General requirements

Not only the Tax Code of the Russian Federation, but also some legislative acts regulate the procedure for dealing with reserves, and since 2021, significant changes have been made to this process. So, doubtful debt for each debtor is identified by deducting from it your accounts payable to him. The limit value subject to reserve based on the results of the last reporting period is calculated and taken as a larger figure from 10 percent of the proceeds in the current period or based on the results of the previous year.

How to create a reserve in accounting

Doubtful debts are reserved based on the judgment that it acts as an estimate and it, in turn, takes into account deviations in the valuation of assets, receivables and other existing liabilities. It is with the help of this kind of reserves that it is possible to correct accounting statements in the interests of correctly reflecting the state of affairs in the company at the reporting date.

Taking into account accounting regulations, the company is obliged to reserve certain funds in the event that a receivable debt is considered doubtful. As a conclusion, we can say with confidence that the process of creating reserves is an obligation, but not a right, of all companies of any legal form. When calculating the amount to reserve, take into account absolutely all counterparties, both those who participated in the advance and those who act as the borrower.

It is important to know that reserves should be created after an inventory of calculations. The law does not provide for periods for the formation of reserves, so companies have the right to set it in their own way, but you should not do this less often than you provide reporting to users for review. There may be good reasons for not using the reserve and such balance is added to the final financial result at the end of the year when the annual balance sheet is prepared. Accounting in this case affects the debit turnover of 63 accounts and the credit turnover of 91.01. Upon the occurrence of a new inventory, if the debt remains listed as doubtful, you accrue a new reserve for it. Amounts allocated for reservations are considered other company expenses.

Features of reflecting reserves in tax accounting

The provision for doubtful debts in 1C 8.3 is reflected in the interests of two types of accounting, and in tax doubtful debt is recognized as a receivable for the sale of products when it was not repaid on the established dates under the contract between the parties and there is no security or guarantee for it. You should not recognize as such those debts for the supply of products and services from suppliers, including advances and debts of borrowers, as well as payment of penalties and fines. The Ministry of Finance outlined this position in its clarifications.

Payers who advance profit reserves calculate it every month, while everyone else does this procedure quarterly. The amounts for reserves are added to non-operating expenses and it directly depends on how long the debt has been on the company’s balance sheet. It is worth considering:

- half of the debt with a period of formation from 45 to 90 calendar days (inclusive).

- completely with a period of occurrence exceeding 90 calendar days.

At the end of the reporting date, the amount of the calculated reserve should be compared with the remaining previously reserved amount and the conclusion is drawn:

- when the reserve is calculated to be less than its balance on the balance sheet, the resulting margin is attributed to non-operating income;

- the opposite situation of the appearance of a reserve value greater than that taken into account on the company’s balance sheet indicates the addition of the balance to non-operating expenses.

The balance of the reserve value means the difference between the previously accrued reserve and the value calculated by the accountant at the new reporting date.

Reflection of reserves for doubtful debts in 1C: Accounting 8

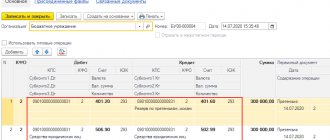

In relation to “1C:Accounting 8”, the accrual of reserves for doubtful debts in tax accounting is reflected by filling in the resources Amount NU Dt and Amount NU Kt accounting records for the debit of account 91.02 and the credit of account 63 (the amount of the reserve is indicated in the resources).

Please note that this calculation of reserves is carried out anew each time. If the new amount of the reserve turns out to be greater than what was previously accrued, then the tax accounting reflects the increase in the reserve, otherwise the restoration of the reserve (reflected by filling in the resources Amount NU Dt and Amount NU Kt accounting records for the debit of account 63 and the credit of account 91.01).

If the organization does not make changes to its accounting policies for the next tax period regarding the formation of reserves for doubtful debts (i.e., continues to form them), then the unused amount of reserves is carried over to the next tax period. In this case, the amount of reserves recognized as non-operating expenses for the corresponding reporting period of the next tax period is determined based on revenue for the same period. If the amount of the newly created reserve is less than the amount of the balance of the unused reserve of the previous period, the difference is subject to inclusion in non-operating income. If the amount of the newly created reserve is greater than the amount of the balance of the reserve of the previous period, the difference must be included in non-operating expenses.

Due to differences in the rules for determining the amount of reserves in accounting and for profit tax purposes, differences may arise in the assessment of reserves in account 63 (respectively, also income and expenses accounted for in account 91). In accordance with PBU 18/02 “Accounting for corporate income tax calculations”, these differences are permanent. The amount of the permanent difference is recorded in the resource Amount PR... of the debit and credit accounts of the posting in which the specified accounts are corresponding. In this case, permanent differences recorded in account 91 are taken into account when calculating income tax for the corresponding period: a permanent tax liability or a permanent tax asset is recognized, i.e., an entry is generated in account 68.04.2 “Calculation of income tax” in correspondence with bill 99.02.3 “Permanent tax liability”.

Note that if the accounting policy parameters indicate the application of PBU 18/02, then permanent differences will also arise in the case when reserves for doubtful debts are created only in accounting or only in tax accounting.

Provision for doubtful debts in 1C 8.3

For your convenience and saving time and labor resources, the developers have made the process of creating reserves automatic and your participation here is reduced to a minimum. In the table below we will look at where to look for such functionality.

| No. | Accounting type | Characteristic |

| 1 | Accounting | The command is placed in the accounting policy in the main menu settings |

| 2 | Tax | In the interest of taxing company profits, please refer to the tax and reporting settings form in the main menu |

According to the regulations, the procedure for creating reserves for doubtful debts is not active. To satisfy accounting tasks in the accounting policy, you must activate the switch for the formation of provisions for doubtful debts. When you need to reserve a certain amount in tax accounting, then in the customizable parameters for taxes and reports in the income tax menu, you will need to activate the switch for the formation of reserves for doubtful debts. When closing a month, when at least one of the listed flags is checked, regulations for calculating reserves for doubtful debts will be added. Even if you do not have any reserves, the form will be generated automatically by the machine, but will not have any movements in the accounting registers.

What is meant by the concept of doubtful debt? When automatically creating reserves, regardless of the type of accounting, the software accepts the outstanding debt on accounts 62.01 and 76.06. An important feature that should not be forgotten is that only ruble contractual relationships with counterparties can be reserved.

Formation of a reserve for doubtful debts in 1C: Enterprise Accounting 3.0

A reserve for doubtful debts is created so that the organization's reporting reflects the true financial result and the volume of real obligations of buyers and customers. It doesn’t matter whether the payment is already overdue or whether there is confidence that the counterparty will violate the agreement in the future.

In general, there is a significant difference between the reserve for doubtful debts in accounting and tax accounting. In particular, reserves are required in accounting. But for tax accounting there is no such requirement.

By the way, pay attention. You need to create a reserve only when you do not have confidence or any additional guarantees that the overdue receivable will be repaid.

Doubtful debts include any debt to the taxpayer if this debt simultaneously satisfies three conditions (clause 1 of Article 266 of the Tax Code of the Russian Federation):

- arose in connection with the sale of goods, performance of work, provision of services;

- not repaid within the terms established by the relevant agreement;

- is not secured by collateral, surety, or bank guarantee.

Form the reserve for doubtful debts in the following order. First, determine the amount of each individual doubtful debt. A reserve will need to be created for each such case. At the same time, determine its size also taking into account the assessment of the debtor’s financial condition and the likelihood of repaying obligations in whole or in part. After all, the amount of the reserve for doubtful debts is an estimated value. It is not necessary to include the entire amount of doubtful debt.

For the purposes of forming reserves for doubtful debts, doubtful debt in the program is considered to be debt not repaid on time, reflected in the debit of accounts 62.01 “Settlements with buyers and customers” and 76.06 “Settlements with other buyers and customers”.

To calculate the period of occurrence of doubtful debts, the following indicators are used:

- The due date for payment of debt by buyers, set in the accounting parameters settings (section Administration - Accounting Parameters - Deadlines for payment by buyers);

- The payment deadline is set in the contract card with the counterparty (Settlements group).

The date from which the period for the occurrence of doubtful debts is calculated in the program is determined as follows. If in the contract:

- a payment deadline has been established, then the debt is considered doubtful if it is not repaid (in whole or in part) after a specified number of days, starting from the date the receivable arose;

- If the payment period has not been established, then a debt is considered doubtful if it is not repaid (in whole or in part) after the number of days specified in the accounting settings, starting from the date the receivable arose.

The rules for calculating the reserve are determined by law. The amount of doubtful debt is included in the reserve depending on the period of its occurrence (clause 4 of Article 266 of the Tax Code of the Russian Federation):

- over 90 calendar days – 100% of the debt amount;

- from 45 to 90 calendar days (inclusive) – 50% of the debt amount;

- up to 45 days – 0% reserve is not created.

In addition, the maximum amount of the reserve cannot exceed (clause 4 of Article 266 of the Tax Code of the Russian Federation):

- based on the results of the tax period - 10% of the revenue for the specified tax period;

- 10 percent - from revenue for the previous tax period (for example, for 2021);

- 10 percent - from revenue for the current reporting period in which the reserve is created (for example, for the 1st quarter of 2021).

based on the results of the reporting periods - the greater of the values:

Revenue for calculating the reserve limit is determined in accordance with Art. 249 of the Tax Code of the Russian Federation excluding VAT (paragraph 5, paragraph 2, clause 1, Article 248 of the Tax Code of the Russian Federation). Non-operating income under subaccount 91.01 “Other income” is not taken into account for calculating the limit.

On the last day of the reporting (tax) period, the amount of the calculated reserve is compared with the amount of the reserve balance:

- if the amount of the reserve is less than the balance of the reserve, then the difference is included in non-operating income;

- if the amount of the reserve is greater than the balance of the reserve, then the difference is included in non-operating expenses.

If a reserve for the next period is not created, then the balance of the reserve is included in non-operating income (clause 7 of Article 250 of the Tax Code of the Russian Federation).

The balance of the reserve is determined as the difference between the amount of the reserve calculated as of the previous reporting date and the amount of bad debts that arose after the previous reporting date.

The accrued reserve for doubtful debts can only be used to cover losses from bad debts. Their list is given in paragraph 2 of Art. 266 Tax Code of the Russian Federation.

Due to differences in the rules for determining the amount of the reserve in accounting and tax accounting, differences in assessment may arise:

- reserves accounted for on account 63

- income and expenses recorded on account 91

- as a result, profits and losses recorded in account 99

In accordance with PBU 18/02, these differences are permanent. Constant differences in account 99.01 are taken into account when calculating income tax as PNO or PNA and are reflected in the entries:

- debit 99.02.3 credit 68.04.2 – PNO accrued

- debit 68.04.2 credit 99.02.3 – PNA accrued

Settings in the program

To set up the program, the first step is to enable the functionality for calculating reserves for doubtful debts using the menu item “Main” - “Accounting Policy”.

By clicking on the hyperlink “Tax and Report Settings”, go to the “Income Tax” settings and check the box “Creation of reserves for doubtful debts”

After setting these parameters, we proceed to setting the terms of settlements with customers.

Setting up settlements with customers

The program allows you to set deadlines in two ways:

1. Specify the lines in the contract with the buyer. The payment term can be specified in any number of days. Also, this method has priority in calculations.

2. Specify the setting for all contracts as a whole. To do this, use the menu item “Administration” - Accounting Settings.

In the parameters, select the hyperlink “Payment period for buyers”.

In the setup form, indicate the required number of days in the “Buyer’s debt payment period” field.

After making the necessary settings in the program, for the calculation of doubtful debts, the “Month Closing” (Operations) processing is used.

This regulatory operation accrues the reserve immediately in both accounting and tax accounting.

The legislation does not establish a method for calculating the reserve for doubtful debts in accounting. The rules are prescribed in the Tax Code and are valid only for tax accounting. Therefore, each business entity must independently determine the method and method for calculating reserves and stipulate this in its accounting policies. The program stipulates that the calculation of reserves for doubtful debts in accounting is carried out according to the rules of tax accounting.

Transaction transactions.

In tax accounting, there is a limitation when calculating reserves. This limitation is determined during the implementation of the regulatory operation “Calculation of shares of write-off of indirect costs”.

Calculation of the period of occurrence of doubtful debt

For that. To clearly understand when a debt becomes doubtful, a number of parameters are provided. So, among them are:

- the payment deadline under the contract is specified in the form of the agreement with the counterparty;

- the moment of debt payment by counterparties is specified in the initial settings and can be accessed through the administration team.

Another nuance that is worth paying your attention to is determining the countdown date for the appearance of doubtful debts and the machine sets it like this:

- when the contract stipulates a clear date for payment, the debt becomes doubtful when it is not at least partially repaid within the specified period after the appearance of the receivable;

- If there are no specific terms for payment in the executed agreement between the parties, the status of doubtful is assigned when, in the customizable accounting policy parameters, the number of days has passed from the appearance of receivables on the balance sheet.

Please note that when making a reservation, the machine does not control the validity of the debt as doubtful in the absence of guarantees for it. But this can be done in another way, in order to control this moment using the form, the payment deadline under the agreement is set in the agreement card with the counterparty. That is, when the company has received a guarantee from the debtor for the debt and you assume that the client is solvent, then it is worth removing this debt from the list of doubtful ones. You have the right to do this by extending the period for payment of the debt by days.

Features of provisions for doubtful debts

Many enterprises have problems associated with dishonesty of counterparties. The latter close debts, allowing for delays, which result in an increase in accounts receivable reflected in the 1st section of the balance sheet.

However, if the counterparty’s debt is in doubt and it cannot be collected (assuming that the counterparty has financial difficulties), then the size of the asset on the balance sheet will be inappropriately inflated. Users will not have a chance to correctly assess the actual situation in the enterprise.

It is for the possibility of changing the book value of assets in accounting that there is such a tool as the reserve for doubtful debts. Its main task is to ensure that the financial statements of companies can correspond to the truth, and internal and external users of the statements are able to fully assess the financial situation of the company.

Regulations on reserves

The machine prompts the user to reserve debts every month. But this may not always be necessary for those companies that report income taxes once a quarter, and is it worth doing the extra work every month? Of course not, it will be enough to reserve finances quarterly. You can refuse such a monthly regulatory option at the time of closing the period by using the skip option command. The regulation itself includes two stages:

- Calculation of doubtful debt. As already mentioned, in 2017 a decision was made if there are different types of obligations with one supplier, the accounts receivable are reduced by the amount of the accounts payable and the machine has such a change in legislation.

- The reserve amount has been calculated and entered into the accounting registers. The amount of the reserve is calculated as a percentage of the amount of debt based on the timing of late payment. In the interests of tax accounting, the amount to be reserved is limited to the amount according to the regulations for calculating shares of write-off of indirect expenses. In this case, the reserve norm for accounting for income tax is determined.

It has already been mentioned that the upper limit of the reserve is limited to 10 percent. This means that when the total reserve for the duration of the debt is greater than the established limit, then the reserve for each debt is considered a non-operating expense multiplied by a coefficient. This indicator is the ratio of the amount of reserves according to the standard to the entire amount of reserves calculated according to the timing of the debt.

Accounting for provisions for doubtful debts

In the 1C:ERP Enterprise Management 2 program, the mechanism for the formation and use of reserves for doubtful debts has been significantly revised. Support is provided for accounting for reserves for doubtful debts in accordance with Order of the Ministry of Finance of Russia dated July 29, 1998 N 34n and Art. 266 Tax Code of the Russian Federation. Implemented:- accounting for permanent and temporary differences when calculating reserves for doubtful debts;

- calculation of reserve amounts for doubtful debts in accounting separately from tax accounting;

- the possibility of forming a reserve for doubtful debts on advances issued to suppliers and loans issued;

- formation of a reserve for doubtful debts for debt accounted for in conventional units and in currency;

- debt write-off using existing reserves.

The ability to account for reserves for doubtful debts becomes available in the 1C:ERP Enterprise Management 2 program when the Master data and administration flag is set - Setting up master data and sections - Regulated accounting - Reflection of transactions - Regulated accounting . The parameters for the formation of reserves for doubtful debts for each organization are set in the accounting policy settings.

Setting the frequency of accrual of reserves for doubtful debts separately for accounting and tax accounting purposes is included in the settings group Create reserves for doubtful debts . The flags that establish the formation of reserves for doubtful debts for accounting and tax purposes have been renamed:

- flag in tax accounting in in tax accounting, with frequency;

- flag in accounting in in accounting, with frequency.

Possible intervals for accrual of reserves for doubtful debts are specified for accounting purposes: Month, Quarter, Year ; for tax accounting purposes: Month, Quarter .

Using the hyperlink Set up the procedure for assessing debt, you go to the workplace Setting up the procedure for assessing debt, in which, for accounting purposes, the size of the reserve is set depending on the number of days of accounting for debt for each type of debt (advances issued, debt of counterparties in rubles, debt of counterparties in foreign currency and cu, loans issued). Availability of settings for the type of debt Debt of counterparties in currency and monetary units. is set by turning on the Master data and administration flag – Master data and sections setup – Enterprise – Currencies – Multiple currencies. The presence of a setting for the type of debt Loans issued is set by turning on the Master data and administration flag – Master data and sections setup – Treasury and mutual settlements – Loan and deposit agreements. For tax accounting purposes, the calculation of the amounts of reserves for doubtful debts is carried out in accordance with Art. 266 Tax Code of the Russian Federation.

In the Type of differences field PBU 18/02 , it is determined what type of differences (permanent or temporary) should be reflected in accounting for different assessments of the provision for doubtful debts for accounting and tax accounting purposes. The presence of the specified field is determined by the presence of the flag Applies PBU 18/02 “Accounting for income tax calculations” in the organization’s accounting policy settings. Automatic transfer of amounts between permanent and temporary differences is not implemented.

In the Month Closing , the routine operation Formation of reserves for doubtful debts has moved to the Formation of expenses group. The specified regulatory operation appears if the formation of reserves for doubtful debts in accounting or tax accounting is noted in the organization’s accounting policy settings. Click the More details hyperlink in the line of the regulatory operation Formation of reserves for doubtful debts to go to the list of documents Accrual and write-off of reserves for doubtful debts.

In the Month Closing the document Accrual and write-off of provisions for doubtful debts will be created automatically and filled with the balances of receivables and counter payables as of the document date in accordance with the settings specified in the organization’s accounting policy card. Information on receivables accounted for in conventional units and in currency, as well as debt on loans issued and advances issued to suppliers, are determined automatically, but the reserve for them is not calculated. The lines corresponding to the specified debt contain the Do not accrue provisions for doubtful debts flag, which can be changed by the user. For tax accounting purposes, the maximum amount of the reserve for doubtful debts, calculated at the end of the tax period, is automatically calculated and recorded in the NU Expense Limit field, in accordance with Art. 266 Tax Code of the Russian Federation.

Information about receivables and counter payables in the document Accrual and write-off of provisions for doubtful debts is filled in the analytics of settlement objects and settlement documents. Accounts receivable data is compiled by business area. Information about counter accounts payable is taken into account when calculating reserves for doubtful debts starting from 01/01/2017. In the documents Accrual and write-off of provisions for doubtful debts with a date earlier than 01/01/2017. Accounts payable bookmarks no.

The amount of the reserve in the document Accrual and write-off of reserves for doubtful debts for each line of the Accounts receivable tabular section is calculated using the formula:

Reserve = (Debt – Collateral – Counter debt) * Valuation coefficient * Limitation coefficient, where:

- Collateral – if there is collateral for the debt, the amount is determined by the user in the Collateral column;

- Debt – the client’s receivables, advance payment or loan issued, established in the Debt column;

- Assessment coefficient is the percentage of debt included in doubtful debt depending on the period of its occurrence. For accounting purposes, it is taken from the organization’s accounting policy settings. This coefficient can be changed by the user in the line of the Accounts Receivable tabular section for a specific debt. For tax accounting purposes, the assessment coefficient is determined in accordance with clause 4 of Art. 266 Tax Code of the Russian Federation;

- Counter debt is a payable to the counterparty indicated in the Accounts Payable tabular section. The adjustment of accounts receivable to accounts payable of the organization is made starting from the first in time of occurrence. (Clause 1 of Article 266 of the Tax Code of the Russian Federation). Counter debt is taken into account only when calculating doubtful debts of clients;

- Limitation coefficient - determined for tax accounting purposes for each line of the Accounts Receivable tabular section, for which the Do not accrue provisions for doubtful debts attribute is not set. Limitation coefficient for a line = NU expense limit * NU reserves / Total in the NU Reserves column. The amount of the NU reserve calculated taking into account the limitation is filled in the NU Reserve (ogr) column.

The Reserve column shows the amount of the reserve in the currency of the settlement object.

When the user checks the corresponding box, the automatically calculated values in the columns Valuation, %, Accounting Reserves, Reserve of the Accounts Receivable tabular section can be adjusted.

Automatic generation and completion of the document Accrual and write-off of provisions for doubtful debts assumes that:

- if the organization’s accounting policy does not use the formation of reserves for doubtful debts for accounting and tax purposes, then the document will not be created;

- one document per month is created for each organization in the information base;

- when a document is automatically created, the following are translated into it from a similar document for the previous month: amounts of accounts receivable with manual adjustments;

- amounts of receivables with debt type Other;

- security amounts;

- attribute Do not accrue provisions for doubtful debts.

- if in the accounting policy of the organization the interval for accrual of reserves for doubtful debts for accounting or tax accounting purposes differs from the Month value, then the document is created, but is not posted in the corresponding accounting;

- if, when generating a debt document with manual adjustments, the amount or terms of the debt change, then:

- if there are lines with the checkbox checked, the document is not posted, the routine operation Formation of reserves for doubtful debts of the Month Closing procedure is considered not completed;

- Manual user participation is expected to correct the document.

- added column Rating, %;

- added Collateral Amount column;

- Implemented indication of debt payment deadlines in report lines.

- if the organization's accounting policy includes the calculation of reserves for doubtful debts for accounting purposes, then in the workplace Setting up the procedure for assessing debt for the type of debt Debt of counterparties in rubles, the size of the reserve is set depending on the number of days of debt accounting in accordance with Art. 266 Tax Code of the Russian Federation. If the organization’s accounting policy specifies other parameters for the formation of reserves for doubtful debts, then it is necessary to adjust the default values filled in;

- if the organization’s accounting policy includes the calculation of reserves for doubtful debts for accounting and tax accounting purposes, then the interval for accrual of reserves for doubtful debts is set to Month and in the Type of differences PBU 18/02 the value Permanent differences is set. If the organization’s accounting policy specifies other parameters for the formation of reserves for doubtful debts, then it is necessary to adjust the default values;

- for the predefined expense item Formation of reserves for doubtful debts, it is set to belong to Other activities and in the Type of expenses field the value Deductions to valuation reserves is set;

- for the predefined income item Closing reserves for doubtful debts, in the Type of income field, set the value Deductions to valuation reserves;

- Provisions for doubtful debts appears in the list Items of assets and liabilities ;

- Regular transaction documents created before updating the information base with the transaction type Formation of reserves for doubtful debts are not changed. If, after updating the information base, the routine operations of the Month Closing procedure are performed again, then the execution of these documents is automatically canceled and the documents Accrual and write-off of provisions for doubtful debts are generated, filled out and posted. For the correct formation of initial data in operational accounting registers and accounting registers, the first document in the information base, Accrual and write-off of reserves for doubtful debts, restores all reserves for doubtful debts existing at the time of its formation and re-accrues reserves for doubtful debts.

- such lines are marked with the appropriate flag;

If the 1SPARK Risks service is connected in the 1C:ERP Enterprise Management 2 program, then for each row of the tabular section of the Accounts Receivable document of the Accrual and Write-off of Provisions for Doubtful Debts, indices assessing the reliability of the counterparty are displayed and highlighted in color.

Accounting for the amounts of reserves for doubtful debts by type of accounting is maintained in the accumulation register Reserves for doubtful debts. When posting the document Accrual and write-off of provisions for doubtful debts, the amounts of reserves indicated in it are compared with the amounts of reserves listed in the accounts. If the new estimate of the reserve is greater than the current estimate, then additional reserve accrual occurs. If the new estimate is less than the current estimate, then the reserve is reduced.

Debt is written off from the created reserves for doubtful debts using the document Treasury - Offsetting and debt write-off - Debt write-off for debt of customers and suppliers on advances issued and the document Treasury - Financial instruments - Adjustments of debt on financial instruments for debt on loans issued. The specified documents include the type of write-off of receivables from reserves. When conducting documents, they form transactions and movements in the operational accounting registers for writing off accounts receivable at the expense of the amounts of reserves for doubtful debts.

Movements in operational accounting registers and entries for accounting for operations of the formation and use of reserves for doubtful debts are shown in the table:

In the report Regulated accounting - Accounting and tax accounting - Certificates and calculations - Provisions for doubtful debts , used to analyze the status of accounting for provisions for doubtful debts, the following changes have occurred:

The reflection of transactions for accounting for provisions for doubtful debts in the management balance sheet of organizations has been implemented. For this purpose, the list of Financial results and controlling – Management balance sheet – Items of assets and liabilities includes a predefined element Provisions for doubtful debts with the item type Passive. Operations for the formation and use of reserves for doubtful debts are taken into account in the accumulation register of Assets and Liabilities with reference to this predefined item. For the purposes of forming a management balance sheet and accounting according to IFRS, the resource SumAdr of the accumulation register of Provisions for doubtful debts is used. In the SumUpr resource, the amount of the provision for doubtful debts is taken into account in the management accounting currency. In the routine operation Formation of reserves for doubtful debts of the Month Closing procedure, the resource SumControl is revalued according to the data of the resource Sum (the amount of the reserve in the currency of the settlement object) and the Currency dimensions.

When updating the infobase: