We will not consider payroll calculations in detail, but will analyze the entries that are generated in accounting after the calculations are completed for each employee.

Stages of work on payroll accounting in an organization:

- payroll;

- deductions from wages;

- calculation of insurance premiums;

- payment of wages;

- payment of personal income tax and contributions.

To record all transactions related to wages, account 70 “Settlements with personnel for wages” is used. The credit of this account reflects accruals, the debit - personal income tax, other deductions and salary payments. Postings for payroll, deductions, personal income tax and insurance contributions are usually made on the last day of the month for which wages are accrued. Postings for salary payments and personal income tax and contributions are made on the day of the actual transfer (issue) of funds.

Payroll

Quick establishment of primary accounts, automatic payroll calculation, multi-user mode, free updates and technical support in the online service Kontur.Accounting!

Get free access for 14 days

Wage expenses are written off against the cost of production or goods, therefore the following accounts correspond to account 70:

- for a manufacturing enterprise - 20 account “Main production” or 23 account “Auxiliary production”, 25 “General production expenses”, 26 “General (administrative) expenses”, 29 “Servicing production and facilities”;

- for a trading enterprise - account 44 “Sales expenses”.

The wiring looks like this:

D20 (44.26,…) K70

This posting is made for the total amount of accrued salary for the month, or for each employee, if accounting on account 70 is organized with analytics for employees.

The procedure for calculating the advance payment is similar. Its date depends on the payment method established in the organization:

1. If the advance is paid in a fixed amount from the employee’s monthly salary, then an entry for calculating the advance is not needed. Make only the monthly payroll entry on the last day of that month;

2. If the advance depends on the time that the employee actually worked in the first half of the month, then, as a rule, additional reserve deductions for personal income tax, alimony and other payments are made. Create an entry for accruing the advance at the end of the first half of the month for which it was accrued. For the same date, create a deduction entry.

Issuing money to persons who are not registered with the enterprise

If, as a result of production needs, it is necessary to issue money to persons who are not full-time employees, then the financial transaction is carried out using separate payment documents issued for each person. It is allowed to include the entire payroll of employees in the list, subject to a previously executed agreement.

The procedure for issuing money from the cash register

The issuance of funds to persons attracted to carry out contract work is carried out according to the statement. The document is drawn up separately for each enterprise from which employees were sent. It is certified not only by the management of the issuing organization, but also by the signature of the responsible employee of the company where the employees are on staff.

Salary deductions

Quick establishment of primary accounts, automatic payroll calculation, multi-user mode, free updates and technical support in the online service Kontur.Accounting! Get free access for 14 days

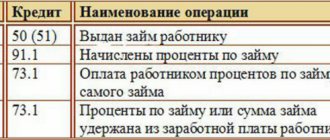

Deductions from salary reduce the amount of accruals and go through the debit of account 70. As a rule, all employees have one deduction - personal income tax. Here account 70 corresponds with account 68 “Calculations for taxes and fees”, posting:

D70 K68

In postings for other deductions and reserve deductions for personal income tax, the loan account changes, depending on where it goes. For example, when withholding under a writ of execution in favor of a third party, account 76 “Settlements with various debtors and creditors” is used, posting:

D70 K76

The accrual and withholding of personal income tax and other payments is made by postings on the last day of the month for which the salary is accrued. Postings for personal income tax payment - on the day the money is written off from the account or issued from the cash register.

What can funds issued from the cash desk be spent on?

The intended use of funds issued from the cash desk of a business entity is regulated by the instructions of the Central Bank of the Russian Federation. If the fact of their spending outside the established directions is recorded, a fine will be imposed on the company by the Tax Service and the servicing banking institution.

The direction of use of money from the cash register depends on the source of its replenishment. The cash register can be replenished through a direct withdrawal of funds from the current account of a business entity. Money can come from accountable persons returning funds that have the status of an advance that were not used for the purposes for which they were issued, or from the founders of the company in the form of a loan. If a company specializes in sales, then cash most often comes from customers.

Trade revenue, determined by the funds contributed by customers for purchased goods or services provided, can be used to a limited extent for the needs of the enterprise and to ensure its functioning.

Wage

You can pay hired workers from the cash register or by transferring the required amount to a card account. When making cash payments, funds can be used from the proceeds or withdrawn from the current account of the business entity. If the company’s employee is a non-resident of the country, then the payment under the wage item falls into the category of foreign exchange transaction, therefore, in order to avoid later troubles, the easiest way is to transfer the money to a bank account.

Money to report

In what situations is cash issued from the cash register?

Accountable money can be issued from funds in the institution’s cash desk, regardless of the source of its replenishment. To receive them you need:

- report on a previous similar operation;

- fill out an application that should reflect goals, amounts and deadlines;

- draw up an order for the release of funds;

- prepare payment documentation.

Legal acts do not regulate the limit amounts for issuance, therefore money in any quantity can be issued under this article, provided that their purpose is properly justified. The procedure for carrying out the operation of issuing funds on account must be regulated in local acts of the business entity covering the scope of accounting policies.

Material aid

Material assistance falls into the category of social benefits for which proceeds can be spent without restrictions. Payment is difficult to plan in advance, since the basis for its implementation is unplanned situations. A financial transaction must be preceded by its formalization, which consists of filling out an application from the employee with justification for the request and the reasons for the application. The document is the basis for drawing up an order, payment documentation and making payments from the cash register.

Debt to supplier

Registration of the procedure for issuing money

Debt to suppliers can be paid from the company's cash desk, regardless of the source of its formation. An exception is payment for rent of premises or equipment, which cannot be realized from cash proceeds. To pay off rent arrears, the head of the company will have to order money from the bank to withdraw from the current account, enter it into the cash register, and after withdrawal, pay the landlord. In order to prevent problematic situations with representatives of inspection authorities, the person responsible for conducting financial transactions must:

- do not exceed the cash payment limit;

- demand from the supplier a receipt confirming receipt of payment;

- keep powers of attorney from the supplier’s representative, executed by its management to receive funds.

Calculation of insurance premiums

Account 70 is not included in postings for insurance premiums, because they are not accrued to employees and are not deducted from their salaries.

Insurance premiums are included in the cost of production, i.e. pass through the debit of accounts 20 (26, 29, ...) or 44 in correspondence with account 69 “Calculations for social insurance and security”. 69 accounts usually have subaccounts for each contribution. Wiring:

Convenient online accounting

Quick establishment of a primary account, automatic payroll calculation, multi-user mode in Kontur.Accounting

Try it

D20 (44, 26, …) K69

Issuing funds from the cash register. Procedure for completing the procedure

The basis for issuing funds from the cash register of an enterprise is an expense cash order.

As an alternative, a financial transaction may be carried out on pay slips, invoices or applications for the issuance of funds. When preparing documents, they require a stamp with the details of the cash order and the signature of the head of the company and the person authorized to approve the accounting documentation. Such details do not need to be filled out if the payment document is accompanied by papers on the basis of which the financial transaction is carried out.

Legislative regulation of the procedure

Companies specializing in the purchase of various products for the purpose of retail resale or use to ensure the functioning of production can pay cash from the cash register to account for the delivered raw materials. For all amounts issued during the daily period, at the end of the working day, a general cash order of an expense nature is issued, in accordance with the information from the receipts confirming the fact of the transaction.

Using account 70 in accounting

Count 70 is passive. On the credit side of the account, settlements with employees are made - the formation of amounts intended for payments to employees, and on the debit side - transactions for deductions from wages.

When making mutual settlements with employees, account 70 provides for the opening of subaccounts. This greatly simplifies the work, since each employee is assigned to a separate sub-account. This provision is purely advisory in nature and is not mandatory; a decision on it is made by the management team and is reflected in the accounting policies of the organization.

Account 70 reflects the flow of material resources for mutual settlements with employees of the enterprise and costs associated with all kinds of obligations of employees. Calculations are carried out for each employee, and then the data is collected into a final reporting sheet for the entire organization.

In the event that an employee does not receive wages on time (for example, due to absence from work), the unclaimed amount is identified as deposited and at the end of the month is transferred to a special separate account.

Account characteristics

To record payroll calculations, account 70 is used. When asked which account 70 is active or passive, you can clearly answer that it is an active-passive account.

Depending on the situation, it can have two balances at once. The debit balance reflects the debt of persons working at the enterprise for the wages paid to them by the enterprise. The loan balance, on the contrary, reflects the employer’s debt to the employees working in the company.

When determining the final account balance, it matters which side the balance is on. If by debit, then the debit turnover reflects the increase in debt, and the credit turnover reflects its repayment.

The opening balance is added to the debit turnover, after which the resulting result must be compared with the credit balance. If the final value of the difference with the loan turnover turns out to be positive, then the final balance is a debit.

When the initial balance of account 70 is on credit, then the increase in debt is reflected on the credit side, and its repayment on the debit side. If the difference between the amount of the opening balance and the turnover on the credit account with the debit turnover is positive, then the ending balance is in credit. Otherwise, at the end of the period, a debit balance of account 70 is obtained.

Attention! The turnover sheet for account 70 can reflect two balances at once. This is due to the fact that subaccounts within it can be either debit or credit, and the synthetic account has a folded double balance.

In the balance sheet, account 70 balances are reflected as follows:

- In the asset as part of current assets on line 1230 as accounts receivable.

- In liabilities as part of short-term liabilities on line 1520 as accounts payable.

You might be interested in:

Postings for payment of dividends to the founder in accounting

What subaccounts are used?

Analytical accounting for account 70 is built for each employee separately. As a rule, information on people is combined into higher subaccounts, which are created for each department in the company.

The Chart of Accounts does not establish subaccounts recommended for opening, therefore it is customary to independently create subaccounts of a higher order with the following grouping:

- Settlements with staff members.

- Calculations under contract agreements.

- Settlements with part-time workers.

- Settlements with disabled personnel.

Interaction with other accounts

Based on the extensive classification of payments and wage deductions, a large number of items of settlements with employees are distinguished. That is why account 70 corresponds with the vast majority of other accounts. We list the main ones:

- By loan — 20, 23, 25, 26, 28, 29, 44, 69, 84, 96;

- By debit — 50, 51, 52, 55, 68, 69, 71, 73, 76, 79, 94.

Receipt of wages by employees in kind is documented by posting to accounts 70 and 90. From the debit of account 70 to the credit of account 90 “Sales”, the amount of wages equal to the amount of goods issued is written off. And also from the debit of account 90 to the credit of account 43 “Finished products”, the transfer of goods (materials, products) to employees is registered.

Purpose of deposited salary: nuances

Let's consider an example of an atypical salary payment scheme - when it comes to depositing funds. What is it?

At some enterprises, salaries are issued through a cash register. This means that to receive it, the employee must personally appear at the enterprise. But for one reason or another, for example due to being on sick leave, he may not have time to arrive for the payment of wages on time.

To ensure that the employee has the opportunity to receive his salary later, the accounting department deposits it - temporarily reserving it for a future payment by returning it to a bank account or placing it in the cash register (in the latter case, you need to monitor the cash register limit).

If deposited wages are generated, then the posting reflecting this fact will look like this: Dt 70 Kt 76.4. The fact of the return of the amount corresponding to the deposited salary to the current account (if such a decision is made) is reflected by the posting: Dt 51 Kt 50. The fact of its payment when the employee applies is shown by correspondence: Dt 76.4 Kt 50.

An employee can receive a deposited salary within 3 years from the date of salary accrual (letter of the Federal Tax Service of Russia dated October 6, 2009 No. 3-2-06/109). If he does not do this, then the payment is written off as non-operating income. This fact is reflected by the posting: Dt 76.4 Kt 91.