Accounting software under the simplified tax system: postings

Accounting for the company's software is regulated by the basic accounting standards - the Law “On Accounting” dated December 6, 2011 No. 402-FZ and PBU 14/2007. When purchasing exclusive rights to software, the company becomes the owner of the program. If the software meets the criteria for an intangible asset specified in clause 3 of PBU 14/2007 (the object is separated from other assets, is used in the company’s activities for more than a year, is capable of bringing benefits to the company, its value is reliably determined, and its sale is not expected within a year), then it is accounted for at actual cost as part of intangible assets on account 04. Costs incurred will be written off by monthly depreciation over the useful life period established by the company. The service life of the software is determined based on the period of time when the operation of the asset is most profitable for the company, and can be reviewed annually.

Initially, the costs of purchasing software are accumulated in accounting on the account. 08 (D/t 08 - K/t 60, 76), and upon commissioning they go to the debit of the account. 04 (D/t 04 - K/t 08). Write-off of the cost of software is fixed by depreciation every month during the useful life - D/t 20.26, 44 - K/t 05.

If the program was purchased under a simple (non-exclusive) license, this means that the company received the right to use the software for a certain time, and the right to dispose of it remains with the developer. Since the program will not be the property of the company, it cannot be recognized as an intangible asset. In this case, the costs of its purchase are reflected as follows:

- deferred expenses (FBP) (D/t 97 – K/t 60, 76) and are written off evenly every month if the purchase is paid for in a one-time payment (D/t 20,26,44 – K/t 97);

- current expenses, if the company makes periodic payments for using the program (D/t 20.26.44 – K/t 60.76).

The estimated cost of the purchased license is taken into account on the company's balance sheet, for example, in the debit of account 012. Software costs are written off in the manner prescribed by the company, after commissioning and documentation of the installation of the program. Expenses for installing, configuring, and maintaining software are recognized in accounting as current costs and are written off in the reporting period when they were incurred (D/t 20.26.44 – K/t 60.76).

Income minus expenses: features for the simplified tax system

What conditions must companies fulfill in order to apply the special regime? Which expenses need to be taken into account and which ones should not? What rate should tax beneficiaries apply? And how to fill out the Income and Expense Accounting Book in 1C without errors?

Let's answer all these questions today.

A special list of non-accounted payments has been formed. Inspectors pay special attention to them. And if you do not take into account all the important points, you can receive additional taxes with penalties and fines.

According to the current law, the taxpayer independently chooses the object of taxation. This does not apply to participants in a simple partnership agreement or trust management of property. They are required to pay a single tax only on income reduced by the amount of expenses (Article 346.14 of the Tax Code of the Russian Federation).

What do companies need to do using the simplified tax system?

In order for you to use the special mode, the following conditions must be met:

- income limit from the beginning of the year - 150,000,000 rubles;

- the maximum cost of fixed assets is RUB 150,000,000;

- the share of legal entities in the authorized capital is no more than 25 percent;

- there are no branches.

Keep in mind that the rate and how the tax is calculated depends on the property. The rate is higher for those who take into account expenses.

Be sure to check before the end of the year whether the income limits for the year have been exceeded, as well as the cost of fixed assets and the number of employees. If it turns out that the numbers exceed the norm, then next year you will not be able to use the special regime.

What expenses should be taken into account for the “income minus expenses” object?

With a simplified system, it is possible to reduce the tax base only for those expenses that are indicated in the closed list of paragraph 1 of Article 346.16 of the Tax Code of the Russian Federation.

The most important types of costs are taken into account here (for the purchase of fixed assets, materials, goods, labor, etc.).

Before you recognize an expense, find out if it's on the list.

If the costs are in the list, then you need to make an entry in the Accounting Book when you pay the costs and fulfill other conditions (clause 2 of Article 346.17 of the Tax Code of the Russian Federation). Be extremely careful. Inspectors will pay attention to all shortcomings.

List of expenses under the simplified tax system, income minus expenses - 2021 with explanation

| No. | Type of consumption |

| 1 | Expenses for the acquisition, construction and production of fixed assets, as well as for the completion, retrofitting, reconstruction, modernization and technical re-equipment of fixed assets |

| 2 | Expenses for the acquisition of intangible assets, as well as the creation of intangible assets by the taxpayer himself |

| 3 | Expenses for the acquisition of exclusive rights to inventions, utility models, industrial designs, programs for electronic computers, databases, topologies of integrated circuits, production secrets (know-how), as well as rights to use the specified results of intellectual activity on the basis of a license agreement |

| 4 | Expenses for patenting and (or) payment for legal services to obtain legal protection of the results of intellectual activity, including means of individualization |

| 5 | Expenses for scientific research and (or) development work, recognized as such in accordance with Article 262 of the Tax Code of the Russian Federation |

| 6 | Expenses for repairs of fixed assets (including leased ones) |

| 7 | Rental (including leasing) payments for rented (including leased) property |

| 8 | Material costs |

| 9 | Labor costs, temporary disability benefits |

| 10 | Costs for all types of compulsory insurance of employees, property and liability, including insurance premiums |

| 11 | VAT amounts on purchased and paid goods (works, services) |

| 12 | Interest paid for the provision of money (credits, borrowings) for use. Expenses for services provided by credit institutions, including those related to the sale of foreign currency when collecting taxes, fees, penalties and fines from the taxpayer’s property |

| 13 | Expenses for ensuring fire safety, property protection services, servicing fire alarms, purchasing fire protection services and other security services |

| 14 | Amounts of customs duties paid when importing goods into the territory of the Russian Federation and other territories under its jurisdiction and not subject to refund to the taxpayer |

| 15 | Costs for maintaining official transport, as well as expenses for compensation for the use of personal cars and motorcycles for business trips within the limits established by the Government of the Russian Federation |

| 16 | Travel expenses |

| 17 | Payment to a public and (or) private notary for notarization of documents |

| 18 | Expenses for accounting, auditing and legal services |

| 19 | Expenses for publication of accounting (financial) statements |

| 20 | Stationery costs |

| 21 | Expenses for postal, telephone, telegraph and other similar services, expenses for payment of communication services |

| 22 | Purchase costs: acquisition of the right to use computer programs and databases under agreements with the copyright holder (licensing agreements). These costs also include costs for updating computer programs and databases. |

| 23 | Expenses on advertising of manufactured (purchased) and (or) sold goods (works, services), trademark and service mark |

| 24 | Expenses for the preparation and development of new production facilities, workshops and units |

| 25 | Amounts of taxes and fees paid. An exception is the simplified tax and VAT listed according to the rules of paragraph 5 of Article 173 of the Tax Code of the Russian Federation |

| 26 | Expenses for payment of the cost of goods purchased for further sale, as well as costs associated with the acquisition and sale of these goods, including costs for storage, maintenance and transportation of goods |

| 27 | Expenses for payment of commissions, agency fees and fees under agency agreements |

| 28 | Costs of providing warranty repair and maintenance services |

| 29 | Costs for confirming the compliance of products or other objects, production processes, operation, storage, transportation, sales and disposal, performance of work or provision of services with the requirements of technical regulations, provisions of standards or terms of contracts |

| 30 | Costs of conducting a mandatory assessment of the correctness of tax payment in the event of a dispute regarding the calculation of the tax base |

| 31 | Fee for providing information on registered rights |

| 32 | Expenses for paying for the services of specialized organizations for the production of documents for cadastral and technical registration (inventory) of real estate (including title documents for land plots and documents on land surveying) |

| 33 | Costs of paying for the services of specialized organizations for conducting examinations, surveys, issuing opinions and providing other documents, the presence of which is mandatory for obtaining a license (permit) to carry out a specific type of activity |

| 34 | Legal costs and arbitration fees |

| 35 | Periodic (current) payments for the use of rights to the results of intellectual activity and rights to means of individualization (in particular, rights arising from patents for inventions, utility models, industrial designs) |

| 36 | Entrance, membership and target fees paid in accordance with Federal Law of December 1, 2007 No. 315-FZ “On Self-Regulatory Organizations” |

| 37 | Costs of conducting an independent assessment of qualifications, training and retraining of personnel on the taxpayer’s staff |

| 38 | Costs for servicing cash register equipment |

| 39 | Costs for removal of solid waste |

| 40 | The amount of payment to compensate for damage caused to public roads of federal significance by vehicles with a permissible maximum weight of over 12 tons, registered in the register of vehicles of the toll collection system |

In addition to the list from the table, there are three more cost requirements:

- They must meet the criteria of paragraph 1 of Article 252 of the Tax Code of the Russian Federation, which means they must be justified and documented.

- They must be paid (clause 2 of Article 346.17 of the Tax Code of the Russian Federation).

- They need to be carried out (to receive goods, to use services, to accept work).

What cannot be taken into account when simplifying in 2018?

If you did not find your expenses either in the closed list or in other laws, you cannot take them into account when calculating the amount of the simplified tax.

| Type of consumption | Why can't it be taken into account? |

| Electronic signature for participation in tenders in government procurement | Letter of the Ministry of Finance of Russia dated 08.08.2014 No. 03-11-11/39673 |

| Special assessment of jobs | Letter of the Ministry of Finance of Russia dated June 30, 2014 No. 03-11-09/31528 |

| Insurance for rental premises | Letter of the Ministry of Finance of Russia dated May 20, 2009 No. 03-11-09/179 |

| Cost of drinking water for workers | Letter of the Ministry of Finance of Russia dated December 6, 2013 No. 03-11-11/53315 |

| Purchase and redemption of land plots. You can only take into account expenses if you bought land for resale | Letter of the Ministry of Finance of Russia dated 08/07/2017 No. 03-11-11/50441 |

| Costs for the right to install advertising structures | Letter of the Federal Tax Service of Russia dated August 6, 2014 No. GD-4-3/15322 |

| Organizational management expenses | Letter of the Ministry of Finance of Russia dated January 20, 2017 No. 03-11-06/2/2506 |

| Costs for delivery of unclaimed goods by mail | Letter of the Ministry of Finance of Russia dated May 30, 2016 No. 03-11-06/2/31125 |

| Entertainment expenses, corporate events for employees and clients, recruitment agency services, marketing services | In paragraph 1 of Art. 346.16 of the Tax Code of the Russian Federation there are no such expenses |

Tax rate for simplified tax system income – expenses

In 2021, with the simplified tax system for income minus expenses, the basic rate is 15%. But you need to take into account the fact that regional authorities can reduce the rate to 5 percent.

In addition, for start-up entrepreneurs who work in the production, social or scientific fields, as well as in the provision of household services to the population, the tax rate can be reduced to 0.

Also, for organizations and entrepreneurs in Crimea and Sevastopol, regional authorities have the right to reduce the rate to 3 percent. In Crimea and Sevastopol, for the object “income minus expenses” in 2021, the rate is 10% (part 2 of article 2.1 of the Law of the Republic of Crimea dated December 29, 2014 No. 59-ZRK/2014, subparagraph 3 of part 1.1 of article 2 of the Law Sevastopol dated 02/03/2015 No. 110-ЗС). In addition, for organizations and entrepreneurs who operate in the field of agriculture, fish farming, education, healthcare, recreation and entertainment, the rate is 5/% (Part 1, Article 2 of the Law of Sevastopol dated November 14, 2014 No. 77- ZS).

Accounting for income and expenses in 1C

All taxpayers using the simplified tax system are required to keep a book of income and expenses (KUDiR). Otherwise, you can receive a considerable fine (Article 120 of the Tax Code of the Russian Federation). A fine will also be imposed if the book is filled out incorrectly.

Filling out KUDiR in 1C: Accounting 3.0

To begin, in the accounting policy setup form, go to “Setting up taxes and reports.”

Next, you need to select the “Simplified (income minus expenses)” tax system.

Now you can go to the “STS” section of this setting and configure the procedure for recognizing income. This is where it is indicated which transactions reduce the tax base. If you have a question why an expense does not fall into the book of expenses and income in 1C, first of all look at these settings.

Some items cannot be unchecked as they are required to be filled out. The remaining flags can be set based on the specifics of your organization.

We set up the printing of KUDiR itself. To do this, in the “Reports” menu, select the “STS Book of Income and Expenses” section of the “STS” section. The ledger report form will open in front of you. Click on the "Show Settings" button. If you need to detail the records of the received report, check the appropriate box.

Before forming KUDiR in 1C: Accounting 3.0, it is necessary to complete all operations for closing the month and check the correctness of the sequence of documents. All expenses are included in this report after they are paid.

The D&R accounting book is generated automatically and quarterly. To do this, click on the “Generate” button.

The book of income and expenses contains 4 sections:

- Section I. This section reflects all income and expenses for the reporting period quarterly, taking into account the chronological sequence.

- Section II. This section is filled out only if the simplified tax system is “Income minus expenses”. This contains all costs for fixed assets and intangible assets.

- Section III. This contains losses that reduce the tax base.

- Section IV. This section displays amounts that reduce tax, for example, insurance premiums for employees, etc.

If everything is configured correctly, then the KUDiR will be formed correctly.

Manual adjustment

If something is filled out incorrectly, the entries can be corrected manually. To do this, in the “Operations” menu, select “STS Income and Expense Book Entries.”

Create a new document. Three tabs will appear. The first tab corrects the entries in section I. The second and third tabs are in section II. Make the necessary entries in this document. After this, the KUDiR will be formed taking into account the new data.

Analysis of accounting status

This report can help you visually check whether the book of income and expenses is filled out correctly. To open it, select “Accounting analysis according to the simplified tax system” in the “Reports” menu.

We remind you that for the correct operation of your 1C systems, you need to update configurations after releases. You can always find out about the release of new updates and the validity period of your 1C:ITS from the First Bit specialists by phone or come to our office.

Tax accounting of software costs under the simplified tax system

In order to recognize exclusive rights to software as an intangible asset in tax accounting, the following conditions must be met (clause 4 of article 346.16, clause 1 of article 256 of the Tax Code of the Russian Federation):

- their cost must exceed 100,000 rubles,

- useful life - more than 12 months,

- the property is depreciated and used for its own needs.

Expenses for this asset are written off quarterly in equal amounts during the tax period (year) after payment and acceptance of the software for accounting.

An asset acquired with periodic payment delineation during the term of the agreement cannot be classified as an intangible asset (clause 8, clause 2, article 256 of the Tax Code of the Russian Federation). The costs for such software are written off upon each subsequent payment.

If a non-exclusive right to use the software has been acquired, then in tax accounting the expenses are written off immediately after payment and acceptance of the asset for accounting as part of the RBP.

"1C Accounting" for simplification

This accounting program is a real salvation for taxpayers, because simplified legal entities are required to maintain both accounting and tax records. Since most taxpayers under the simplified tax system are representatives of small businesses, the extra costs of maintaining a staff of accountants can be prohibitive.

For information on existing legislative concessions for small businesses, see the material “The Ministry of Finance spoke about concessions in accounting for small businesses .

First you need to decide which version of the program to use. For simplifiers, it would be more advisable to use the basic version, because it costs less, and the available settings are more than enough to organize accounting and tax accounting.

Despite the apparent simplicity of accounting using the simplified taxation system, taxpayers face a number of difficulties. The cash method of accounting for expenses is especially difficult to use for those simplifiers who have chosen “income minus expenses” as the object of taxation.

“Accounting for expenses under the simplified tax system with the object “income minus expenses”” will help you understand .

The best option for simplified taxation systems is the special package “1C: Simplified” of the 1C: Accounting program, version 8 (revision 3.0). Also, in the new section “Tax accounting under the simplified tax system”, consulting articles are regularly added to help the accountant when working with the program.

Examples of software accounting (STS)

Example 1

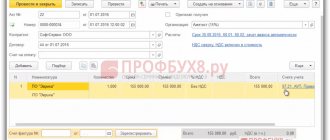

In April 2021, the enterprise acquired the exclusive right to software worth 150,000 rubles, paying in full and installing the software in April. The asset is recognized in the structure of intangible assets, the useful life is set at 3 years (36 months). In accounting, software costs will be written off by depreciation over 3 years. Postings:

| Operations | D/t | K/t | Sum |

| Purchasing software | 08 | 60 | 150 000 |

| Payment | 60 | 51 | 150 000 |

| Putting software into operation as intangible assets | 04 | 08 | 150 000 |

| From May 2021 to April 2021, depreciation is calculated monthly (150,000/36) | 20 | 05 | 4166,67 |

In tax accounting, the accountant will write off the costs of purchasing an asset before the end of the tax year, distributing the costs quarterly - in the 2nd, 3rd and 4th quarters, 50,000 rubles each. (150000/3), and reflecting them in KUDiR.