How the rules for registration at the location of separate divisions have changed

A new division is opening

Let us recall that in accordance with the previous edition of Articles 23, 83 and 84 of the Tax Code of the Russian Federation, several actions were required to be taken to register at the location of any separate unit. Namely: within one month, inform your inspection about the opening of a new unit (form No. S-09-3, approved by order of the Federal Tax Service of the Russian Federation dated April 21, 2009 No. MM-7-6 / [email protected] ). Within the same period, submit to the Federal Tax Service at the location of the new unit an application for registration (form No. 1-2 Accounting, approved by order of the Federal Tax Service of the Russian Federation dated December 1, 2006 No. SAE-3-09 / [email protected] ).

Among other things, the application was required to include documents confirming the creation of the unit. Thanks to the amendments, companies will no longer have to take actions that the tax authorities themselves can perform. Thus, according to the new rules, registration of a company at the location of the branch or representative office must occur without its participation. The organization is only required to make the necessary changes to the Unified State Register of Legal Entities. Let us remind you that according to the Federal Law of 08.08.01 No. 129-FZ on registration, tax authorities must be informed about the creation of a new branch or representative office within three working days (Clause 5, Article 5 of Law No. 129-FZ). After this, the inspectors themselves must register the company at the location of the branch or representative office based on data from the Unified State Register of Legal Entities (clauses 3, 4, article 83, clause 2, article 84 of the Tax Code of the Russian Federation *). Additionally, you do not need to notify your tax office about the opening of a branch or representative office (subclause 3, clause 2, article 23 of the Tax Code of the Russian Federation).

If an organization creates another separate division (not a branch or representative office), the inspectorate with which the company is registered must be informed about this within a month (Clause 2 of Article 23 of the Tax Code of the Russian Federation). Based on this message, tax authorities must register the company at the location of the unit within five working days (clause 4 of article 83, clause 2 of article 84 of the Tax Code of the Russian Federation). In this case, inspectors do not have the right to demand any other documents.

Let us note that the new version of paragraph 1 of Article 83 of the Tax Code of the Russian Federation obliges companies to register for tax purposes at the location of each separate division. Previously, this was not required if the company, for some other reason, was already registered with the inspectorate to which the new division belonged.

Let us mention one more addition. It concerns the case when a company has several separate divisions in one municipality. In such a situation, the organization can register at the location of one of them. The law being commented on clarified that a company must submit a notification of its choice to the inspectorate at the location of its head office (Clause 4 of Article 83 of the Tax Code of the Russian Federation).

The address of the department and other information changes

Until now, changing the address of a separate division meant the emergence of a new problem for an accountant. Since the Tax Code did not stipulate the procedure for “re-registration” of separate divisions, inspectors demanded that the division be first deregistered at the old address and then registered at the new address. And this had to be done even if the unit moved within the territory under the jurisdiction of the same tax office (letter of the Ministry of Finance of Russia dated June 18, 2010 No. 03-02-07/1-282).

Now the procedure will be significantly simplified. If the address of a separate division that is not a branch or representative office changes, it will be sufficient to inform the Federal Tax Service Inspectorate at the location of the company. This must be done within three working days (subclause 3, clause 2, article 23 of the Tax Code of the Russian Federation). Based on this message, tax authorities will make changes to their databases and, if necessary, will register the company at the new location of the unit (clauses 3, 4 of Article 84 of the Tax Code of the Russian Federation). Please note that it is necessary to notify tax authorities not only about a change in the address of a separate division, but also about changes in other information contained in the message about the creation of a division (name of the division, details of the head, contact information, etc.).

Read more: If there is no debt on the bailiffs website

As for changing the address or other information about a branch or representative office, then, as in the case of the creation of such divisions, inspectors will take all the data they need from the Unified State Register of Legal Entities. The company is only required to submit an application to update the information in this state register on time. Additionally, there is no need to report a new branch address or changes in other data in accordance with Article 23 of the Tax Code of the Russian Federation. Based on the information entered into the Unified State Register of Legal Entities, tax authorities will deregister the company at the previous address of the branch and register it with the inspectorate at the new address of this division (clauses 3, 4 of Article 84 of the Tax Code of the Russian Federation).

Separate division is closing

If an organization decides to close a separate division (including a branch or representative office), it will need to be reported to the tax authorities within three working days (subclause 3.1, clause 2, article 23 of the Tax Code of the Russian Federation). This period is counted from the date of the decision to terminate activities through a branch or representative office. And if another separate division is closed, then the period is counted from the day when it actually stopped working. The message is submitted to the inspectorate at the location of the head office. The Tax Code does not require any additional documents to be attached to such a message.

The legislator did not specify when the tax authorities will deregister the company at the location of the former branch or representative office. But this will not happen before the corresponding changes are made to the Unified State Register of Legal Entities, and not before the on-site audit of the company is completed (if the tax authorities decide to conduct one).

The period during which tax authorities must deregister a company at the location of another separate division has not changed. It is 10 working days from the date of receipt of the message about the closure of the unit, but can be extended if the tax authorities organized an on-site audit (clause 5 of Article 84 of the Tax Code of the Russian Federation).

Note that previously the deadline for informing tax authorities about the liquidation of any division was one month (previous wording of subclause 3, clause 2, article 23 of the Tax Code of the Russian Federation). But at the same time, it was also necessary to submit an application to deregister the company at the location of the closed division.

Messages can be sent electronically

Please note there is an important change regarding the reporting of detached units (meaning all reports mentioned in this material). According to the new rules, such information can be transmitted in three ways: by submitting it in person; send by regular mail by registered mail; transmit electronically via telecommunication channels. In the latter case, the document is signed with an electronic digital signature of the person who sent the information or his representative (Clause 7 of Article 23 of the Tax Code of the Russian Federation).

New forms and formats of messages, as well as the procedure for sending them, must be adopted by the Federal Tax Service. Drafts of these documents are posted on the official website of the Federal Tax Service of Russia, however, there is no information about their official approval yet.

*Here and below, new editions of articles of the Tax Code of the Russian Federation are indicated.

Many large companies have separate divisions. In the process of activity, various situations arise when branches, representative offices and other “separate units” change their location. Such a change is subject to state registration and in order to make it, the organization must follow a certain procedure.

The process for making changes depends on the specific type of separate unit. One procedure applies for representative offices and branches, and another for other types of separate divisions. This procedure is regulated by the provisions of federal laws No. 14-FZ of 02/08/1998 “On Limited Liability Companies”, No. 129-FZ of 08/08/2001 “On State Registration of Legal Entities and Individual Entrepreneurs”, the Tax Code of the Russian Federation, as well as by-laws - by order of the Ministry of Finance Russia on the approval of Administrative Regulation No. 169n dated September 30, 2016. Let’s consider how the address of a separate division is changed, and the company’s procedure for doing so.

Changing the address of a separate division - the procedure for calculating income tax

Tax returns continue to be compiled for a separate division on a cumulative basis from the beginning of the year

02/10/2020Russian tax portal

Prepared answer:

Expert of the Legal Consulting Service GARANT

auditor, member of RSA Elena Melnikova

The answer has passed quality control

The separate division changed its address in the middle of the year; the division was not closed. How to correctly calculate income tax for this division?

On this issue we take the following position:

Since in the situation under consideration there was a change in the location of the separate division, and not its closure or liquidation, tax returns continue to be compiled for the separate division on an accrual basis from the beginning of the year.

Justification for the position:

If an organization has separate divisions (hereinafter also referred to as OP), payment of income tax (including advance payments) is carried out in accordance with Art. 288 Tax Code of the Russian Federation.

Based on paragraph 1 of Art. 288 of the Tax Code of the Russian Federation, organizations that have an OP, calculate and pay the amounts of advance payments to the federal budget, as well as the amounts of tax calculated based on the results of the tax period, at their location without distributing the indicated amounts according to the OP.

Payment of advance payments, as well as tax amounts subject to credit to the revenue side of the budgets of the constituent entities of the Russian Federation, is made by Russian organizations at the location of the organization, as well as at the location of each of its OPs based on the share of profit attributable to these OPs, defined as the arithmetic average the share of the average number of employees (labor costs) and the share of the residual value of the depreciable property of this OP, respectively, in the average number of employees (labor costs) and the residual value of the depreciable property, determined in accordance with paragraph 1 of Art. 257 of the Tax Code of the Russian Federation, in general for the organization (clause 2 of Article 288 of the Tax Code of the Russian Federation, see also letters of the Ministry of Finance of Russia dated 01/23/2017 N 03-03-06/1/3007, dated 02/01/2016 N 03-07-11/4411 , dated 05/19/2016 N 03-01-11/28826).

In accordance with paragraph 1 of Art. 289 of the Tax Code of the Russian Federation, taxpayers, regardless of whether they have an obligation to pay tax and (or) advance payments for tax, the specifics of calculation and payment of tax, are required, at the end of each reporting and tax period, to submit the relevant tax documents to the tax authorities at the place of their location and the location of each OP declarations in the manner prescribed by this article.

The organization, which includes the OP, at the end of each reporting and tax period, submits to the tax authorities at its location a tax return for the organization as a whole, with distribution among separate divisions (clause 5 of Article 289 of the Tax Code of the Russian Federation).

Advance payments for income tax, calculated based on the results of the reporting period (first quarter, half-year, nine months of the calendar year), and income tax, calculated based on the results of the tax period, are paid to the budget of the constituent entity of the Russian Federation at the location of the EP no later than 28 calendar days after the end of the corresponding reporting period (for advance payments) and March 28 of the year following the expired tax period (Article 285, paragraph 4 of Article 288, paragraphs 3, 4 of Article 289 of the Tax Code of the Russian Federation).

Thus, at the end of each reporting period, corporate income tax is calculated based on the profit subject to taxation, calculated on an accrual basis from the beginning of the tax period to the end of the reporting period. The procedure for calculating tax does not depend on a change in the location of the organization and a change in the place of registration of the organization with the tax authority (letter of the Ministry of Finance of Russia dated March 15, 2018 N 03-02-07/1/16043).

The form, presentation format and procedure for filling out (hereinafter referred to as the Procedure) the tax return for corporate income tax are established by order of the Federal Tax Service of Russia dated October 19, 2016 N ММВ-7-3/ [email protected]

Paragraph 1 of clause 1.4 of the Procedure states that the organization, which includes OPs, at the end of each reporting and tax period submits to the tax authority at its location a Declaration drawn up for the organization as a whole with the distribution of profits among the OPs in accordance with Art. 289 Tax Code of the Russian Federation. The distribution of profits according to the OP is carried out in Appendix No. 5 to Sheet 02 of the declaration “Calculation of the distribution of advance payments and corporate income tax to the budget of a constituent entity of the Russian Federation by an organization that has separate divisions.”

At the same time, based on clause 4.1.5 of the Procedure, when submitting an income tax return after changing the location of a separate division, OKTMO at the new location of the organization should be indicated.

If the location of a separate division changes, the activities of the organization through the separate division do not cease and tax returns (including updated tax returns for previous reporting and tax periods) are submitted to the tax authority at the new location of this separate division, see letter of the Federal Tax Service of Russia dated November 20, 2015 N SD-4 -3/20373. The same letter states that if the location of a separate division of an organization changes, the tax authority at its previous location transfers documents to the tax authority at the new location of this separate division.

In relation to the situation under consideration, the letter of the Federal Tax Service of Russia dated March 18, 2011 N KE-4-3 / [email protected] explains that since when the location of a separate division changes, the activities of the organization through this separate division do not stop, then, accordingly, tax returns continue compiled for this separate division on an accrual basis from the beginning of the year. Payment of tax to the budget of a constituent entity of the Russian Federation after a change of location must be continued at the location of the separate division at the new address (see also letters of the Federal Tax Service of Russia for Moscow dated August 28, 2012 N 16-15/ [email protected] , Federal Tax Service of Russia dated August 31 .2015 N PA-4-6/15235, Information from the Federal Tax Service of Russia for the Vladimir Region dated September 30, 2015 “When the location of a separate unit changes, the checkpoint does not change”).

Thus, since in the situation under consideration there was a change in the location of the separate division, and not its liquidation, tax returns continue to be compiled for the separate division on an accrual basis from the beginning of the year.

Subscribe Post:

Representative offices and branches

To change the address of a representative office or branch, it is necessary to analyze the organization’s charter. If this document contains information about the address of such a separate division, then changes to the charter will be required. Let us recall that the current legislation does not oblige such information to be indicated in the charter of a legal entity, but practice shows that in many cases information about branches and their addresses is still available in this document. Therefore, changing the address of a separate division in such situations will require a procedure for amending the charter.

Read more: How to get free medicine for cancer patients

To do this, it is necessary to convene an extraordinary meeting of participants, at which a decision must be made to change the document. There are two options here:

Exclusion from the charter of the clause on a separate division;

Entering new information about the location.

The decision of the meeting is approved by the minutes, which, together with an application in form P13001 and with the new edition of the charter, are submitted to the tax office to register the changes.

In a situation where the organization’s charter does not contain information about a branch or representative office, the procedure for making changes is somewhat different. The head of the organization must make an appropriate decision, on the basis of which an application on form P14001 is filled out. The application must be received by the tax office at the place of registration of the organization within three working days from the date of the decision. Let us note that if the charter of an organization or the regulations on a branch provide for a different procedure for making decisions regarding its activities, including decisions on its name, location and other issues, then the procedure specified in these documents must be observed, for example, a general meeting of participants was held.

Please note that currently there is no need for a separate division to additionally notify the tax authorities at its location about the changes being made. Information about this is received by them through departmental exchange.

Accounting in branches and representative offices

A separate division carries out activities in accordance with the goals and objectives of the parent company. Functions, types of activities, level of legal capacity and powers are determined by the parent organization and are enshrined in the regulations on the separate division. Including accounting, accounting is possible in two options.

- Option 1: the division does not have its own balance sheet.

In this case, the branch does not have its own accounting department and current account. All settlements with contractors, including payroll personnel, are carried out by the head office accounting department. In this case, the division has the right to issue, for example, shipping documents, but they will be accepted for accounting in the head accounting department.

- Option 2: the division is on an independent balance sheet.

This option involves creating an accounting service and maintaining records within the department. It has a current account with a credit institution and can carry out settlements with counterparties independently. Data from the financial statements of the division are taken into account in the general summary of the enterprise. A separate division carries out accounting according to the rules of the accounting policy of the parent company.

You will learn how to correctly draw up an accounting policy for your company from our material “How to draw up an organization’s accounting policy (2020)?”

Changing the address of a separate division within one tax office

The legislation clearly states that a change in the address of a legal entity or its separate divisions must be registered by an authorized government agency. Therefore, a change in the location of a separate division, even within the territory under the jurisdiction of one tax inspectorate, entails the need to notify the Federal Tax Service. This requirement also applies if the head office and a separate division fall under the competence of one territorial division of the tax service.

At the same time, in practice there are situations when such notification is not required. For example, information about a branch indicates only the building number, without indicating the specific premises where the branch is located. In this case, moving to a new premises within the same building does not entail the need to declare changes to the tax office.

Documents on changing the address of a separate division are submitted directly to the tax service division at the place of registration of the organization, or are sent there via telecommunication channels, or by registered mail.

Good afternoon. The address of a separate division within one city has changed, information about the change of address is submitted at the place of registration of the parent organization. Do I need to submit information about a change of address to the NI at the place of registration of the separate division? How does the separating checkpoint change in this case?

Good evening, Olga! “Taxpayers - parent organizations are required to report to the tax authority at the location of the organization about all separate divisions (hereinafter referred to as OP) of the Russian organization created on the territory of the Russian Federation (with the exception of branches and representative offices), and changes to information previously reported to the tax authority about such separate divisions:

- within one month from the date of creation of the OP of the Russian organization;

- within three days from the date of change in the relevant information about the OP of the Russian organization.”

The notification of a change in the address of the OP in form No. S-09-3-1 is indeed submitted to the tax authority at the location of the parent organization, which you did absolutely correctly. Next, the tax authority at the location of the OP’s old location deregisters the OP and transfers it for registration at the new address of the OP’s location and immediately assigns a new checkpoint if, when the address changes, the tax authority also changes. In any case, the taxpayer does not make any further communications, but only waits for a Notification from the tax authority at the place of registration of the OP at the new address.

Changing the “separate address”

In essence, this means that, for example, when concluding a new lease agreement for premises to carry out activities through a division at an address under the jurisdiction of another tax authority, the company must carry out the procedure of closing one “separate unit” and opening a new similar structure. Moreover, most likely, the company will have to do the same even if the division changes its address within the territory of the same tax office. Thus, the financiers emphasized, the installation of at least one stationary workplace of a company outside its location is already recognized as the creation of a separate division, regardless of whether this fact is reflected in the constituent documents of the company or not. When changing the address of the company itself, tax registration at the new location is carried out on the basis of documents received by the new controllers from the “old inspection”. But if a separate unit moves. But liability for failure to comply with the message form has not been established. The equipment of a stationary workplace means the creation of all conditions necessary for the performance of labor duties, as well as the performance by the employee of such duties (letter of the Ministry of Finance of Russia dated July 28, 2011 No. 03-02-07/1-265, resolutions of the Federal Antimonopoly Service of the North Caucasus District dated 20 06. 2007 No. F08-3590/2007-1449A, Federal Antimonopoly Service of the North-Western District dated 02.11.2007 in case A26-11293/2005).

- territorial isolation: location other than the location of the organization (location of its permanent executive body). Formally, this condition is met if at least the number of the building differs in the address of the location of the organization and the separate subdivision if other components coincide (locality, street, house).

- availability of equipped stationary workplaces. According to law enforcement practice, a separate unit can arise if even one stationary workplace is equipped (used).

The above signs together mean that the organization carries out activities through its own separate division. For the purposes of tax control, the Russian organization at the place of such activity (location of a separate division) must be registered with the tax authority (Article 83 of the Tax Code of the Russian Federation).

izmenenie_adresa_obosoblennogo_podrazdeleniya_poryadok_deystviy.jpg

Related publications

Many large companies have separate divisions. In the process of activity, various situations arise when branches, representative offices and other “separate units” change their location. Such a change is subject to state registration and in order to make it, the organization must follow a certain procedure.

Read more: Where in Podolsk you can change your medical policy

The process for making changes depends on the specific type of separate unit. One procedure applies for representative offices and branches, and another for other types of separate divisions. This procedure is regulated by the provisions of federal laws No. 14-FZ of 02/08/1998 “On Limited Liability Companies”, No. 129-FZ of 08/08/2001 “On State Registration of Legal Entities and Individual Entrepreneurs”, the Tax Code of the Russian Federation, as well as by-laws - by order of the Ministry of Finance Russia on the approval of Administrative Regulation No. 169n dated September 30, 2016. Let’s consider how the address of a separate division is changed, and the company’s procedure for doing so.

What should a separate division be like for an organization to have the right to the simplified tax system?

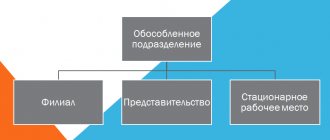

Article 346.12 of the Tax Code of the Russian Federation prohibits the use of a preferential simplified taxation system for organizations that have branches (the requirement for the absence of a representative office has already been abolished). Of course, the question arises - how to register a separate division so that it is not recognized as a branch, and at the same time the organization retains the right to the simplified tax system? To understand this, you will have to refer to the provisions of three codes: Tax, Civil and Labor:

- The Tax Code (Article 11) gives the concept of a separate division of an organization as “... any territorially separate division from it, at the location of which stationary workplaces are equipped.” However, the Tax Code of the Russian Federation does not provide a description of the types of separate divisions.

- The Civil Code (Article 55) characterizes a separate division only in the form of a representative office and a branch . That is, from these provisions it is also unclear what other separate divisions, besides a representative office and a branch, can be.

- The Labor Code (Article 40) indicates that “... a collective agreement can be concluded in the organization as a whole, in its branches, representative offices and other separate structural units .” Thus, only here can one see that separate divisions can be something other than a branch and representative office.

As a result, we are dealing with some elusive concept of another separate division, therefore, when creating such a division, we must simply avoid the criteria that characterize it as a branch or representative office. These characteristics in the law are more than meager:

- a representative office is a separate division of a legal entity located outside its location, which represents the interests of the legal entity and protects them;

- a branch is a separate division of a legal entity located outside its location and performing all or part of its functions, including the functions of representative offices;

- representative offices and branches are not legal entities, and information about them must be indicated in the Unified State Register of Legal Entities, and therefore in the organization’s charter.

It is no coincidence that we understand this issue in such detail, because non-compliance with these requirements (sometimes implicit) can deprive an organization of the opportunity to work on the simplified tax system, and unexpectedly. For example, the manager believes that the created separate division is not a branch, so the organization continues to work on a simplified system, although it no longer has the right to do so.

In such cases, the organization will be recognized as operating under the general taxation system from the beginning of the quarter in which a separate division with the characteristics of a branch was created. And the loss of the right to simplification leads to the need to charge all general taxes: profit tax, property tax, VAT, and it is with the latter that the most problems can arise. VAT must be charged on the cost of all goods, works and services sold for the current quarter, and if the buyer or customer refuses to pay it additionally, then the tax will have to be paid at their own expense.

Representative offices and branches

To change the address of a representative office or branch, it is necessary to analyze the organization’s charter. If this document contains information about the address of such a separate division, then changes to the charter will be required. Let us recall that the current legislation does not oblige such information to be indicated in the charter of a legal entity, but practice shows that in many cases information about branches and their addresses is still available in this document. Therefore, changing the address of a separate division in such situations will require a procedure for amending the charter.

To do this, it is necessary to convene an extraordinary meeting of participants, at which a decision must be made to change the document. There are two options here:

Exclusion from the charter of the clause on a separate division;

Entering new information about the location.

The decision of the meeting is approved by the minutes, which, together with an application in form P13001 and with the new edition of the charter, are submitted to the tax office to register the changes.

In a situation where the organization’s charter does not contain information about a branch or representative office, the procedure for making changes is somewhat different. The head of the organization must make an appropriate decision, on the basis of which an application on form P14001 is filled out. The application must be received by the tax office at the place of registration of the organization within three working days from the date of the decision. Let us note that if the charter of an organization or the regulations on a branch provide for a different procedure for making decisions regarding its activities, including decisions on its name, location and other issues, then the procedure specified in these documents must be observed, for example, a general meeting of participants was held.

Please note that currently there is no need for a separate division to additionally notify the tax authorities at its location about the changes being made. Information about this is received by them through departmental exchange.

Application for registration of another separate division in form S-09-3-1

The application itself is a one-page form. The company should not have any difficulties filling it out.

The application shall indicate:

- TIN/KPP of the parent company;

- its full name;

- tax office code;

- OGRN of the parent enterprise;

- number of new units;

- Full name of the head of the company, his Taxpayer Identification Number;

- contact information (phone number, email address);

- round seal of the company.

Do you want to see a correctly completed application for opening an OP for the tax office? Then get trial access to K+ and move on to the sample prepared by specialists.

If the application is submitted not personally by the manager, but by a representative, then his data is filled out in the document. At the same time, his powers must be documented. Typically, a standard power of attorney form is used for these purposes.

The application is submitted in 2 copies. You can also provide a copy of the application as a second copy. This is necessary to mark on it the date of acceptance by the tax inspector.

Other separate divisions

Changing the address of a separate division that does not belong to the category of branches or representative offices is simplified. To register a change, it is necessary for the head of the organization to issue an appropriate order. After this, a tax notification is submitted about the change of address of the separate division, in form C-09-3-1. This notification is sent within three days (from the date of the decision) to the tax office at the place of registration of the legal entity.

In this case, it is also not necessary to notify the tax authorities at the location of the separate division.

Grounds for refusal to change address

Change of address may be refused. As a rule, the grounds for refusal are as follows:

- Ignoring the deadline for submitting an application (later than 3 days after the decision is made).

- All necessary documents have not been collected.

- Typos and errors in the application.

- The location provided as the address does not exist.

- Legal address is a mass address.

ATTENTION! Sometimes the tax office refuses to change the address due to the presence of a large debt or because the organization is in bankruptcy. However, such refusals are not considered legitimate. They can be challenged in court.

Responsibility for violation of the procedure for registering a separate subdivision

Violation of the deadlines for submitting messages and applications for registration of a separate division entails the following fines:

- violation of the deadline for filing an application for registration - 10 thousand rubles (Article 116 of the Tax Code of the Russian Federation);

- Conducting activities as a separate division without registration - a fine of 10 percent of the income received as a result of such activities, but not less than 40 thousand rubles (Article 116 of the Tax Code of the Russian Federation);

- violation of the deadline for registration with the Social Insurance Fund - 5 thousand rubles or 10 thousand rubles if the violation lasts more than 90 calendar days (Article 19 No. 125-FZ of July 24, 1998).

Registration of changes in the location of a legal entity and its address in 2021.

Currently, the statutory documents do not indicate the legal address, but only the location of the legal entity. Therefore, if when changing the address there is no change in the location of the legal entity, then there is no need to make changes to the constituent documents. For example, your organization has the address: st. Lenin, Moscow, and you change it to the address: on the street. Voikova, Moscow. In this case, the change of address occurs without changing the location of the organization, because the location remains Moscow. Here you will only need to make changes to the Unified State Register of Legal Entities. In this case, no state duty is paid.

However, if the location of the legal entity changes when the address changes, then it is necessary to make changes to the constituent documents. The state duty in this case will be 800 rubles.

When changing the legal address associated with a change in the location of a legal entity, documents are submitted to the tax service twice:

- To enter information into the unified state register of legal entities that a legal entity has made a decision to change its location - within 3 working days after the day this decision was made.

- For state registration of a change in the address of a legal entity, at which the location of the legal entity changes - before the expiration of 20 days from the date of entering into the unified state register of legal entities information that the legal entity has made a decision to change the address of the legal entity, at which the location of the legal entity changes faces.