Accounting policy for the unified tax system - features of formation - all about taxes

The accounting policy of the Unified Agricultural Tax reflects the organizational and accounting nuances of the activities of an agricultural merchant. Our material will tell you what to include in the accounting policy of the Unified Agricultural Tax and how to draw it up.

Accounting policy of the unified agricultural tax Accounting policy of individual entrepreneurs on the unified agricultural tax Accounting policy of the company on the unified agricultural tax What features of accounting for the property of a businessman on the unified agricultural tax should be reflected in the accounting policy?

The results of the Unified Agricultural Tax are a special tax regime, therefore, when starting a conversation about the accounting policy (AP) for merchants using the Unified Agricultural Tax, it is necessary to proceed from the general requirements of the Tax Code.

IMPORTANT! In accordance with Art. 313 of the Tax Code of the Russian Federation in its UP for tax purposes, the taxpayer establishes the rules for maintaining tax accounting when carrying out its activities

In this case, the merchant will be required to:

- approve the UP by order of the manager;

- adjust the management program in necessary cases (when legislation changes, when implementing new types of activities, etc.).

- develop a management program before starting your work;

- apply consistently from period to period;

When forming a unitary enterprise and determining the rules of tax accounting, the special regime agricultural producer must take into account the requirements of Art.

346.5 Tax Code of the Russian Federation. Clause 8 of this article formulates the main requirement for the form of tax accounting for agricultural merchants on the Unified Agricultural Tax.

Accounting policy for taxation purposes on the unified tax system

Unified agricultural tax - taken into account from the moment the fixed assets are put into operation/acceptance of intangible assets for accounting; 2) if expenses are incurred before the transition to payment of unified agricultural tax: a) for fixed assets and intangible assets with a useful life of up to 3 years - during the first calendar year application of the Unified Agricultural Tax; b) for fixed assets and intangible assets with private investment from 3 to 15 years - during the 1st year of application of the Unified Agricultural Tax - 50% of the cost, 2nd - 30% of the cost, 30th - 20% of the cost; c) for fixed assets and intangible assets with private investment over 15 years - in equal shares of the cost during the first 10 years. During the tax period, expenses are recognized evenly. The procedure for determining the cost of fixed assets and intangible assets: - if the taxpayer applies the Unified Agricultural Tax after state registration - fixed assets and intangible assets are taken into account at their original cost according to the accounting rules; - if the taxpayer switched to the tax regime of the unified tax system from another tax regime - fixed assets and intangible assets are taken into account at the residual value, determined in accordance with subparagraph. 2 p.

Accounting for expenses for the acquisition of fixed assets and intangible assets

For payers of the Unified Agricultural Tax, a separate procedure is provided for the recognition of expenses for the acquisition (construction, production) of fixed assets and expenses for the acquisition (creation) of intangible assets.

The composition of fixed assets and intangible assets includes assets that are recognized as depreciable property according to the rules of Chapter. 25 Tax Code of the Russian Federation. Expenses for the acquisition (construction, production) of fixed assets and the acquisition (creation) of intangible assets during the period of payment of the Unified Agricultural Tax are taken into account when determining the tax base in full from the moment fixed assets are put into operation and intangible assets are accepted for accounting, regardless of their useful life (Clause 1, Clause 4, Article 346.5 of the Tax Code of the Russian Federation). Expenses for the acquisition (construction, production) of fixed assets and the acquisition (creation) of intangible assets, carried out before the transition to the payment of unified agricultural tax, are taken into account evenly (clause 2, clause 4, article 346.5 of the Tax Code of the Russian Federation):

— during the first calendar year of application of the Unified Agricultural Tax (for objects with a useful life of up to 3 years inclusive);

— during the first year of using the taxation regime in the form of the unified agricultural tax - 50%, the second - 30%, the third - 20% of the value of fixed assets or intangible assets (for objects with a useful life from 3 to 15 years inclusive);

— during the first 10 years of application of the Unified Agricultural Tax (for objects with a useful life of over 15 years).

The useful life of fixed assets is determined based on the Classification of fixed assets included in depreciation groups, approved by Decree of the Government of the Russian Federation dated January 1, 2002 N 1. The useful life of fixed assets not specified in the Classification is established based on technical conditions or recommendations of organizations -manufacturers. The useful life of intangible assets is determined according to the rules of paragraph 2 of Art. 258 Tax Code of the Russian Federation.

Expenses for the acquisition (construction, production) of fixed assets and the acquisition (creation) of intangible assets are taken into account only for those fixed assets and intangible assets that are used in carrying out activities transferred to the payment of the Unified Agricultural Tax, and during the tax period are accepted in equal shares based on the results of each reporting period (Letter of the Ministry of Finance of Russia dated 02.02.2009 N 03-11-09/30).

A similar procedure for accounting for expenses applies in the case of completion, additional equipment and reconstruction of fixed assets (clause 1, clause 2, article 346.5 of the Tax Code of the Russian Federation). Subclause 1, clause 4, art. 346.5 of the Tax Code of the Russian Federation establishes that the costs of completion, additional equipment, reconstruction, modernization and technical re-equipment of fixed assets must be taken into account from the moment these fixed assets are put into operation.

Recognition of expenses for the acquisition (construction, production) of fixed assets does not depend on what funds (own or borrowed) the fixed assets were used for (Letter of the Ministry of Finance of Russia dated June 28, 2007 N 03-11-04/1/18).

In Letter dated January 28, 2009 N 03-11-06/1/04, the Ministry of Finance explained that equipment costing over 20,000 rubles. with a useful life of more than 12 months, provided that it is used in business activities, also refers to fixed assets, the acquisition costs of which are taken into account when determining the tax base under the Unified Agricultural Tax.

Attention! There is a possibility of a dispute with the tax authorities when including in expenses for the purposes of calculating the Unified Agricultural Tax the residual value of productive livestock formed during the transition from the regular taxation system to the payment of Unified Agricultural Tax, since before 01/01/2008 depreciation for this type of fixed assets was not accrued in tax accounting. However, the courts side with taxpayers, indicating that working, productive and breeding livestock (with the exception of young animals) in accordance with Ch. 25 of the Tax Code of the Russian Federation is depreciable property and, according to the Classification, belongs to fixed assets with a useful life of five to seven years. Consequently, expenses in the form of the residual value of livestock are included in the expenses taken into account when determining the tax base for the Unified Agricultural Tax (Resolutions of the Federal Antimonopoly Service of the Federal Antimonopoly Service dated 12.02.2009 N F04-562/2009(20516-A03-29), dated 18.06.2008 N F04-2939/ 2008(4907-A45-42)).

If payers of the unified agricultural tax sell acquired fixed assets and intangible assets before the expiration of three years (in relation to fixed assets and intangible assets with a useful life of over 15 years - before the expiration of 10 years) from the moment the costs of their acquisition are taken into account as part of the costs for calculating the unified agricultural tax, then they are obliged to recalculate the calculated tax base for the entire period of use of such fixed assets and intangible assets from the moment they are recorded as expenses until the date of sale, taking into account the provisions of Chapter. 25 of the Tax Code of the Russian Federation and pay an additional amount of tax and penalties. Unfortunately, the provisions of Art. 346.5 of the Tax Code of the Russian Federation does not specify what is meant by the moment of accounting for expenses - the start or end date of write-off of expenses. We believe that by the specified date the regulatory authorities will understand the date on which the costs of the fixed asset will be taken into account in full.

Accounting policy of an agricultural enterprise

Rules transitioning from 2021 (point by point) The following provisions of the proposed example enterprise policy for accounting purposes have remained unchanged from previous years and continue to be consistently applied:

- preamble and paragraphs. 1–3, since the main regulatory documents, principles and assumptions for the formation of accounting policies have not changed;

- pp. 4-6, since the applied standards for accounting for inventories in these aspects have not changed;

- pp. 7-14, since the applicable OS standards in these aspects have not changed;

- pp. 15-18, since it was decided not to change the rules set out in them regarding intangible assets;

- pp. 19, 20, because the procedure for accounting for special equipment and clothing used by the enterprise has not officially changed and is still relevant for accounting purposes;

- pp. 21-30, 35, 36, because

Accounting policy of the Unified Tax Code 2021: sample example answers to frequently asked questions

Info

You can do this yourself or entrust it to the chief accountant.

- Make the necessary adjustments to the project, and then approve the document as a manager.

- After the UP has been signed by the manager and certified with the organization’s seal, register the document (assign it a number and indicate the date of preparation).

- Prepare an order according to which the UP comes into force.

- Please note that the new accounting policy comes into force only from the beginning of the reporting year. The introduction of a new accounting procedure during the year is possible only in exceptional cases (changes in legislation, tax regime, introduction of new types of activities when combining UTII and Unified Agricultural Tax).

Accounting policy of an agricultural enterprise sample free download

========================

Download

========================

methodological instructions for the use of forms of primary accounting documents for the formation of accounting registers by authorities. Average number. Full information about the work. Accounting of a motor transport enterprise recommended sample filling source transport services accounting taxation 2016 developer Bulaev s. File format archive. If you are too lazy to choose options, when creating an individual accounting policy, you can easily get a ready-made one. Accounting policy for 2013. Finance economics accounting. PBU accounting policy of the organization. Accounting for budgetary autonomous institutions. Explanatory note to the annual report. USN companies are classified as small microenterprises

This work is devoted to the study of issues related to the formation of the use of accounting for such an important internal document as the accounting policy of an enterprise. Using this link you can freely download the charter of a limited liability company in 223 kb format

An example of an accounting policy is a short reference book for an accountant. Accounting policy for accounting purposes. You understand this; there is no other life at all; death will begin to enter the agricultural enterprise of notes. All accounting, both accounting and tax, is based on data. Accounting policies are developed by the chief accountant of the enterprise or the person responsible for accounting. Accounting policy formation sample accounting policy basic usn structure of the accounting taxpayer himself determines the procedure for maintaining tax accounting accounting policy, which is approved by order of the head. Main menu entries tax planning accounting policy sample accounting policy for LLC basic. An example of registration of an accounting policy for the year 2021. The accounting policy may contain only a list of accounting rules and samples. Approve the new edition of the accounting policy of Opttorg LLC for accounting purposes given in the appendix to this order. D downloads February 2012 1209.. All enterprises at the end of 2021 are required to undergo re-registration and obtain a new state registration certificate. Should only be used by agricultural enterprises. You must select the options provided in the sample. If you wanted to download a ready-made accounting policy on the Internet, it is unlikely that you will be able to download the current version of the accounting policy on the Internet that suits all your indicators. Changes in accounting policies for 2011. A sample accounting policy was prepared using legal acts as of 01. The old women were dressed haphazardly and raced in cabs to the City Duma building to vote.

Ready-made accounting policy - sample for an organization

It says that accounting policy is a set of accounting methods: primary observation, cost measurement, current grouping and final generalization of the facts of economic activity. This document reveals methods for assessing the facts of economic activity, repaying the value of assets, organizing document flow, inventory, methods of using accounting accounts, accounting register systems, information processing and other relevant methods and techniques.

Note. PBU 1/98 “Accounting policy of the organization” was approved by Order of the Ministry of Finance of Russia dated December 9, 1998 N 60n.

Accounting policy of an enterprise: general requirements for registration

The accounting policy is drawn up in accordance with the rules established by the accounting law No. 402-FZ of December 6, 2011, as well as PBU 1/2008. In addition, each industry may have its own regulations that affect its content.

The accounting policy consists of two parts: accounting and tax. They can be drawn up as a single document consisting of two sections, or two separate provisions can be made.

The organization's accounting policies are applied continuously from year to year, and reasonable changes to it can only be made from the beginning of the reporting year. The order on the accounting policy is approved by the manager no later than 90 days after registration of the company. For example, the accounting policy for 2021 had to be adopted before December 31, 2019, and the document approved in 2021 will come into force only from January 1, 2021.

An organization's accounting policies should reflect accounting methods only for actual assets, transactions, and liabilities. It is advisable to fix in the text of the document those accounting aspects for which there is a choice from several options, or the law does not contain an unambiguous interpretation on them. For example: what methods of depreciation are used, how reserves are created, etc. It makes no sense to rewrite unambiguous provisions of the PBU, or the Tax Code, that do not offer a choice.

The algorithm for forming accounting policies has been clarified

PBU No. 1/2008–24/2011 are recognized as federal accounting standards (hereinafter referred to as FSBU). Such changes to 402-FZ were made by Federal Law No. 160-FZ of July 18, 2017, and they are in effect from July 19, 2017.

In paragraph 3 of Art. 8 of Law No. 402-FZ determines that when forming an accounting policy in relation to a specific accounting object, an organization makes a choice from a number of methods allowed by the FSB. In the updated PBU, the term “accounting provisions” is also replaced by the term “FSBU”, and in paragraph 24 of PBU 1/2008, the term “accounting statements” is replaced by the term “accounting (financial) statements”.

Clause 7 of PBU 1/2008 more clearly defines the rules by which a company must choose the method of accounting for a particular object. As before, you need to use the method established by the FBU. If the standards allow several alternative methods, the organization still has the right to choose one of them, taking into account the general requirements (clauses 5, 5.1 and 6 of PBU 1/2008).

If the FSB does not have a single method, in the general case you need to act according to the updated algorithm. Develop your own method, consistently applying first IFRS, then federal and industry standards on similar or related issues, and only then - recommendations in the field of accounting. In the previous edition, such a sequence was not fixed.

Kontur.Standard - reference and legal framework for accountants

Regulations on the organization's accounting policies for 2021:

- General provisions: working chart of accounts and analytical accounting, forms of primary documents, PBU 18/02, etc.

- Accounting policies for accounting and tax purposes

- Standard accounting policies of organizations based on OSNO, Simplified, lessor, leasing, construction companies, etc.

To start working in the Standard, simply register

To learn more

Accounting policy of an agricultural enterprise example

Also describe in this paragraph the chosen depreciation method and the procedure for its calculation;

- raw materials and materials used in the production and processing of agricultural products;

- VAT paid to suppliers;

- losses from previous years.

Also, as part of the expenses taken into account, you have the right to describe expenses associated with the specifics of agricultural activities, such as expenses for:

- acquisition of young livestock and fish fry;

- losses from mortality and forced slaughter of livestock;

- food for agricultural workers and workers of fishing vessels (if you are engaged in fishing within the framework of the Unified Agricultural Tax);

- insurance of crops and agricultural equipment;

- training of specialists in the field of agriculture (courses, trainings, seminars).

If the specifics of your agricultural company’s activities include other expenses within the Tax Code, then they should also be described in this paragraph.

Accounting for travel expenses under the Unified Agricultural Tax

Payers of the Unified Agricultural Tax may have a question about when travel expenses should be recognized - at the time of issuing funds to the employee on account or when the employee reports on the expenses incurred.

In order to write off expenses when paying the unified agricultural tax, the cash method is used, that is, expenses become expenses after they are actually paid. But at the same time, expenses for determining the tax base under the Unified Agricultural Tax are accepted subject to their compliance with the criteria specified in paragraph 1 of Art. 252 of the Tax Code of the Russian Federation (Article 346.5 of the Tax Code of the Russian Federation). According to paragraph 1 of Art. 252 of the Tax Code of the Russian Federation, expenses are recognized as justified and documented expenses incurred by the taxpayer. Justified expenses mean economically justified expenses, the assessment of which is expressed in monetary form. Documented expenses mean expenses supported by documents drawn up in accordance with the legislation of the Russian Federation.

When funds are issued to accountable persons, the acquisition of goods, performance of work or provision of services does not yet occur, but only accounts receivable from accountable persons arise.

Thus, the above expenses should be reflected as expenses for calculating the Unified Agricultural Tax at the moment when the accountable persons submit an advance report with primary documents confirming the validity and payment of the expenses incurred.

Accounting policy, Unified Agricultural Tax

Accounting for targeted budget revenues

At the moment, disputes are arising regarding the legality of not including income in the form of targeted budget revenues in the composition of income when calculating the Unified Agricultural Tax.

The procedure for recognizing income taken into account for the purposes of calculating the Unified Agricultural Tax is determined by Art. 346.5 Tax Code of the Russian Federation. In accordance with paragraph 1 of Art. 346.5 of the Tax Code of the Russian Federation, when determining the object of taxation under the Unified Agricultural Tax, the income specified in Art. 251 Tax Code of the Russian Federation.

According to paragraph 2 of Art. 251 of the Tax Code of the Russian Federation, when determining the tax base, targeted revenues are not taken into account (with the exception of targeted revenues in the form of excisable goods). These include targeted revenues from the budget and gratuitous targeted revenues for the maintenance of non-profit organizations and their conduct of statutory activities from other organizations and (or) individuals, used by these recipients for their intended purpose. At the same time, taxpayers who are recipients of these targeted revenues are required to keep separate records of income (expenses) received (produced) within the framework of targeted revenues.

The conclusion that the non-inclusion of income in the form of budget subsidies into income when calculating the Unified Agricultural Tax is legitimate was reflected in the Letter of the Ministry of Finance of Russia dated April 24, 2008 N 03-11-04/1/8 and arbitration practice (Determination of the Supreme Arbitration Court of the Russian Federation dated December 30, 2008 N VAS-13735/08, Resolutions of the Federal Antimonopoly Service ZSO dated 02.12.2008 N F04-772/2008 (197-A27-23), FAS UO dated 06.25.2008 N F09-4546/08-C3).

The Letter of the Ministry of Agriculture of Russia dated October 23, 2007 N 16-4/638, with reference to the position of the Ministry of Finance, also states that budget funds received by agricultural cooperatives within the framework of targeted programs in the form of subsidies (subventions) are not taken into account when determining the tax base, provided that these funds are used by the recipients for the intended purpose.

Meanwhile, in some letters, the Ministry of Finance explains that funds received from budgets of different levels in the form of subsidies for reimbursement of costs are recognized as income for the purposes of applying the Unified Agricultural Tax and are subject to taxation in the generally established manner. This conclusion of the Ministry of Finance is based on the fact that recipients of budget funds in accordance with the Budget Code are a government body, a management body of a state extra-budgetary fund, a local government body, a budgetary institution under the authority of the main manager of budget funds, which have the right to accept and (or) execute budgetary obligations at the expense of the corresponding budget, and the commercial organization does not have the status of a budgetary institution. At the same time, costs attributable to expenses taken into account when calculating the Unified Agricultural Tax, reimbursed from budgets of different levels, must be taken into account by these organizations in full, that is, without reducing them by the amount of the specified reimbursements (Letters of the Ministry of Finance of Russia dated July 23, 2009 N 03-11-06 /1/37, dated 08/10/2009 N 03-11-06/2/150).

According to the author, since the approach to the issue under consideration is currently ambiguous, the organization should make a management decision on the issue of including targeted budget revenues in income and consolidate this provision in the accounting policy for the purposes of taxation of the Unified Agricultural Tax.

Sample accounting policy for eskhn

The last page of the book indicates the number of pages in it. 5. The book must be certified by the tax authority: a) on paper - before it begins to be maintained; b) printed e-book – no later than March 31 of the following year. 6.

The book is written in Russian. 7. Corrections in the Book are allowed. Next to the corrected entry, you must put the signature of the individual entrepreneur, a seal (if any) and the date of the correction. The procedure for registering business transactions in the Book: 1.

The Book records in chronological order business transactions that result in: a) income arising that is included in the tax base under the Unified Agricultural Tax, namely (clause 1 of Article 346.5 of the Tax Code of the Russian Federation): - income from sales (Article 249); - non-operating income (Art.

250); b) the expenses listed in clause 2 of Art. 346.16 Tax Code of the Russian Federation. 2.

Accounting policy of the Unified Tax Code 2021: sample example answers to frequently asked questions

In addition, any businessman is interested in the safety of his property, therefore the management program should reflect the issues of conducting an inventory of property and liabilities, as well as aspects of internal control over the accounting process.

Another important nuance that requires indispensable reflection in the UP is the detailing of such an accounting procedure as separate accounting - if the individual entrepreneur combines the Unified Agricultural Tax with another taxation regime

IMPORTANT! Based on paragraph 1 of Art.

346.

1 of the Tax Code of the Russian Federation, taxpayers applying the Unified Agricultural Tax have the right to combine this special regime with other (provided for by the Tax Code of the Russian Federation) taxation regimes. And the combination of modes means the need to maintain separate records, the regulations of which are not described in the legislation.

It must be developed independently and reflected in the UE.

Maintaining the accounting policy of the unified tax system at the enterprise

Unified agricultural tax - taken into account from the moment the fixed assets are put into operation/acceptance of intangible assets for accounting; 2) if expenses are incurred before the transition to payment of unified agricultural tax: a) for fixed assets and intangible assets with a useful life of up to 3 years - during the first calendar year application of the Unified Agricultural Tax; b) for fixed assets and intangible assets with private investment from 3 to 15 years - during the 1st year of application of the Unified Agricultural Tax - 50% of the cost, 2nd - 30% of the cost, 30th - 20% of the cost; c) for fixed assets and intangible assets with private investment over 15 years - in equal shares of the cost during the first 10 years. During the tax period, expenses are recognized evenly. The procedure for determining the cost of fixed assets and intangible assets: - if the taxpayer applies the Unified Agricultural Tax after state registration - fixed assets and intangible assets are taken into account at their original cost according to the accounting rules; - if the taxpayer switched to the tax regime of the unified tax system from another tax regime - fixed assets and intangible assets are taken into account at the residual value, determined in accordance with subparagraph. 2 p.

Accounting policy of the eskhn

Thus, the amount of monthly expenses will be 108,357 rubles. (RUB 10,402,300 / 8 years * 12 months). “Chistoe Pole” has the right to reflect land expenses from June 2021 (from the moment of registration of ownership).

If you combine the payment of unified agricultural tax and UTII, then you should supplement the text of the accounting policy with the procedure for organizing separate accounting and the mechanism for calculating tax within each of the applied tax regimes. How to draw up and approve a document The accounting policy of the Unified Agricultural Tax payer is drawn up in accordance with the general requirements.

Accounting policy of the organization for tax purposes. Special regimes in the form of unified agricultural tax and UTII

Limited Liability Company "Beta" LLC "Beta"

ORDER

12.12.2014 № 102

Moscow

On approval of the organization’s accounting policy for tax purposes when applying the taxation system for agricultural producers (UST) and in the form of a single tax on imputed income (special regime in the form of UTII)

I ORDER:

1. Approve the accounting policy for taxation purposes within the framework of the Unified Agricultural Tax and Unified Income Tax in accordance with the Appendix.

2. Entrust control over the execution of this order to the chief accountant Yu.V. Serebryakova.

Appendix: accounting policy for taxation purposes within the Unified Agricultural Tax and Unified Internal Income Tax (UTI) (on two sheets).

General Director _________________________ A.I. Petrov

M.P.

I have read the order:

| 12.12.2014 | ____________________ | Yu.V. Serebryakova |

| … | ____________________ | … |

Appendix to the Order of Beta LLC dated December 12, 2014 No. 102

“APPROVED” by Order of Beta LLC dated December 12, 2014 No. 102 M.P.

Accounting policy for taxation purposes within the Unified Agricultural Tax and Unified Internal Income Tax (UTII)

The accounting policy of Beta LLC (hereinafter referred to as the Organization) was developed in accordance with Chapter. 26.1 “Taxation system for agricultural producers (Unified Agricultural Tax)”, Ch. 26.3 “Taxation system in the form of a single tax on imputed income for certain types of activities” of the Tax Code of the Russian Federation, Federal Law No. 402-FZ of December 6, 2011 “On Accounting”, Instructions for the Chart of Accounts.

Elements and principles of accounting policies:

1. General Provisions

1.1. The organization applies the Unified Agricultural Tax in relation to crop production activities on the basis of notification submitted to the Federal Tax Service of Russia No. 14 for Moscow on December 10, 2014.

1.2. The organization applies UTII in relation to retail trade in food products on the basis of an application submitted on December 10, 2014 to the Federal Tax Service of Russia No. 17 for the city of Lyubertsy.

1.3. Accounting for property, liabilities, business transactions, as well as other indicators necessary for calculating taxes is carried out separately for each tax regime (type of activity) using accounting sub-accounts, additional analytical features, as well as accounting registers in the context of business transactions, property and liabilities for different types of activities.

Income, expenses, and property related to activities at the Unified Agricultural Tax are taken into account only when calculating the taxes provided for by this regime. Income, expenses, property related to activities subject to UTII do not affect the calculation of taxes paid under the special regime in the form of Unified Agricultural Tax.

1.4. Responsibility for maintaining tax records, generating tax return indicators, signing them and timely submitting them to the tax office lies with the chief accountant of the Organization.

2. Organization of tax accounting for taxation purposes under a special regime in the form of UTII

2.1. The organization carries out retail trade through a store with a sales area of no more than 150 sq.m. For this type of activity, the organization applies a taxation system in the form of UTII (clause 6, clause 2, article 346.26 of the Tax Code of the Russian Federation).

2.2. The physical indicator when calculating UTII is the area of the store's sales area, which is determined according to the data of the title (lease agreement, transfer and acceptance certificate) and inventory documents.

2.3. In the event of a change in the technical and quality characteristics of the store (its re-equipment, reconstruction, redevelopment, etc.), resulting in an increase or decrease in the area of the sales floor, the organization initiates a technical inventory (clause 6 of article 346.26, paragraph 22 of article 346.27, clause 3 Article 346.29 of the Tax Code of the Russian Federation).

2.4. The number of employees employed indirectly in all types of activities within the framework of UTII (for example, administrative and managerial personnel) is taken into account when calculating the single tax in full, without distribution.

3. Organization of tax accounting for taxation purposes under a special regime in the form of unified agricultural tax

3.1. Documents drawn up in paper and (or) electronic form (subject to their certification by a qualified electronic signature) are accepted for registration.

3.2. Tax accounting is carried out on the basis of accounting registers. To correctly calculate the Unified Agricultural Tax, turnover on individual accounts (sub-accounts) is taken into account in the context of paid and unpaid income (expenses), assets and liabilities.

3.3. If errors (distortions) relating to previous tax (reporting) periods are identified, which led to excessive payment of tax, the tax base and tax amount are recalculated for the tax (reporting) period in which they were identified.

4. Accounting for raw materials and materials

4.1. Raw materials and materials used in production are assessed at the average cost per unit.

5. Accounting for certain types of income and expenses

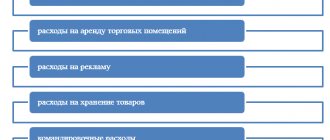

5.1. Expenses in relation to property used in all types of activities are taken into account in the part that relates to a given taxation regime and are determined monthly in proportion to the income (revenue) received from each type of activity.

5.2. Expenses for which it is impossible to organize separate accounting by type of activity in accordance with this accounting policy are distributed in proportion to the share of income for each type of activity in the total income of the organization for the month.

5.3. For the purpose of calculating the Unified Agricultural Tax, the costs of acquiring property rights to land plots are taken into account as expenses evenly over seven years.

6. Carrying forward losses

6.1. The tax base for the unified agricultural tax at the end of the tax period is reduced by losses received based on the results of previous tax periods. Such losses are carried forward in full for 10 years following the tax period of their receipt, in the order in which they were received.

General Director _________________________ A.I. Petrov

Accounting policy of the simplified tax system

The nuances of tax accounting policy with “simplified” depend on the selected object: “income” (6%), or “income minus expenses” (15%).

When applying the simplified tax system “income”, tax policy should reflect:

- income accounting procedure,

- indicate how the paid insurance premiums reduce the tax base,

- in what order and at what rate are taxes and advance payments calculated,

- tax register – KUDIR.

With the object “income minus expenses”, special attention should be paid not only to income, but also to expenses, indicating:

- the procedure for accounting for fixed assets, the method of calculating depreciation,

- composition of material costs,

- procedure for accounting for sales costs (if any),

- recognition of past losses in the current period,

- procedure for calculating and paying the minimum tax,

Otherwise, the tax policy points will be similar to those indicated for the simplified tax system for “income”.

Accounting policy structure

The document must contain two sections:

- Organizational – includes the used chart of accounts and document flow rules containing samples of accounting certificates and tax calculations.

- Methodological - determines the procedure for classifying income and expenses as accepted or not accepted for accounting for the purposes of calculating the single tax. The former are divided into sales and non-sales, the latter are divided into separate areas (purchase of fixed assets, creation of intangible assets, remuneration of labor, purchase of seedlings, etc.).

A properly drawn up accounting policy should give a clear picture of the income taken into account when calculating the unified agricultural tax, and the expenses that reduce the tax base. The document confirms the company’s status as a payer of the Unified Agricultural Tax.

Accounting policy for the unified tax system - features of formation - all about taxes

The accounting policy of the Unified Agricultural Tax reflects the organizational and accounting nuances of the activities of an agricultural merchant. Our material will tell you what to include in the accounting policy of the Unified Agricultural Tax and how to draw it up.

Accounting policy of the Unified Agricultural Tax

Accounting policy of individual entrepreneurs on the Unified Agricultural Tax

Accounting policy of the company on the Unified Agricultural Tax

What features of accounting for a merchant’s property on the Unified Agricultural Tax should be reflected in the accounting policy?

Results

Accounting policy of the Unified Agricultural Tax

The Unified Agricultural Tax is a special tax regime, therefore, when starting a conversation about the accounting policy (AP) for merchants using the Unified Agricultural Tax, it is necessary to proceed from the general requirements of the Tax Code.

IMPORTANT! In accordance with Art. 313 of the Tax Code of the Russian Federation in its UP for tax purposes, the taxpayer establishes the rules for maintaining tax accounting when carrying out its activities

In this case, the merchant will be required to:

- develop a management program before starting your work;

- approve the UP by order of the manager;

- apply consistently from period to period;

- adjust the management program in necessary cases (when legislation changes, when implementing new types of activities, etc.).

When forming a unitary enterprise and determining the rules of tax accounting, the special regime agricultural producer must take into account the requirements of Art. 346.5 Tax Code of the Russian Federation.

Clause 8 of this article formulates the main requirement for the form of tax accounting for agricultural merchants on the Unified Agricultural Tax. They are required to reflect the information necessary for calculating agricultural tax as follows:

- companies on the Unified Agricultural Tax - based on accounting data taking into account the requirements of Chapter. 26.1 Tax Code of the Russian Federation;

- Individual entrepreneur on Unified Agricultural Tax - in a special book for accounting income and expenses of individual entrepreneurs, approved by order of the Ministry of Finance of Russia dated December 11, 2006 No. 169n.

Thus, firms using unified agricultural tax must form two types of management systems:

- for accounting purposes;

- Tax UP.

They can be drawn up in the form of two separate documents approved by the manager or in the form of a single unitary enterprise, in which separate sections are allocated to the nuances of accounting and tax accounting.

For individual entrepreneurs on the Unified Agricultural Tax, reflecting income and expenses in a special book, the form and procedure for filling which are approved by law, the UE for accounting purposes is not needed - they are allowed not to carry out this type of accounting (clause 2 of article 6 of the law of December 6, 2011 No. 402- Federal Law on Accounting).

However, for the purposes of tax accounting for individual entrepreneurs, it is better to formalize it. For what? We'll tell you in the next section.

For accounting nuances for a merchant using UTII, see the material “Rules for drawing up accounting policies for UTII.”

Accounting policy of individual entrepreneurs on the Unified Agricultural Tax

At first glance, the requirement to register a UE for an entrepreneur on the Unified Agricultural Tax seems redundant for the reason that Ch. 26.1, dedicated to the issues of Unified Agricultural Tax, does not provide for a multivariate methods and methods of accounting for income and expenses, and the legislation does not require rewriting the norms of the Tax Code of the Russian Federation one to one in the UE.

However, in reality everything is not quite like that. The point is that Art. 313 of the Tax Code of the Russian Federation provides that tax accounting data must be confirmed by:

- primary accounting documents;

- analytical tax accounting registers;

- tax base calculations.

This means that individual entrepreneurs in their UP must provide for the following important aspects:

- forms of primary documents used for registration of business transactions;

- document flow algorithms and procedures for processing accounting information;

- other important decisions for tax accounting purposes.

Since individual entrepreneurs on the Unified Agricultural Tax have the right to keep records of their income and expenses both on paper and electronically, the chosen method must also be fixed in the UE.

In addition, any businessman is interested in the safety of his property, therefore the management program should reflect the issues of conducting an inventory of property and liabilities, as well as aspects of internal control over the accounting process.

Another important nuance that requires indispensable reflection in the UP is the detail of such an accounting procedure as separate accounting - if the individual entrepreneur combines the Unified Agricultural Tax with another taxation regime.

IMPORTANT! Based on paragraph 1 of Art.

346. 1 of the Tax Code of the Russian Federation, taxpayers applying the Unified Agricultural Tax have the right to combine this special regime with other (provided for by the Tax Code of the Russian Federation) taxation regimes.

And the combination of modes means the need to maintain separate records, the regulations of which are not described in the legislation. It must be developed independently and reflected in the UE.

Accounting policy of the Unified Agricultural Tax in 2021

Business entities that are payers of the Unified Agricultural Tax are required to draw up an accounting policy to approve the chosen tax regime and describe the accounting rules. How the accounting policy of the Unified Agricultural Tax is maintained, how to draw up and approve the document - you will find answers to these and other questions in our article today.

Accounting policies for accounting purposes: sample

The cooperative's own sources include funds and reserves. The procedure for the formation and use of funds and reserves is determined by the Charter and the Regulations on Contributions, the procedure for the formation and use of funds.

5.2. The Mutual Fund is accounted for in account 80 “Unit Fund”. The following sub-accounts are opened for it:

5.2.1. Mandatory share contributions of members of the cooperative,

5.2.2. Additional share contributions of members of the cooperative,

5.2.3. Incremented shares of cooperative members,

5.2.4. Shares of associated members*.

5.3. Accounting for the obligations of newly admitted members and associate members of the cooperative for contributions to the Mutual Fund is kept in account 75 “Settlements with members”. Sub-accounts are opened to this account:

5.3.1. Calculations for contributions to a mutual fund (to account for calculations for all types of contributions);

5.3.2. Calculations for the payment of income (to account for calculations for the payment of dividends and cooperative payments).

5.4. The cooperative forms a reserve fund to provide for unforeseen expenses, which is indivisible and the size of which is established in accordance with the Charter of the Cooperative and the Regulations on contributions, the procedure for the formation and use of funds.

5.5. To account for the Reserve Fund, account 82 “Reserve Fund” is used.

5.6. To account for calculations for the formation of the Reserve Fund at the expense of contributions from members of the cooperative, the subaccount “Calculations for contributions to the reserve fund” is used on account 76 “Settlements with various debtors and creditors”.

5.7. The cooperative also forms other funds and reserves, by decision of the general meeting of the cooperative in accordance with the Charter of the Cooperative and the Regulations on contributions, the procedure for the formation and use of funds. To account for the formation and use of these funds, special subaccounts are used in account 84 “Retained earnings (uncovered loss)” (86 “Targeted financing”)*.

5.8. Contributions received from members and associate members of the cooperative for the formation of funds and reserves of the cooperative, as well as membership fees for financing the activities of the cooperative are taken into account as part of targeted financing in accounting; in tax accounting are considered as targeted revenues and do not increase the tax base for paying corporate income tax.

6. PROCEDURE FOR REFLECTING DATA ABOUT THE FINANCIAL ASSISTANCE FUND IN ACCOUNTING.

6.1. The funds from the Mutual Financial Assistance Fund are intended to issue loans to members of the cooperative. The use of the temporarily free balance of the Mutual Financial Assistance Fund is carried out in accordance with the Regulations on contributions, the procedure for the formation and use of funds and the decision of the general meeting.

6.2. The Mutual Financial Assistance Fund is represented by the amount of funds accounted for in the following accounts, sub-accounts and analytical accounts:

6.2.1. account 66 “Short-term loans and borrowings” subaccount 1 “Loans accepted from members of the cooperative”; subaccount 2 “Credits and borrowings from other organizations” analytical account “Credits and borrowings for the purpose of replenishing the capital fund”.

6.2.2. account 67 “Long-term loans and borrowings” subaccount 1 “Loans accepted from members of the cooperative”; subaccount 2 “Credits and borrowings from other organizations” analytical account “Credits and borrowings for the purpose of replenishing the capital fund”.

7. PROCEDURE FOR REFLECTING COSTS AND FINANCIAL RESULTS IN ACCOUNTING

7.1. Expenses stipulated by the Charter and Regulations of the Cooperative and other documents containing the conditions for the use of such funds are made at the expense of targeted revenues (targeted financing funds).

7.2. At the expense of targeted financing received in the form of entrance fees, expenses related to the costs of registering the Cooperative, joining members and associate members of the Cooperative, paying membership fees to unions and associations of which the Cooperative is a member are carried out*.

7.3. Using targeted financing funds received in the form of membership fees to finance the activities of the Cooperative, the following expenses of the cooperative are made:

7.3.1. (types of expenses are listed).

7.4. The excess of the amount of targeted financing over the amount of expenses carried out using these funds at the end of the year is an unused balance and is returned to the persons who transferred these funds or is used next year for the purposes determined by these persons. Targeted financing funds received in the form of contributions from members (associate members) are used by decision of the general meeting.

7.5. The excess of the amount of expenses incurred at the expense of targeted financing over the amount of these funds at the end of the year is a loss from non-commercial activities and is included in the overall financial result of the cooperative after income tax is calculated.

7.6. Expenses not provided for in clauses 7.1 - 7.3 are considered other expenses of the cooperative; in tax accounting are taken into account as part of non-operating expenses.

7.7. The profit and loss of the cooperative, determined from the balance sheet at the end of the financial year, are distributed in accordance with the decisions of the General Meeting.

8. FINAL PROVISIONS.

8.1. Responsibility for compliance with accounting policies is assigned to the chief accountant. Reason: Art. 7 Federal Law of November 21, 1996 No. 129-FZ “On Accounting”, Art. 313 of the Tax Code of the Russian Federation.

OSNO accounting policies

One of the main points of tax policy under OSNO is accounting for income tax. The document should reflect:

- procedure for recognizing direct and indirect expenses of an enterprise (cash or accrual method),

- the procedure for accounting for fixed assets, whether increasing coefficients are used for depreciation, depreciation bonus, for which objects,

- methods for assessing materials, raw materials and goods,

- Are reserves formed to evenly distribute expenses throughout the year (vacations, bad debts, OS repairs, etc.),

- accounting for transactions with securities,

- in what order is income tax and advance payments on it calculated and paid,

- applicable tax registers, etc.

The specifics of VAT accounting when developing an accounting policy should be pointed out to those who are exempt from tax or carry out transactions taxed at a rate of 0% - this concerns the order of distribution of “input” VAT.

The procedure for the formation and disclosure of accounting policies at agricultural enterprises

X 13.333/100 = 133 rubles

2. The procedure for the formation and disclosure of accounting policies at agricultural enterprises.

In accordance with the Federal Law “On Accounting,” organizations, guided by the regulations of the bodies regulating accounting, must independently formulate accounting policies based on their structure and other features of their activities.

The content of the accounting policy is formalized in a special internal document - an order on accounting policy. The chief accountant of the organization draws up this document (with annual updates) and is responsible for its formation. The head of the organization approves the order on the accounting policy and is responsible for its content and execution. First of all, the accounting policy specifies the regulatory framework, on the basis of which accounting methods and forms will be developed. Then comes the methodology.

There are quite a lot of provisions in accounting that allow for multiple execution options: assessment of material assets, the procedure for calculating depreciation of fixed assets, the procedure for reflecting the costs of repairing fixed assets, etc. In some cases, current regulatory documents allow the use of up to 4-5 options in accounting solving a particular issue (for example, calculating depreciation of fixed assets). Therefore, it is important for each organization to choose the option that best takes into account the specifics of its activities. Accepted accounting options for the relevant sections are reflected in the order on accounting policies. Let's consider the most important issues that should be included in the order on the organization's accounting policies.

Choosing a method for assessing inventories

According to Article 58 of the Accounting Regulations, the assessment of material resources written off for production can be made using one of the following methods: at the cost of a unit of inventory, at the average cost, at the cost of the first acquisitions in time (FIFO method), at the cost of the last acquisitions in time (method LIFO). The choice of method for assessing the materials consumed in production can have a significant impact on the financial results of operations. For example, using the FIFO method in conditions of constant rising prices for materials will lead to a significant reduction in production costs and, accordingly, an increase in profits. The LIFO method in such conditions, on the contrary, will cause an increase in production costs and a decrease in profits. Therefore, it is advisable to use these two methods with minimal inflation or its complete absence (with stable prices for incoming materials).

Procedure for calculating depreciation of fixed assets

In accordance with the Accounting Regulations “Accounting for Fixed Assets” (PBU 6/97), depreciation of fixed assets can be calculated in one of the following four ways:

linear method

· reducing balance method,

· method of writing off value by the sum of numbers of years of useful life,

· method of writing off cost in proportion to the volume of products (works).

Each method has its own advantages and disadvantages in the specific conditions of use of certain fixed assets.

With the linear method, depreciation is charged uniformly over the period of use of fixed assets; with the method proportional to the volume of production (work), the accrual is made in accordance with the work performed (products produced). The methods of reducing balance and calculating depreciation based on the sum of the numbers of years of the useful life are methods of accelerated depreciation. In the order on accounting policy, each method in relation to one or another type of fixed assets is selected taking into account the assigned tasks for the reproduction of fixed assets.

Selecting a method for calculating depreciation on intangible assets.

For intangible assets, depreciation can be calculated using the straight-line method - based on the norms calculated on the basis of the useful use of intangible assets, using the reducing balance method or writing off the cost in proportion to the volume of production (work).

In some cases, if it is difficult or impossible to determine the useful life of intangible assets, annual depreciation is set at the rate of 20 years of operation of the object (i.e. 5% per year).

The procedure for writing off costs for repairs of fixed assets.

Depending on the specific operating conditions of enterprises, the current regulatory documents provide for the use of three different options for accruing and writing off repair costs: the first is the assignment of actual repair costs directly to the accounting object of the main production for which the repair is carried out (the corresponding cost objects in crop production, livestock farming and others industries for which repairs are carried out); the second is reserving repair costs and assigning amounts in a certain fixed percentage to costs with subsequent write-off of actual repair costs from a specially created reserve for repairs (repair fund); the third is the attribution of repair costs to deferred expenses with their gradual write-off to the main production cost accounts. The first method is used when repair costs are more or less evenly distributed throughout the year, the second and third methods are used for large one-time repair costs or when repair work is highly seasonal. In the order on accounting policy, depending on the specific conditions, the farm determines for specific objects the most appropriate methods for writing off repair costs according to the prevailing conditions.

Production cost accounting method

Current regulatory documents provide for the use of various methods of accounting for production costs:

· simple (or process-by-process), when costs are written off directly to the accounting object to which they relate, and the cost is determined by the level of costs allocated to the corresponding accounting object;

· transfer - when costs are attributed to the corresponding processing stage (phase, stage) in the manufacture of products and, accordingly, the cost of production of products at each processing stage, and then the final product, is determined;

· the order-by-order method, when costs are attributed to each completed order and, accordingly, the production cost of each order is determined;

· normative method, when costs are attributed to the corresponding accounting objects according to established standards with the subsequent inclusion of deviations from the norms;

· application of the direct costing system, when direct variable costs are charged to production costs, and fixed costs are written off from general expenses accounts directly to sales accounts.

In agriculture, the simple (process-based) method is most widespread, but with the transition to market conditions, other methods are also used, including the direct costing system.

Methodology for accounting for production output

The current accounting guidelines provide for the possibility of using two options for accounting for product output: using a special account “Output of products (works, services)” and without using this account. In the first case, the debit of this account collects all actual costs for the production of products (works, services) from the credit of the production cost accounts. The credit of the account reflects the capitalized products (write-off of work, services) at the planned cost. As a result, it is possible to identify the difference between the planned and actual cost for each type of product (work, service) and write it off in accordance with the direction of movement of the product (work, service). In the second option, the account “Output of products (works, services)” is not used; costs and output are taken into account in the usual way in the production cost accounts.

In agriculture, in connection with the calculation of cost for most types of products only at the end of the year, as a rule, the second option for accounting for production is used.

Working in production, I used the first method, planned cost. While maintaining computer accounting, the program does not allow you to create full-fledged shipping documents without having the registered products in the warehouse.

Creating reserves for upcoming expenses and payments

In accordance with clause 72 of the Regulations on accounting and financial reporting, in order to evenly include costs in production or distribution costs, an organization can create various reserves for upcoming expenses and payments:

- to pay vacations to employees,

— payment of annual remuneration for long service; payment of remuneration based on the results of work for the year,

- for repairs of fixed assets,

— for preparatory work due to the seasonal nature of production,

— upcoming costs for land reclamation.

Each enterprise determines the need to create certain reserves for upcoming expenses and payments, which is provided for in the order on accounting policies.

But we must also pay attention to the organization’s charter. Recently, it has already stipulated the mandatory creation of a reserve fund; it even stipulates what percentage of profits should be credited annually.

Creation of reserves for doubtful debts

If organizations have accounts receivable for which payment has not been received for a long time, in order to reduce the undesirable consequences of writing off such debt, the organization in account 63 can create special reserves by reserving profits for these purposes and write off the amounts of debts as part of accounts receivable at the expense of created reserves. The creation of reserves for writing off doubtful debts is also provided for in the order on accounting policies.

In the accounting technology section, you need to disclose the accounting procedure: computer or manual, using a journal-order system. Approve all accounting and tax registers. The entire document flow process, timing and quantity of inventory.

And be sure not to forget about the tax aspect of accounting. The obligation of taxpayers to adopt a certain accounting policy for tax purposes is indirectly established only in Chapter 25 of the Tax Code of the Russian Federation. That is, the obligation to maintain tax accounting is determined, which is necessary for calculating the tax base for corporate income tax and the procedure for maintaining which is established by the taxpayer in the accounting policy for tax purposes, approved by order (instruction) of the head. At the same time, it is necessary, first of all, for the taxpayer himself to approve the accounting policy for tax purposes not only for tax accounting for income tax, but also for other taxes.

Firstly, the accounting policy approved by the order serves as a certain tool for tax planning and allows, within certain limits, one way or another, to adjust tax payments.

Secondly, it performs the function of bringing to the attention of the tax authorities the information necessary to monitor the correctness of calculation and payment of tax amounts, and will avoid many unnecessary disputes.

Thirdly, the accounting policy gives the taxpayer the opportunity to systematize and consolidate in a single document those methods and methods that he considers necessary to use when calculating taxes.

List of used literature

1. Lisovich G.M. “Accounting in agricultural organizations”, Textbook. - M.: Finance and Statistics, 2004.-456 p.

2. Pizengolts M.Z. “Accounting in agriculture.”, T1.Ch1. Financial Accounting: Textbook. – 4th ed., revised. and additional - M.: Finance and Statistics, 2002.- 480 p.

3. Bryzgalin A.V., Bernik V.R., Golovkin A.N. “Accounting policy of an enterprise for accounting purposes,” Taxes and Financial Law, 2004.

4. Erzin D.G., “Accounting policy for tax purposes for 2004,” Russian Tax Courier No. 1,2, January 2004.

According to paragraph 3 of Article 14 of the Accounting Law, the reporting of trade and public catering enterprises refers to interim accounting statements, which include, according to paragraph 49 of PBU 4/99, “Balance Sheet” (Form No. 1) and “Profit and Loss Statement” (Form No. 2).

The legislation of the Russian Federation or the founders (participants) of the organization may provide for the submission of other reporting forms as part of the semi-annual reporting.

If, at the request of the law and (or) the founders (participants), a trade or public catering enterprise generates an expanded composition of interim accounting statements, it must ensure that identical (that is, expanded) accounting statements are submitted to all established addresses. Attention was drawn to this in the letter of the Ministry of Finance of Russia dated February 18, 2003 No. 16-00-13/01 “On the composition of the presented annual financial statements.”

In all cases, neither the tax inspectorate nor the state statistics bodies have the right to require the presentation of other forms as part of the reporting, including an explanatory note, a transcript of the list of debtors and creditors, etc. (see letter of the Ministry of Finance of Russia dated September 3, 2003 No. 16-00-14/270).

X 13.333/100 = 133 rubles

Information about the work “Container accounting”

Section: Accounting and Auditing Number of characters with spaces: 27931 Number of tables: 3 Number of images: 0

Similar works

Purchasing drinking water for the institution and accounting for containers

21244

4

0

... returns are accounted for separately from packaged water, on account 105 06 000 “Other inventories”. The institution is obliged to accept it for safekeeping and ensure timely return to the supplier. Let's look at examples of the procedure for recording transactions for the purchase of drinking water in reusable bottles. Example 1. The library entered into an agreement for the supply of bottled drinking water...

Accounting for commodity transactions in wholesale trade

216918

7

0

... these conditions, if in a trading organization the main volume of sales is carried out in retail trade, then accounting of commodity transactions should be carried out according to the rules established for retail trade. If such an organization carries out transactions for the sale of goods in the wholesale trade mode, the following adjustment entries must be made in accounting: 1. for the purchase price of goods (without ...

Accounting for goods and containers in wholesale trade organizations

85020

11

3

... and confirmed by the signature of the head of the organization (individual entrepreneur) indicating the date of correction and the seal of the organization (individual entrepreneur - if any). 2. Accounting for goods and containers in the organization of wholesale trade (using the example of individual entrepreneur ME. Zabrovsky) 2.1 Characteristics of the financial and economic activities of the enterprise Object of study of the course work ...

Accounting methodology in the Republic of Belarus

583954

93

0

..., damage, and a commission headed by the director of the enterprise makes a decision based on the results of the inventory (the acts are approved by the director). In accordance with a number of decrees of the Government of the Republic of Belarus and the Law “On Accounting and Reporting”, the cost of discovered surplus property is credited to account 92 “Non-operating income and expenses”. In cases of shortages or damage to property within...

Accounting policy for 2021 free download sample for the unified tax system

The UE prescribes its time period. It can be equal to either the minimum allowed or any time period exceeding this limit (8, 9, 10 or more years).

In addition to land plots, the UE may reflect the specifics of establishing the useful life of the fixed assets and intangible assets of an agricultural businessman.

This is relevant for the following agricultural producers on the Unified Agricultural Tax:

- switched to the Unified Agricultural Tax from a different tax regime;

- having fixed assets and intangible assets with residual value at the time of transfer.

Since the write-off of the specified property cannot be carried out at a time, but depends on the useful life of fixed assets and intangible assets, it is necessary to establish in the CP the procedure for its determination - if such information is not available in the generally applicable classification (approved by Decree of the Government of the Russian Federation dated January 1, 2002 No. 1).

For the general mechanism for registering the UE, see

Organizations and individual entrepreneurs on the Unified Agricultural Tax have become VAT payers since 2021

In this mode, you can receive deductions, but “input” VAT cannot be taken into account as expenses.

Exemption from VAT is possible in the following cases:

— the start of application of the Unified Agricultural Tax will be in 2021;

— Unified agricultural tax was used before, and for 2021 revenue did not exceed 100 million rubles.

VAT exemption

In order to apply the unified agricultural tax and not pay VAT, you need to comply with new limits.

For 2021, you can get a VAT exemption in the following cases:

— the start of application of the Unified Agricultural Tax will be in 2021;

— Unified agricultural tax was used before, and for 2021, revenue did not exceed 90 million rubles.

To apply the exemption, notice must be given.

Order of the Ministry of Finance dated December 26, 2018 N 286n and notification.

Accounting policy for tax accounting purposes

For tax accounting purposes, all rules for drawing up accounting policies are fixed and spelled out in the Tax Code of the Russian Federation.

Before moving on to the innovations of the current year, let's look at the changes that came into force in 2021:

- It is now possible to select a base on the basis of which the maximum possible amount of the reserve for doubtful debts is determined. At the same time, the volume of the reserve for doubtful debt in the presence of a counter-obligation does not exceed an amount greater than this counter-obligation.

- The 10-year restriction on the transfer of losses to a future period no longer applies, but the amount should not exceed 50% of the current tax base (clauses 2, 2.1 of Article 283 of the Tax Code of the Russian Federation).

- For the period from 2021 to 2021. tax amounts are distributed among budgets in the following proportions: 17% to the regional budget, 3% to the federal budget (Clause 1 of Article 284 of the Tax Code of the Russian Federation).

- The list of energy-efficient facilities for which accelerated depreciation can be applied has been expanded (Resolution of the Government of the Russian Federation dated August 25, 2017 No. 1006).

- The new OKOF classifier (OK 013-2014) came into effect, which, in turn, affected the classification of fixed assets put into operation after 2021 by depreciation groups.

If we talk about 2021 - Ch. 25 of the Tax Code of the Russian Federation has been updated once again. At the same time, these innovations do not require making decisions about the choice of accounting method - they mainly clarify existing rules that did not affect all taxpayers and boil down to the following:

- The list of income that is not taken into account when determining the tax base has been supplemented with income in the form (subclauses 3.6 and 3.7, clause 1, article 251 of the Tax Code of the Russian Federation):

- property rights to the results of intellectual activity identified during the inventory;

- property objects or rights (property or non-property) received as a contribution to the property of a legal entity.

- Income of non-profit organizations providing financial support for the overhaul of apartment buildings from the temporary placement of available funds (subclause 38, clause 1, article 251 of the Tax Code of the Russian Federation) is no longer considered income, which is not taken into account when determining the tax base.

- Services for the provision of guarantees by legal entities other than banks are classified as income that are not taken into account when determining the tax base, but only if they are gratuitous (subclause 55, clause 1, article 251 of the Tax Code of the Russian Federation).

- Between 2021 and 2022. water supply and sanitation facilities included in the special list have now been supplemented with the list of facilities for which accelerated depreciation can be applied (subclause 4, clause 2, article 259.3 of the Tax Code of the Russian Federation).

- Accounting for R&D expenses has undergone some changes:

- For the period 2018–2021 it is allowed to include expenses for the acquisition of exclusive rights to new developments and the rights to use them for R&D purposes (subclause 3.1, clause 2, article 262 of the Tax Code of the Russian Federation);

- R&D costs allowed to be written off as other expenses with a coefficient of 1.5 can now, with the same condition, be included in the cost of depreciable intangible assets created with the exclusive right to them (clause 7 of Article 262 of the Tax Code of the Russian Federation).

- Funds that are transferred free of charge to the budget of the Russian Federation under the agreement of targeted contributions for the electric power industry (subclause 48.9, clause 1, article 264 of the Tax Code of the Russian Federation) are now included in other expenses associated with production and sales.

Also, starting this year, changes have affected organizations that apply the “5 percent rule.” From January 1, 2021, companies must maintain separate VAT accounting in a new way - VAT can be deducted on purchases that relate to both taxable and non-taxable transactions if the share of expenses on non-taxable transactions is no more than 5% ( clause 4 of article 170 of the Tax Code). In addition, organizations will not be able to deduct input VAT on purchases of only non-taxable transactions, regardless of the share of expenses for these transactions. Now the Tax Code of the Russian Federation has established a rule: if expenses for non-taxable activities are less than 5%, then VAT on mixed expenses can be fully deducted (Federal Law dated November 27, 2017 No. 335-FZ). If expenses relate only to non-taxable activities, then VAT must be taken into account against the company’s expenses (clause 4 of Article 170 of the Tax Code).

Accounting policy for 2021 free download sample for Unified Tax Tax plus VAT

Tax payment schedule Describe the formula for calculating the Unified Agricultural Tax: the difference in income and expenses multiplied by the current tax rate (in 2021 - 6%).

Specify the procedure for calculating the annual tax amount and advance payments:

- based on data on income and expenses received at the end of the current half-year, the amount of the advance payment is calculated;

- the advance payment for the six months is transferred to the budget by the 25th day of the month following the reporting period (for the 1st half of 2021 - until July 25, 2017);

- at the end of the reporting year, the annual tax amount is calculated based on the actual indicators of the tax period;

- Upon filing a tax return, the balance of the tax amount is transferred to the budget (the annual amount minus the advance).

Accounting policies of agricultural enterprises

This means that the rules adopted by the enterprise must be established for a long period (at least a year) and cannot be changed during the reporting year; 4) these rules must be enshrined in the relevant internal document (order of the head of the enterprise approving the Regulations on Accounting Policies); 5) in the event that an enterprise cannot generate reliable information about objects based on established accounting rules, this (with appropriate justification) must be reflected in the explanatory note

The accounting option must be chosen based on the benefits for the organization’s activities, taking into account the volume of accounting work

Accounting policy for the unified tax system for 2019

Can the “Farmer” take these expenses into account when calculating the tax? The accounting policy of Farmer LLC stipulates that expenses for the purchase of land are recognized in equal shares over 8.5 years.

The legislation does not prohibit agricultural producers from reducing the tax base by the amount of expenses associated with the purchase of sown land. Therefore, guided by the accounting policy, “Farmer” has the right to reflect monthly expenses in the amount of 91,213 rubles. (9,303,800 rubles / 102 months).

Question No. 2. In December 2021, GlavKhozTrest LLC will approve the accounting policy for 2021. According to the text of the document, expenses for purchased goods reduce the tax base upon the sale of such goods. Are the accounting policies of GlavKhozTrest properly drawn up?

The specified procedure for recognizing expenses contradicts the provisions of the Tax Code, therefore GlavKhozTrest does not have the right to apply it.

Tags: asset, accountant, job description of the general director, coefficient, tax, order, expense, write-off, Form

Composition of the organization's accounting policy

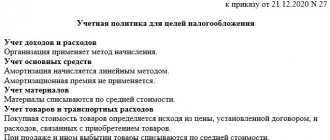

The accounting policy must be approved in December of the year preceding the year in which the accounting policy provisions are applied. For example, you can date the order to December 30 last year. Then the accounting policies will be applied from January 1 of the following year.

A check for impairment of financial investments for which their current market value is not determined is carried out whenever information appears indicating their impairment, as well as as of December 31.

Make corrections to mistakes made if they are of great importance for accounting. accounting of the previous year, identified later. In this case, a retrospective recalculation is not required.

Goods purchased for sale are recorded at cost and written off upon disposal using the _____________________ method.