What is UTII-4

Form UTII-4 is a document that confirms that a businessman wishes to stop paying tax on imputed income, that is, UTII. This paper does not always indicate that the citizen wants to stop engaging in entrepreneurial activity altogether. Perhaps he simply wants to change the tax regime.

Also, filling out this form is required if the limits for individual entrepreneurs on a single tax are exceeded. In this case, a transition to a new regime is necessary. When drawing up the document, the reason for stopping the payment of imputation must be indicated.

Where can I download the UTII-4 form for free?

You can download UTII form 4 for free on our website (see link below).

Read about what other responsibilities a citizen has after being deregistered as a UTII payer in the material “Deregistered as a UTII payer? .

” You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

Filling out the form correctly in 2021

To fill out, you must first download and print the application for withdrawal from UTII IP for 2021. You need to fill it out with a blue or black pen. Features of document preparation:

- letters must be written in capitals;

- each column corresponds to only one character;

- they do not leave empty fields, but put dashes in them;

- Full name is indicated in the nominative case;

- All types of activities must be registered;

- the document should not contain errors or typos;

- You cannot cover up imperfections with a stroke or remove them with an eraser; you will have to fill out the form again.

Important! The application must carefully indicate the reason for deregistration. If you select the value under code “4”, this means that the citizen wants to stop paying tax not on all types of work, but only on specific ones.

The reason for stopping payment of UTII tax is indicated by the appropriate code:

- “1”, if the businessman completely leaves business;

- “2”, if a citizen wishes to change the tax payment regime;

- “3”, if the entrepreneur committed violations of the conditions for applying the UTII regime, for example, the number of workers exceeded 100 people;

- “4” in other situations.

The law does not prohibit filing an application through a representative. But in this case, it is required to indicate in the document the presence of a power of attorney from the individual entrepreneur.

Sample for individual entrepreneurs

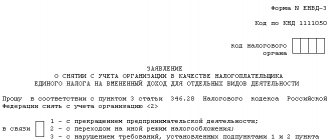

To correctly fill out Form 4 UTII, a sample form for individual entrepreneurs can be viewed on the Internet. The document has a strictly regulated form, consisting of 2 sections.

The first includes the title page. It contains the following information:

- Personal data of an individual entrepreneur.

- INN, OGRNIP.

- A code indicating the reason why you need to remove it from UTII.

- The date from which activities under this regime cease.

- List of papers attached to the application.

- Date of document preparation and signature.

The second section is applications. Their number directly depends on how many types of activities the businessman wants to close according to imputation. The application states the following:

- Type of work.

- IP address.

- Applicant's signature.

Important! It is allowed to enter no more than 3 types of business activities on one sheet.

XLS file

If you have any doubts about the correctness of filling out the application, it is better to write it directly at an appointment with a tax inspector. This is convenient, since you can clarify or ask something at any time.

Filling Features

- When printed, fill out the form with a blue or black ballpoint pen. For electronic reporting, the 18-point Courier New font is used. Letters are in capitals.

- In all graphs there is one character per field. There are dashes in empty fields.

- Choose your reason for filing carefully. Value 4 (other) assumes that the individual entrepreneur closes only certain specific types of activities, leaving others on UTII.

- All full names (individual entrepreneur and his representative, if any) are indicated in the nominative case.

- If the form is submitted not by an entrepreneur, but by an authorized person, it is necessary to indicate the contact information of this person and the name of the document that allows the individual entrepreneur to submit.

- In the appendix we indicate all types of activities. If there are more than three, we print more attachments on the title page (in the column “The attachment to the application is compiled on... pages”).

- Activity codes can be found here. It is worth remembering that they do not comply with OKVED.

In the example, we have one type indicated; in all others on the form, we fill in the empty cells with dashes, as shown in the example.

Application deadlines

The deadline for submitting an application for deregistration of UTII is strictly regulated by law. The following periods are provided:

- 5 days from the day the businessman ceased to operate, if the citizen voluntarily decided to close the business or apply another tax;

- 5 days from the last day of the month of the tax period when violations occurred on the part of the individual entrepreneur, if termination of activities is a compulsory measure.

Note! In the UTII 4 application, it is required to indicate the date when the citizen stopped his work under imputation. This will be the date of deregistration.

Appendix to form No. UTII-4

Attention! The application is filled out only if the individual entrepreneur indicated code “4” as the reason for deregistration.

Line "TIN"

, as well as the page serial number are filled in automatically.

In the field “Code of type of entrepreneurial activity”

the code of the corresponding type of activity is selected from the directory.

In the field “Address of place of business activity”

the address at which the individual entrepreneur will conduct the imputed activity is indicated: postal code, region code, city, street, etc.

Attention! It is not allowed to indicate the address of the place of business activity without indicating the code of the type of business activity.

How to quickly deregister on UTII-4

Submission of an application for withdrawal from UTII from an individual entrepreneur is carried out both personally and through a representative. In the latter case, a power of attorney is required to perform this action on behalf of the businessman.

They submit documents to the tax office, where the entrepreneur is registered as a payer of the imputed tax fee. If a citizen works in different localities, he will have to visit each local tax office separately.

If a businessman works within one city, then all types of businesses that need to be closed can be combined into one application.

Removal from “imputed” registration: in what cases is it carried out?

In fact, the law provides a business entity with:

- the right to independently choose the tax regime used to fulfill obligations to the budget (if the taxpayer meets the established criteria);

- the right to refuse to apply one or another preferential tax regime;

- the right to switch to the tax payment regime that is most beneficial for the taxpayer, if the latter considers this transition expedient, by writing an application for withdrawal from UTII to the Federal Tax Service at the place of registration.

Tax legislation identifies three main reasons why a legal entity may apply for a waiver of imputation. These include:

- termination of activities carried out on UTII;

- violation of the conditions for the application of the “imputed” regime established by Art. 346.26 Tax Code of the Russian Federation;

- transition to another tax system.

The exclusion of a taxpayer from the “imputed” category is carried out by the Federal Tax Service, where the organization must submit an application for termination of UTII, completed in accordance with the approved rules.

To refuse the “imputed” special regime, the legal entity draws up a UTII-3 application in a standardized form and submits it to the inspectorate that registered the “imputed” person.

Serving options

There are several ways to send deregistration documents:

- Personally visit the tax office and hand over UTII-4 to the employees in 2 copies. The specialist will check the correctness of the document. If everything is in order, he returns one copy, having previously marked acceptance.

- Through the post office. It should be sent by a valuable letter, making an inventory of the attachment. It is important that the documents arrive on time, so you need to send the application taking into account the sending time.

Deregistration of UTII is carried out immediately. The starting point is the date that the taxpayer indicated in the application.

The Federal Tax Service told what to do after the cancellation of UTII

Good afternoon, dear colleagues.

The Federal Tax Service of Russia issued a really great letter. I recommend studying it, because most likely you will find it useful.

Letter of the Federal Tax Service of Russia dated November 20, 2020 No. SD-4-3/ [email protected] “On sending clarifications in connection with the abolition of UTII”

We all know that from January 1, 2021, UTII will be cancelled. In this letter, tax officials very well explain various situations related to the abolition of UTII.

What taxation regime can UTII taxpayers switch to after its abolition?

In this letter, tax officials tell you which tax regime you can switch to after the abolition of UTII. Naturally, they mention OSN, simplified tax system 6% or 15%, PSN (patent taxation system).

If you have a very microscopic business and you work alone, then you can switch to PIT (professional income tax). But the turnover here is very low, and you will not be able to recruit employees.

On the issue of the need to submit an application for deregistration as a UTII taxpayer in connection with the abolition of this taxation regime

“Deregistration of organizations and individual entrepreneurs registered with the tax authorities as UTII taxpayers will be carried out automatically (letter of the Federal Tax Service of Russia No. SD-4-3 / [email protected] dated 08.21.2020).”

To which tax authority is it necessary to submit a tax return for UTII for the 4th quarter and in what period after 01/01/2021

“The UTII taxpayer is obliged to submit tax returns based on the results of the tax period no later than the 20th day of the first month of the next tax period (clause 3 of Article 346.32 of the Code).

Payment of UTII is made by the taxpayer based on the results of the tax period no later than the 25th day of the first month of the next tax period to the budgets of the budget system of the Russian Federation at the place of registration with the tax authority as a taxpayer of UTII in accordance with paragraph 2 of Article 346.28 of the Code (paragraph 1 of Article 346.32 Code).

Thus, the UTII tax return for the 4th quarter of 2020 must be submitted no later than January 20, 2021, and the tax must be paid no later than January 25, 2021.”

From 2021, UTII does not apply. What is the procedure for the transition of UTII payers to the use of the simplified tax system?

First of all, you need to submit an application to switch to a simplified system no later than December 31, 2021. Because if you do not submit an application to switch to a special tax regime, you will automatically be transferred to the OSN. The application must be submitted to the same tax authority where you were registered.

The organization applies two taxation systems: UTII and simplified tax system. According to the criteria established by Chapter 26.2 of the Code, the organization will not have the right to apply the simplified tax system in 2021. Do I need to report this?

“If the taxpayer fails to comply with the conditions for applying Chapter 26.2 of the Code in 2021, including for income, including income from activities for which UTII was previously applied, the taxpayer loses the right to apply the simplified tax system and is obliged to report this to the tax authority in the above order.”

On the issue of the need to notify the tax authority about the transition to the use of the simplified tax system by taxpayers combining UTII and simplified tax system

“Taxpayers who previously notified the tax authority about the transition to the simplified tax system are recognized as taxpayers applying the simplified tax system even after 01/01/2021, including for income that was subject to UTII before 2021. In this regard, there is no need to submit a second notification about the transition to the simplified tax system.”

It would be a little unprofessional of me if I didn't go into detail about this. I already grabbed only separate pieces, so let's look at a couple of the most interesting points, perhaps related to OSN. And if you previously worked for UTII, study this letter yourself.

On the issue of taxation by an organization of income received during the period of application of the general taxation regime from the sale of goods purchased during the period of application of UTII

First you need to separate the cash method from the accrual method. If we are talking about the cash method, provided that your company’s turnover was less than 1 million rubles per quarter, then:

“If on average over the previous four quarters the amount of revenue from the sale of goods (work, services) of these organizations without value added tax (hereinafter referred to as VAT) did not exceed one million rubles for each quarter, then in accordance with paragraph 1 of Article 273 of the Code, the organization has the right determine income (expenses) using the cash method.”

That is, the amount of sales of goods that she bought on UTII, but will sell on OSN, forms the taxable base for income tax as money is received. But if it was the accrual method, then it doesn’t matter when the money arrived. If you have shipped goods that you purchased before January 1, 2021 (at UTII), then you have a tax base and immediately have the opportunity to put this entire business on costs.

If you had an advance payment (cash method), which was made back in December, and the shipment will be in January, then:

“In accordance with subparagraph 1 of paragraph 1 of Article 251 of the Code, when determining the tax base for corporate income tax, income in the form of property, property rights, work or services that are received from other persons in the order of advance payment for goods (work, services) by taxpayers is not taken into account , which determine income and expenses on an accrual basis.

<�…>

Consequently, for taxpayers using the accrual method, income from the sale of goods (work, services) in respect of which an advance was received (payment, partial payment) during the period when the taxpayer applied UTII is taken into account for the purpose of calculating corporate income tax during the period when he applied the general taxation regime "

At one time, the Ministry of Economic Development, having received documents from Titov’s business ombudsman service, sent a letter to the Ministry of Finance. In this document, the Ministry of Economic Development asked the Ministry of Finance not to abolish UTII, but to initiate a law to extend this special regime at least until 2024. The Ministry of Finance wrote in response that the UTII will be canceled anyway. Because, as the Ministry of Finance wrote (I’ll say it in simple words): “Now we can control every penny on the territory of the Russian Federation. And since we can do this, then why should we leave UTII? We had UTII for those times when we could not control financial flows. Now everything is under control and we can collect taxes on every transaction. We are canceling UTII so that the budget receives more taxes.”

The Ministry of Economic Development wrote in its letter that if UTII is cancelled, the taxpayer will be forced to switch, for example, to the simplified tax system. And taxes for this businessman will increase from 50% to 300%. And if the taxpayer is forced to switch from UTII to OSN, then his taxes will increase by 3-7 times, that is, by 300-700%.

Survey

Don't you think that these figures from the Ministry of Economic Development were inflated? Do you already have your own calculations? Have you considered how much your taxes will increase? Please write your calculations in the comments. It is important. Businessmen should know what is happening with their neighbor and what to prepare for. In the end, it is not even the businessman who will suffer, but the end buyer. The consumer will pay for everything.

Apparently, businessmen will be forced to raise prices, but there is another problem. We are hitting the ceiling of effective demand. Because the economy is a little stagnant. Solvency simply falls. For example, recently the head of the Accounts Chamber (former Minister of Finance), Mr. Kudrin, said that as of this fall, at least 1/3 of Russian micro, small and medium-sized businesses will go bankrupt due to the second wave of the coronavirus pandemic. Based on this complex of factors, UTII residents will also face an increase in taxation.

Please tell me in the comments what you think about it. And if you need tax optimization services, then contact my specialists. We've been doing this for almost 20 years.

Thank you and good luck in your business.

Late submission of form

The legislation strictly regulates the deadline for filing an application for termination of UTII. Therefore, violation of the established period entails administrative liability. Failure to notify a government organization in a timely manner may result in a small fine of 200 rubles.

At the same time, lawyers warn that if an entrepreneur continues to be registered as a UTII payer, then he will have to pay the tax in full for the entire time that he kept silent about the termination of imputation activities, for example, for a quarter or even for a calendar year.

If he files a zero return, this may be perceived by tax officials as an attempt to evade paying taxes. Such a charge will result in more severe fines.

Thus, the UTII-4 form is a document that indicates the termination of the activities of an individual entrepreneur under the imputed tax regime. The paper is filled out according to a strict form and must be submitted to the Federal Tax Service in the manner and within the time limits established by law.

What is the deadline for submitting an application to deregister a UTII payer?

The current rules of law determine that an entrepreneur must be deregistered as a UTII payer within five days from the date of termination of activity or transition to another taxation system.

To do this, the individual entrepreneur must send a tax application, for which the UTII-4 form is provided. For these purposes, LLC uses the UTII-3 form.

An entrepreneur may stop using imputation for the following reasons:

- Termination of the area of activity in which the UTII system was installed.

- Closing the individual's individual entrepreneurial activity as a whole.

- Violation of the criteria for using the UTII system.

- Changing the tax system used to another.

Attention!

If an entrepreneur decides to change the applicable regime, he must take into account that the use of the new taxation system in some cases is possible only from the beginning of the year. Therefore, a situation may arise that the individual entrepreneur left the imputation, but, for example, could not switch to a simplified taxation system. In this case, a common taxation system will automatically be established.

Having received this application, the tax office must consider it within five days, and at the end of this period, issue a notice to the entrepreneur about the closure of the UTII.