Excise tax accounting. Features of accounting for excise taxes on alcohol and alcohol-containing products

The following persons are recognized as taxpayers if they carry out transactions subject to excise taxes: Organizations, individual entrepreneurs, Persons recognized as taxpayers in connection with the movement of goods across the customs border.

To reflect in accounting transactions related to excise taxes paid to suppliers of excisable goods, account 19 subaccount “Excise taxes on paid materials and valuables” is intended. Debit 19 of the account reflects the amount of excise taxes paid to the supplier for excisable goods used as raw materials for the production of excisable goods D 19 K 60 – excise tax allocation. If non-excisable products are produced from excisable raw materials, then the excise tax is not allocated, but is included in the cost of the purchased raw materials Dt 10.20 - Kt 19.

Excise goods: ethyl alcohol from all types of raw materials; alcoholic products with a share of ethyl alcohol of more than 1.5%, with the exception of wine materials; beer; tobacco products; auto and motorcycle; petroleum products; alcohol-containing with a volume fraction of alcohol over 9%.

The tax base for excise taxes is the volume, quantity, and other indicators of imported marked goods in physical terms, in respect of which fixed (specific) excise tax rates are established, or the cost of imported excisable goods, in respect of which ad valorem excise tax rates are established, or the volume of imported marked goods in in kind for calculating excise taxes when applying a fixed (specific) tax rate and the estimated cost of imported excisable goods, calculated on the basis of maximum retail prices, for calculating excise taxes when applying an ad valorem (in percentage) tax rate in relation to goods for which combined excise tax rates are established, consisting of fixed (specific) and ad valorem (percentage) rates.

The amount of excise duty on excisable goods for which fixed tax rates is calculated as the product of the corresponding tax rate and the tax base in natural units. The amount of excise duty on excisable goods for which ad valorem (in percentage) tax rates are established is calculated as the corresponding tax rate is a percentage of the tax base. The amount of excise duty on excisable goods in respect of which combined tax rates are established is calculated as the amount obtained as a result of the addition of excise duty amounts calculated as the product of a fixed tax rate and the volume of excisable goods sold in kind and as the corresponding ad valorem (in percentage) tax interest rate share of the maximum retail price of such goods. The total amount of excise tax when carrying out transactions with excisable petroleum products is determined separately from the amount of excise tax on other excisable goods.

The amount of excise tax is calculated based on the results of each tax period in relation to all transactions for the sale of excisable goods, the date of sale (transfer) of which relates to the corresponding tax period. Tax period Calendar month.

Tax deductions for excise duties are made when the following is carried out.

Structure of the tobacco excise tax declaration

——————————¬——————+ Declaration structure +——————¬¦ L—T———————T— ¦¦ ¦/ ¦/ ¦¦ — ————————-¬ ——————————¬ ¦+>¦ Title page ¦ ¦ Section 1 “Amount of excise duty ¦ ¦¦ L—————————- ¦ on tobacco products, ¦¦ ¦ subject to payment to the budget, ¦ ¦¦ ¦ according to the taxpayer”¦ ¦¦ L—————————— ¦¦ ¦¦ —————————-¬ —— ————————¬ ¦+>¦ Section 2 “Calculation of the amount ¦ ¦Section 3 “Calculation of the amount of excise tax” ¦¦ ¦excise tax on tobacco products”¦ ¦ for tobacco products, ¦ ¦¦ L————— ————- ¦ application of exemption ¦¦ ¦ from excise taxation ¦ ¦¦ ¦ for which documents ¦ ¦¦ ¦ are not confirmed” ¦ ¦¦ —————————-¬ L——————— ——— ¦¦ ¦ Section 4 “Presented ¦ ——————————¬ ¦¦ ¦ for reimbursement of the amount of excise duty ¦ ¦ Mandatory attachments ¦¦ ¦ for tobacco products, fact ¦ ¦ for calculating the tax base ¦¦ ¦ exports of which ¦ L——————————¦ ¦ documented ¦¦ ¦ in the tax period, ¦L>¦ and also documented ¦ ¦ confirmed fact ¦ ¦ export of tobacco products, ¦ ¦ for which there were previously ¦ ¦ a guarantee¦ ¦ of a bank or a bank ¦ ¦ guarantee” ¦ L—————————-

Fig. 6

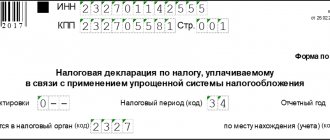

Let's consider the procedure for filling out the declaration according to example 1.

How to record excise taxes in accounting?

conditions:

-Purchased goods are intended for implementation. transactions subject to excise tax.

-the amount of excise tax is actually paid to the supplier of the goods

- purchased goods must be accepted for accounting, i.e. capitalized on the balance sheet of the enterprise

— the company has documents, confirmed. Right to deduction (invoices, invoices)

In accounting, the tax deduction of excise duty is reflected by the posting: D68 K19 The accrual of excise duty on sold excisable goods in accounting is reflected in the same way as the accrual of VAT: D 90 K 68.

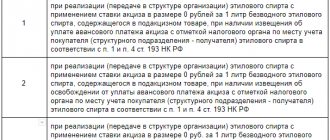

Features of accounting for excise taxes on alcohol products. For alcoholic products, the amount of the refundable excise tax depends on the amount of alcohol dispensed into the production. If non-excise products are produced from raw materials, then the excise tax amount is written off to cost accounts 20-19. Reimbursement of excise duty on alcoholic beverages is made on the basis of the following conditions : the alcohol is processed. The products produced are sold, the alcohol must be paid for, and the excise tax must be paid. The amount of excise tax calculated on the basis of the volume fraction of alcohol used for the production of wine materials or other products is subject to deductions. The deduction is made when the taxpayer provides the following documents to the tax authorities: purchase and sale agreement; payment documents with a bank mark; waybill and invoice; blending acts; acts for writing off wine materials in production. If excess alcohol losses occur: 91-19 excise tax write-off; 20-19 Alcoholic products are labeled specially. Federal stamps.. List of stamps. on the increase article of production, i.e. on s/s. Dt10 – Kt 60 – purchase of brand Dt19 – Kt 60; Dt 20 - Kt 10 - after selling products with the brand, the cost of the brand is included in expenses; Dt 68 – Kt 19. For alcohol-containing products, the accrual of excise duty depends on the availability of the purchaser and purchaser of the sales certificate for operations with denatured ethyl alcohol. From August 1, 2011, the excise tax rate on ethyl alcohol from all types of raw materials (including raw alcohol) and cognac alcohol depends on whether the organization pays an advance payment of excise tax (clause 1 of Article 193 of the Tax Code of the Russian Federation). Thus, when shipping or transferring alcohol within one organization, producers of alcoholic or alcohol-containing products who pay an advance payment are provided with a zero excise tax rate. The same rate is applied by manufacturers of perfumes, cosmetics and household chemicals in metal aerosol packaging.

If manufacturers use alcohol-containing products as raw materials, the amount of deduction will be less than the amount of excise tax actually paid when purchasing alcohol-containing products. In this case, the amount of deduction will be determined based on the excise tax rate on ethyl alcohol. Excise tax rate on alcohol-containing products. set at the same level as the excise tax rate on alcohol products with a volume fraction of ethyl alcohol up to 9%. Payment of excise duty upon the sale (transfer) by taxpayers of excisable goods produced by them is made based on the actual sale (transfer) of goods for the expired tax period no later than the 25th day of the month following the expired tax period. Taxpayers are required to submit a tax return to the tax authorities at their location and at the location of separate divisions no later than the 25th day of the month following the expired tax period.

The excise tax amount is calculated by applying the established excise tax rate to the tax base.

The amount of excise tax on the gambling business is calculated by applying the excise tax rate established for the tax period to the number of objects of taxation.

If the number of taxable objects changes in the tax period, the amount of excise tax on the introduced (retired) object is paid in full;

For excisable goods produced from customer-supplied raw materials and materials, excise duty is paid on the day the product is transferred to the customer or the person specified by the customer.

When transferring crude oil or gas condensate produced on the territory of the Republic of Kazakhstan for industrial processing, excise tax is paid on the day of its transfer .

Excise taxes on other excisable goods are subject to transfer to the budget no later than:

1) on the thirteenth day of the month for transactions made during the first ten days of the tax period;

2) on the twenty-third day of the month for transactions made during the second ten days of the tax period;

3) on the third day of the month following the reporting month, for transactions completed during the remaining days of the tax period.

When producing excisable goods from own raw materials, which are subject to excise duty, the excise tax on these raw materials is paid within the time limits established for the payment of excise duty on finished excisable goods.

The excise tax on the gambling business is paid in conjunction with a fixed total tax (patent) monthly later than the 20th day of the month following the reporting one.

Piece accounting

From July 1, 2021, records of the turnover of labeled alcohol are carried out individually. Corresponding changes have been made to Federal Law No. 171, which currently regulates the alcohol market in Russia. The methodology for organizing accounting according to the new rules is posted on the Rosalkogolregulirovanie website. Previously mandatory paper certificates accompanying alcoholic beverages have been cancelled. Officials believe that this will reduce the labor costs of alcohol accounting organizations.

Let's look at how things work in practice. For piece accounting you need:

- increasing the number of warehouse workers and their training;

- purchase of new equipment and software, without which accounting is impossible (generation of codes for group packaging, continuous scanning of bottles from the manufacturer, scanning when accepting goods for sale, etc.);

- updating the existing software to meet legal requirements, attracting expensive specialists to configure the software, organizing the storage and correct use of huge information arrays.

At the same time, there is no single solution for all participants in the “alcohol” business: an importer of alcohol, a manufacturer or an organization that has suppliers in the wholesale or retail segment of the market - each will face individual problems and will be forced to create their own accounting system in a short time. At the same time, the legislator places responsibility for errors entirely on the organization, without adjustments for the urgency and volume of work.

Example: an alcohol seller complied with the requirements of the law and completely switched to a new accounting system, incurring costs. His supplier partner has not connected to piece accounting: there are no available funds or the process has not yet been completed. The result will be the return of the consignment of goods. The manufacturer is forced to organize accounting for both bottles and group containers - directly on the conveyor, during packaging, or later using a discrete hardware complex. The importer will not be able to keep records of group packaging; he will need to scan each bottle when unpacking the container and independently generate codes for group packaging, re-glue the labels on the box and enter new data into the system.

Attention! According to Art. 14.16 of the Code of Administrative Offenses of the Russian Federation for violation of rules in the field of circulation of alcohol and alcoholic products provides for fines for officials from 10-15 thousand

rubles and more depending on the severity of the offense. An organization may be fined from one hundred thousand to half a million rubles.

Service Temporarily Unavailable

If the payer has several gambling establishments in the region (city), the excise tax is paid separately for each facility.

Excise tax on the activities of organizing and conducting lotteries is paid before or on the day of registration of the issue of the sale of lottery tickets.

Payment of excise tax is made at the place of registration of the excise payer, with the exception of the following cases.

Excise tax payers who have structural divisions pay excise tax at the location of the structural divisions in the prescribed manner if they:

1) production of alcoholic products and all types of alcohol and (or) bottling them;

2) carry out wholesale and retail sales of gasoline (except for aviation) and diesel fuel.

1. At the end of each tax period, the taxpayer is obliged to submit an excise tax declaration to the tax authorities at the place of his registration no later than the 20th day of the month following the tax period.

2. Excise tax payers who have structural units simultaneously with the declaration submit excise tax calculations for structural units.

3. The declaration and calculations for excise duty for structural units are submitted to the tax authority no later than the 20th day of the month following the tax period.

Deadlines for paying excise duty on imported excisable goods

Excise taxes on imported goods are paid on the day determined by the customs legislation of the Republic of Kazakhstan for the payment of customs duties.

Excise duty on imported excisable goods subject to marking is paid before or on the day of receipt of excise stamps.

When actually importing excisable goods, the amount of excise tax is subject to clarification.

| Debit | Credit | Contents of business transactions | Source documents |

| Excise taxes are assessed when petroleum products are received by an organization that has a certificate. | Invoices | ||

| 90-2 | 19, 41 | Excise tax has been assessed on the transfer of petroleum products to persons who do not have a certificate. | Invoices |

| Excise taxes are presented for deduction when transferring petroleum products to persons who do not have a certificate. | Invoices | ||

| 41, 43 | Excise taxes are accrued when an organization that does not have a certificate takes into account oil products produced independently or received as payment for services related to their production. | Invoices | |

| Excise taxes have been accrued on advance payments received for the upcoming shipment of products (goods), the date of sale of which for the purpose of calculating excise taxes is the date of payment. | Invoices | ||

| The amount of excise tax is deducted from the advance payment upon shipment of products (goods). | Invoices | ||

| 90-4 | Excise taxes are charged on the sale of excisable goods. |

Accounting entries for excise taxes

Invoices91-2 Excise taxes are accrued upon the transfer of excisable products as a contribution under a simple partnership agreement (joint activity) or a contribution to the authorized capital of other organizations. Invoices Excise taxes are accrued upon the transfer of natural gas for processing on a toll basis and (or) in the structure of the organization for manufacture of other types of products. Invoices Accrued excise taxes on the use of excisable products for one's own needs in the main production. Invoices Accrued excise taxes on the transfer of natural gas for use for one's own needs in the main production. Invoices Transferred excise taxes to the budget. Payment order (0401060), Bank statement on current account.Accounting entries for accounting for payments for the use of natural resources

| Debit | Credit | Contents of business transactions | Source documents |

| 20, 23, 25, 26 | Fees have been charged for the use of water resources. | Tax return for fees for the use of water bodies, Accounting certificate. | |

| Fees for the use of water resources are listed. | Payment order (0401060), Bank statement on current account. | ||

| 20, 23, 25, 26 | A fee has been charged for the negative impact on the environment. | Accounting information | |

| A fee for negative impact on the environment is listed. | Payment order (0401060), Bank statement on current account. |

Accounting entries for accounting for mineral extraction tax

| Debit | Credit | Contents of business transactions | Source documents |

| 20, 23, 25, 26 | Mineral extraction tax accrued | Tax return for mineral extraction tax, Accounting certificate. | |

| Advance payments for mineral extraction tax have been paid. | Payment order (0401060), Bank statement on current account. | ||

| Mineral extraction tax has been paid. | Payment order (0401060), Bank statement on current account. |

Accounting entries for accounting for regional taxes and fees

| Debit | Credit | Contents of business transactions | Source documents |

| 91-2 | Property tax has been assessed. | Tax return for property tax, Accounting certificate. | |

| Property tax has been paid. | Payment order (0401060), Bank statement on current account. | ||

| Transport tax has been charged. | Tax return for transport tax, Accounting certificate. | ||

| Transport tax has been paid. | Payment order (0401060), Bank statement on current account. | ||

| 91-2 | Regional licensing fees have been assessed. | Accounting information. | |

| Regional license fees have been paid. | Payment order (0401060), Bank statement on current account. |

Date added: 2017-01-21; | Copyright infringement

Recommended content:

Related information:

Search on the site:

Budget payments, taxes and fees

Accounting for value added tax calculations.

To reflect in the accounting of business transactions related to VAT, accounts 19 “Value added tax on acquired assets” and 68 “Calculations for taxes and fees”, subaccount “Calculations for value added tax” are intended.

Account 19 has the following subaccounts:

- 19-1 “Value added tax on the acquisition of fixed assets”;

- 19-2 “Value added tax on acquired intangible assets”;

- 19-3 “Value added tax on purchased inventories.”

In the debit of account 19 for the corresponding subaccounts, the customer organization reflects the tax amounts on purchased material resources, fixed assets, intangible assets in correspondence with the credit of accounts 60 “Settlements with suppliers and contractors”, 76 “Settlements with various debtors and creditors”, etc.

For fixed assets, intangible assets and inventories, after they are registered, the amount of VAT recorded on account 19 is written off from the credit of this account depending on the direction of use of the acquired objects to the debit of the accounts:

- 68 “Calculations for taxes and fees” - for production use; accounting for sources of covering costs for non-productive needs (29, 91, 86) - when used for non-productive needs;

- 91 “Other income and expenses” - when selling this property.

Tax amounts on fixed assets, intangible assets, other property, as well as on goods and material resources (work, services) to be used in the manufacture of products and operations exempt from tax are written off as a debit to production cost accounts (20 “Basic production", 23 "Auxiliary production", etc.), and for fixed assets and intangible assets - taken into account along with the costs of their acquisition.

When selling products or other property, the calculated tax amount is reflected in the debit of accounts 9012021087 “Sales” and 91 “Other income and expenses” and the credit of account 68, subaccount “Calculations for value added tax” (for sales “on shipment”), or 76 “Settlements with various debtors and creditors” (when selling “on payment”). When using account 76, the amount of VAT as a debt to the budget will be accrued after the buyer pays for the products (debit account 76, credit account 68). Repayment of debt to the budget for VAT is reflected in the debit of account 68 and the credit of cash accounting accounts.

Accounting for excise taxes, income taxes, property taxes and personal income taxes

Excise tax accounting is carried out basically in the same way as VAT accounting using accounts 19 and 68.

When calculating income tax, account 99 “Profits and losses” is debited and account 68 “Calculations for taxes and fees” is credited. Tax penalties due are recorded in the same accounting entry. The listed amounts of tax payments are written off from the current account or other similar accounts to the debit of account 68.

Accounting for personal income tax. The procedure for calculating and paying this tax is discussed in Chapter 12, and the procedure for accounting for the unified social tax is also set out there (see clause 12.8).

Property tax accounting. Accounting for settlements of organizations with the budget for corporate property tax is kept on account 68 “Calculations for taxes and fees”, in the subaccount “Calculations for property tax”.

The accrued tax amount is reflected in the credit of account 68 “Calculations for taxes and fees” and the debit of account 91 “Other income and expenses”. The transfer of the amount of property tax to the budget is reflected in accounting as the debit of account 68 “Calculations for taxes and fees” and the credit of account 51 “Current account”.

Sales tax accounting.

Sales tax is calculated using the following accounting entry:

Debit account 90 “Sales” | Credit to account 68 “Calculations for taxes and fees”, | subaccount “Sales tax calculations” |

The transfer of sales tax to the budget is reflected in the debit of account 68 from the credit of cash accounting accounts.

Deduction of input excise tax

Reflect the deduction of the excise tax amount in accounting by posting:

Debit 68 sub-account “Calculations for excise taxes” Credit 19 sub-account “Excise taxes”

– excise tax is accepted for deduction.

For information on the rules for applying excise tax deductions, see When and how excise tax can be accepted for deduction.

An example of how to reflect the deduction of input excise tax in accounting and taxation

Alpha LLC, which has a certificate for the production of denatured ethyl alcohol, sold 1,000 liters of denatured alcohol to a cosmetics production plant in February. The negotiated cost of alcohol is 177,000 rubles. (including VAT – 27,000 rubles, excise tax – 102,000 rubles). The buyer has a certificate for the production of alcohol-containing products. In April, the buyer used all the denatured alcohol received to produce alcohol-containing tincture “Cucumber” in metal aerosol packaging. Documents confirming the plant’s right to a tax deduction were submitted to the tax office in May. The excise tax rate per 1 liter of denatured alcohol is 102 rubles.

The plant accountant made the following entries in the accounting records.

In February:

Debit 10 subaccount “Raw materials and supplies” Credit 60 – 48,000 rub. (RUB 177,000 – RUB 27,000 – RUB 102,000) – denatured alcohol was received from the supplier for the production of alcohol-containing products;

Debit 19 subaccount “Calculations for VAT” Credit 60 – 27,000 rub. – input VAT is reflected;

Debit 19 subaccount “Excise taxes” Credit 60 – 102,000 rub. (1000 l × 102 rubles) – reflects the amount of excise tax presented by the supplier when purchasing denatured alcohol for the production of alcohol-containing products;

Debit 68 subaccount “Calculations for VAT” Credit 19 subaccount “Calculations for VAT” – 27,000 rubles. – input VAT is accepted for deduction;

Debit 60 Credit 51 – 177,000 rub. – paid to the supplier for denatured alcohol.

In April:

Debit 44 Credit 10 subaccount “Raw materials and materials” – 57,000 rubles. – 1000 liters of denatured alcohol were written off for the production of Cucumber tincture.

For tax accounting purposes, denatured alcohol is written off at cost, taking into account accrued excise tax, which amounts to 159,000 rubles. (RUB 57,000 + RUB 102,000). In this regard, a permanent tax asset arises in the amount of 20,400 rubles. ((RUB 159,000 – RUB 57,000) × 20%), which is reflected in the accounting records as follows:

Debit 68 subaccount “Calculations for income tax” Credit 99 – 20,400 rubles. – reflects the amount of the permanent tax asset.

In May:

Debit 68 sub-account “Calculations for excise taxes” Credit 19 sub-account “Excise taxes” - 102,000 rubles. (1000 l × 102 rubles) – excise tax related to denatured alcohol sold for the production of alcohol-containing products is accepted for deduction upon submission of supporting documents to the tax office;

Debit 68 subaccount “Calculations for income tax” Credit 99 – 20,400 rubles. – the amount of the permanent tax asset is reversed when excise tax is accepted for deduction.