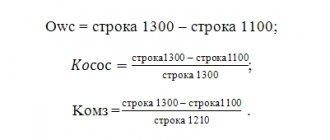

Formula for calculating a company's own working capital

Regularly determining its own working capital in the balance sheet is necessary for every organization that cares about its financial condition and regular increase in profits. This is necessary not only to give the organization financial stability, but also to always be able to assess the financial prospects of the company, making the necessary adjustments. Also, by calculating your own working capital, you can assess the chances of getting rid of all existing short-term liabilities by selling current assets.

The formula for the balance of own working capital is as follows:

This is a general formula that allows you to quickly obtain the necessary information and coordinate the vector of further development of the organization, depending on the data received. This formula is also suitable for calculating funds on a new balance. In this case, you can calculate your own working capital in the balance sheet according to the line:

Moreover, if you do not have any information necessary to carry out calculations, there is a second formula that allows you to find out the necessary data. It is also suitable for both old and new balances:

As an example, we can imagine a conditional company and assume that its short-term liabilities total 5,360 rubles, and its current assets equal 7,500 rubles. In this case, the organization’s own working capital will be 7500 – 5360 = 2140 rubles. This is a positive indicator, indicating that current assets exceed short-term liabilities, which means that the financial viability of the company allows it to confidently move into the future.

Definition

Own working capital (SOC) is the cost of the excess of current assets over short-term liabilities. In another way, this source of financing is called working capital. These are funds that are deposited on the company’s balance sheet and are used to finance current activities.

SOS show how much money a company has, the amount of capital it can freely manage, including to cover short-term liabilities.

Sources of SOS formation:

An alternative algorithm for calculating the amount of own working capital

The formula discussed above is not the only possible one. In economic practice, quite often they use another calculation option using sections 1, 3 and 4 of the balance sheet. It looks like this:

SOK = KR + DP – VA,

where: KR – part of own funds reflected in the section “Capital and reserves”;

DP – long-term liabilities from section 4;

VA – non-current assets from section 1.

The company's equity has a significant impact on the amount of working capital. It is best to consider this dependence with an example.

Example 2

If an entrepreneur who decided to create a company limited himself to the minimum authorized capital provided for opening an LLC, he would have problems with working capital already at the beginning of his activity.

This is due to the fact that the authorized capital of an LLC allowed by law is minimally limited to 10,000 rubles, and this amount is clearly not enough to purchase raw materials, materials or goods, pay for retail or production space, or hire personnel.

A newly minted businessman would have to try hard to find resources to increase working capital

to the required level. A large amount of the authorized capital, on the contrary, removes a significant part of the problems at the stage of starting a business and allows you to fully finance all the current needs of a young company.

In addition to the authorized capital, the company's own funds also include reserve capital, additional capital, retained earnings and additional valuation made on non-current assets. For the 2nd calculation option, Section 4 considers the amounts of long-term loans, borrowings, accounts payable, estimated liabilities, deferred tax liability and other long-term liabilities. We can say that he is fully involved in the formula.

Next, you simply need to add up the data from the indicated articles of sections 3 and 4 and subtract from them the amount of fixed assets, intangible assets from section 1. The result of the calculation will be the amount of own working capital

companies.

To better understand both techniques, it is best to refer to the example described below.

How is SOS and their turnover calculated?

The SOS formula was established by the now inactive FSFO Order No. 31-p dated 08/12/94 and Government Decree No. 498 dated 05/20/94. According to these documents, the formula was established to assess the security of an enterprise. It was used to calculate the level of solvency of the company. The minimum indicator was considered to be a coefficient of 0.1. However, these documents have now been abolished due to the excessive rigidity of the criteria characteristic of the early policies of Russian financial legislation. At the same time, the calculation formula was established on the basis of the English version, so it is successfully used today.

How is the SOS value calculated?

The formula for calculating SOS is:

COC = OA – KO,

Where:

- COC – own working capital;

- OA – assets in circulation of the enterprise;

- KO – obligations with a short duration (less than a year).

How is OS turnover calculated?

The turnover formula looks like this:

KO = OP ÷ CCA,

Where:

- KO – fixed assets turnover ratio;

- OP – indicator of the volume of products sold during the analysis period;

- CCA is the average value of the enterprise's assets during the analysis period.

Example of quarterly calculation of SOS

Let's consider the dynamics of the solvency of the textile manufacturing company Romashka LLC in 2021 based on quarterly reporting.

| No. | Balance indicator | |

| under section II (working capital) | under Section V (current liabilities) | |

| I quarter 2021 | ||

| 1 | 835495 | 575897 |

| II quarter 2021 | ||

| 2 | 1250581 | 995167 |

| III quarter 2021 | ||

| 3 | 1398451 | 1084799 |

| IV quarter 2021 | ||

| 4 | 1189756 | 872183 |

Accordingly, the SOS was:

- SOS Q1 2021 = 835495 – 575897 = 259598;

- SOS II quarter 2021 = 1250581 – 995167 = 255414;

- SOS III quarter 2021 = 1398451 – 1084799 = 313652;

- SOS IV quarter 2021 = 1189756 – 872183 = 317573.

The above calculation shows that the amount of Romashka LLC’s own working capital is always greater than zero. In addition, since the beginning of the year the figure has increased by 57,975 rubles. Accordingly, at the end of 2017, the solvency of Romashka LLC increased.

Determination of net working capital from the balance sheet of an enterprise

The balance sheet is a mandatory form of reporting, which reflects the capital of a business entity and the sources of its origin.

In Russian practice, the balance sheet is divided into two parts: assets and liabilities. An asset reflects the amount of funds that an enterprise uses in its economic activities, and a liability reflects who provided these funds (owners or creditors).

So, using the balance sheet, you can find out the amount of net working capital.

To do this, we find in the balance sheet:

- line 1200 (Section II “Current assets”);

- line 1500 (Section V “Short-term liabilities”).

The required indicator is the difference between 1200 and 1500 lines.

PURE ob.c = page 1200 – page 1500

The sufficient amount of net working capital for enterprises varies; it depends on the scope of economic activity of business entities, the scale of production, and the characteristics of the technological cycle.

But for all organizations there is a general rule for the optimal amount of working capital.

- If the volume of net working capital is large, the enterprise uses its own funds ineffectively (has large inventories, high debtor debt).

- With small amounts of net working capital (or even its negative value), the organization is unable to repay short-term obligations. With such a course of affairs, bankruptcy of the enterprise is possible.

To prevent this situation from occurring, it is necessary to monitor the state of net working capital, systematically analyzing and optimizing it.

Calculation example

For ease of calculation, let’s take the balance sheet data.

It is best to use the first formula with two variables. An example calculation is available. Table 1. Calculation example, thousand rubles.

| Month and year | Line 1200 | Line 1500 | SOS |

| January 2017 | 1 500 | 1 200 | 300 |

| February 2017 | 1 700 | 1 520 | 180 |

| March 2017 | 1 350 | 1 580 | -230 |

| April 2017 | 1 560 | 1 250 | 310 |

| May 2017 | 1 750 | 1 260 | 490 |

| June 2017 | 1 840 | 1 345 | 495 |

| July 2017 | 1 950 | 1 580 | 370 |

| August 2017 | 1 850 | 1 650 | 200 |

| September 2017 | 1 840 | 1 440 | 400 |

| October 2017 | 1 760 | 1 380 | 380 |

| November 2017 | 1 830 | 1 280 | 550 |

| December 2017 | 1 750 | 1 270 | 480 |

| Total for the year | 20 680 | 16 755 | 3925 |

| Average per month | 1 723,3 | 1 396,3 | 327,1 |

Thus, the enterprise has experienced a surplus of its own working capital in all months of 2021, except one. The deficit was noted only in March and amounted to minus 230 thousand rubles. In general, for the remaining months the amount of own working capital was relatively stable. On average for the year, the amount of SOS was equal to 327.1 thousand rubles.

Rice. 1. SOS in dynamics on the chart

Short-term liabilities and working capital

The relationship between a company's current liabilities and the amount of working capital is inverse. In other words, the greater the value of the company's current liabilities, the less the amount of its own working capital.

Section 5 of the balance sheet “Current liabilities” includes 5 positions. Short-term interest-bearing loans and borrowings require the greatest attention from the company's financial service. Their servicing requires the greatest possible accuracy, and any late payments on them entail losses for the company in the form of penalties imposed on it according to the contract.

Unpaid debt to contractors or employees can also cause quite significant financial losses. So:

- Delay in payment of wages may result in the need to incur additional expenses to pay compensation to employees. The Labor Code of the Russian Federation stipulates that its size must be at least 1/300 of the discount rate of the Central Bank of the Russian Federation, and the maximum can be limited only by the conditions specified in the company’s collective agreement. Such payments will increase the enterprise's unproductive costs, and as a result there may simply not be enough financial resources to maintain the technological process.

- Violation of tax payment deadlines or errors in determining their amount also entail the imposition of fines and increased losses for the company.

All such risks must be regularly assessed and measures taken to prevent losses.

Uncontrolled growth of short-term debt leads to an increase in the need for cash, which directly affects the lack of resources to ensure the company's current operations and reduces the size of its working capital.

In addition to the above formula, there is another algorithm for determining the amount of own working capital using other balance sheet indicators. It also needs to be considered in more detail.

Goals for determining the company's own funds

Having calculated the amount of your own working capital, you can first of all determine how much of your own funds is allocated to servicing current assets. In this case, the indicator obtained in this way can take on both positive and negative values or be equal to 0.

If the amount of current assets is less than 0, this indicates the poor financial condition of the company, since the funds available to it are not enough to repay even short-term debts. In the event of minimal market turmoil, it may find itself in an unenviable position.

What are the reasons for this state of affairs? They can be completely different:

- low level of asset management in general;

- excessive passion for investing in non-current assets, in particular in unfinished construction;

- a significant increase in buyer debts;

- lack of profit (asset growth) for a long time;

- other reasons.

An excessively high value of the amount of own working capital should also not be perceived as a positive phenomenon. An excessive value indicates inefficient use of the company's assets. This may be expressed, for example, in attracting bank loans in a larger volume than necessary, or in thoughtless use of net profit. of working capital equal to 0 in newly created companies or firms that actively attract credit resources for current activities.

By regularly examining the level of its own working capital , the company can promptly influence it in order to maintain its optimal value. Measures that improve working capital parameters include:

- reducing material balances in warehouses;

- timely control over the collection of receivables and avoidance of delays.

The list of possible actions is quite wide and should be applied by managers depending on the specific situation based on detailed information about the structure of assets and liabilities.

***

Based on the balance sheet data, you can calculate the amount of your own working capital as of a certain date. For this, there are 2 formulas, each of which gives the correct result, but when using different reporting items. The final amount of calculations fully characterizes the amount of funds allocated for the current financial servicing of the company’s current assets and maintaining its basic detail.

In the process of studying the state and total size of one’s own working capital, one can evaluate the results of its use and develop measures to improve its structure, areas of use, and find ways to increase or, conversely, decrease to the optimal level.

Similar articles

- Working capital in the balance sheet, line

- Working capital financing policy

- Corporate working capital management

- Increase in working capital: calculation

- Net working capital

How to properly manage the CSC?

Working capital needs to be effectively regulated. The best measures in this direction could be:

- assessment of the level and structure of current assets;

- establishing and monitoring compliance with the proportions between long-term and short-term loans, current assets and liabilities;

- optimization of investment in each of the current assets and the structure of balance sheet liabilities;

- formation of an optimal ratio of accounts payable and receivable;

- maintaining company liquidity and monitoring cash flows.

Any company must determine for itself the optimal size of PSC and use it to adjust the amount of current assets and liabilities. This is the only way it can maintain its profitability and solvency at the required level.

Working capital is calculated based on data on the assets and liabilities of the company using simple formulas. But the result obtained without detailed information about the structure and sources of working capital

does not provide much in terms of subsequent analysis. Details are in our article.

SOS analysis

In itself, the indicator of own working capital does not contain any information. It must be analyzed in parallel with inventories as the least liquid assets and other sources of financing (amount of loans, etc.). What is important here is the ratio and its change in dynamics.

The goals of SOS analysis for the head of the company:

- identify the cost of the organization’s fixed working capital;

- determine the amount of surplus or deficit of SOS;

- identify a possible threat to solvency;

- establish how the situation has changed in dynamics.

You can understand whether the company has enough SOS using its own working capital ratio. This indicator is used to determine the insolvency (bankruptcy) of an enterprise.

How to calculate NER: examples

How to calculate the value of the indicator in practice and evaluate the financial condition of the company based on it? It is worth considering several calculation examples.

| Indicator code | Balance sheet item |

| Current assets | |

| Current responsibility | |

| Net Working Capital |

Conclusion! In 2015, the amount of working capital increased. The company's desire to use resources more efficiently next year led to a deterioration in its solvency. In the short term, it may be unable to meet its current obligations.

Figure 1. Dynamics of NWC for PJSC NK Rosneft in 2014-2016, billion rubles.

The dynamics of working capital shows that the Rosneft oil corporation lost its “safety cushion” in 2016.

| Indicator code | Balance sheet item |

| Current assets | |

| Current responsibility | |

| Net Working Capital |

Conclusion! The value of the indicator increases, therefore, the financial stability of the enterprise and its ability to meet its obligations in the short term increases.

Figure 2. Dynamics of NWC for Kamaz PJSC in 2014-2016, million rubles.

The dynamics of the coefficient, calculated on the basis of the balance sheet data of Kamaz PJSC for 2015 and 2021, showed its growth. For such a large engineering giant, which requires a significant amount of resources to ensure stable operation, the growth of NWC is a very favorable trend.

Characteristics of the equity capital of a commercial company

Any type of entrepreneurial activity requires the availability of a certain amount of own funds at the initial stage. As a rule, it consists of founding contributions from one or more business owners in the form of cash, capital goods, cars and real estate. All the company’s work is subsequently built on their basis, since without material support it would simply be impossible. At the same time, each type of asset has a different degree of return during use and can be sold over different time periods.

Let's assume that the production of plastic containers was chosen as a business direction. For this, there are the necessary machines and production areas have been allocated. However, without the availability of free funds in the current account and in the cash register, it will not be possible to purchase raw materials, materials, pay for the services of qualified workers, and the idea will not be able to be implemented.

How to get the necessary amount of money for a successful start and subsequent maintenance of production? There are quite a lot of options:

- obtain a loan at interest from a credit institution;

- borrow from a more successful friend;

- sell off existing “extra” property.

This list does not exhaust all possible options, since human ingenuity is limitless and the emergence of new ideas on how to acquire money is quite possible.

Working capital

necessary to maintain the continuing operations of the company.

It advances it even before receiving the first incoming cash flows at the initial stage and helps to ensure further continuous circulation of materials and resources in production, trade, agriculture or services. Calculating the amount of working capital

gives the entrepreneur information about his business capabilities, his ability to maintain business processes at the proper level, without unforeseen delays and stoppages.

Sources of working capital financing

From the point of view of choosing a source of financing in the working capital of an enterprise, its constant and variable parts are distinguished. The permanent portion is usually financed through long-term debt or equity. In turn, its variable part (for example, seasonal or unexpected needs) is usually financed through short-term sources of debt financing.

- Short-term loan. If a company has a temporary need for additional working capital, a short-term loan (repayment period less than 12 months) is a convenient source of financing.

- Credit line . If the need for additional financing cannot be predicted in advance, a credit line can satisfy it in a short time.

- Factoring. The disadvantage of this source of funding is its high cost, but it can be used when other sources are not available.

- Trade receivables. If an enterprise has a reliable business reputation, its management may ask suppliers to increase the deferred payment, for example from 30 to 40 days. The downside to this source of finance is that an increase in trade receivables is not a good sign for other creditors.

- Financing from own funds. Retained earnings are a widely used source of financing additional working capital requirements. In exceptional cases, owners can provide additional funds by increasing the authorized capital.