In this article, we will analyze the procedure for writing off materials in 1C Accounting (using the example of the BP 8.3 configuration), and also give step-by-step instructions for making a write-off. First, we will consider the methodological approach from the point of view of accounting and tax accounting, then the procedure for user actions when writing off materials in 1C 8.3. It should be noted that the general procedure for writing off materials is considered, without taking into account certain industry nuances. For example, a development, agricultural or manufacturing enterprise requires additional standard documents or acts for the write-off of materials.

Methodological guidelines

In accounting, the procedure for writing off materials is regulated by PBU 5/01 “Accounting for inventories.” According to clause 16 of this PBU, three options for writing off materials are allowed, focused on:

- the cost of each unit;

- average cost;

- the cost of the first acquisition of inventories (FIFO method).

In tax accounting, when writing off materials, you should focus on Article 254 of the Tax Code of the Russian Federation, where under paragraph number 8 options for the valuation method are indicated, focusing on:

- unit cost of inventory;

- average cost;

- cost of first acquisitions (FIFO).

The accountant should establish in the accounting policy the chosen method of writing off materials for accounting and tax accounting. It is logical that in order to simplify accounting, the same method is chosen in both cases. Write-off of materials at average cost is often used. Write-off at unit cost is appropriate for certain types of production where each unit of materials is unique, for example, jewelry production.

Typical postings for write-off of materials

| Account debit | Account credit | Wiring Description |

| 20 | 10 | Write-off of materials for main production |

| 23 | 10 | Write-off of materials for auxiliary production |

| 25 | 10 | Write-off of materials for general production expenses |

| 26 | 10 | Write-off of materials for general business expenses |

| 44 | 10 | Write-off of materials for expenses associated with the sale of finished products |

| 91.2 | 10 | Disposal of materials when they are transferred free of charge |

| 94 | 10 | Write-off of the cost of materials if they are damaged, stolen, etc. |

| 99 | 10 | Write-off of materials lost due to natural disasters |

Before writing off materials in 1C 8.3, you should set (check) the appropriate accounting policy settings.

Consumption or release of materials into production

Consumption by production or organization managers of materials from the warehouse is their internal movement.

When materials are disposed of or consumed in production, accounting is carried out using the following methods:

- Piece by piece

- Weighted average price

- FIFO (first-in-first-out)

Postings:

| Account Debit | Account Credit | Description | Sum | A document base |

| 20.01 | 10.01 | Materials transferred to main production | cost price | Limit-fence card Requirement-invoice Invoice |

| 10.01 | To auxiliary production | cost price | ||

| 10.01 | For general production needs | cost price | ||

| 10.01 | For general business needs | cost price |

Accounting policy settings for writing off materials in 1C 8.3

In the settings, we will find the “Accounting Policy” submenu, and in it – “Method for assessing inventories”.

Fig. 1 Method for assessing MPZ

Here you should remember a number of specific features characteristic of the 1C 8.3 configuration.

- Enterprises in general mode can choose any valuation method. If you need a valuation method based on the cost of a unit of material, you should choose the FIFO method.

- For enterprises using the simplified tax system, a method such as FIFO is considered the most suitable. If the simplification is 15%, then in 1C 8.3 there will be a strict setting for writing off materials using the FIFO method, and the choice of the “Average” valuation method will not be available. This is due to the peculiarities of tax accounting under this taxation regime.

- Pay attention to the supporting information 1C, which says that only according to the average, and nothing else, the cost of materials accepted for processing is assessed (account 003).

If you still have questions about setting up your accounting policies, contact our specialists for advice on 1C programs, we will be happy to help you.

Free expert consultation

Natalia Sevorina

Consultant-analyst 1C

Thank you for your request!

A 1C specialist will contact you within 15 minutes.

Write-off of materials step-by-step instructions for accounting

Any organization acquires materials for the company’s activities not for their own sake. And the purchased valuables will not lie dead weight in the warehouse for the director to admire. They are intended for use in production, sales or administrative purposes. Therefore, purchased materials are subsequently consumed in production.

However, in the warehouse the storekeeper or warehouse manager is responsible for them, and the materials are taken into account on account 10. When the materials leave the warehouse, the situation will change: the account and the person in charge will change. In this article we will analyze the write-off of materials with step-by-step instructions for this procedure for you.

articles:

1. Accounting entries for writing off materials

2. Registration of write-off of materials

3. Write-off of materials - step-by-step instructions if not everything is consumed

4. Standards for writing off materials for production

5. Example of a write-off act

6. Methods for writing off materials for production

7. Option No. 1 – average cost

8. Option No. 2 – FIFO method

9. Option No. 3 – at the cost of each unit

So, let's go in order. If you don't have time to read a long article, watch the short video below, from which you will learn all the most important things about the topic of the article.

(if the video is not clear, there is a gear at the bottom of the video, click it and select 720p Quality)

We will look at write-offs of materials in more detail than in the video later in the article.

Accounting entries for write-off of materials

So, let's start by determining where the purchased materials can be sent. It should be noted that materials are truly ubiquitous and there are ways to, as they say, “plug a hole” in any problem area of the organization:

- - serve as the basis for the production of products

- - be an auxiliary consumable material in the production process

- — perform the function of packaging finished products

- - used for the needs of the administration in the management process

- — assist in the liquidation of decommissioned fixed assets

- - used for the construction of new fixed assets, etc.

And the accounting entries for writing off materials depend on what materials are released from the warehouse for:

Debit 20 “Main production” – Credit 10 – raw materials released for production

Debit 23 “Auxiliary production” - Credit 10 - materials were released to the repair shop

Debit 25 “General production expenses” – Credit 10 – rags and gloves were issued to the cleaner servicing the workshop

Debit 26 “General business expenses” – Credit 10 – paper for office equipment issued to the accountant

Write-off of materials in 1C 8.3

To write off materials in the 1C 8.3 program, you need to fill out and post the “Requirement-invoice” document. The search for it has some variability, that is, it can be carried out in two ways:

- Warehouse => Requirement-invoice

- Production => Requirement-invoice

Fig.2 Request-invoice

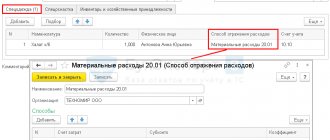

Let's create a new document. In the document header, select the Warehouse from which we will write off materials. The “Add” button in the document creates records in its tabular part. For ease of selection, you can use the “Selection” button, which allows you to see the remaining materials in quantitative terms. In addition, pay attention to the related parameters - the “Cost Accounts” tab and the “Cost Accounts on the “Materials” tab” checkbox setting.

If the checkbox is not checked, then all items will be written off to one account, which is set on the “Cost Accounts” tab. By default, this is the account that is set in the accounting policy settings (usually 20 or 26). This indicator can be changed manually. If you need to write off materials to different accounts, then check the box, the “Accounts” tab will disappear, and on the “Materials” tab you will be able to set the necessary transactions.

Fig.3 Materials

Below is the form screen when you click the "Select" button. For ease of use, to see only those positions for which there are actual balances, make sure that the “Only balances” button is pressed. We select all the necessary positions, and with a mouse click they go to the “Selected Positions” section. Then click the “Move to Document” button.

Fig.4 Transfer to document

All selected items will be displayed in the tabular part of our document for write-off of materials. Please note that the parameter “Cost accounts on the “Materials” tab” is enabled, and from the selected items “Apple jam” is written off to the 20th account, and “Drinking water” – to the 25th.

In addition, be sure to fill out the sections “Cost division”, “Nomenclature group” and “Cost item”. The first two become available in documents if the settings are set in the system parameters “Keep cost records by department - Use several item groups”. Even if you keep records in a small organization where there is no division into item groups, enter the item “General item group” in the reference book and select it in the documents, otherwise problems may arise when closing the month. At larger enterprises, proper implementation of this analytics will allow you to quickly receive the necessary cost reports. A cost division can be a workshop, a site, a separate store, etc., for which it is necessary to collect the amount of costs.

The product group is associated with the types of products manufactured. The amount of revenue is reflected by product groups. In this case, for example, if different workshops produce the same products, one product group should be indicated. If we want to see separately the amount of revenue and the amount of costs for different types of products, for example, chocolate and caramel candies, we should establish different product groups when releasing raw materials into production. When indicating cost items, be guided at least by the tax code, i.e. you can specify the items “Material costs”, “Labor costs”, etc. This list can be expanded depending on the needs of the enterprise.

Fig.5 Indication of cost items

After specifying all the necessary parameters, click the “Pass and close” button. Now you can see the wiring.

Fig.6 Swipe and close

During further accounting, if you need to issue a similar demand invoice, you can not create the document again, but make a copy using the standard capabilities of the 1C 8.3 program.

Fig.7 1C 8.3

Our company provides support and implementation services for 1C programs, and you can also order modifications to 1C from us. If you have any questions, please contact him, we will be happy to help you.

Costs of construction of fixed assets

Reflection in accounting of the customer's purchase of materials for construction and installation work by contractors.

| № | Debit | Credit | Contents of operation |

| Accounting entries at the time of posting of materials, if their receipt is reflected by the customer organization without using account 15 “Procurement and acquisition of material assets” | |||

| 1 | 10 | 60, 76 | The purchase price of the material, excluding VAT, purchased for construction and installation work by a contractor is reflected (accrued) |

| 2 | 10 | 60, 76 | Transport and procurement costs are reflected (accrued) without VAT |

| Accounting entries at the time of posting of materials, if their receipt is reflected by the customer organization using account 15 “Procurement and acquisition of material assets” | |||

| 1 | 15 subaccount “Procurement and acquisition of materials” | 60, 76 | The purchase price of the material, excluding VAT, purchased for construction and installation work by a contractor is reflected (accrued) |

| 2 | 15 subaccount “Procurement and acquisition of materials” | 60, 76 | Transport and procurement costs are reflected (accrued) without VAT |

| 3 | 10 | 15 subaccount “Procurement and acquisition of materials” | Materials intended for construction and installation work by the contractor were received into the warehouse(s) |

| Accounting entries when reflecting VAT on materials purchased for contract work | |||

| 1 | 19 | 60, 76 | VAT is taken into account (accrued) on the cost of materials purchased for construction and installation work by the contractor |

| 2 | 19 | 60, 76 | VAT on transportation and procurement costs is taken into account (accrued) |

| 3 | 68 subaccount “VAT calculations” | 19 | The amount of VAT on the cost of materials purchased for construction and installation work by a contractor has been accepted for deduction from the budget. |

| Accounting entries when paying for materials | |||

| 1 | 60, 76 | 50, 51 | The buyer organization paid the supplier the debt for materials purchased from him |

| 2 | 60, 76 | 50, 51 | Paid the cost of transportation and procurement costs |

Reflection in accounting of the transfer of materials by the customer to contractors for construction and installation work.

| № | Debit | Credit | Contents of operation |

| Accounting entries when the customer transfers materials for construction and installation work to contractors | |||

| 1 | 10-7 | 10 | The actual cost of materials transferred to contractors for construction and installation work was written off to a separate sub-account (for their separate accounting) |

| Accounting entries when returning materials to the customer by contractors after completion of construction and installation work | |||

| 1 | 10 | 10-7 | The actual cost of the balance of materials received (returned) after completion of construction and installation work by contractors was calculated from a separate subaccount |

Reflection in accounting of actual expenses (expenses) associated with the construction of fixed assets.

| № | Debit | Credit | Contents of operation |

| Accounting entries when writing off the cost of materials used for the construction of fixed assets, if the materials are accounted for at invoice cost | |||

| 1 | 08-3 | 10 | The actual cost of materials used in the construction of fixed assets was written off |

| Accounting entries when writing off the cost of materials used for the construction of fixed assets, if the materials are accounted for at book value | |||

| 1 | 08-3 | 10 | The accounting cost of materials used in the construction of fixed assets was written off |

| 2 | 08-3 | 16 subaccount “Deviation in the cost of materials” | The positive difference between the book value and invoice value (overconsumption) of the material is written off, reflected in the debit of account 16 or |

| 08-3 | 16 subaccount “Deviation in the cost of materials” | The negative difference between the book value and invoice value (savings) of the material, reflected on the credit of account 16, was reversed | |

| Accounting entries when calculating depreciation of equipment used in the construction of fixed assets | |||

| 1 | 08-3 | 02 subaccount “Depreciation of fixed assets accounted for on account 01” | The amount of depreciation of a fixed asset object is reflected |

| Accounting entries when calculating wages and contributions from accrued wages of workers engaged in the construction of fixed assets | |||

| 1 | 08-3 | 70, 69 | Reflects the accrued amount of wages and contributions from the accrued wages of workers engaged in the construction of fixed assets |

| Accounting entries when reflecting debts for taxes and fees included in capital construction costs | |||

| 1 | 08-3 | 68 | Taxes and fees accrued on capital construction costs or |

| 08-3 | 68 | Overpayment of taxes and fees on capital construction costs has been reversed | |

| Accounting entries for own works (services), when writing off general business expenses attributable to the construction of fixed assets | |||

| 1 | 08-3 | 26 | The share of general business expenses attributable to the construction of fixed assets is reflected |

| Accounting entries for own works (services), when writing off costs (expenses) of auxiliary (auxiliary) productions attributable to the construction of fixed assets | |||

| 1 | 08-3 | 23 | The share of costs (expenses) of auxiliary production attributable to the construction of fixed assets is reflected |

| Accounting entries for work (services) with VAT provided by third-party organizations for the construction of fixed assets | |||

| 1 | 08-3 | 60, 76 | The cost of consumed works (services) without VAT on investments in non-current assets has been accrued |

| 2 | 97 | 60, 76 | The cost of consumed works (services) without VAT is reflected as part of expenses (expenses) for future periods |

| 3 | 19-1 | 60, 76 | Accounted for (accrued) VAT on work (services) performed by a third party |

| 4 | 60, 76 | 50, 51 | The cost of consumed work (services) for the construction of a fixed asset facility was paid to a third party |

| Accounting entries for works (services) without VAT provided by third-party organizations for the construction of fixed assets | |||

| 1 | 08-3 | 60, 76 | The cost of consumed works (services) with VAT on investments in non-current assets has been calculated |

| 2 | 97 | 60, 76 | The cost of consumed works (services) with VAT is reflected as part of expenses (expenses) for future periods |

| 3 | 60, 76 | 50, 51 | The cost of consumed work (services) for the construction of a fixed asset facility was paid to a third party |

| Accounting entries when creating reserves for future expenses at the expense of capital construction costs (expenses) | |||

| 1 | 08-3 | 96 | Monthly contributions to reserves for future expenses are included in the costs (expenses) of capital construction |

| Accounting entries when writing off deferred expenses for the reporting period (month) for costs (expenses) of capital construction | |||

| 1 | 08-3 | 97 | Current expenses (expenses) of future periods are written off as expenses (expenses) of capital construction |

Reflection in accounting of the correction of the error in writing off the customer's materials for construction and installation work by contractors, if the error was identified in the current year.

| № | Debit | Credit | Contents of operation |

| 1 | 08-3 | 10-7 | The actual cost of materials erroneously written off for the contractor’s construction and installation work was restored (reversed) in the month the error was identified. |

Reflection in accounting of VAT deductions for construction and installation work performed for own consumption.

| № | Debit | Credit | Contents of operation |

| Accounting entries when calculating VAT | |||

| 1 | 19 subaccount “VAT on the construction of fixed assets” | 68 subaccount “VAT calculations” | VAT is charged on the cost of construction and installation work for own consumption performed during the tax period |

| Accounting entries when an organization accepts for deduction of VAT on the volume of construction and installation work in the same tax period in which it was calculated for payment | |||

| 1 | 68 subaccount “VAT calculations” | 19 subaccount “VAT on the construction of fixed assets” | VAT, calculated on the amount of actual expenses for the construction of an object using an economic method, is accepted for deduction at the time of determining the tax base for construction and installation work for own consumption - the last date of each tax period |

Reflection in accounting of the write-off of identified shortages and losses in capital construction in the event of identification of the guilty parties.

| № | Debit | Credit | Contents of operation |

| Accounting entries when writing off shortages (losses) of valuables identified during the inventory of construction projects, as well as shortages of capital investments identified during the construction of fixed assets | |||

| 1 | 94 | 08-3 | The identified amount of actual costs (expenses) of capital construction is reflected, attributable to shortages and losses during the construction of fixed assets. |

| Accounting entries for compensation of valuables according to the loss rate | |||

| 1 | 08-3 | 94 | The loss of valuables was capitalized (reimbursed) - shrinkage, crushing, spraying, etc. within the limits of the norms for capital construction costs |

| Accounting entries for compensation of shortfalls in capital investments and valuables in excess of the loss rate at the expense of the guilty parties | |||

| 1 | 73-2, 76 | 94 | The shortage of capital investments and the loss of valuables in excess of the norm are compensated at the expense of the guilty persons or |

| 70 | 94 | The shortage of capital investments and loss of valuables in excess of the norm is repaid from the wages of the guilty persons | |

| Accounting entries when restoring the amount of VAT on missing values in excess of the norms of natural loss | |||

| 1 | 94 | 68 subaccount “VAT calculations” | The amount of VAT on valuables written off due to their shortage or damage in excess of the norms of natural loss has been restored. The amount of VAT on missing or damaged valuables in excess of the norms of natural loss is reflected in the account of shortages and losses from damage to valuables or |

| 19-394 | 68 subaccount “VAT calculations” 19-3 | The amount of VAT on valuables written off due to their shortage or damage in excess of the norms of natural loss has been restored. The amount of VAT on missing or damaged values in excess of the norms of natural loss is reflected in the account of shortages and losses from damage to valuables | |

| Accounting entries for VAT refunds in excess of natural loss norms at the expense of the guilty parties | |||

| 1 | 73-2, 76 | 94 | The amount of VAT on missing or damaged valuables in excess of the norms of natural loss has been reimbursed at the expense of the guilty persons or |

| 70 | 94 | The amount of VAT on missing or damaged valuables in excess of the norms of natural loss was repaid from the wages of the guilty persons | |

| NOTE. In development of account 94 “Shortages and losses from damage to valuables”, additional sub-accounts can be opened, in particular 94-1 “Shortages and losses from damage to valuables by individuals who are employees of the organization”, 94-2 “Shortages and losses from damage to valuables by individuals who are not employees of the organization”, 94-3 “Shortages and losses from damage to valuables by organizations - legal entities” and 94-4 “Shortages and losses from damage to valuables when the perpetrators are not identified” | |||

Reflection in accounting of the write-off of identified shortages and losses in capital construction in the event of failure to identify the perpetrators.

| № | Debit | Credit | Contents of operation |

| Accounting entries when writing off shortages (losses) of valuables identified during the inventory of construction projects, as well as shortages of capital investments identified during the construction of fixed assets | |||

| 1 | 94 | 08-3 | The identified amount of actual costs (expenses) of capital construction is reflected, attributable to shortages and losses during the construction of fixed assets. |

| Accounting entries for compensation of valuables according to the loss rate | |||

| 1 | 08-3 | 94 | The loss of valuables was capitalized (reimbursed) - shrinkage, crushing, spraying, etc. within the limits of the norms for capital construction costs |

| Accounting entries for compensation of shortages of capital investments and valuables in excess of the loss rate in the event of failure to identify the perpetrators | |||

| 1 | 91-2 | 94 | The shortage of capital investments and loss of valuables in excess of the norm is repaid at the expense of other expenses of the organization |

| Accounting entries when restoring the amount of VAT on missing values in excess of the norms of natural loss | |||

| 1 | 94 | 68 subaccount “VAT calculations” | The amount of VAT on valuables written off due to their shortage or damage in excess of the norms of natural loss has been restored. The amount of VAT on missing or damaged valuables in excess of the norms of natural loss is reflected in the account of shortages and losses from damage to valuables or |

| 19-3 | 68 subaccount “VAT calculations” | The amount of VAT on valuables written off due to their shortage or damage in excess of the norms of natural loss has been restored | |

| 94 | 19-3 | The amount of VAT on missing or damaged valuables in excess of the norms of natural loss is reflected in the account of shortages and losses from damage to valuables | |

| Accounting entries for VAT refunds in excess of the norms of natural loss in the event of failure to identify the perpetrators | |||

| 1 | 91-2 | 94 | The amount of VAT on missing or damaged valuables in excess of the norms of natural loss is repaid at the expense of other expenses of the organization |

Reflection in accounting of the write-off of identified shortages and losses in capital construction due to emergency circumstances.

| № | Debit | Credit | Contents of operation |

| Accounting entries when writing off, due to emergency circumstances, shortages (losses) of valuables identified during the inventory of construction projects, as well as shortages of capital investments identified during the construction of fixed assets | |||

| 1 | 91-2 | 08-3 | The identified amount of actual costs (expenses) of capital construction attributable to shortages and losses during the construction of fixed assets is reflected as other expenses |

| Accounting entries for compensation of identified loss of valuables due to emergency circumstances within the limits of the loss rate | |||

| 1 | 08-3 | 91-1 | The loss of valuables was capitalized (reimbursed) - shrinkage, crushing, spraying, etc. within the limits of the norms for capital construction costs. The loss of valuables according to the norms is reflected in other income of the organization |

| Accounting entries when restoring VAT on written-off valuables in the event of their shortage, damage or damage due to emergency circumstances, if loss rates are determined for valuables | |||

| 1 | 91-2 | 68 subaccount “VAT calculations” | The amount of VAT on valuables written off due to their shortage or damage in excess of the norms of natural loss has been restored. The amount of VAT on missing or damaged valuables in excess of the norms of natural loss is reflected as other expenses or |

| 19-3 | 68 subaccount “VAT calculations” | The amount of VAT on valuables written off due to their shortage or damage in excess of the norms of natural loss has been restored | |

| 91-2 | 19-3 | The amount of VAT on missing or damaged valuables in excess of the norms of natural loss is reflected as other expenses | |

Reflection in accounting of the transfer of project documentation developed by a third party.

| № | Debit | Credit | Contents of operation |

| Accounting entries when reflecting expenses for the acquisition of design documentation for the construction of fixed assets | |||

| 1 | 08 | 60, 76 | The actual cost excluding VAT of the purchased project documentation is reflected as non-current assets |

| 2 | 19 | 60, 76 | VAT is reflected on the purchased design documentation |

| Accounting entries when transferring funds | |||

| 1 | 60, 76 | 51 | The cost of design work has been paid |

| Accounting entries for the sale of project documentation. The enterprise decided that it was inappropriate to use design documentation during the construction of the facility and to sell it to another enterprise at a negotiated price | |||

| 1 | 62, 76 | 91-1 | Revenue from the implementation of project documentation is reflected |

| 2 | 91-2 | 68 subaccount “VAT calculations” | VAT debt to the budget was accrued from the cost of sold documentation |

| 3 | 91-2 | 08 | Actual costs (cost) of project documentation are written off as other expenses |

| 4 | 68 subaccount “VAT calculations” | 19 | Accepted for VAT deduction on project documentation |

| Accounting entries upon receipt of funds | |||

| 1 | 51 | 62, 76 | Payment for project documentation reflected |

Algorithms for calculating average price

Algorithm for calculating the average price, using the example of the “Apple jam” position. Before write-off, there were two receipts of this material:

100 kg x 1,000 rubles = 100,000 rubles

80 kg x 1,200 rubles = 96,000 rubles

The total average at the time of write-off is (100,000 + 96,000)/(100 + 80) = 1088.89 rubles.

We multiply this amount by 120 kg and get 130,666.67 rubles.

At the time of write-off, we used the so-called moving average.

Then, after the write-off, there was a receipt:

50 kg x 1,100 rubles = 55,000 rubles.

The weighted average for the month is:

(100,000 + 96,000 + 55,000)/(100 + 80 + 50) = 1091.30 rubles.

If we multiply it by 120, we get 130,956.52.

The difference 130,956.52 – 130,666.67 = 289.86 will be written off at the end of the month when performing the routine operation Adjustment of item cost (the difference of 1 kopeck from the calculated one arose in 1C due to rounding).

Fig.8 Adjustment of item cost

Materials accounting

In order to control the availability and movement of inventories, a business entity can use both unified forms approved by Decree of the State Statistics Committee of the Russian Federation dated July 30, 1997 No. 71a, and those developed independently, taking into account the requirements for the mandatory details of the primary document (Article 9 of the Law “On Accounting” dated 06.12. 2011 No. 402-FZ) and enshrined in the company’s accounting policies.

Among the unified forms, the most popular are the following:

- demand-invoice;

- invoice for the release of materials to the third party;

- receipt order;

- limit fence card.

Materials are capitalized at the actual cost recorded in the documentation upon receipt. Inventory in an organization is accounted for either at its actual cost of receipt or at accounting prices, which must be enshrined in the accounting policy. When using the 2nd option, you should use account 16 “Deviation in the cost of material assets” and account 15 “Procurement and acquisition of material assets” to reflect the difference between the accounting and actual costs.

Example 1

Retro LLC has enshrined in its accounting policy the need to accept materials at discount prices. A batch of raw materials (granulated sugar) was received for further use in production in the amount of 100 kg for the amount of 4,000 rubles. Accepted accounting (planned) prices for this item are 45 rubles. for 1 kg. The following postings have been made:

| Debit | Credit | Amount, rub. |

| 4 000 | The receipt of raw materials (granulated sugar) from the supplier was capitalized | |

| VAT allocated | ||

| 4 500 | Accepted raw materials at discount prices | |

| The excess of the book value over the actual value is written off |

If the accounting price were less than the actual cost, then the last entry would have the following form:

Dt 16 Kt 15. – the difference in the excess of the cost of goods over the accounting prices is written off.

Example 2

LLC "Raduga" upon receipt of materials capitalizes them at actual cost. When purchasing office supplies (20 pencils for a total of 1,000 rubles), the following entries were made for administrative needs:

| Debit | Credit | Amount, rub. |

| 1 000 | Stationery purchased from supplier | |

| VAT allocated | ||

| 1 000 | Stationery supplies were transferred upon request-invoice for the needs of the administrative apparatus |

After receipt, the materials are written off for production or other general business needs using one of the existing methods, which also must be reflected in the accounting policy:

- By average cost - when writing off, the average price of 1 unit of homogeneous material is formed.

- At the cost of each unit - suitable for a small group of inventories in cases where it is possible to form the cost of each unit.

- Using the FIFO method - this method allows you to take into account the cost of the first received materials in expenses (clause 16 of PBU 5/01).

Important addition

The generation of invoice requirements and their use for write-off requires the fulfillment of an important condition: all materials written off from the warehouse must be used for production in the same month, that is, writing off their full value as expenses is correct. In fact, this is not always the case. In this case, the transfer of materials from the main warehouse should be reflected as a movement between warehouses, to a separate sub-account of account 10, or, alternatively, to a separate warehouse in the same sub-account in which it is accounted for. With this option, materials should be written off as expenses using a materials write-off act, indicating the actual quantity used.

The version of the act printed on paper should be approved in the accounting policy. In 1C, for this purpose, the document “Production Report for a Shift” is provided, through which, for the products produced, you can write off materials manually, or, if standard products are produced, draw up a specification for 1 unit of product in advance. Then, when specifying the quantity of finished products, the required amount of material will be calculated automatically. This work option will be discussed in more detail in the next article, which will also cover such special cases of write-off of materials as accounting for workwear and write-off of customer-supplied raw materials into production.

If you regularly have questions about setting up 1C programs, contact our specialists. We will be happy to advise you and also select the optimal tariffs for 1C service, focusing on your individual tasks.

How to simplify the write-off of materials

Accounting for materials is a labor-intensive process and often causes difficulties for accountants of construction companies. Is it possible to make it simpler and not complete unnecessary paperwork?

Let's talk about this.

Providing materials. Accounting with the general contractor

The situation is as follows. The organization knows for sure that it is buying materials for a specific object - they are immediately shipped there, bypassing the warehouse, which, in fact, does not exist. In this case, the organization is the general contractor. The work is performed by a subcontractor, partly using materials from the general contractor. Is it legal to register the receipt of materials through a receipt order using Form No. M-4 with the following entries: DEBIT 10 CREDIT 60

– materials for the construction of the facility were purchased;

DEBIT 19 CREDIT 60

– value added tax on materials is allocated.

And then immediately write off the building materials through “movement” according to form No. M-11 (“Demand-invoice”) on the date of signing the act of work performed by the subcontractor with the entry: DEBIT 20 CREDIT 10 –

the cost of the materials consumed is written off. And the necessary forms No. M-15 (“Invoice for the release of materials to third parties”) and No. M-29 (“Report on the consumption of basic materials in construction in comparison with the consumption determined according to production standards”) should be drawn up separately and simply attached to the general document flow ? Let us remind you: forms No. M-4, No. M-11, No. M-15 were approved by Decree of the State Statistics Committee of Russia dated October 30, 1997 No. 71a. Form No. M-29 is not unified (approved by the Central Statistical Office of the USSR on November 24, 1982 No. 613).