This follows from the provisions of paragraph 7 of Article 42, parts 1, 2, 5, 8 of Article 44 of the Law of April 5, 2013 No. 44-FZ.

Read more: To find out the identity, how long can they detain

How the customer takes into account application security depends on where it is received - to his account or to the account of the electronic signature operator.

1. The security is credited to the customer’s account

The money that is received to secure the application should be reflected in account 304.01 “Settlements for funds received for temporary disposal” according to KFO 3 “Funds for temporary disposal” (clause 21, 267 of the Instructions to the Unified Chart of Accounts No. 157n). There is no need to account for money in off-balance sheet account 10 “Securing the fulfillment of obligations” (letter of the Ministry of Finance of Russia dated June 27, 2014 No. 02-07-07/31342).

The order in which collateral is recorded depends on the type of institution.

In the accounting of government institutions:

Is the institution served by the Russian Treasury? Then the application security money will be credited to a personal account with attribute 05 “Personal account for accounting for transactions with funds coming at the temporary disposal of the recipient of budget funds” (subclause “e”, clause 4, clause 8.2 of the Procedure approved by order of the Treasury of Russia dated October 17 2016 No. 21n).

If the institution is served by the financial authority of a constituent entity of the Russian Federation or municipal entity, the money will be credited in the manner established by the relevant financial authority (Article 220.1 of the Budget Code of the Russian Federation).

In accounting for funds from the procurement participant, reflect the following posting:

| № | Contents of operation | Account debit | Account credit |

| 1. | The application security money has been placed at the temporary disposal of the institution | KIF.3.201.11.510 simultaneously increasing off-balance sheet account 17 (analytics code 510) | gKBK.3.304.01.730 |

Then the customer returns this money to the procurement participants or transfers it to budget revenue (Part 13, Article 44 of Law No. 44-FZ of April 5, 2013, Clause 3, Article 41 of the Budget Code of the Russian Federation).

If you are returning money to a participant, make an entry in your accounting:

| № | Contents of operation | Account debit | Account credit |

| 1. | The application security money was returned to the participant | gKBK.3.304.01.830 | KIF.3.201.11.610 simultaneously increasing off-balance sheet account 18 (analytics code 610) |

This procedure is established by paragraph 106 of Instruction No. 162n, paragraphs 365, 367 of the Instructions to the Unified Chart of Accounts No. 157n.

If you are transferring money to budget revenue, in the payment document indicate code 000 1 1600 140 “Monetary penalties (fines) for violation of the legislation of the Russian Federation on the contract system in the field of procurement of goods, works, services to meet state and municipal needs for the needs of the Russian Federation” ( letter of the Ministry of Finance of Russia dated September 17, 2015 No. 02-08-07/53443).

In place of the 1st–3rd digits of the income code, indicate the code of the chief administrator, in place of the 14th–20th digits – the code of the subtype of income.

In what order to reflect the transfer of money depends on the powers of the budget revenue administrator:

| № | Contents of operation | Account debit | Account credit |

| The institution has been given powers to accrue income: | |||

| 1. | Money transferred to budget revenue | gKBK.3.304.01.830 | KIF.3.201.11.610 |

| 2. | Accrued budget income from application support funds | KDB.1.209.40.560 | KDB.1.401.10.140 |

| 3. | The cash receipts administrator is notified of the expected income (according to notification f. 0504805) | KDB.1.304.04.140 | KDB.1.303.05.730 |

| 4. | The money was credited to budget revenue (according to notification f. 0504805 from the cash receipts administrator) | KDB.1.303.05.830 | KDB.1.209.40.660 |

| The institution has been given all the powers of the revenue administrator: | |||

| 1. | Money transferred to budget revenue | gKBK.3.304.01.830 | KIF.3.201.11.610 |

| 2. | Accrued budget income from application support funds | KDB.1.209.40.560 | KDB.1.401.10.140 |

| 3. | Money credited to budget income | KDB.1.210.02.140 | KDB.1.209.40.660 |

This procedure follows from paragraphs 86, 91, 104, 109, 120 of Instruction No. 162n.

Is it possible to recover a penalty under a contract from its security (collateral, bank guarantee)

The customer may withhold a penalty from the monetary security of the contract (letter of the Ministry of Economic Development of Russia dated July 30, 2015 No. D28i-2233).

The Russian Ministry of Finance believes that this can only be done if such an opportunity is spelled out in the contract itself. The clarifications concern penalties for payment of the contract, but they can also be applied to security.

How can a customer and supplier calculate and take into account penalties for a contract under Law No. 44-FZ

How to pay a contract minus penalties

Situation:

whether the recipient of budget funds - a government institution - has the right to pay for the contract minus the amount of the penalty. The supplier violated the terms of the contract

Yes, you have the right. But only if the institution, the PBS, immediately transfers the money to budget revenue.

The supplier did not fulfill the obligation under the contract on time - the customer will present a penalty. Specify how to collect it in the contract. We will tell you how to reduce the payment under the contract by the amount of the penalty.

Do not draw up an additional agreement to the contract, but simply indicate in the acceptance certificate of goods, works or services:

- contract price;

- the amount of the penalty;

- the grounds on which the customer demands a penalty and how it is calculated;

- the total amount to be paid to the contractor.

Include all required details in the acceptance certificate, otherwise the document will be declared invalid. Additionally, draw up a reconciliation report.

This conclusion follows from paragraph 1 of Article 330, paragraph 1 of Article 332 of the Civil Code of the Russian Federation, part 6 of Article 34 of the Law of April 5, 2013 No. 44-FZ and is explained in letters of the FAS Russia dated December 10, 2015 No. AC/70978/15, the Ministry of Finance of Russia dated September 4, 2012 No. 02-06-10/3525.

How to transfer to the budget

The penalty is budget income. If you reduce the contract payment to the counterparty by the amount of the penalty, the budget will not receive income, and the expenditure portion will decrease. This is an offset between the revenue and expenditure parts of the budget. However, the Budget Code of the Russian Federation does not provide for the execution of the budget based on income by offsetting expenditure obligations (clause 3 of Article 41, Article 218 of the Budget Code of the Russian Federation).

We included a condition on the offset of sanctions against payment - specify the customer’s obligation to transfer the penalty to the budget (Article 313 of the Civil Code of the Russian Federation). In this case, pay the contract minus the penalty and change the budget obligation. And transfer the penalty yourself to budget revenue. In the payment document, indicate the name of the counterparty for whom you are transferring the fine or penalty.

For federal

institutions, the Ministry of Finance of Russia has established such a procedure. They transfer the penalty to the budget on the same day when they pay the main obligation under the contract. That is, an application for payment of the contract is submitted to the Treasury of Russia along with an application for the transfer of the penalty to the budget.

Read more: Veterinary activities are subject to licensing

This follows from paragraph 8 of the Procedure, approved by order of the Ministry of Finance of Russia dated November 17, 2021 No. 213n, and clarifications in the letter of the Ministry of Finance of Russia dated December 26, 2011 No. 02-11-00/5959.

Attention:

If you do not transfer the penalty to the budget, the inspectors will recognize you as a violator of budget legislation.

KBK for payment

The penalty is non-tax budget revenue. The customer applies liability measures to the counterparty for violating the terms of a civil transaction. Therefore, when you transfer a penalty to the budget, use the generalized code 000 1 1600 140 “Other receipts from monetary penalties (fines) and other amounts for damages.” Then detail the code to the budget level where the money will go. If the institution is federal - code 000 1 16 900 10

00 0000 140, regional - code 000 1 16 900

20

00 0000 140. For other codes, see Appendix 1 to the instructions approved by Order of the Ministry of Finance of Russia dated July 1, 2013 No. 65n. In place of digits 1–3 of the income classification code, enter the code of the chief administrator. There are 14–20 digits in place - the code for the subtype of income.

This procedure follows from paragraph 3 of Article 41 of the Budget Code of the Russian Federation, Articles 329, 330 of the Civil Code of the Russian Federation. The Russian Ministry of Finance further clarifies the issue in paragraph 2 of letter No. 02-08-07/53443 dated September 17, 2015.

How to adjust a budget commitment

Withhold a penalty from the contract fee - reduce the institution’s obligations to the supplier. To do this, submit to the Russian Treasury at the place of service:

- application for amendments to the budget obligation (f. 0531705). In section 2 of the application “Counterparty details”, indicate the details of the contractor and administrator of budget revenues;

- acceptance certificate with information about the penalty and the reasons why it was collected.

Such clarifications are given in the joint letter dated November 8, 2013 of the Ministry of Finance of Russia No. 02-03-007/47762 and the Treasury of Russia No. 42-7.4-05/3.3-684.

An example of how a customer can reflect in accounting the payment of obligations under a contract minus the amount of the penalty. The supplier violated the terms of the contract

On November 27, 2021, the state institution “Alpha”, the administrator of budget revenues, concluded a government contract with LLC “Proizvodstvennaya” for the supply of office equipment. Contract price – 1,000,000 rubles. If the counterparty violates the delivery deadline, Alpha has provided for penalties, as well as the opportunity to withhold them from payment under the contract. The customer transfers the penalty to the budget income.

The delivery period under the contract is 30 calendar days. The “master” was 12 days late.

The refinancing rate on the day the penalty is paid is 9 percent.

Contract Manager A.S. Kondratyev calculated the penalties:

1,000,000 rub. × 12 days × 9%: 300 = 3600 rub.

The Alpha accountant made the following entries in accounting:

| № | Contents of operation | Account debit | Account credit | Amount, rub. |

| 1. | Penalties were presented to the “Master” for violating delivery deadlines | KDB.1.209.40.560 | KDB.1.401.10.140 | 3600 |

| 2. | The liability accepted for accounting is the cost of office equipment | KRB.1.106.31.310 | KRB.1.302.31.730 | 1 000 000 |

| 3. | The obligation to the “Master” was reduced by the amount of the penalty | KRB.1.302.31.830 | KDB.1.209.40.660 | 3600 |

| 4. | The obligation under the contract has been paid minus the penalty (RUB 1,000,000 – RUB 12,000) | KRB.1.302.31.830 | KRB.1.304.05.310 | 996 400 |

| 5. | The amount of penalties withheld to fulfill obligations was transferred to budget revenues | KDB.1.303.05.830 | KRB.1.304.05.310 | 3600 |

| 6. | The amount of penalties under the contract was received as budget revenue | KDB.1.210.02.140 | KDB.1.303.05.730 | 3600 |

How can a budgetary and autonomous institution reflect in the Report (f. 0503737) penalties (penalties, fines) from contract security?

Security under a contract is a means of temporary disposition, which is reflected in KFO 3. There is no need to fill out a Report for them (f. 0503737). But reflect the income from penalties (penalties, fines) in the Report, since these funds are taken into account under KFO 2 “Income-generating activities of the institution.” This follows from paragraphs 21, 267 of the Instructions for the Unified Chart of Accounts, paragraph 34 of the Instructions, approved by Order of the Ministry of Finance of Russia dated March 25, 2011 No. 33n.

For more information on accounting for penalties from contract security, see the recommendations. Next, we’ll look at how to fill out the Report for these transactions (f. 0503737).

When you withhold sanctions under a contract from the amount of its security, this is a non-cash transaction. After all, there is no actual movement on the account. Therefore, reflect such income in column 8 “Fulfilled planned assignments through non-cash transactions.”

This follows from paragraph 42 of the Instruction, approved by order of the Ministry of Finance of Russia dated March 25, 2011 No. 33n, and is explained in Appendix 1 to the letter of the Ministry of Finance of Russia dated July 1, 2015 No. 02-07-07/38257.

An example of how to generate a Report (f. 0503737) on penalties (fines, fines) from contract security

For nine months of 2021, the budgetary institution "Alpha" entered into a contract under which it received security of 10,000 rubles.

The supplier has violated its obligations. "Alpha" charged him a penalty of 8,500 rubles. and withheld her from securing the contract. Alpha returned the remaining amount of security to the supplier.

Alpha's accountant documented the transactions with the following entries:

| № | Contents of operation | Account debit | Account credit | Amount, rub. |

| 1. | Contract security has been deposited into your personal account | 3.201.11.510 | 3.304.01.730 | 10 000 |

| 2. | Penalty income accrued | 2.209.40.560 | 2.401.10.140 | 8500 |

| 3. | Counterclaims for: | |||

| 3.1. | – return of contract security to the supplier | 3.304.01.830 | 3.304.06.730 | 8500 |

| 3.2. | – payment by the supplier of penalties under the contract | 2.304.06.830 | 2.209.40.660 | 8500 |

| 4. | Shows how the cash balances on your personal account have changed: | |||

| 4.1. | – the balance of funds in temporary disposal has been reduced by the amount of security | 3.304.06.830 | 3.201.11.510 simultaneously increasing off-balance sheet account 18 (analytics code 610) | 8500 |

| 4.2. | – the balance for paid activities was increased by the amount of the penalty from the security | 2.201.11.510 simultaneously increasing off-balance sheet account 17 (income code 140) | 2.304.06.730 | 8500 |

| 5. | The balance of the security amount was transferred to the supplier | 3.304.01.830 | 3.201.11.610 simultaneously increasing off-balance sheet account 18 (analytics code 610) | 1500 |

Read more: Interested Witnesses in Civil Proceedings

For transactions, the accountant filled out the Report (f. 0503737) by sections.

Section 1 “Institutional income”:

| Indicator name | Line code | Analytics code | Planned appointments completed | |||

| through bank accounts | total | |||||

| Income – total | 010 | X | – | – | 8500 | 8500 |

| Amounts of forced seizure | 140 | – | – | 8500 | 8500 | |

Section 3 “Sources of financing the institution’s fund deficit”:

The company may be fined by the tax authorities, for example, for late submission of reports. Counterparties may impose fines for violating the terms of contracts. The opposite may also happen - the organization itself will receive monetary compensation from a supplier who did not ship the goods on time. Accounting for sanctions in each specific case has its own characteristics. Let's look at them in more detail.

Legal interest

From June 1, 2015, debtors are obliged to pay creditors legal interest on monetary obligations (Article 317.1 of the Civil Code of the Russian Federation, paragraph 1 of Article 2 of the Law of March 8, 2015 No. 42-FZ).

Interest is called legal because the right to receive it is directly provided for by the Civil Code of the Russian Federation and does not require confirmation of this in contracts. For example, under a contract for the sale of goods, the obligation to pay legal interest by default will arise from the buyer if he pays for the goods after shipment: the next day or later.

If the parties initially agree not to accrue legal interest, then the contract says: “legal interest is not accrued” or “interest on monetary obligations is not accrued.” Of course, you also won’t have to pay interest if no debt has arisen. For example, if the buyer paid for the goods on the day of shipment.

Interest is calculated on the entire amount of the debt from the next day after the occurrence of the monetary obligation until the day of its actual repayment, inclusive. It does not matter whether the payment is overdue or not.

For example, under a purchase and sale agreement, define the default period for calculating legal interest as follows:

| Condition in the contract | Execution of obligations | Period for calculating legal interest |

| Pay for the goods within 5 calendar days from the date of shipment | Paid on the day of shipment | 0 days (no interest accrued) |

| Paid on the 5th calendar day from the date of shipment | 5 days | |

| Paid on the 10th calendar day from the date of shipment | 10 days (including 5 days of delay) |

Calculate legal interest based on the refinancing rates that were in effect during the period of use of funds. That is, if the rate has changed, then the calculation should take this into account.

Determine the percentage using the formula:

| Legal interest | = | Debt amount | × | Refinancing rate | : | 365/366 days | × | Number of days of using funds |

This follows from the provisions of Article 317.1 of the Civil Code of the Russian Federation.

Penalty from the buyer for violating the delivery deadline for wiring and VAT! Help me please!

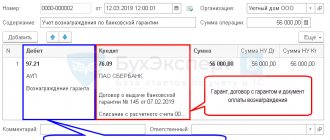

Decisions of the arbitration court enter into legal force one month after their adoption, unless an appeal has been filed (clause 1 of Article 180 of the Arbitration Procedure Code of the Russian Federation). Consequently, the reflection of penalties for violation of contractual obligations based on a court decision in accounting should occur in the reporting period when a month has passed from the date of the decision of the arbitration court. Amounts of claims (claims) submitted that are not recognized by the payer (not awarded by the court) are not accepted for accounting. Penalties collected from counterparties for non-compliance with contractual obligations, in amounts recognized by payers or awarded by the court, are reflected in the following entries: - debit 76-2 “Settlements on claims” credit 91-1 “Other income”: penalties recognized by the debtor or awarded by the court; — debit 51 credit 76-2: penalties received.

simplified tax system

Regardless of the object of taxation, include the penalty (interest on late payments) as part of the income when calculating the single tax (clause 1 of Article 346.15 of the Tax Code of the Russian Federation). The tax base needs to be increased only after the amounts of sanctions are actually received from the counterparty (clause 1 of Article 346.17 of the Tax Code of the Russian Federation).

An example of how interest is reflected in taxation for late fulfillment of a monetary obligation. The organization applies simplification

Alpha LLC entered into a loan agreement with its employee - workshop manager A.S. Kondratiev. According to the agreement, the organization provides him with a cash loan in the amount of 45,000 rubles. The employee returned the money eight days late. The bank interest rate on deposits is conditionally 10 percent per annum.

The agreement does not establish the borrower's liability in the form of a penalty. Therefore, Alpha decided to collect late interest from the debtor. The accountant calculated the amount of interest based on the average bank interest rate on deposits: 45,000 rubles. × 10%: 360 days. × 8 days = 100 rub.

Kondratiev deposited interest in the organization's cash desk in cash on March 1.

When calculating the single tax, the Alpha accountant included in income the amount of interest in the amount of 100 rubles.

Penalty under a supply agreement

A fine can be imposed on both the buyer and the supplier of goods in the following situations:

1. The supplier violated the terms of delivery of goods specified in the contract.

2. The buyer did not pay for the goods within the terms specified in the delivery agreement.

Most often, the violator pays penalties calculated for each day of late payment. If the terms of the contract are violated, the guilty party must pay a penalty in accordance with the contract. The company whose rights have been violated submits a written demand (claim) to the guilty organization for payment of a penalty (Article 331 of the Civil Code of the Russian Federation). The parties can agree to postpone the payment of the fine by signing an additional agreement.

Often the violator of the contract refuses to pay the fine. In this case, you can file a lawsuit. If the court makes a positive decision, the counterparty will be required to pay a fine. Most likely, the violator will be required to reimburse court costs and the state fee paid by the plaintiff for the consideration of the case in court.