Taking inventory at the end of the year is the responsibility of all organizations. The inventory must be carried out according to strictly defined rules, otherwise the results will be considered invalid and the company risks receiving a fine for a gross violation of accounting rules. At the same time, small companies often have questions about the procedure for organizing this event. Let us examine in more detail the main issues of the procedure for conducting the annual inventory for 2021 in 2021, including taking into account the coronavirus.

How to form an inventory commission

According to the Methodological Instructions for Inventory (approved by Order of the Ministry of Finance dated June 13, 1995 No. 49, hereinafter we will simply call them Instructions), it should be carried out by an inventory commission .

These Instructions impose conditions :

- number of members – at least 3 people ;

- financially cannot participate in the commission .

Accordingly, organizations with a small number of employees have a question: what to do if it is impossible to form an inventory commission from the existing employees - as required by the Directions? For example, the company has only 5 employees, of which three are financially responsible.

Let us immediately note that such circumstances are not a reason not to carry out an inventory. In clause 38 of PBU 4/99 “Accounting statements of an organization” and clause 26, clause 27 of the Regulations on accounting and financial reporting, such exceptions are not provided .

There is only one way out in such circumstances - to involve outside . For example, clause 2.3 of the Guidelines allows for the involvement of employees of independent audit companies in the inventory.

If an already appointed member of the inventory commission does not show up for the inventory (for example, he got sick), there are 2 options for getting out of the situation:

- Pause inventory.

- Appoint a replacement for the absent person by a separate order from management.

We do not recommend conducting an inventory with incomplete commission . If the inspectors subsequently discover that one of the participants physically unable to be present during the recount (for example, the documents contain his sick leave or a business trip report), the inventory will be considered formal , and its results will be invalid.

This is a gross violation of accounting rules. It is punishable under Art. 15.11 of the Code of Administrative Offenses of the Russian Federation with a fine of 5,000 - 10,000 rubles for violation imposed on company officials. If the violation occurs repeatedly, the fine is doubled , and officials responsible for accounting in the organization may be disqualified for up to 2 years .

Deadline for taking inventory in bankruptcy proceedings

The Law “On Insolvency (Bankruptcy)” dated October 26, 2002, No. 127-FZ, sets a deadline for implementing the procedure for inventorying the property of a bankrupt enterprise. Responsibility for organizing the process of recalculating the organization's assets rests with the bankruptcy trustee. The period for conducting an inventory in bankruptcy proceedings cannot exceed 3 months.

The only way to extend the duration of inventory activities is to justify the need for such a step in court. In Art. 139 of Law No. 127-FZ states that a month after the assessment of the property assets of a bankrupt enterprise and assessment of their value, the sale of assets begins.

How to suspend activities while taking inventory

A company with a small staff may have a large amount of inventory or a large product range. In addition, small and medium-sized businesses have every buyer or client “on their account.” Therefore, neither the owners nor the management want to close, for example, a store or a catering outlet for several days (especially in the days before and after the New Year).

How to fulfill the condition of the Instructions on the suspension of the movement of material assets during the inventory?

inventory plan before the event begins .

EXAMPLE

If the company has a separate store (shops) and a warehouse, you can recalculate the warehouse on one date, allowing the store to work as usual (make the appropriate delivery of goods from the warehouse in advance), and count the store on the next date, choosing the most suitable time for this.

In practice, the recount of a retail outlet is often scheduled outside of its normal operating hours or in such a way that the overlap between inventory time and operating hours is small . As a rule, when recalculating a point, you can do it in less time than when recalculating a warehouse, so some temporary shift can be organized.

In this case, the company conducting the recalculation should remember the rules for involving employees in overtime work. For example, if a salesperson works a regular shift and then stays to take part in inventory, then this would be overtime .

In a situation where it is impossible to completely stop work during the recalculation, you can apply the rules for the arrival and departure of valuables during inventory. They do this as follows:

- if during the inventory something arrived at the warehouse (for example, a car with goods arrived), then it is permissible for the financially responsible person to carry out acceptance in the presence of members of the commission. In this case, the receipt is recorded in a separate document - the inventory “Inventory assets received during inventory”. When comparing balances at the beginning of the inventory according to documents with actual balances of inventory items for this separate inventory, they are not taken into account ;

- if during the inventory you need to ship something (for example, an order to a buyer placed before the start of the recount), for such an operation you must obtain written permission from the manager and chief accountant. The release of goods and materials should also be carried out by the mat. responsible persons in the presence of members of the commission. For inventory items disposed of in this way, there is also a separate inventory “Inventory items released during inventory counting.” Registration of disposal of mat. by the responsible person in the presence of the commission in this case is equivalent to a recount . That is, the results of inventory items released during the inventory can participate in summing up the inventory.

EXAMPLE

If product A at the time of shipment had not yet been counted by the commission, 5 pieces were released according to the inventory, 10 pieces were added to the inventory list after counting, the total balance according to the documents was 15 pieces, then there is neither a shortage nor a surplus for product A.

If during the inventory there are internal movements (for example, goods from an already counted own warehouse arrived at the store while the inventory is being taken there), this needs to be documented in the same way - with a separate inventory for the receipt of goods and materials during the inventory. To ensure that inventory results (especially with internal movements) do not contain errors , the accountant needs in advance correct separate accounting for storage locations of inventory items.

Inventory: answering organizational questions

Is it necessary to conduct an annual inventory of a company's assets and liabilities?

Yes, conducting an annual inventory is a mandatory procedure for all enterprises. Its implementation before drawing up annual financial statements is required by Part 1 of Art. 10 of the Accounting Law

and

pp.

5 and

7

І Regulations No. 879 *.

* Regulations on the inventory of assets and liabilities, approved by Order of the Ministry of Finance dated September 2, 2014 No. 879

.

What regulatory documents should be followed when conducting an annual inventory and recording its results?

The most important document that enterprises must follow, regardless of their legal form and form of ownership, is Regulation No. 879 .

In addition, special inventory documents are used, in particular, for inventory:

— oil and petroleum products — Instruction No. 281

;

— ethyl alcohol — Instruction No. 264

;

— assets and liabilities of agricultural enterprises — ( Recommendation Method No. 37 )

etc.

Which objects are subject to annual inventory and within what time frame?

The annual inventory covers all types of assets and liabilities of the enterprise ( clause 6

and

7 sec.

I Regulations No. 879 ).

It is carried out annually before the preparation of annual financial statements .

The timing of the inventory is established in paragraph 10 of section. I Regulations No. 879

, which recommends that it be carried out annually

before the balance sheet date (i.e. December 31) .

But December 31st is the cut-off date for inventory to be completed. But the period of its implementation depends on the type of assets and liabilities being inventoried (see table). Deadlines for annual inventory

| № p/p | Type of assets and liabilities | When to take inventory |

| 1 | Non-current assets* (except for unfinished capital investments, fixed assets, which at the time of inventory will be located outside the enterprise) | During the period 3 months before the balance date |

| Inventories (except for work in progress and semi-finished products, other materials that will be located outside the enterprise at the time of inventory) | ||

| Current biological assets | ||

| Accounts receivable and payable | ||

| Expenses and income of future periods | ||

| Liabilities (except for unused provisions, settlements with the budget and contributions to compulsory state social insurance) | ||

| * When conducting an inventory, you must take into account the following requirements of clause 10 of section. I Regulations No. 879 : - land plots, buildings, structures and other real estate objects can be inventoried once every 3 years; - tools, instruments, inventory (furniture) can be inventoried annually in the amount of at least 30% of all specified objects with mandatory coverage of all these objects within 3 years; — library collections, by decision of the director, can be inventoried during the year according to the schedule established by him. If there is a volume of library collections from 100 to 500 thousand items, the inventory can be carried out for 5 years, covering at least 20% of items annually, and more than 500 thousand items - for 10 years, covering at least 10% of items annually; — precious metals and precious stones , which are contained in fixtures, equipment and other products, are inventoried simultaneously with the inventory of these assets. | ||

| 2 | Unfinished capital investments | Within 2 months before the balance date |

| WIP and semi-finished products | ||

| Financial investments | ||

| Cash | ||

| Targeted financing funds | ||

| Obligations regarding unused provisions, settlements with the budget and contributions to compulsory state social insurance | ||

| 3 | OS objects, in particular cars, sea and river vessels that will go on long voyages | Before temporary departure from the enterprise |

| Other material assets that will be located outside the enterprise at the inventory date | ||

| Note (!): During the inventory check: - | ||

Specific dates for the start/finish of inventory (within the time limits from Regulation No. 879

), its duration, as well as the objects subject to inventory, are established by the manager in

the order for the inventory .

Moreover, it is interesting: the inventory of specific objects begins after the date for which it is scheduled . For example, according to the order of the manager, the inventory is carried out as of November 30, 2019. This means that the inventory itself will take place in December (for example, from December 2 to December 16, 2021). In this case, inventory records are filled out as of the end of the day on November 30.

The exception is cases of inventory of fixed assets and materiel, which at the inventory date will be located outside the enterprise. They are inventoried until they are temporarily removed from the territory of the enterprise.

Is it necessary for a small enterprise to approve working inventory commissions to carry out an inventory? Or is it enough that we have created permanent inventory commissions?

As a rule, working inventory commissions are created at large enterprises. The reason is simple: a large enterprise requires a large number of inventory items and one commission is simply not able to cope with such a volume of work. Therefore, at such enterprises, the inventory commission primarily performs organizational, regulatory and control functions listed in clause 2.5 of section. II Regulations No. 879

(Wed. 025069200).

In turn, working inventory commissions are engaged in inventory of property directly at storage and production sites.

At enterprises with a small amount of inventory work, a permanent commission organizes and conducts an inventory of assets independently .

Do the working inventory commissions include MOLs?

Restrictions in this regard are established in clause 2.4 of section. II Regulations No. 879

. It stipulates that the MOL cannot be a member of the commission to inspect assets held in its custody, since it is the person being inspected.

It turns out that it is impossible to include the MOL in the commission that will conduct an inventory of the property entrusted to it .

At the same time, in our opinion, nothing prevents the MOL from taking part in the inventory as part of another working commission, which will recalculate the assets managed by other MOLs.

The company employs only one person - the director. Can the inventory commission consist of one person?

In such a situation, the Ministry of Finance offers two options for action (see letter of the Ministry of Finance dated May 27, 2014 No. 31-08410-07-29/12918

):

— approve the composition of the inventory commission of one person or

— include in the commission specialists hired under a civil contract.

Of course, at first glance, the option of conducting an inventory by a commission of one employee is the simplest, and therefore optimal for such a small enterprise. But not everything is so simple, because in this case you will unwittingly violate the provisions of clause 2.4 of section. II Regulations No. 879

.

Let us remind you: it prohibits the inclusion in the commission of those employees who are in charge of the assets for which the inventory is being carried out .

And we have exactly this situation: the company has only one employee, who is financially responsible for all assets. In order not to violate the requirements of Regulation No. 879

, we would still recommend focusing on the second option: including in the commission a specialist invited to carry out an inventory on the basis of a civil contract.

One of the members of the inventory commission is absent for a valid reason. Is it possible to “recount” assets and liabilities without it?

Clause 1 section. II Regulations No. 879

for such cases, it provides the following: the inventory is carried out

by the full composition of the inventory commission.

It turns out that, whatever the reason for the absence of one or more members of the inventory commission, it is impossible to carry out an inventory with an “understaffed” staff. But there is a way out: a member of the commission who is absent due to illness or in connection with a business trip must be replaced (see letter of the Ministry of Finance dated December 15, 2003 No. 31-04200-30-23/19

). To do this, it is necessary to issue an order from the manager, by which the absent employee is excluded from the commission, and another employee is added to the commission in his place.

Another option is to suspend or reschedule the start of the inventory (of course, this option is suitable in case of a short absence of a commission member).

During the inventory, the enterprise employee responsible for the storage and use of assets fell ill (was on vacation). Is it possible to conduct an inventory of the assets entrusted to him without him?

All the same paragraph 1 section. II Regulations No. 879

requires an inventory to be carried out

in the presence of the MOL . Therefore, it will not be possible to take inventory of assets in the absence of the MOL and not violate Regulation No. 879

.

So what should we do? And it all depends on whether someone fulfills the duties of a temporarily absent MOL or not. If the responsibilities of the MOL were transferred to another employee, then an agreement on financial responsibility should be concluded with him and an inventory of valuables should be carried out when changing the MOL. In this case, the inventory of assets can be carried out in the presence of not the main MOL, but under the “supervision” of its temporary replacement.

If you do not appoint an acting MOL, then there is nothing left but to suspend the inventory (if it has already begun) or postpone the start of its implementation.

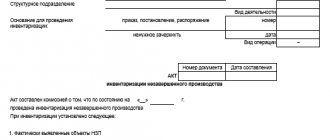

What documents are used to document the results of the inventory?

During the inventory, the working inventory commission draws up ( clause 15 of section II of Regulation No. 879

):

— inventory records , which record the presence, condition and valuation of the enterprise’s assets and assets owned by other enterprises and recorded off the balance sheet;

— inventory acts , which show the presence of monetary documents, strict reporting document forms, financial investments, cash, as well as the completeness of the reflection of funds in bank accounts (registration accounts), receivables and payables, liabilities, targeted financing funds, expenses and income future periods, provisions (reserves) created in accordance with the requirements of P(S)BU, IFRS

and other acts of legislation.

Upon completion of the inventory, the completed inventory lists (inventory acts) are transferred by the commission to the accounting department. Here, all calculations carried out by the working inventory commission in the inventory lists are checked and in case of discrepancies (surpluses or shortages) between the data of the inventory lists (inventory acts) and the accounting data, comparative statements of assets and liabilities ( clause 20 of section II of Regulation No. 879

).

And finally, the inventory commission formalizes the inventory results with an inventory protocol . It cites ( clause 1, section IV of Regulation No. 879

): inventory results, conclusions about identified discrepancies between the actual availability of assets and liabilities and accounting data, the causes of shortages, losses and surpluses, proposals for offsetting shortages and surpluses by re-grading, proposals for writing off shortages within the limits of natural loss norms, as well as excess shortages and losses from damage to valuables, indicating the reasons and measures taken to prevent such losses and shortages, and other essential information.

The protocol of the inventory commission, together with other “inventory” documents, is submitted to the manager for approval.

The manager approves the protocol within 5 working days after completing the inventory.

Based on the approved protocol, the inventory results are reflected in the accounting and financial statements of the period in which it was completed.

Part of the company's assets is located in the territory of the anti-terrorist operation (ATO). How to take inventory of property to which we do not have access?

Let us remind you (!): Section 8. I Regulations No. 879

establishes

simplified inventory requirements for enterprises: located in temporarily occupied territory;

located in the territory of the ATO; structural units (separate property) of which are located in temporarily occupied territory or in the territory of the ATO. For them, the legislator has moved the deadlines for carrying out mandatory inventory, including before the preparation of annual financial statements, until the moment when it becomes possible to ensure safe and unhindered access of authorized persons to assets, primary documents and accounting registers , which reflect the liabilities and equity capital of these enterprises. And only after gaining access to property, enterprises are obliged to:

— take inventory as of the 1st day of the month following the month in which obstacles to access to assets, primary records and accounting registers disappeared;

— reflect the results of the inventory in the accounting of the corresponding reporting period.

A document confirming limited access to assets for the purpose of inventory, and therefore the right to apply simplified inventory rules, is a certificate of the Ukrainian Chamber of Commerce and Industry.

See letters of the SFSU

dated February 14, 2018 No. 611/6/99-99-15-02-02-15/IPK

and

dated June 23, 2016 No. 13823/6/99-99-15-02-02- 15

.

It turns out that enterprises whose property is located in the anti-terrorist operation (JFO) zone are not exempt from the inventory of objects located there, but they can carry it out outside the time limits established by Regulation No. 879

timing, and when this will become possible.

Assets for which an inventory has not been carried out are shown in the financial statements according to accounting data **. Moreover, the fact that the information in the financial statements is provided without conducting an inventory due to lack of access to assets must be indicated in the notes to the financial statements (see letter of the Ministry of Finance dated June 29, 2016 No. 31-11410-07-10/18732

).

** Since due to the armed conflict there was a decrease in the usefulness of the enterprise’s assets, they are shown in accounting taking into account the provisions of

P(S)BU 28

.

It is impossible to write off “occupied” assets without inventory. That is, they will have to be kept on the balance sheet until the moment when the company receives safe and unhindered access to them and can assess their physical condition.

See

letters from the SFSU dated 02/17/2017 No. 3339/6/99-99-15-02-02-15

and

dated 02/10/2017 No. 2714/6/99-99-15-03-02-15

.

Is the presence of financially responsible persons required during inventory?

As a general rule, the financially responsible person must be present during the inventory. But only entrusted to him . Yes, mat. responsible employees of a separate warehouse must be present during the recount by the warehouse commission, but are not required to be, for example, in a store where store employees are responsible for the safety of inventory items.

What if checkmate? the responsible person cannot be present during the recount due to objective reasons? Is it possible to carry out an inventory?

It is possible , but subject to several mandatory steps :

1. Mat. The responsible employee should be given a written invitation to be present during the recount of the valuables entrusted to him. To which the employee must also give a written response , in which he sets out the reasons why he cannot be included in the inventory.

If this requirement cannot be met (for example, the employee is absent for unknown reasons), an act of absence is drawn up.

2. Based on the employee’s response or absence certificate, the manager needs to issue an order to conduct a recount in the absence of the financially responsible person.

3. In all inventory documents, in places where an absent employee should be noted, entries are made that he is absent and for what reason. Each such record is certified by the signatures of all members of the commission.

4. Allowed instead of swearing. responsible person to attract independent witnesses to observe the recount. If necessary (for example, when the material person in charge challenges the inventory results), witnesses can confirm that the process was carried out without violations on the part of the commission.

Documenting

Information about the actual availability of property and the reality of recorded financial obligations is recorded in inventory records or inventory reports. These documents are drawn up in at least two copies. Data from the results of inventories carried out in the reporting year are summarized in the statement of results identified by the inventory. Inventory documents are presented in the table.

Table

.

INVENTORY DOCUMENTS

| Title of the document | Form number | Document that approves the form |

| Inventory list of fixed assets | INV-1 | Resolution of the State Statistics Committee of Russia dated August 18, 1998 No. 88 |

| Inventory label | INV-2 | |

| Inventory list of inventory items | INV-3 | |

| Inventory report of goods shipped | INV-4 | |

| Inventory list of inventory items accepted (handed over) for safekeeping | INV-5 | |

| Act of inventory of materials and goods in transit | INV-6 | |

| Inventory report of fixed assets unfinished by repair | INV-10 | |

| Act of inventory of future expenses | INV-11 | |

| Cash inventory report | INV-15 | |

| Inventory list of securities and forms of strict reporting documents | INV-16 | |

| Act of inventory of settlements with buyers, suppliers and other debtors and creditors | INV-17 | |

| Comparison statement of the results of inventory of fixed assets | INV-18 | |

| Comparison sheet of inventory inventory results | INV-19 | |

| Statement of results identified by inventory | INV-26 | Resolution of the State Statistics Committee of Russia dated March 27, 2000 No. 26 |

What are the ways to carry out inventory starting in 2021?

Until recently, in practice there were only 2 ways of conducting inventory: natural and documentary.

Let us remind you:

- Natural inventory is the direct observation of inventory objects, their recalculation, measurement, weighing, etc., as well as the establishment of their actual quantity.

- Documentary inventory is a revision of documentation in order to document the presence/absence of inventory items.

With the advent of the COVID-19 pandemic in our lives in 2021, another method of inventory has appeared - remote. That is, with the help of audio and video recording and communication means.

Of course, such an inventory cannot be completely . Someone must be, for example, in a warehouse or at a point, carrying out a physical count. In this case, it is permissible for other participants (for example, members of the inventory commission) to observe the process remotely . Thus, the restrictions necessary to counter the spread of the virus are implemented.

Inventory using audio and video recording and communications means is permissible temporarily . For now - between the end of 2020 and the beginning of 2021.

It is important to remember that any inventory method used must first be prescribed in accounting policies . Therefore, having decided to carry out an inventory taking into account current sanitary and epidemiological requirements, you must first include this method in the accounting policy, and only then issue an order to conduct an inventory.

Read also

25.07.2019

When to take inventory?

The specific timing of the inventory before drawing up annual reporting depends on the category of the controlled object. But in general, uniform recommendations should be followed, that is, verification activities should be completed before reporting begins at the end of the year.

Consider special recommendations when conducting an inventory.

- Fixed assets should be inventoried at least once every three calendar years. A longer period is established for the library collection - at least once every five years.

- The remaining property, monetary assets and liabilities should be inventoried at least once a year.

- For objects for which the inventory was carried out between October and December of the reporting year, the procedure may not be carried out.

- For companies located in the Far North, it is allowed to carry out control activities during the period of least balance.

It is possible to provide for additional exceptions and rules for conducting control activities. The main thing is that exceptional rules do not contradict current legislation and are documented. For example, they are reflected in the company's accounting policies.

Reflection of inventory results in accounting and reporting

The results of the annual inventory must be included in the annual financial statements, which means they must be reflected in the accounting records no later than December 31 of the reporting period.

The basis for recording entries in accounting are inventory materials and decisions made by the head of the organization. In this case, the final amounts of surplus and shortage must be entered into the matching statements, which are formed as the difference between the initial amount (number) of disagreements and the amounts of corrected errors and misgrading. If the amounts of discrepancies that arose due to errors in accounting are corrected during the inventory, then their adjusted values are subject to reflection in the reconciliation sheet in the column “Adjusted due to clarification of accounting entries.”

Based on the results of the inventory, all measures must be taken to correct and supplement accounting records in such a way as to obtain affirmative answers on the following points:

— assets and liabilities exist and belong to the organization at the inventory date;

— there are no unaccounted assets, liabilities, transactions or business events;

— the value of assets and liabilities, the amount of transactions and events of economic activity are documented;

— income and expenses are reasonable and relate to the relevant period.

Identified errors must be corrected, receivables and payables, the statute of limitations for which has expired or which are unrealistic to collect, must be written off, established surpluses must be capitalized, and shortfalls must be collected from financially responsible persons or written off.

Typical errors when reflecting inventory results in accounting and reporting include:

- damaged property that can be used or sold to third parties has not been capitalized;

— the results of the inventory are reflected in the accounting records untimely (in subsequent periods);

— surpluses and shortages are recognized for transactions not reflected in previous periods;

— incorrect accounting entries were made in the presence of a court decision refusing to recover damages from the guilty party. If the court refuses to recover damages from the perpetrators or the latter are not established, then losses from the shortage of property and its damage are written off to the financial results;

— permanent differences are not reflected in the accounting if the employer refuses to collect the amount of damage from the guilty party;

— the offset of homogeneous mutual claims has not been carried out;

— written off receivables are not reflected in off-balance sheet accounts;

- misgrading was incorrectly recognized. When regrading, the shortage can be covered by surpluses of similar material assets. Offsetting surpluses and shortages during regrading is possible if they arose in one audited period, with one financially responsible person and for one name of material assets.

Procedure for summing up inventory

As a rule, in most organizations, inventory is completed with the preparation of inventory lists, acts and collation sheets, which are transferred to the accounting department to reflect the results of the inventory. At the same time, the requirements for summing up the inventory by the inventory commission are not met. Let's define them.

The inventory results must be reviewed at a meeting of the inventory commission, which identifies the reasons for the need to make clarifying entries in accounting and suggests ways to reflect the inventory results in accounting.

When considering the inventory results, the inventory commission establishes :

— reasons for surplus and shortage, including misgrading, as well as errors made in the process of accounting for property and liabilities;

— the presence of financially responsible persons, the causes of damage, the perpetrators and the existence of conditions for the occurrence of financial liability of employees, the exact amount of damage and the amount of damage to be recovered from the perpetrators.

Based on the facts of identified surpluses and shortages, the commission receives detailed explanations from financially responsible persons. If financially responsible persons refuse to give explanations regarding the shortage, a corresponding act is drawn up.

If the shortage did not arise through the fault of the financially responsible persons, the commission draws up a comprehensive explanation of the reasons why the shortage is not attributed to the guilty persons. Moreover, the fact of the absence of the guilty person should be documented, for example, by a decision to suspend the preliminary investigation.

Also, the inventory commission draws up an inventory of objects that are unsuitable for further use and cannot be restored, indicating the time of commissioning and the reasons for unsuitability (damage, complete wear and tear), as well as proposals for sources of write-off of these objects.

As a result of consideration of the results of the inventory, the inventory commission should develop proposals for regulating the identified discrepancies, including the offset of surpluses and shortages as a result of regrading, on possible methods of collecting doubtful receivables or the need to write them off.

At a meeting of the inventory commission, the final inventory act is approved, which records the conclusions, decisions and proposals based on the results of the inspection, and a protocol is drawn up. The final act is submitted to the head of the organization for consideration. It can be supported by generalized inventory results in a form independently developed by the insurer. The results should include indicators of inventories and reconciliation sheets. A breakdown of property and liabilities can be provided only for those objects for which discrepancies have been established.

It is the head of the organization who makes the final decision based on the inventory results, which is formalized by order (instruction, decision). The order to approve the inventory results is the basis for reflecting the relevant decisions in accounting.

How to hold an event: step-by-step instructions

Step 1. Form an inventory commission

The commission may include full-time employees of the enterprise (accountant, lawyer, document specialist, head of the labor protection department, etc.) and representatives of third-party companies (auditor). The law does not establish the number of people on the commission. As a rule, the commission is formed from an odd number of participants in order to eliminate the uncertainty of the voting result. The chairman is appointed by the manager, his deputy or the chief accountant.

The created commission is considered permanent, that is, it is not necessary to recruit it from scratch before each new inspection. If a company has many divisions scattered geographically, then several working commissions are created. In this case, the event starts in all departments simultaneously.

Step 2. Issue an order

The order is issued in free form, but it must list the composition of the commission, indicate the timing and reason for the inspection. In our example, the basis for inventory is reporting at the end of the year. The document details are entered into the control log.

Example of an inventory order

Since 2013, unified templates are no longer required. An organization can develop forms independently, including the mandatory details listed in clause 2 of Art. 9 of the law of December 6, 2011 No. 402-FZ.

Step 3. Fix the balances

Before the procedure, the commission must obtain up-to-date information about asset balances according to accounting data. This work is performed by the accounting department:

- receives receipts from accountables and financially responsible persons;

- pulls up the latest cash and inventory flow reports;

- compiles registers and attaches collected documentation to them.

The chairman of the commission receives the prepared documents, endorses them and stamps the date.

Step 4. Check assets and liabilities

The manager creates the conditions for conducting the audit. For example, inspectors must be provided with measuring instruments and measuring containers. If you have to move heavy objects, you need to hire loaders. During the inventory, the premises with inventory items are sealed and the acceptance and release of valuables is suspended.

The commission recounts the property, assigns an inventory number to each object, and draws up an inventory. If some types of property cannot be counted individually, appropriate weighings and measurements are made. Checking the actual presence of valuables is carried out only in the presence of financially responsible persons and all members of the working commission.

The commission establishes the presence of intangible assets and financial liabilities according to documents, and enters the information into inventory acts.

Important! If at least one member of the commission is absent from the inspection, its results may be invalidated. Therefore, the number of signatures in the inventory documentation must correspond to the number of commission members.

Step 5. Compare the data and present the results

The data obtained as a result of the audit is compared with accounting indicators. If discrepancies are found, comparison sheets must be filled out.

The final stage is a meeting following the results of the inventory. Members of the commission summarize the results, analyze the causes of discrepancies and propose ways to eliminate them. The minutes of the meeting and accompanying documents are transferred to the manager, who approves the results of the event in an orderly manner. Inventory documentation goes to the accounting department, and employees put accounting data in order: surpluses come in, shortages are written off.

According to Article 238 of the Labor Code, management may oblige financially responsible persons to compensate for losses if a shortage is discovered. caused to the employer in full.