Trade tax - what kind of tax is it?

The provisions of legislative acts establish that a trade tax is a mandatory payment from trade, which is calculated every quarter by business entities for payment to the budget in certain regions.

It applies to local taxes. It is expected that it will be collected by municipalities in three cities of federal significance - Moscow, St. Petersburg, and Sevastopol. However, local legislators must prepare a special legislative framework for this fee.

According to the Tax Code of the Russian Federation, for the purposes of calculating the trade tax, trade means the activity of selling goods through stationary facilities with and without retail space, non-stationary trade facilities, as well as the sale of goods from a warehouse. The obligation to calculate the trading fee also arises for the organizers of market trade.

Trade tax is levied on trade objects, which means the real and movable property of companies and entrepreneurs used by them to carry out sales.

Attention! Thus, the basis for the trade tax is not the income received from the sale of goods, but the physical indicators of the object of trade.

Trade fee calculation

The calculation formula is not very complicated (RF Tax Code, Article 417, paragraph 1):

Amount of payment for the trade fee = Rate (C) * Actual value of the physical indicator (FL)

If the object of tax calculation (FL) is the area of the sales floor, in this case it should include the following area (Tax Code of the Russian Federation, Article 346.43, paragraph 3, paragraph 5, Article 415, paragraph 5):

- Rented part of the retail space.

- Aisles for shoppers.

- Workplaces for service personnel.

- Cash registers and location of cash control units.

- Part of a pavilion or store occupied by equipment that is intended for display, serving customers, conducting cash transactions with them, and used for demonstrating goods.

Excluded area (according to letter of the Ministry of Finance No. 03-11-06/24876):

- Passages for customers (vestibules, staircases, corridors, etc.) leading to the sales floor, but not located in the hall itself.

- Premises in which customers are not served: utility rooms, premises for administrative and domestic purposes, including those used for storing and receiving goods, as well as for preparing them for sale.

Inventory and title documents are used to determine the area of a trade facility. These may include:

- Purchase and sale agreements.

- Explications, plans, diagrams.

- Technical passport of the object.

- Premises rental agreements.

- Other documents.

We also draw your attention to the fact that the fee is also paid in respect of rented property.

Where applicable in 2021

The Tax Code of the Russian Federation establishes that a trade tax should be introduced in three regions of Russia, which are cities of federal significance. These are Moscow, St. Petersburg, Sevastopol.

In order for local authorities to levy a trade tax on the territory of these subjects, they must prepare and approve a number of regulatory documents.

Currently, the corresponding law has been adopted only by the Moscow authorities. Therefore, today the trade tax is paid by business entities operating in the field of trade in the capital. The rest of the federal cities are still engaged in preparatory work.

Important! In this case, the business entity may not be registered in Moscow. It is enough that he uses a trade facility located on the territory of a given city. Before starting activities, he needs to submit a notification to the Federal Tax Service at the location of this facility.

What is a trade fee?

Trade tax (TC) is a relatively new (introduced in 2015) payment to the budget for taxpayers engaged in commercial activities. Chapter 33 of the Tax Code of the Russian Federation is dedicated to him. According to the Tax Code of the Russian Federation, this payment can be introduced only in Moscow, St. Petersburg and Sevastopol by adopting the relevant regulations. At the moment (October 2021), such a regulatory act has been adopted only in Moscow - the Law “On Trade Fees” dated December 17, 2014 No. 62. That is why issues related to the vehicle are of concern mainly to Muscovites. Although residents of St. Petersburg and residents of Sevastopol should not calm down. Recently, the country's leadership has often mentioned the emerging trend towards economic growth, and in this regard, decisions related to increasing the tax burden on business cannot be ruled out in 2018.

Who pays it

Determining the need to pay a trade tax depends on two indicators.

Tax system

The law establishes a trade fee for individual entrepreneurs using the simplified tax system and OSNO, as well as companies using the same regimes. If a business entity applies an agricultural tax or a patent system, then they are exempt from paying the fee.

A special situation has been established for those who apply UTII. The law determines that it is impossible to pay imputation and trade fees at the same time. Therefore, it is necessary to withdraw from UTII, switch to a different system, and depending on this, determine the need to use the trade tax.

Activities

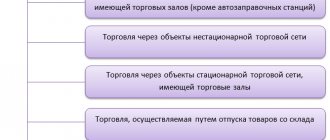

By law, all business entities that trade in retail, small wholesale or wholesale are required to make payments when using the following facilities:

- Stationary facilities with a sales area;

- Stationary facilities without a sales area;

- Non-stationary objects;

- Warehouses.

However, this type of activity must additionally be specified in local law. Thus, on the territory of Moscow, trade from warehouses is not subject to trade tax, since this type of activity is not prescribed in the adopted legal act.

Attention! The activities of retail markets are also subject to the trading tax. However, in this case, payment is made not from each trading place, but from the area of the entire market.

Who should pay the trading fee and how to calculate it in 2021 - basic rules

First of all, it is necessary to make a reservation that such a tax is quarterly. It turns out that all indicators used directly for calculations (it doesn’t matter whether you use a calculator or do the calculations yourself) are written out for the quarter. The payment, according to the Tax Code of the Russian Federation, is intended for organizations and individual entrepreneurs who operate in trade in the territory of the corresponding individual district and/or city at the federal level with the designation of the object of trade (in Moscow, rates are still the highest today, and they can be calculated using a calculator ).

When you need to calculate the amount of tax to be paid, you need to actually assign the physical characteristics of the element of the sale (for example, the area of the property, which can be taken from the accompanying documents) multiplied by the rate in the district.

This physical characteristic of an element usually means (this depends on the segment of the activity being carried out) the area of the object, or the element of trade itself.

In today's Tax Code of the Russian Federation, only the maximum maximum rates are written down, and the final contributions, calculated using a calculator, are required to be established by municipal structures separately.

Trade fee in 2021 in Moscow

This tax in 2021 will only apply to the capital, where there will be only Moscow rates (you can calculate it using a calculator). They differ not only in the segment of trading activity, but also in the address where the sales element is located, which is quite fair. After all, in fact, there is, for example, a newspaper stand on Tverskaya Street. or on the edge of Moscow, the profit of its owner/tenant will also depend.

Trade tax in St. Petersburg

In February/March 2015, the Council of Deputies submitted a bill to the State Duma (taking into account the Moscow region) establishing a three-year break for the introduction of trade taxation within the borders of the Moscow region, St. Petersburg and the new Sevastopol. They justified such a decision by saying that such a tax would certainly be an additional tax sanction and an administrative stopper for business.

The trade fee reduces the tax under the simplified tax system by what percentage?

Now, everyone working according to the “simplified” rules has the right to indexation of the amount, which cannot be more than 50% of all taxes paid.

What is subject to trading tax in 2020

To calculate the trade fee, it is not the income indicator (real or conditional) that is used, but the very fact of the existence of a retail facility. The latter refers not only to real estate in the form of kiosks or shops, but also delivery trade.

Thus, payment of the trade fee does not depend on the following indicators:

- Availability of ownership rights to the retail outlet. Business entities that use real estate for trading activities are required to pay the fee, regardless of whether they are owners or tenants;

- Amount of income. This indicator is not involved in determining the fee. In fact, the amount of tax determines the type and location of the object;

- Place of registration of the business entity. If the activity is carried out in a territory that is subject to a trade tax, it must be paid regardless of the actual registration of the businessman;

- Regularity of trade. The fee must be calculated and paid once a quarter, regardless of whether trading activity was carried out during this period or not.

Attention! The sales fee is determined based on two physical characteristics - the actual presence of the object and the area of the trading floor.

If in the first case a ready-made rate indicator is used, then in the second case it is necessary to allocate the area of the hall from the total area of the store. To avoid problems with regulatory authorities, the last figure must be taken from official documents.

Examples of calculating trade fees

To get the amount of tax you must pay, you need to multiply the square footage of your retail property by your county's rate. Let's consider a specific example of calculation. How much will the owner of a stationary network trading floor with an area of 100 square meters pay? meters in Vnukovo? Since the area is more than 50 sq. meters, first we calculate the tax on them: 50 x 420 = 21,000 rubles. Next 50 sq. meters cost 50 x 50 = 250 rubles.

Another example: a businessman owns two properties. One of them is in the market, its area is 40 square meters. meters, the other is a non-stationary retail network in Butovo. In the first case, the location does not matter; in the second, the area of the object does not matter. A place on the market will cost the owner 40 x 50 = 2,000 rubles, and a second object will cost 28,350 rubles.

What types of activities are not subject to trade tax?

Local authorities have the right to determine a list of activities for which it is not necessary to calculate and transfer the trade tax. The following activities are established for Moscow:

- Retail trade using automatic machines;

- Sales at weekend fairs, special and regional fairs;

- Trade in theaters, museums, cinemas, provided that at the end of the quarter the income from ticket sales is at least 50%;

- Trade at vegetable warehouses;

- Trade through facilities located on the territory of markets;

- Autonomous budgetary and government institutions;

- Post offices;

- Non-stationary retail outlets that sell printed products;

- Religious organizations when selling in their places of worship.

You might be interested in:

Limit value of the base for calculating insurance premiums in 2019: table of values

In addition, the following types of household services are exempt:

- Hairdressers and beauty salons;

- Laundries, dry cleaners;

- Repair of shoes, clothes, watches, jewelry;

- Manufacturing of haberdashery and keys.

However, for all these objects additional conditions are established:

- Providing services is the main source of income for them;

- The size of the object is no more than 100 sq. m., while the display and demonstration of goods is carried out on no more than 10% of the area.

Attention! Online stores do not need to pay a fee, provided that they do not provide courier delivery of goods with payment on the spot.

All business entities that fall under the trade tax benefit must still register with the Federal Tax Service, indicating the type of benefit in the notification.

General information about the trade fee

Trade tax (TS) is a relatively new payment to the budget established by the Tax Code of the Russian Federation in November 2014 for commercial firms selling goods in Moscow, St. Petersburg and Sevastopol. However, it can only be collected if the legislative assemblies of the listed cities adopt normative legal acts that put it into effect. At the moment, only the capital authorities have developed and approved relevant regulatory sources.

In general, the calculation of the trade fee by legal entities and individual entrepreneurs who are its payers must be carried out independently. The fact is that when registering with the Federal Tax Service as a tax payer, they must submit a notification to the tax authorities in the TS-1 form, which indicates:

- the collection rate in rubles established for a specific type of retail facility;

- collection rate in rubles established for 1 sq. m area of the used retail facility;

- calculated vehicle for the quarter;

- information about vehicle benefits;

- the actual amount of trade tax payable for the quarter.

Moreover, the first 2 indicators are mutually exclusive. We will consider the features of their use later in the article.

If the listed information is not provided, then the tax authorities, having discovered the fact that the company is carrying out trading activities, will independently accrue TC based on the available data on the objects of trading. However, these figures will most likely be quite unexpected for the owner of a company or individual entrepreneur.

The amount indicated in the tax notice of payment of the trade fee must be paid into the budget by the 25th day of the month following the previous quarter. If the vehicle is not paid, then the Federal Tax Service, as in the case of other taxes, will require this to be done, and may also impose a fine in the amount of 20% of the unpaid amount of the fee and penalty in accordance with Art. 75 of the Tax Code of the Russian Federation. If a company deliberately evades making the appropriate payment to the treasury, the fine will be 40%.

Thus, it is in the interests of the entrepreneur to provide the Federal Tax Service with calculations of the trade tax in advance by sending Form TS-1.

Trade tax rates in Moscow in 2021: table

Let's consider the rates for trade fees in Moscow in 2021, which are set depending on the location of the trade facility.

| Type of trade | Central administrative district (CAO) | Zelenogradsky, Trinity and Novomoskovsky JSC | Southern administrative district (Southern Administrative District) |

| Trade through a stationary network that does not have halls (without gas stations) | 81000 rub. for each object | 28350 rub. for each object | 40500 rub. for each object |

| Trade through a non-stationary network (except for delivery and distribution) | 60,000 rub. for each object | 21000 rub. for each object | 30,000 rub. for each object |

| Trade through facilities with halls up to 50 sq. m. | 1200 rub. for every sq. m. area up to 50 sq. m. | 420 rub. for every sq. m. area up to 50 sq. m. | 600 rub. for every sq. m. area up to 50 sq. m. |

| Trade through facilities with halls over 50 sq. m. m. | 50 rub. for every sq. m. area over 50 sq. m. | 50 rub. for every sq. m. area over 50 sq. m. | 50 rub. for every sq. m. area over 50 sq. m. |

| Delivery and distribution trade | 40500 rub. for each object | ||

| Retail markets | 50 rub. for every sq. m. market | ||

Continuation:

| Type of trade | Molzhaninovsky district of Northern Administrative Okrug Northern district of NEAD Vostochny, Novokosino and Kosino-Ukhtomsky districts of the Eastern Administrative District Nekrasovka SEAD Northern Butovo and Southern Butovo South-Western Administrative District Solntsevo, Novo-Peredelkino and Vnukovo CJSC Mitino and Kurkino North-West Administrative District | All areas of the Northern Administrative District (except Molzhaninovsky) All districts of NEAD (except Northern) All districts of the Eastern Administrative District (except for the districts of Vostochny, Novokosino and Kosino-Ukhtomsky) All districts of the South-Eastern Administrative District (except for the Nekrasovka district) All districts of the South-Western Administrative District (except for the Northern Butovo and Southern Butovo districts) All districts of the closed joint-stock company (except for the districts of Solntsevo, Novo-Peredelkino and Vnukovo) All districts of the Northwestern Administrative District (except for the Mitino and Kurkino districts) |

| Trade through a stationary network that does not have halls (without gas stations) | 28350 rub. for each object | 40500 rub. for each object |

| Trade through a non-stationary network (except for delivery and distribution) | 21000 rub. for each object | 30,000 rub. for each object |

| Trade through facilities with halls up to 50 sq. m. | 420 rub. for every sq. m. area up to 50 sq. m. | 600 rub. for every sq. m. area up to 50 sq. m. |

| Trade through facilities with halls over 50 sq. m. m. | 50 rub. for every sq. m. area over 50 sq. m. | 50 rub. for every sq. m. area over 50 sq. m. |

| Delivery and distribution trade | 40500 rub. for each object | |

| Retail markets | 50 rub. for every sq. m. market | |

Who should pay the trade tax

The circle of persons obligated to register with the tax authority as a payer is determined by Art. 411 and art. 413 of the Tax Code of the Russian Federation and is specified in Art. 2 of the Moscow Law “On Trade Fees”. These include legal entities (except for those using the Unified Agricultural Tax) and individual entrepreneurs (except for those operating under a patent or located on the Unified Agricultural Tax), carrying out:

- the process of organizing retail markets (the fee is levied on the entire market area, not objects);

- trade of various scales (wholesale, retail, small wholesale) using property:

- trade through stationary facilities, with or without (with the exception of gas stations) sales areas;

- trade through non-stationary objects, including delivery and retail trade.

In addition, the list of the Tax Code mentions trade by releasing goods from a warehouse as a taxable activity, but in the Moscow Law this point was omitted when establishing the amount of the fee, which suggests that the capital authorities decided not to impose a trade tax on this type of activity .

Tax calculation example

Stolitsa LLC owns three kiosks in the Central Administrative District of Moscow, as well as a store with an area of 76 square meters. m. on the territory of the Southern Administrative District.

The rate for a kiosk on the territory of the Central Administrative District is 81,000 rubles per object. The rate for a store in the Southern Administrative District is 600 rubles for the first 50 square meters. m, and 50 rubles for all subsequent ones.

Collection amount for the store: 600 x 50 + 26 x 50 = 31,300 rubles.

Collection amount for kiosks: 81,000 x 3 = 243,000 rubles.

Total fee per quarter: 31,300 + 243,000 = 274,300 rubles.

How to calculate trade fee?

The calculation of the vehicle in 2021 is carried out by the taxpayer independently. To do this, you need to multiply the vehicle rate by the physical parameter of the object. This parameter can be either the number of household objects of a given type (if the object itself is taxed), or the area of the household object (if a unit of area is taxed for this type of retail outlets).

The payment deadline for the vehicle is the 25th day of the month after the end of the billing quarter.

Example

Individual Entrepreneur Semyon Fedorovich Smolentsev owns the following retail outlets:

- A store with an area of 70 sq. m in New Moscow.

- Two pavilions with an area of 30 sq. m and 35 sq. m inside the Moscow Ring Road (outside the Central Administrative District).

- A stall in the Central Administrative District.

How does S. F. Smolentsev calculate the trading fee:

- per store - 21,000 rubles. + (50 rub. × 20 sq. m.) = 22,000 rub.

- For pavilions - 2 × 30,000 rubles. = 60,000 rub.

- For a stall - 1 × 81,000 rubles. = 81,000 rub.

The total amount of TC for the quarter payable by S. F. Smolentsev:

22,000 + 60,000 + 81,000 = 163,000 rubles.

Procedure for registering as a tax payer

The payer of the trade tax is an entrepreneur or company that has sold goods at least once during the quarter in the territory of the municipality where the trade tax has been introduced. In this case, you must independently register with the tax authority as a payer.

For this operation, a special notification has been developed in the TS-1 form. It can be submitted in one of the following ways:

- In person in paper format;

- By mail with the described attachment;

- When using Internet services, the document must be signed with an electronic signature.

The business entity is given five days to complete this operation. The application must indicate the type of activity, as well as the details of the outlet. After processing the notification, the Federal Tax Service provides the taxpayer with a certificate of registration.

Important! Even those business entities that fall under the established benefits are required to submit a notification and do not have to pay customs duties.

If trading activities are terminated, the entity must draw up a special TS-2 notification. It specifies a specific end date for the activity and the fee must be calculated for that date. It is mandatory to submit this form; if the activity is actually completed, but the notification has not been sent, then the business entity will still be required to calculate and transfer the trade fee.

Procedure for paying trade tax

An organization carrying out trade using an object is required to register with the tax authority of the region where the object is registered or trade is conducted and obtain a vehicle payer certificate. To do this, you need to submit a notification (form TS-1).

The notification indicates: type of activity, trade objects, its characteristics (area, quantity).

Situations may arise:

- If the object is registered in Moscow, and the company is outside it, then a notification of registration must be submitted to the Moscow inspectorate.

- If a non-stationary object is registered (car store) outside of Moscow, and trade takes place on the territory of Moscow, then you also need to register in Moscow.

- If there are several retail facilities in Moscow, registered in different areas, then you need to submit one notification indicating the list of facilities. This notification is submitted to the inspectorate in which the first object on the list is registered.

In case of termination of trading activities, it is necessary to deregister with the tax office. To do this, you need to submit a notification indicating the date of termination of trade (form TS-2).

If the parameters of a retail facility (area, location) change, it is also necessary to submit a notification.

The notification is submitted within five working days from the date of acquisition of the trade item (or the occurrence of any changes). Further, from the moment of registration of the notification, the company is registered within 5 days. From the moment of registration, the payer receives a certificate (TC form) from the tax authority. Even if an organization falls under the exemption and does not pay the trade fee, it is still required to register.

Notifications can be submitted in paper or electronic form with an electronic signature on the website of the Federal Tax Service of the Russian Federation. Penalties for failure to register are presented in the table.

| Type of violation | Amount of fine |

| For failure to comply with registration deadlines. | 10,000 rubles. |

| For carrying out trade without registration. | 10% of income as a result of trading for the reporting period, but not more than 40,000 rubles. |

| Late submission of notification of changes in the parameters of a retail facility. | 200 rubles. |

| Inaccurate information in the notification, resulting in an incomplete payment of the fee. | 20% of the amount of the unpaid fee (if it was not intentional) + additional payment of the fee. 40% of the amount of the unpaid fee (if it was intentional) + additional payment of the fee. |

Where is the notification sent?

I defined the nuances of registering as trade tax payers in my letter.

It says that the registration and deregistration procedure must be carried out:

- If the activity for which it is necessary to pay a trade fee is carried out using a property - at the location of the property;

- In all other situations - at the location of the company or the place of residence of the entrepreneur.

For example, if an entrepreneur is registered in the Moscow region, or another region of the country, but in Moscow carries out activities in the form of trade in real estate, then he is obliged to send a notice of the trade fee to the inspectorate for the location of this property.

Attention! However, the same entrepreneur who sells in Moscow from a car shop or trade tent must register at his place of residence.

If an entrepreneur has several points in the territory of the municipality from which he is obliged to pay the trade tax, but they belong to different inspections, then the notification must be sent to the Federal Tax Service authority, whose outlet will be indicated first on the form.

Penalty for late submission of notice

If a business entity carries out trade that is subject to the trade tax, but has not issued a TS-1 notification within the established time frame, this will be equated to illegal entrepreneurship, i.e., conducting activities without tax registration.

For this violation, a fine is provided in the amount of 10% of the income received from this activity, but not less than 40,000 rubles. This punishment is established by the Tax Code.

In addition, according to the Code of Administrative Offenses, a fine may be imposed on officials. It will be 2-3 thousand rubles.

Is there reporting on vehicles?

No additional reporting has been introduced for the trading fee. Therefore, there is also no obligation to provide a declaration at the same time as paying the fee. However, there are several mandatory forms that every fee payer must fill out.

When registering, each payer sends a notification TS-1. In the event that a business entity changes information about the taxable object, its location, etc., then you also need to fill out and submit the TS-1 form.

Since payers of the fee have the right to reduce calculated income taxes or similar ones by these amounts, the amount of the fee is indicated in the corresponding declaration:

- In the income tax return, which is prepared by those located on OSNO, data on the trading fee is entered on Sheet 02, in lines 265-281.

- Entrepreneurs who report income by filing a 3-NDFL declaration indicate the amount of the fee paid in Section 2 of this form;

- Individual entrepreneurs and companies that use the simplified tax system for income submit a declaration under the simplified tax system. It contains a separate Section 2.1.2 for the purposes of the trade fee. Business entities that do not pay the fee simply do not fill out this sheet of the form;

- Individual entrepreneurs and companies that use the simplified tax system “income minus expenses” reflect the amount of the fee paid in the Book of Income and Expenses in the column “Expenses”. There are no separate fields in the declaration for this case.

How to Avoid Trade Fees

Individual entrepreneurs will be able to avoid trade tax if they switch to a patent tax system. The annual cost of a patent is determined to be 6% of your local government's potential annual income (this amount can be found in the relevant law in your region). For example, for stores with a retail area of up to 50 sq. m in the central regions of Moscow, a patent costs 324,000 rubles per year. From 2021, the patent is allowed to be reduced by insurance premiums.

However, before switching to a patent, it is necessary to make sure that the individual entrepreneur falls under the conditions of application of this regime.

Where do you need to pay for the vehicle?

The Tax Code establishes that the trade fee is a local level tax. Local authorities are directly involved in determining the procedure for its calculation, as well as benefits. It follows from this that the payment of this payment should be made to the local budget.

According to the Tax Code, the tax period is set to a quarter. The amount of the fee must be calculated starting from the quarter in which the notification was sent to the tax authority.

The transfer of the fee is made before the 25th day of the month that follows the billing quarter.

If the authorized body reports to the tax office about identified objects of taxation for which the business entity itself has not sent a notification, then the trade tax must be transferred within 30 days from the date of receipt of the information.

The payment order is issued as for ordinary taxes. The KBK trading fees are set as follows:

- for tax - 182 1 0500 110;

- for penalties - 182 1 0500 110;

- for a fine - 182 1 0500 110.

The procedure for reducing taxes by the size of the vehicle

According to the law, taxpayers in some cases may indicate the listed amounts of trade tax as expenses in the applicable tax systems, and in others they have the right to reduce the calculated income tax (or a payment replacing it) by the amount paid.

BASIC

With this system, the trade tax cannot be expensed, but the amount of the calculated income tax (or advance payment) can be reduced. It is necessary to take into account that only that part of the tax that is transferred to the local budget is subject to reduction.

Entrepreneurs paying personal income tax

They can reduce the amount of personal income tax, which was determined at the end of the year at a rate of 13%. There is a nuance when reducing taxes. This operation can only be done if the entrepreneur trades at the place of registration and pays personal income tax in the same area.

Important! However, in the case when an individual entrepreneur pays tax at his place of registration, but carries out trading activities and pays trade taxes in another city, then it is impossible to reduce the tax.

simplified tax system income minus expenses

In this system, it is allowed to include the amounts of the listed trade fee among the expenses that reduce income when determining the single tax.

simplified tax system income

Entrepreneurs and companies on this system have the right to reduce the single tax by the amounts of trade tax that were paid in the same period. But there is also a nuance here - such a reduction is only possible if the single tax and the vehicle are transferred to the same local budget.

If several types of activities are carried out on the simplified tax system, then a trade tax deduction can only be obtained from the tax on receipts from retail trade. In this case, the individual entrepreneur or company will need to organize separate accounting of income from trade and other activities.

We reduce taxes by the amount collected

The law provides for the possibility of reducing taxes by the amount of trade tax paid. Individual entrepreneurs working on the general taxation system can reduce the amount of personal income tax at the end of the year, and organizations have the opportunity to reduce income tax and that part of advance payments that is paid to the budget of the constituent entity of the Russian Federation in the territory in which this fee was introduced.

Individual entrepreneurs and organizations using the simplified tax system with the “Income” will be able to reduce the amount of tax and advance payments remaining after the reduction in insurance premiums. However, the same condition applies: the tax can be reduced only if the fee and the simplified tax system are paid in the same region.

Individual entrepreneurs and organizations using the simplified tax system with the object “Income minus expenses” will be able to include trading fees as expenses. Thus, the amount of the trade tax increases expenses, rather than reducing the amount of tax.

Contour.Elba will help here too! We will automatically calculate how much less the tax amount will be and tell you where the sales tax is included.