To avoid claims from tax inspectors, an accountant needs to know how to correctly arrange business trips and how to take into account business travel expenses for tax purposes. In this article we talk about the taxation of travel expenses - how certain expenses incurred by the company when sending a subordinate on a business trip will affect the calculation of income tax, personal income tax, insurance contributions to extra-budgetary funds, payments in case of occupational diseases and accidents on production and VAT.

Taxation of travel expenses: value added tax (VAT)

An accountant has the opportunity to apply for a deduction for value added tax only if the goods (work, services) that were purchased by a seconded employee on a trip were purchased on the territory of one of the constituent entities of Russia.

In the event that the route begins or ends abroad of the Russian Federation, services for the transportation of baggage or the transportation of passengers, which were issued under uniform international transportation documents, will be subject to VAT at a zero rate. Accordingly, there is no requirement to include VAT in the cost of a travel ticket (train or plane) to the destination of the posted employee located abroad and back to the place of permanent work.

Important!

If the VAT amount in travel documents purchased in one of the CIS countries is written on a separate line, a tax deduction cannot be issued.

The inability to claim for tax deduction the amount of VAT indicated on the travel document as a separate line is explained by the fact that:

- The place of sale of services, as a general rule, is the place where the company operates or services are provided to an individual entrepreneur.

- An exception to this rule are the situations referred to in paragraphs. 1-4 p. 1 tbsp. 148 of the Tax Code (that is, in each of these cases, the service is still considered to be sold on the territory of the Russian Federation).

- Railroad transportation is not included in the list of exceptions to the general rule, since nothing is said about them in the mentioned article of the Tax Code of the Russian Federation (which means that transportation services will be provided in the country in which the carrier company operates).

In connection with all of the above, a ticket purchased at the ticket office of an airline or railway station in another country makes it clear that the services of the carrier company are provided not on the territory of Russia, but abroad. That is why the “input” VAT, written as a separate line in the travel document, is not claimed by the company’s accountant for tax deduction.

Which employee trips can be considered business trips?

According to Art. 166 of the Labor Code of the Russian Federation, a business trip is recognized as sending an employee outside the enterprise on behalf of the employer to resolve production issues and perform official tasks. The minimum duration of such a trip is one day, but the maximum is unlimited (its duration is determined by the employer, taking into account the complexity and volume of the work ahead).

The following cannot be considered a business trip:

- a business trip that does not require the employee to travel outside the locality in which the employing organization is located;

- business trips of persons whose permanent work is traveling in nature (couriers, forwarders) or carried out on the road (this is how conductors and train drivers work). Since travel is part of a job function, they cannot be considered a business trip;

- travel of employees working at the enterprise on GPC terms.

Taxation of travel expenses: insurance contributions to extra-budgetary funds

According to the text of Federal Law No. 212-FZ of July 24, 2009, from January 1, 2010, enterprises must make deductions of insurance payments to extra-budgetary funds instead of paying the unified social tax (UST). Insurance premiums are levied on employee payments specified in employment agreements. The list of payments for which insurance premiums are not charged is listed in the text of Article 9 of the mentioned legislative act. For example, insurance premiums should not be charged for compensation paid to subordinates for expenses incurred in the performance of their official functions. As for business trips, if the posted employee has documents proving the fact of incurring expenses, the compensation payments issued to him will not be subject to contributions.

Important!

If an employee returning from a business trip does not have documentary evidence of the expenses he incurred on a business trip, only amounts within the limits approved by current legislation will not be subject to insurance premiums.

The following payments to seconded employees returning from a trip are not subject to insurance payments:

- daily allowance (the rate of payment must be specified in the collective agreement or other internal act of the company);

- costs of purchasing a travel ticket to the destination and back to the employer’s enterprise;

- costs of exchanging cash at a currency exchange office (or checks at a banking institution) for foreign currency;

- consular fee for visa application;

- costs of paying for telephone operator services and other communication services;

- costs of rented living quarters;

- costs for transporting personal belongings (luggage);

- costs of purchasing tickets in public transport (sometimes paying for taxi services) to travel to the place of train departure or plane departure, to the destination or to the place of transfer;

- various commission fees;

- airport fees.

Taxation of travel expenses: personal income tax

Costs incurred by a posted employee while on a business trip are not subject to personal income tax, since the company only compensates the employee for expenses (that is, the amount of compensation does not bring commercial benefits to the subordinate).

Important!

If the amount of daily payments exceeds the norm (when traveling within Russia - 700 rubles per day, when traveling abroad - 2,500 rubles per day), the excess amount is included in the tax base for calculating personal income tax. If the daily allowance was paid in foreign currency for a trip abroad, it is necessary to calculate the amount in rubles at the Central Bank exchange rate on the date of payment.

The accountant must also remember that if an employee incurred expenses to pay for rented housing (hotel room or apartment) and received compensation in an amount exceeding the amount of 2.5 thousand rubles per day of stay (without confirming the expenses with payment documents residential premises), personal income tax must be withheld from the compensation amount.

Important!

Compensation payments for VIP lounges (at airports open for international traffic, Russian border checkpoints at railway stations, sea and river ports) are not subject to personal income tax - this decision was made by the Arbitration Judges and the Federal Antimonopoly Service of the Moscow Region (the Ministry of Finance has a different opinion) .

If an accountant doubts whether personal income tax should be withheld from compensation for the use of taxi services while an employee is on a business trip, when there is documentary evidence of payment for travel, the following rules should be followed:

- If the employee traveled by taxi to the destination, place of departure or transfer point, the compensation payment does not need to be subject to personal income tax.

- If the employee used the services of a taxi to travel to the destination and back to the employer, personal income tax is also not required to be withheld from compensation.

- If public transport was not available at the time required by the subordinate, and he had to use a taxi to get from the hotel to work, the amount of compensation is not subject to income tax, but provided that there are documents confirming the fact of the trip, the call of a taxi is due to production needs, and the possibility of using taxi service is specified in the collective agreement of the enterprise.

- If a posted employee took a taxi around the city during a business trip, the compensation amount is subject to personal income tax.

The following are cases when it is necessary to charge personal income tax on compensation for payment of rented housing by a posted employee, and when tax withholding is not required:

- In any case, if the employer paid the employee compensation for travel and/or accommodation costs, while the employee did not provide documents confirming the expenses, personal income tax is charged on the entire amount of compensation.

- If the employer agrees to compensate for accommodation costs, including breakfast at the hotel, personal income tax will have to be withheld from the cost of food (insurance contributions must also be calculated).

Daily allowance for a business trip in Russia 2020

Daily allowances in Russia are paid based on a fixed amount of money for one day of work. The rate is multiplied by the number of business travel days, including travel. The fee for one day can be any, but not less than 100 rubles.

Income and contributions are not taken from the limit of 700 rubles. per day in Russia. This means that everything issued in excess of the norm is subject to personal income tax and contributions.

All days are taken into account, including travel time, forced stops on the road, days of residence, delays due to business needs or force majeure.

An example of calculating daily allowance in Russia in 2021.

Kulik A.G. sent by the general director of the company to Voronezh to conduct a week-long training course for employees of a branch of the company. Kulik presented train tickets, from which it follows:

She left for Voronezh on 04/06/2020 at 19:00. 45 min;

- Returned back to Moscow on 04/11/2020 at 5:20 am.

- The collective agreement states that the daily allowance in Russia is 1000 rubles.

Let's calculate travel expenses:

- Number of business trip days: from 04/06/2020 to 04/11/2020 – 6 days;

- Daily allowance: 1000 * 6 = 6000 rubles;

- We find the limit exempt from personal income tax and contributions: 6 * 700 = 4200;

- We calculate the balance subject to tax and contributions: 6000 – 4200 = 1800;

- Subtract income: 1800 – (1800*13%) = 1800 – 234 = 1566;

- The total payment to Kulik will be: 4200 + 1566 = 5766 rubles.

Taxation of travel expenses: income tax

The procedure for accounting for expenses incurred by the company for an employee’s business trip is presented in the table below:

| Type of expenses | Possibility of taking into account costs when calculating income tax |

| Daily allowance | The full amount of daily allowance can be taken into account when calculating income tax. In this case, no documents confirming expenses are required - an accounting certificate with calculations, an order for sending on a business trip, tickets indicating the point of departure and arrival are sufficient. |

| Compensation for travel to the destination and back to the employer’s enterprise | Can be fully taken into account when reducing the tax base for income tax. When purchasing luxury train tickets (or business class air tickets), their cost can also be taken into account in full. If there is documentary evidence and justification for the need to pay for a luxury lounge or the cost of chartering an aircraft for travel to the place of performance of an official assignment and back to the place of work, these costs can also be taken into account when calculating income tax. |

| Travel compensation in case of loss of travel documents confirming the fact of the trip | If it was not possible to obtain a duplicate ticket, copy of a travel document or a certificate from the transport company, it is prohibited to take into account travel expenses when calculating income tax. |

| Compensation for the purchase of an electronic ticket | If there is documentary evidence of the purchase of an electronic ticket (printout, boarding pass, cash register receipt, slip, electronic terminal receipt), you can take into account the cost of the electronic document when calculating income tax. |

| Taxi fare compensation | Taxi fares can be taken into account if:

|

| Compensation for living expenses | If there is documentary evidence of payment for housing, the company's expenses can be taken into account in full. If there are no documents, costs cannot be taken into account. |

| Visa costs | If the trip took place, you can take the expenses into account when calculating your income tax. If the employee has not traveled abroad, costs cannot be taken into account. |

| Losses associated with payment of a fine for returning a ticket in case of interruption of an international business trip | You can include it in expenses and reduce the tax base for income tax. |

| Expenses for the services of intermediary companies (travel agencies, etc.) | They can be taken into account if there is a certificate of work performed with a breakdown of the cost of each service provided. |

What is the amount of daily allowance not subject to personal income tax in 2021?

Fiscal authorities can also take into account funds spent and not documented in excess of the standards in the base for calculating personal income tax (Resolution of the Federal Antimonopoly Service of the West Siberian District dated December 23, 2013 No. A27-1862/2013). The validity of the payment of the daily allowance itself within the limits established by law in the event of the loss of travel documents can be confirmed by local documents of the enterprise - orders for sending on a business trip, time sheets, reports on the completion of official assignments. Read the article about what actions to take in the absence of residence documents.

When one-day business trips occur, compensation payments to employees are not considered daily allowance. Such costs should be classified as other expenses (Article 168 of the Labor Code of the Russian Federation). However, such compensation payments are subject to personal income tax according to the same standards - 700 rubles.

in the Russian Federation, and over 2,500 rubles. - outside the territory of the Russian Federation. This is confirmed by officials (). In some cases, business trips take place within the same locality.

When an employee travels outside the workplace specified in the employment contract to separate divisions of the organization or the head office, the trip is also considered a business trip (clause

3 of the Decree of the Government of the Russian Federation of October 13, 2008 No. 749). At the same time, trips should not be permanent, and the employee’s activities cannot be associated with a traveling schedule. Read about the peculiarities of personal income tax taxation of payments for the traveling nature of work.

For a one-day business trip outside the state, daily allowance is paid in the amount of 50% of the standard expenses outside the Russian Federation (clause

20 of the Decree of the Government of the Russian Federation of October 13, 2008 No. 749). Such daily allowances are also not subject to personal income tax within generally accepted limits.

Legislative regulation

| Decree of the Government of the Russian Federation dated December 29, 2008 No. 1043 | On the abolition of the daily allowance rate of 100 rubles |

| clause 3 art. 217 Tax Code of the Russian Federation | The fact that travel expenses, confirmed by documents, are not included in the tax base for personal income tax |

| Art. 210 Tax Code of the Russian Federation | On the withholding of personal income tax from compensation for payment of accommodation and travel on a business trip, if the amounts of expenses were not documented |

| Letter of the Ministry of Finance of the Russian Federation dated October 14, 2009 No. 03-04-06-01/263 | On the withholding of personal income tax from the cost of breakfasts included in the invoice for hotel accommodation |

| Letter of the Ministry of Finance No. 03-03-06/1/30978 | On the possibility of taking into account, when calculating income tax, a company’s expenses for a remote employee’s business trip |

How to reflect daily allowances in ERSV and 6-NDFL

If you did not include non-taxable daily allowance in the calculation, then it is not necessary to submit an update. In letter No. GD-4-11/, the Federal Tax Service insists that an updated calculation must be sent. But the code requires clarification of the report if the company has underestimated contributions (clauses 1 and 7 of Article 81 of the Tax Code). In this case, the daily allowance did not affect the calculation of contributions, so the organization has reasons not to clarify the ERSV. But if you still decide to correct the report, submit clarifications for all periods from the beginning of the year in which you did not show non-taxable daily allowances.

6-NDFL

. In 6-NDFL, do not record non-taxable daily allowances. Reflect only daily allowances in excess of the norm.

Answers to common questions about taxation of travel expenses

Question #1:

How can an accountant reflect in an employee’s income certificate in Form 2-NDFL the amount of daily allowance by which the payment established by the collective agreement was exceeded and from which personal income tax was withheld?

Answer:

You need to enter data in Section 3 according to income code 4800 “Other income” (instructions are contained in the Appendix to the Order of the Federal Tax Service of Russia dated October 13, 2006 No. SAE-3-04 / [email protected] - in the “Income Codes” directory).

Question #2:

How will the costs incurred by a company to obtain a visa for an employee affect the payment of personal income tax and income tax if the business trip ultimately does not take place?

Answer:

Such costs should not be taken into account when calculating income tax. Also, such expenses will not be included in the employee’s personal income tax tax base.

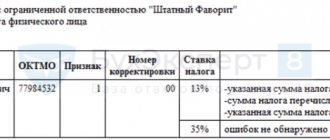

Deadlines for personal income tax payment in 2021: table

To avoid such costs, it is important to be aware of payment dates and adhere to them. See the table for the deadlines for paying personal income tax on different types of income of individuals: wages, vacation pay, sick leave benefits and other payments

Type of income Deadline for transferring personal income tax Salary The next working day after the payment of money Vacations The last day of the month in which the money was transferred to the employee Sick leave The last day of the month in which the money was transferred to the employee Excessive daily allowances for business trips and reimbursement of expenses without supporting documents The next working day after the payment of money Bonuses Next working day after payment of money Type of income When to recognize income When to withhold tax When to transfer personal income tax Basis Salary and bonuses Advance The last day of the month in which the advance was paid On the day of issuance of the second part of the salary The next working day after the issuance of the second part of the salary Clause 2 of Art. 223, para. 1 clause 6 art. 226 of the Tax Code of the Russian Federation Final payment of wages Last day of the month in which income was accrued At the time of payment after recognition of income Next working day after payment of money P

See the table for the deadlines for paying personal income tax on different types of income of individuals: wages, vacation pay, sick leave benefits and other payments. Type of income Deadline for transferring personal income tax Salary The next working day after the payment of money Vacations The last day of the month in which the money was transferred to the employee Sick leave The last day of the month in which the money was transferred to the employee Excessive daily allowances for business trips and reimbursement of expenses without supporting documents The next working day after the payment of money Bonuses Next working day after payment of money Type of income When to recognize income When to withhold tax When to transfer personal income tax Basis Salary and bonuses Advance The last day of the month in which the advance was paid On the day of issuance of the second part of the salary The next working day after the issuance of the second part of the salary Clause 2 of Art. 223, para. 1 clause 6 art. 226 of the Tax Code of the Russian Federation Final payment of wages The last day of the month in which the income was accrued At the time of payment after the recognition of income The next working day after the payment of money P.

2 tbsp. 223, para. 1 clause 6 art. 226 of the Tax Code of the Russian Federation Salary in kind The last day of the month in which the income was accrued From the first cash payment after the income was recognized The next working day after the payment of cash income Clause 2 of Art. 223, para. 1 clause 6 art. 226 of the Tax Code of the Russian Federation Bonuses for holidays, for example, for an anniversary The day when the bonus was paid At the time of payment The next working day after the money was paid Sub.