Who is a tax resident and who is a non-resident?

Statuses are determined by the Tax Code of the Russian Federation (Chapter 23) in order to determine the percentage tax rate for individuals. “Resident” status is granted to persons who are registered and reside in the country and comply with the requirements of the law.

Citizens included in a certain list approved by the legislative bodies of the Russian Federation have “resident” status:

- citizens of Russia (having a civil passport), if they do not live abroad for more than 365 days, as well as those who have received a residence permit of another country;

- staying in another state on a study/work visa;

- foreigners who have received a residence permit;

- officially registered legal entities;

- employees of consulates and diplomatic institutions located in other states;

- municipal bodies and their constituent entities.

Non-residents are individuals/legal entities without a permanent place of residence (not residing on a permanent basis). Such citizens are those who stay less than 183 days in the country within 1 year.

It is important to understand the difference, because even having Russian citizenship, but at the same time being, for example, at work in another state, a person becomes a resident of another country.

Note! Determination of status is directly related to taxation, and also determines the portion of income that is subject to taxation. For a non-resident, the taxable part is the income that he receives in Russia.

What does obtaining a residence permit give?

The main advantages for a foreigner holding a residence permit are the following:

- During the validity period of the residence permit, its holder has the right not to leave the country.

- You can leave Russia as many times as you like, as well as return to Russia, but you can spend no more than 6 months per year abroad. If he has a residence permit, his status as a resident or non-resident will be determined depending on the time he spent abroad.

- It is free to choose your place of residence or place of stay in Russia, and not in the region where you receive a residence permit.

- Freely apply for a job without restrictions by region.

Another advantage of a residence permit is that foreigners, along with citizens of the Russian Federation, have the right to receive a loan from a bank. The same rules for applying for a loan will apply to them as for citizens of the Russian Federation. However, banks are reluctant to provide regular loans to foreigners, but it will be quite possible to get a mortgage loan. In this case, the purchased housing remains pledged to the bank until the loan is repaid, so credit institutions are willing to accept such transactions.

Important! A residence permit (RP) is a document that allows foreign citizens and stateless persons to work and live in the Russian Federation for five years.

The main differences between residents and non-residents

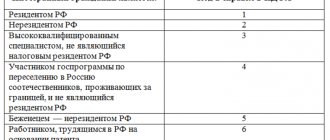

For individuals and legal entities recognized as residents, the tax rate is 13% (for individuals) and 20% (for legal entities). Non-residents pay tax at a rate of 30%. For some categories it may be reduced:

- 13% of personal income tax is for persons with the status of refugees, migrants, highly qualified specialists, as well as for crew members of sea vessels, workers who have issued a labor patent;

- 15% on income received from investment activities.

The main differences are as follows:

- different bet sizes;

- list of objects subject to taxation;

- different procedures for determining the tax base;

- the difference in the possibilities for providing deductions and calculating taxes.

Resident status obliges you to declare, and therefore pay, all types of income, while a non-resident pays taxes only on the income he received in the country.

How to apply for a temporary residence permit in Russia for a citizen of Tajikistan in 2021

The cost of living for the 3rd quarter of 2015 was established by the Government of the Moscow Region No. 1131/45 dated November 30, 2015 and for the working population is 11,990 rubles.

The exceptions are highly qualified specialists, refugees, foreigners who have been granted temporary asylum, migrants who have become participants in the resettlement program for compatriots or who are native speakers of the Russian language and citizens of the Republic of Belarus who may not receive a residence permit.

If an individual was abroad for other purposes and during this period underwent training (treatment) there for up to six months, the days of training (treatment) during the period of stay in the Russian Federation are not included. In particular, similar explanations regarding short-term training can be found in Letter of the Ministry of Finance of Russia dated September 26, 2012 No. 03-04-05/6-1128. That is, if as of December 31, 2021, an employee was recognized as a non-resident, and in January 2018 became a resident, the amount of personal income tax withheld in 2021 is not recalculated.

How to become a tax resident with a residence permit?

The conditions for recognizing an individual as a tax resident are specified in paragraph 2 of Article No. 207 of the Tax Code of Russia. Obtaining a residence permit does not automatically change the status from non-resident to tax resident. In order to obtain a certificate of receipt of this status, you need to contact the appropriate department at the place of registration or registration.

In order to have the necessary documents, you need to submit an application to the Interregional Inspectorate of the Federal Tax Service of the Data Center (centralized data processing) of the Russian Federation.

What status does a residence permit for a resident or non-resident give, how to hire a foreigner

Working abroad legally for foreign citizens on the territory of the Russian Federation is associated with paying taxes and determining the tax status of an individual coming to work in the country. According to clause 2 of Article 207 of the Tax Code of the Russian Federation:

- if you are on Russian territory for less than 183 days, you have tax non-resident status;

- if your stay is longer than 183 days, you become a tax resident.

The period of stay on the territory of the Russian Federation is not violated if you leave the country for a short period of time (no more than 6 months) for treatment or training.

The income of all foreign citizens who are non-residents, according to paragraph 3 of Article 224 of the Tax Code, is taxed at 30%. This tax rate is established in relation to any type of income received by non-resident persons, except for income from equity participation in the work of Russian organizations, to which a rate of 15% is applied.

Non-residents also do not have the right to standard tax deductions provided for in Chapter 23 of the Tax Code of the Russian Federation.

Starting from the 183rd day of official stay in the country, a foreign citizen becomes a resident and pays a tax rate of 13%. He is given the right to all those tax deductions that are provided for by the 23rd chapter of the Tax Code of the Russian Federation. From the previously withheld amount of taxes in the amount of 30%, 17% are returned back. For an accountant whose company employs such foreign citizens, for example, provides work abroad for Ukrainians, it is very important to correctly determine when the tax status of the employee changes and the foreigner becomes a resident. The countdown of days begins not from the moment of concluding an employment contract with the employer, but from the moment of crossing the border of the Russian state. The date of this crossing is determined by the marks in his passport and migration card, and the counting of days begins from the next day after this (Article 6.1 of the Tax Code of the Russian Federation).

After acquiring resident status, the employee has the right to contact the tax service with an application for the return of the excessively withheld 17% (Clause 1 of Article 231 of the Tax Code of the Russian Federation). In order to receive a standard tax deduction, a foreign citizen must write a corresponding application addressed to the tax agent and attach to it documents confirming his right to benefits (clause 4.1 of Article 218 of the Tax Code). In this case, this will be confirmation of receipt of tax resident status.

How to fill out an application?

The taxpayer submits an application of a certain sample to the authorized tax authority. You can submit it in person or through the Internet service of the Federal Tax Service.

Important! Pay attention to the “code” column. When applying in person, you must enter four zeros (0000), if you are sending an application by mail, tax authority code 9965.

The application must be filled out on a computer or manually (in black ink). All fields to be filled out must be written in clear, legible handwriting, without corrections or erasures.

To obtain resident status with a residence permit, the following documents are provided:

- copies of civil passport pages. It must be accompanied by a notarized translation;

- documents that can confirm that the individual was in the country during the period for which he wants to receive the document. A residence permit can serve as such a document; in addition, you can provide a foreign passport with marks of entry into the territory of the Russian Federation;

- certificates confirming income (copy of work book/contract, bank or accounting statement, etc.);

- rights to own real estate, payment of dividends, cash or payment checks, etc.

The application has the following form:

When submitting an application to an authorized person, it may be necessary to certify with the signature and seal of the tax authorities the form that is accepted in a foreign country. In this case, this form is adjusted to the above package of documents.

Tax status (resident/non-resident) if you have a temporary residence permit

A citizen of another state over 18 years of age who permanently resides in the territory of their country can apply to the Russian mission. At the same time, he must submit all documents, write an application and justify the reasons for moving to the country. Some also need to attach certificates confirming passing exams in the Russian language, history and law. After this, the migrant cannot yet call himself a resident of the Russian Federation, because did not live in it for a sufficient period of time. The NC formulation raises more questions than it provides at least one clear answer to the most important question - which category to classify oneself in, and for this you need to understand the procedure for determining status. In addition, the Tax Code of the Russian Federation has approved a list of income for taxation. Art. 209 of the Tax Code regulates various lists of taxable income depending on the residence status of a citizen.

During the tax period, the 12-month period is determined on the relevant date of receipt of income. That is, an employee’s tax status may change during the year. Traveling outside of Russia is only relevant for calculating the number of days of stay in Russia and does not interrupt the flow of the 12-month period.

A residence permit is given after a person from another state has spent more than a year in the country with a temporary residence permit.

Ivan’s salary before taxes is 20 thousand rubles a month, he is not married and has no children, so he will not have any problems. The goals of creating this site are: increasing the legal literacy of everyone and providing a new type of legal assistance - via the Internet.

At the same time, non-residents of the Russian Federation do not have such a right; all accounts opened by them are managed by one or more authorized banks. The same rule applies to the transfer of foreign currency. Money can be transferred from an account to an account opened exclusively with an authorized bank. Agreement between the Government of the Russian Federation and the Government of Ukraine “On the avoidance of double taxation of income and property and the prevention of tax evasion” dated 02/08/1995 (Article 4).

The main criterion for establishing residency status is the period of stay of a person on the territory of the Russian Federation. A person is considered a resident if during the year he stayed in the customs territory of the Russian Federation for at least 183 calendar days.

In such cases, even after a person’s stay in Russia for less than 1 year, he can immediately contact the departments of the Ministry of Internal Affairs to obtain a residence permit.

Where and how to obtain a document confirming the status of a resident of the Russian Federation?

The applicant can indicate the most convenient way to receive a document confirming receipt of resident status under a residence permit: in person, at the specified postal address, or by email.

One of the main goals of obtaining this status is to avoid double taxation. Documents are issued for 1 year, the one indicated in the application, but you can request data for previous years.

Important! If you need several copies of a document, please indicate the required number in the letter attached to your application.

The time period and procedure for considering the application are regulated by the Order. Confirmation of the status “tax resident of the Russian Federation” is issued no later than forty days after submitting the documents. In the case of a negative decision, when the resident status is not confirmed, the applicant receives a written notification indicating the reason for the negative decision.

For help and legal advice, you can contact the Legal Agency https://migron.ru/. Phone: +7 495 118-33-74.

Get a free consultation with a migration lawyer. Write your question in the form, and a migration law specialist will call you back and advise you.

RVP is a resident of the bank

If a foreign citizen arrives in Russia on a visa-free basis (for example, from the territory of Ukraine), then from this year, in order to obtain employment opportunities in our country, he must obtain a patent (Clause 1, Article 2 of Law No. 115-FZ). Please note: citizens of Belarus, Kazakhstan and Armenia do not need to obtain a patent to work in Russia (Clause 1, Article 97 of the Treaty on the Eurasian Economic Union of May 29, 2014). A Russian or a citizen of another country who already has a permanent or temporary residence permit can also apply to the relevant authorities with a request to issue a temporary residence permit to his relative. Provided that the applicant is the legal guardian or parent of a foreign citizen who requires permission.

In order to receive the desired document, applicants should provide to the Main Department of Migration Affairs of the Ministry of Internal Affairs certificates confirming the grounds for issuing a residence permit, an extract from a medical record about the state of health, a passport and its certified translation, confirmation of the source of income, documents for the housing in which it is registered, a receipt of payment duties, photographs.

To calculate wages and other payments, the employer needs to have information regarding the employee’s residency status.