From January 1, 2021, the taxation system in the form of a single tax on imputed income ceases to operate in Russia. In this regard, all tax payers (regardless of the region and type of activity) must choose a different taxation regime by the end of the year. One of the possible options is the simplified taxation system (STS).

The object of taxation when applying the simplified tax system is “income” or “income reduced by the amount of expenses” (clause 1 of article 346.14 of the Tax Code of the Russian Federation). The choice of the object of taxation is carried out by the taxpayer himself (except for the case provided for in clause 3 of Article 346.14 of the Tax Code of the Russian Federation), see clause 2 of Art. 346.14 Tax Code of the Russian Federation.

The cost of purchased raw materials and materials when applying the simplified tax system with the object “income reduced by the amount of expenses” is included in expenses at the time of repayment of debt to the supplier (paragraph 1, paragraph 2, paragraph 1, paragraph 2, article 346.17 of the Tax Code of the Russian Federation).

If in 2021 the taxpayer combined UTII and the simplified tax system “income” or used only UTII, then when switching from 2021 to the simplified tax system “income” no special features will arise in accounting for raw materials and supplies, since the costs of their acquisition are not included in the tax base (p 1 Article 346.18 of the Tax Code of the Russian Federation).

If in 2021 the taxpayer combined UTII and the simplified tax system “income” or applied only UTII, and from 2021 will apply the simplified tax system “income minus expenses”, then:

- expenses for the acquisition of raw materials and materials, capitalized and paid during the period of application of the simplified tax system “income” and / or UTII and written off after the transition to the simplified tax system “income minus expenses”, do not reduce the tax base in the period of application of the simplified tax system “income minus expenses” (clause 1 clause 2, clause 4 of Article 346.17 of the Tax Code of the Russian Federation, letters of the Ministry of Finance of Russia dated October 18, 2017 No. 03-11-11/68187, dated July 3, 2015 No. 03-11-06/2/38727);

- expenses for the purchase of raw materials and materials that were capitalized but not paid during the period of application of the simplified tax system “income” and / or UTII reduce the tax base after the transition to the simplified tax system “income minus expenses” on the date of their payment to the supplier (clause 1, clause 2, art. 346.17 of the Tax Code of the Russian Federation, letters of the Ministry of Finance of Russia dated May 26, 2014 No. 03-11-06/2/24949, dated July 3, 2015 No. 03-11-06/2/38727).

In the program "1C: Accounting 8"

the use of UTII for an organization is possible only in conjunction with the main taxation system (STS “income”, STS “income minus expenses” or STS) until 2021. Since from January 1, 2021, the taxation system in the form of UTII will not be applied, with the release of a new release for 2021, the “UTII” checkbox will be removed automatically and will not be available for editing.

Depending on the taxation system used by the organization in 2021 (before the abolition of UTII), when switching from 2021 to the tax system of the simplified tax system “income” or the simplified tax system “income minus expenses”, the following procedure for preliminary settings is proposed for automatic accounting of carryover balances:

| Tax and reporting settings in 2021 | Method for assessing inventories in 2021 (Accounting policy form) | Tax and reporting settings in 2021 | Method for assessing inventories in 2021 (Accounting policy form) | Procedure |

| Simplified (income) + UTII | On average | Simplified (income minus expenses) | By FIFO | 1. Select the taxation system “Simplified (income minus expenses)” (section “Main - Taxes and reports - Taxation system”), apply changes from the period “January 2021” After the new release for 2021 is released, the “UTII” checkbox will be removed automatically and will not be available for editing. 2. Form a batch to account for remaining materials using the “FIFO” method. 3. For the remaining materials, create a document “Entering balances” with the “Entering balances for tax accounting” checkbox checked (uncheck the other boxes), select the generated batch. |

| Simplified (income) + UTII | By FIFO | Simplified (income minus expenses) | By FIFO | 1. Select the taxation system “Simplified (income minus expenses)” (section “Main - Taxes and reports - Taxation system”), apply changes from the period “January 2021”. After the new release for 2021 is released, the “UTII” checkbox will be removed automatically and will not be available for editing. 2. For material balances, create a document “Entering balances” with the “Entering balances for tax accounting” checkbox checked (uncheck the other boxes), select as a batch the document that reflected the receipt of materials. |

| Simplified (income minus expenses) + UTII | By FIFO | Simplified (income) | On average | 1. Select the “Simplified (income)” tax system (section “Main - Taxes and reports - Taxation system”), apply changes from the period “January 2021”. After the new release for 2021 is released, the “UTII” checkbox will be removed automatically and will not be available for editing. 2. When switching to the “Average” method of assessing the inventory, no additional actions are required. |

| Simplified (income minus expenses) + UTII | By FIFO | Simplified (income) | By FIFO | 1. Select the “Simplified (income)” tax system (section “Main - Taxes and reports - Taxation system”), apply changes from the period “January 2021”. After the new release for 2021 is released, the “UTII” checkbox will be removed automatically and will not be available for editing. 2. Since the method of assessing inventories “According to FIFO” does not change, no additional actions are required. |

| Simplified (income minus expenses) + UTII | By FIFO | Simplified (income minus expenses) | By FIFO | Since the basic tax system and the way in which inventories are assessed do not change, no additional action is required. After the new release for 2021 is released, the “UTII” checkbox will be removed automatically and will not be available for editing. |

| Simplified (income) + UTII | On average | Simplified (income) | On average | Since the main tax system of the simplified tax system is “income” and it does not change, no additional actions are required. The method of assessing the MPP in this case does not matter. After the new release for 2021 is released, the “UTII” checkbox will be removed automatically and will not be available for editing. |

| Simplified (income) + UTII | By FIFO | Simplified (income) | By FIFO | |

| Simplified (income) + UTII | On average | Simplified (income) | By FIFO | |

| Simplified (income) + UTII | By FIFO | Simplified (income) | On average |

Accounting for income and expenses under UTII in 2021 is carried out on accounts 90.01.2 “Revenue for certain types of activities with a special taxation procedure” and 90.02.2 “Cost of sales for certain types of activities with a special taxation procedure.” After the abolition of UTII and the transition to the simplified tax system, income and expenses are recorded in accounts 90.01.1 “Revenue from activities with the main taxation system” and 90.02.1 “Cost of sales for activities with the main taxation system.”

If in the program in 2021 the organization combined the simplified tax system and UTII and to automatically reflect income and expense accounts in documents, the item accounting accounts were set up, then they should be deleted.

Example

Akvarel LLC conducts retail trade in goods.

In 2021, the organization combines the main tax system of the simplified tax system with the object “income” and UTII for certain types of activities, the method of assessing the inventory according to the accounting policy is “According to average”. From January 1, 2021, in connection with the abolition of UTII, the organization switched to the simplified tax system with the object “income reduced by the amount of expenses”, the method of assessing inventories is “According to FIFO”.

In this example, consider business transactions:

01/01/2021 — Changing the object of taxation according to the simplified tax system to “income minus expenses”, UTII does not apply.

12/31/2020 — Formation of a batch to account for remaining materials using the “FIFO” method

12/31/2020 — Entering leftover materials for the simplified tax system indicating the batch and batch status

01/14/2021 — Payment to the supplier for the cost of materials purchased in the previous tax period when applying UTII and the simplified tax system with the object “income”

Note! It is important to follow the sequence of entering transactions for accounting for inventories: first enter balances for the simplified tax system, then other transactions (otherwise the Book of Income and Expenses may be filled out incorrectly).

| № | date | Operation | Dt | CT | Sum | Document 1C Create based on | Package of documents Incoming Outgoing Interior |

| 1 | Program settings | ||||||

| 1.1 | 01.01.2021 | Changing the object of taxation according to the simplified tax system to “income minus expenses” | — | — | — | Form "Taxes and reports" | Accounting policy |

| 2 | Entering balances for materials not paid for during the period of application of UTII and simplified tax system “income” | ||||||

| 2.1 | 31.12.2020 | Remains of materials not paid to suppliers were identified | — | — | 11 700,00 | Report "Turnover Balance Sheet" Report "Debt to Suppliers" | Reports “Turnover balance sheet” Report “Debt to suppliers” |

| 2.2 | 31.12.2020 | A batch was formed to account for remaining materials using the “FIFO” method | 41.01 | 41.01 | 11 700,00 | Operation | Accounting information |

| 2.3 | 31.12.2020 | Remaining materials for accounting according to the simplified tax system have been entered | — | — | 11 700,00 | Entering balances | |

| 3 | Payment to the supplier for materials purchased during the period of application of UTII and simplified tax system “income” | ||||||

| 3.1 | 14.01.2021 | The supplier was paid for materials purchased during the period of application of UTII and the simplified tax system “income” | 60.01 | 51 | 15 600,00 | Debiting from current account | Bank statement |

| 4 | Book of income and expenses according to the simplified tax system | ||||||

| 4.1 | 31.03.2021 | The report “Book of Income and Expenses” according to the simplified tax system has been generated | — | — | — | Book of income and expenses | Book of income and expenses |

Program settings

1.1 Changing the object of taxation according to the simplified tax system to “income minus expenses”

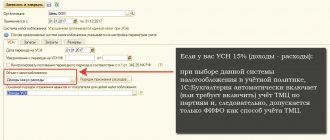

Form “Taxes and reports” (Fig. 1):

- Section: Main

–

Taxes and reports

. - In the list of taxes on the left, place the cursor on Taxation system

, then on the right side of the window follow the link

History of changes

. - Click the Create

, add a new entry, in the

Applies to

, indicate the beginning of the new tax period (“January 2021”) and set the

Taxation system

to the “Simplified (income minus expenses)” position, uncheck the “UTII” checkbox (for the current release, when a new release is released in 2021, this checkbox will be unchecked automatically and will not be available for editing). - Button Record and close

.

Rice. 1

After changing the taxable object, a new entry is automatically created in the Main - Accounting Policies

, in which the switch

Method of estimating the inventory

is set to the “By FIFO” position and is not available for change (Fig. 2).

Rice. 2

Entering balances for materials not paid for during the period of application of the unified income tax and the simplified tax system “income”

Note! Before entering balances, close the 2020 year and perform a balance sheet reformation (processing “Month Closing”). After entering balances, do not close the month for December again.

2.1 Remains of materials not paid to suppliers have been identified

When changing the object of taxation from the simplified tax system “income” to the simplified tax system “income minus expenses”, in order to enter balances for materials and subsequent correct reflection of income and expenses, it is necessary to determine the status of all balances as of December 31 of the year preceding the change in the object of taxation, and indicate it when entering balances in the column State of consumption

:

- Not written off

- the receipt of the asset is reflected in the accounts, the costs of its acquisition are paid to the supplier; - Not written off, not paid

- the receipt of the asset is reflected in the accounting, the costs of its acquisition to the supplier have not been paid; - Not written off, accepted

- the receipt of the asset is reflected in accounting, the costs of its acquisition are recognized as tax accounting expenses according to the simplified tax system.

To determine the status of goods, we will use the reports:

- Account balance sheet

for account 10 (for subaccounts). - Debt to suppliers

;

Report “Account balance sheet” (Fig. 1):

- Section: Reports

–

Account balance sheet

. - Set the period to December 31, 2021, select the account on which goods are recorded (in example 10.06) and generate a report using the Generate

. In the example, as of December 31, 2020, account 10.06 includes: “A4 paper” - 45 pcs. in the amount of RUB 15,600.00;

Rice. 1

Report “Debt to suppliers” (Fig. 2):

- Section: Manager - Debt to suppliers

. - the Period

field to December 31, 2021. - Click the Show settings

on the

Grouping

and select

the Supplier

,

Contract

,

Document

. - Generate

button . - By double-clicking on the cell with the document or with the amount, decipher the unpaid balance to compare it with the balance of materials in the report Account balance sheet

.

Rice. 2

Having analyzed and compared the data from the two reports, we obtain the following summary information as of December 31, 2020:

- materials in balance not paid to suppliers: “Paper 4A” 45 pcs. for a total amount of RUB 11,700.00. (invoice No. 12 dated December 12, 2020, supplier Delta LLC, accounts receivable RUB 15,600.00);

2.2 A batch was formed to account for remaining materials using the “FIFO” method

The document is generated if, in 2021, the tax system “Simplified (income)” and the method of assessing the labor income “According to average” are installed in the program settings. If the method of assessing inventories is “FIFO”, then skip this operation and proceed to operation 2.3.

Document “Operation” (Fig. 3):

- Section: Operations - Operations entered manually

. - Create

button .

Document type - Operation

. - In the from

, indicate the date of the document - December 31, 2021. - Fill out the tabular part using the Add

: In the

Debit

, indicate the goods account (in example 10.06), item and quantity.

When filling out the third subconto, create a new Batch

with the date December 31, 2021 (in the new document, indicate only the date corresponding to the date of the “Operation” document; do not fill in the remaining fields). Select the same document in the following lines of the tabular section when entering balances for other materials. Thus, the remaining goods will be transferred to batch accounting. - In the Credit

, indicate the same data for goods, but without the batch (goods account (in example 10.06), item and quantity). - In the Amount

, indicate the amount of balances for materials. - In the same way, fill in the information for the remaining materials.

.

Rice. 3

2.3 Remaining materials have been entered for accounting for the simplified tax system

Document “Entering balances (Materials)” (Fig. 4-5):

- Section: Main

–

Balance Entry Assistant

. - If the organization previously entered initial balances on the date of start of work with the program (link Date of entry of balances

indicating the date in blue), then for documents

Entering balances

generated on the date of transition to the simplified tax system with the object “income minus expenses”, the date is set directly in each document after unchecking the

Enter accounting balances

.

If the link Set the date for entering balances

is red (i.e., at the beginning of accounting in the information base, documents for entering balances were not created), then follow it and set the date before the start of accounting in the program, and then in the document

Entering balances

after withdrawal

Enter accounting balances

checkbox , set the date to 12/31/2020. - To create a document Entering balances

, double-click the account in the list (account 10 in the example).

In the Enter balances

click the

Create

, then

the Balance entry mode

.

Uncheck the Entering balances for accounting

and

Entering balances for special registers

and click

OK

.

In the from

, indicate/check the date for entering balances – December 31, 2020.

Rice. 4

- Click the Add

to fill out the tabular part of the document.

In the Batch

the Batch

document previously created when filling out

the Operation

document (Fig. 5), (if in 2021 the “FIFO” method of assessing the inventory was used and batch accounting was carried out accordingly, then in this column select the document that reflected receipt of materials). - In the Expense Status

, select the status

Not written off, not paid

, since inventory items were not paid to the supplier in the previous tax period.

In the example: the material “A4 Paper” has not been paid to the supplier - status Not written off, not paid

.

, select the document that reflected the receipt of inventory.

, select

Accepted

.

.

Rice. 5

Click the button to see the result of posting the document - entries have been made in the “Expenses under the simplified tax system” register (Fig. 6).

Rice. 6

Methods for valuing inventories written off for production. Accounting for the write-off of materials into production

The assessment of materials disposed of in production determines the amount of production costs, and, consequently, the amount of balance sheet profit. Therefore, having chosen one of the methods for assessing materials, the organization must consistently follow it during the reporting year, and the change in the assessment method must be justified. The chosen method for valuing disposal materials is fixed in the accounting policies of the organization.

In accordance with clause 73 of PBU 5/01 “Accounting for inventories,” when materials are released into production and otherwise disposed of, they are assessed by the organization in one of the following ways:

a) at the cost of each unit;

b) at average cost;

c) using the FIFO method.

When writing off (selling) materials at the cost of each unit of inventory, two options for calculating the cost of a unit of inventory can be used:

- including all costs associated with the acquisition of stock;

— including only the cost of the stock at the contract price (simplified version).

The use of a simplified version is allowed if it is not possible to directly attribute transportation, procurement and other costs associated with the acquisition of inventories to their cost (for example, with a centralized supply of materials).

In this case, the amount of deviation is distributed in proportion to the cost of written-off (issued) materials, calculated in contract prices.

The assessment of materials supplied at the cost of each unit of stock should be used by the organization in the event that the stocks used cannot replace each other in the usual way or are subject to special accounting (precious metals, precious stones, radioactive substances, etc.).

The main advantage of the method of writing off materials at the cost of each unit is that all materials are written off at their actual cost without any deviations. This method is applicable only in cases where the organization uses a relatively small range of materials, when it is possible to accurately determine which materials are written off.

In cases where it is impossible to accurately track which materials from which particular batch were released into production, it is advisable to use one of the two methods described below.

When writing off (dispensing) materials valued by the organization at average cost, the latter is determined for each group (type) of inventory as the quotient of dividing the total cost of the group (type) of inventory by their quantity, consisting respectively of cost and quantity by balance at the beginning of the month and by incoming inventory this month.

The FIFO method (from the English First In First Out) is based on the assumption that materials are written off to production in the sequence in which they were purchased. Materials from subsequent batches are not written off until the previous one is used up. With this method, materials released into production are valued at the actual cost of materials that were first in date of acquisition, and the balance of materials at the end of the month is valued at the cost of materials that were last in time of acquisition.

In the event that the first lots purchased in time are cheaper, and subsequent ones are more expensive, the use of the FIFO method leads to the following result - materials are written off to production at a lower cost, accordingly, the cost of production is lower and the profit is higher.

If prices for materials tend to decrease, then, on the contrary, if the FIFO method is used, profit will decrease.

There are two ways to determine the cost of materials written off for production using the FIFO method:

1. First, materials are written off at the cost of the first purchased batch; if the quantity of materials written off is greater than this batch, the second batch is written off, etc. The balance of materials is determined by subtracting the cost of written-off materials from the total cost of materials received during the month (taking into account the balance at the beginning of the month).

2. The balance of materials at the end of the month is determined at the price of the most recent purchase.

Payment to the supplier for materials purchased during the period of application of UTII and simplified tax system “income”

3.1 Paid to the supplier of materials purchased during the period of application of UTII and simplified tax system “income”

Document “Write-off from current account” (Fig. 1):

- Section: Bank and cash desk

-

Bank statements

. - Create a document using the Write-off

or open a previously created/downloaded document via “Client-Bank”. - In the Transaction type

, select “Payment to supplier.” - Complete the document. In the example, receivables are paid in the amount of RUB 15,600.

- Carry out

button .

Rice. 1

Click the button to see the result of document processing (Fig. 2).

In the register Book of Income and Expenses (Section I)

(tab of the same name) reflects the amount of payment (column

Expenses in total

), which at the time of posting the document is included in the expenses according to the simplified tax system (corresponding to the balance of materials in the amount of 45 pieces in the amount of 11,700 rubles, including VAT 1950 rubles).

In the register Expenses under the simplified tax system

(tab of the same name) the payment amount reflects the change in status for the material “A4 Paper”:

- The 1st line (movement Expense

) and 2nd line (movement

Receipt

) reflect the change in status -

Not written off, not paid

in the column

Statuses of payment of expenses

changes to

Not written off, accepted

when paying the supplier (thus, for inclusion in expenses under the simplified tax system for this inventory material, two conditions are met: “the goods are received and paid to the supplier).

Rice. 2

The procedure for writing off materials for production.

Clause 16 of PBU 5/01 (as well as clause 73 of the Methodological Guidelines for Accounting

inventories approved by Order of the Ministry of Finance of the Russian Federation dated December 28, 2001 No. 119n) it is determined that when releasing

materials

into

production

, an enterprise for

accounting

can use one of the following methods (methods):

- at the cost of each unit;

- at average cost;

- at the cost of the first acquisition of inventories (FIFO method);

- at the cost of the most recent acquisition of inventories (LIFO method).

A similar list of methods is offered to organizations for tax purposes (clause 8 of Article 255 of Part Two of the Tax Code of the Russian Federation).

In this case, the enterprise has the right to independently choose by what method raw materials will be written off for production (and for other needs). In this case, the chosen method must be recorded in the organization’s accounting policies (both for accounting and tax purposes).

Please note that when choosing a material write-off method, an enterprise should keep in mind the following:

1) this method will be used for all types of raw materials;

2) the chosen method will not change over a long period of time (assuming consistency in the application of accounting policies).

Let's consider the procedure for applying and reflecting in accounting the above methods of writing off raw materials and materials for production.

Issue of materials at cost of each unit

The cost of each unit is used to estimate materials used in a special order (precious metals, precious stones, etc.), as well as inventories that cannot normally replace each other. This method is used only in exceptional cases.

However, this method can also be used by organizations that have a small range of materials.

The above method means that the enterprise evaluates each unit of materials written off (transferred) to production at their actual cost.

It should be recalled that the formation of the cost of materials at an enterprise (regardless of the chosen method for estimating the cost of materials released (written off) into production) can be carried out in two ways:

1) all costs associated with the acquisition (receipt) of materials are reflected in account 10 “Materials” (for each batch of raw materials and materials);

2) costs associated with the purchase of materials are collected on account 15 “Procurement and acquisition of material assets”, and on account 10 are reflected at planned accounting prices.

However, in both the first and second cases, the cost of materials reflected on account 10 will be considered their actual cost, on the basis of which the materials transferred to production will be assessed.

Example

For its production purposes (providing consulting services), a consulting company uses various office supplies as materials, the main part of which is the cost of purchasing paper.

At the beginning of the reporting period, the organization had 10 packs of paper (A4 format) in its warehouse, costing 60 rubles each. During the reporting period (month), another 100 packs of paper were purchased. Of these, 80 packs of A4 format cost 70 rubles each, and 20 packs of A3 format cost 85 rubles each.

During the month, 90 packs of paper were issued to employees (departments) (80 packs - A4 format, 10 packs - A3 format).

Since, in accordance with its accounting policy, the organization records the write-off of materials into production at the cost of each unit, when issuing paper from the warehouse, the invoices must clearly indicate the cost of these materials.

Let's assume that in our example the following amount of paper was issued from the warehouse:

A4 format - 10 packs. x 60 rub.