The VAT reporting has been submitted, it seems that you can relax... However, not all accountants can breathe a sigh of relief - some of them will have to make changes to the reporting. This is usually a consequence of the fact that errors were identified in the submitted declaration, or documents from the counterparty relating to previous periods were received late.

In this article we will look at cases when it most often becomes necessary to resort to filing an amended VAT return, as well as how to do this and avoid possible sanctions.

Tax legislation requirements

Based on Article 81 of the Tax Code of Russia, an organization is required to submit an updated declaration only if errors and unreported data discovered after filing reports lead to an underestimation of the tax amount .

If the primary declaration contains unreliable or incomplete information that does not lead to an underestimation of the tax amount, then the taxpayer is not required to submit an “adjustment”, although he has the right to do so.

What threatens a company or entrepreneur who has filed an updated declaration? The mere fact of its presentation does not entail sanctions - it all depends on whether unreliable primary data caused an understatement of tax. If this is the case, then the arrears and penalties should be paid before submitting the “clarification”. In this case, according to paragraph 4 of Article 81 of the Tax Code of the Russian Federation, the taxpayer will be released from liability for incomplete payment of tax.

If the arrears are not paid before the tax service finds out about it, a fine may be imposed on the organization in accordance with Article 122 of the Tax Code of the Russian Federation.

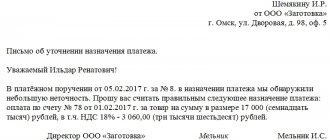

Although the law does not require any explanatory documents to be attached to the updated declaration, it would still be useful to draw up a covering letter . Moreover, when conducting a desk inspection, inspectors will still ask for clarification. The letter should indicate which tax declaration and for what period changes are being made, what erroneous (incomplete or unsubmitted) information is, in which sections and lines of the declaration they are located, as well as provide primary and updated indicators. If errors affected the tax base, a new calculation and tax amount should be provided. In case of payment of arrears and penalties, you should indicate the payment details and, together with the declaration and cover letter, send a scanned copy of it to the tax office.

Technical errors regarding VAT

“Technical” errors are errors that were made not in the invoice, but when registering it in the purchase or sales book.

Technical errors are made precisely when entering information into the database, the so-called “human factor” - gaps, lack of checkpoints for legal entities, presence of checkpoints for individual entrepreneurs, and other problems.

Correction of such errors is carried out depending on how they were detected:

- independently by the taxpayer. The procedure for correcting such errors is not specifically prescribed in the legislation. Such errors are corrected in the standard way - through additional sheets of the purchase or sales book and the submission of an updated VAT return;

- Federal Tax Service during a desk audit. The Federal Tax Service sends a Request for inaccuracies (errors) in the declaration, as a result of which the taxpayer must send Explanations in a uniform format (Order of the Federal Tax Service dated December 16, 2016 N ММВ-7-15 / [email protected] ).

The main mistakes when entering an invoice into the information base:

- in number and date;

- TIN of the counterparty;

- total invoice amount;

- amount of VAT to be deducted.

Specific situations

Now let’s look at common situations in which it is impossible to avoid submitting an updated declaration to the tax service, and also when you can do without it.

Incorrect reporting period

What to do if there is an error in the code of the period for which the declaration was drawn up? The answer is clear - you need to notify the tax service about this error, and as quickly as possible. Otherwise, you can get penalties, and they can be imposed both on the organization (Article 119 of the Tax Code of the Russian Federation) and on the official (15.5 of the Code of Administrative Offenses of the Russian Federation).

Is it necessary to submit a “clarification” in this case? This option is possible, although you may encounter misunderstanding on the part of the Federal Tax Service. They may simply not accept the document, since no primary declaration was filed during the specified period. Or consider the updated declaration as filed for the first time in violation of the deadline, and then the organization may be fined under Article 119 of the Tax Code of the Russian Federation.

It's better to do this:

Declare in writing to the tax office that a return filed with an incorrect period code should be considered submitted for such and such a period (indicating its correct code).

Most often, the Federal Tax Service accepts such explanations and believes that the organization has reported without violations. But if penalties do follow, the organization has a chance to challenge it - in judicial practice there are examples when arbitrators decided such cases in favor of the taxpayer (Resolution of the Federal Antimonopoly Service of the North Caucasus District dated July 30, 2009 in case No. A32-22251/2008- 12/190).

Late documents received

Often in practice there are situations when documents relating to a previous period are received from a counterparty. For example, an invoice for a December transaction can be received as early as January of the following year. In such cases, there is no need to submit a “clarification”, because you can include a “late” invoice in the purchase book in the current period. This rule was introduced at the beginning of 2015 by paragraph 1.1 of Article 172 of the Tax Code of the Russian Federation. Based on it, you can claim VAT deduction for any period within three years from the date of receipt of goods, work or services.

However, this procedure applies only to deductions provided for in paragraph 2 of Article 171 of the Tax Code of the Russian Federation. Other deductions of VAT (for example, paid as a tax agent, on prepayment, etc.) must be declared in the period in which the purchased goods were accepted for accounting, provided they were used to carry out activities subject to VAT.

There was an overstatement of VAT deduction

A situation in which an updated VAT return should definitely be submitted is when, due to an error that has crept in, the tax deduction has been inflated . Indeed, as a result, the amount of tax is underestimated, and this, as was said at the beginning of the article, imposes on the organization the obligation to provide “clarification”. Sometimes this happens due to the fault of the accountant - for example, he registered the same invoice twice or made a technical error when entering information into the accounting system. But this can also be a consequence of erroneous actions by the supplier’s accounting department. Let's say the initial invoice received in the reporting quarter was subsequently corrected and dated to the next period.

Regardless of whose fault it is that the deduction is inflated, an amended return will have to be filed. But before that, you need to correct errors in the purchase book - draw up an additional sheet and enter the correct data into it. Information that is subject to deletion must be written down with a minus sign.

Errors in the purchase book that do not affect the deduction amount

Sometimes in primary documents of past periods you can find technical errors that do not affect the amount of VAT. For example, erroneous indication of TIN, address, name of the counterparty.

By virtue of the aforementioned Article 81 of the Tax Code of the Russian Federation, their presence does not oblige the taxpayer to submit an updated declaration.

However, the tax authorities themselves still recommend doing this, because during a desk audit on VAT, when the data of invoices of counterparties for each transaction is reconciled, these errors pop up, and tax inspectors usually demand clarification.

Receive a corrected invoice

It happens that an accountant discovers errors in the received invoice and asks the supplier to correct them. The latter draws up an adjustment invoice and sends it to the buyer. However, there may be a time gap between these events, and the organization will receive the corrected document in the next quarter.

According to the Federal Tax Service, such an invoice should be registered in the period in which its correct version was received. The deduction previously claimed for it will have to be cancelled, VAT recalculated, its amount and penalties paid, and then an updated declaration submitted.

It is worth noting that this position of the tax service does not find unambiguous support from the arbitrators - they make their decisions both in favor of the Federal Tax Service and in favor of taxpayers.

It should also be remembered that not all erroneous data on invoices can lead to a denial of deduction. Paragraph 2 of Article 169 of the Tax Code of the Russian Federation directly states that if errors do not interfere with identifying the parties to the transaction, the name and cost of the goods, the rate and amount of VAT, then there are no grounds for refusing a deduction on such an invoice. Therefore, before contacting the supplier for an adjustment document, you should make sure that it is necessary.

We send VAT adjustments in the 1C: Accounting program 8th edition. 3.0

In the process of work, every accountant sooner or later encounters various alterations in the accounting of primary documents. Of course, the question arises of how to correctly carry out all the changes in the 1C program so as not to return to it again. There can be many VAT adjustments. In this article we will focus on examples that are most often encountered.

Erroneous duplication in the purchase book

Let's consider the first situation, when in the reporting for the last tax period (second quarter of 2021), we mistakenly duplicated the purchase amount in the purchase book and took the excess for deduction (Fig. 1). The error was discovered late; the declaration had already been submitted.

Any change in the primary documents that entailed a change in the amount of VAT payable or deductible for the previous tax period (quarter) must be recorded with an adjusting VAT return of the same tax period, necessarily accompanied by additional sheets! In this case, the data in section 8 of the corrective VAT declaration (purchase book) remains identical to the original section 8 of the primary declaration.

So, in 1C: Accounting 8th ed. 3.0. we have two identical documents “Receipt of services” with registered invoices for the second quarter (Fig. 2).

We will correct the situation using the reversal method in the current tax period. What does this method mean? We completely record all movements in accounting accounts and registers for the document being reversed and reset it to zero. This operation is automated in the program. To do this, we need to go to the “Operations” section – “Operations entered manually” – create – “Document reversal” (Fig. 3).

In the line “Document to be canceled”, select the extra document “Receipt of services”. Movements on accounts and the “VAT presented” register will be reversed automatically. The accompanying “Invoice received” should be reversed in the same way, since it was through it that the input VAT was accepted for deduction. Here, on the “VAT purchases” tab, you will need to record information that the entry should be included in an additional sheet of the purchase book for the second quarter (Fig. 4).

Incorrect reflection in 1C of the amount or quantity of material assets on the incoming document

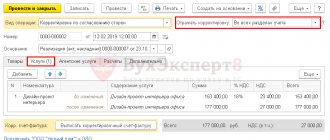

The second option for adjustments, which is very common, is the incorrect reflection in the 1C program of the amount or quantity of material assets according to the incoming document from the supplier and, accordingly, the accepted amount of VAT to be deducted. Let’s say right away that the process of creating an adjustment document in the program is completely automated. We just need to go to the source document for the receipt of goods or services and, based on it, create a document “Adjustment of receipt” (Fig. 5).

For it to be available to the user of the program, full functionality must be available in the “Main” section.

In the “Type of operation” attribute of the document “Adjustment of receipt”, be sure to indicate “Correction of your own error”. It is thanks to him that the corrective entry will be registered in the additional sheet of the VAT return (Appendix 1 to the section of the tax period in which the purchase was originally made and claimed for VAT deduction. If the error is corrected in the same period in which it was made, the corrective a VAT return is not submitted, additional sheets are not generated.

It is thanks to him that the corrective entry will be registered in the additional sheet of the VAT return (Appendix 1 to the section of the tax period in which the purchase was originally made and claimed for VAT deduction. If the error is corrected in the same period in which it was made, the corrective a VAT return is not submitted, additional sheets are not generated.

In the “Reflect adjustment” field, you must select the indicator “In all accounting sections” (with this setting, all changes will be recorded not only in the accounting accounts, but also in the VAT registers, and this is important, since they are responsible for creating the purchase book).

The tabular part, in which we reflect movements on purchased goods and services, will be filled in automatically. In the “After change” line, do not forget to indicate new data on the price and quantity of goods or a different VAT rate (Fig. 6).

And also register the invoice on the “Main” tab. If an error was made in the invoice details, it is corrected in the same way: the correct data must be indicated in the details of the “New value” column. In this case, the “Products” or “Services” bookmarks remain untouched.

In addition, 1C developers have implemented the option of re-editing primary documents and invoices based on existing adjustments.

The terms of delivery of goods have changed

Let's consider the third option for VAT adjustments on the part of the supplier, when no accounting errors were made, the terms of delivery of the goods simply changed (its quantity or price changed, or maybe both).

Unlike the situation when we correct an accounting error, here everything is much simpler in terms of adjustments. There will simply be no need to file a corrective return. All changes will be reflected in the current tax period in the original section 9. To make changes to the implementation, we need to draw up a document “Adjustment of implementation” (Fig. 7). It can be created on the basis of the document “Sales of goods and services”; it is drawn up in the same way as the adjustment described above. However, “Type of operation” in this case will be called “Adjustment by agreement of the parties.”

Don't forget to issue a corrective invoice.

In this article, we looked at how to send VAT adjustments in 1C: Accounting 8th edition. 3.0. We hope you found our material useful. If you have any additional questions about 1C, you can contact our dedicated 1C Consultation Line. We help more than 5,000 Clients per month. We work 7 days a week from 09:00 to 21:00. The first consultation is completely free!

Work in 1C with pleasure!

Algorithm for correcting technical errors

Changes are made to the purchase or sales ledger. If the declaration for the reporting period is submitted, then all changes are made through additional sheets:

- an incorrect entry will be cancelled;

- the correct entry is added.

See also:

- Updated VAT return

- Request from the Federal Tax Service for a “break” in the chain with the counterparty

- The procedure for responding to requirements from the Federal Tax Service for VAT

- The invoice number was entered incorrectly

- Document Adjustment of receipt type of operation Correction of own error

- Procedure for correcting VAT amount errors

- Recording in additional purchase book sheet in 1s 8.3: step-by-step instructions

Did the article help?

Get another secret bonus and full access to the BukhExpert8 help system for 14 days free of charge

Related publications

- The procedure for submitting an updated VAT return...

- The procedure for correcting VAT errors In order to correctly correct a VAT error, you need to understand...

- The procedure for correcting amount errors for VAT From this publication you will learn about the algorithm for correcting amount errors...

- Unaccounted sales of services for the current year, if the accountant did not know about this fact of economic life. You forgot to register the sale in the database and do not understand how to correct it...