Why is it needed and who should have a cashier-operator book (form KM-4)

The cashier-operator's journal was approved by Decree of the State Statistics Committee of December 25, 1998 No. 132 (hereinafter referred to as Decree No. 132), it is also called the unified form KM-4.

The obligation to keep a journal when using cash registers is enshrined in the standard rules contained in the letter of the Ministry of Finance dated August 30, 1993 No. 104. But these rules have lost relevance due to the adoption of a new law on the use of cash registers, according to which most business entities are required to use updated cash register models from July 1, 2017 technology capable of transmitting information to tax authorities about payments to customers online. Read about the use of online cash registers by simplified taxation system payers in this article.

In the new edition of the law “On cash registers” there is no information about the need to use unified forms, and therefore the use of a cashier-operator’s book when working with an online cash register is not necessary. The Ministry of Finance expressed the same opinion in its letter dated June 16, 2017 No. 03-01-15/37692. But companies and individual entrepreneurs have the right to independently maintain this register to account for and control received revenue.

You can find out what documents need to be completed when working with online cash register systems in the Ready-made solution from ConsultantPlus. Trial access to the legal system is free.

Resolution No. 132 provided that the journal is filled out by an employee working at the cash register who serves clients (accepts money from them as payment for goods or services) using a cash register machine (hereinafter referred to as the cash register). The same document stipulated that it should be kept by the manager (manager) or chief (senior) accountant, and given to the cashier before the start of the shift.

You can download the KM-4 log form on our website.

In this register, the cashier had to record the readings taken from the cash register on a daily basis. This journal also served to control the correspondence of the balance in the cash register with what is listed in the car.

Do I need to maintain the KM-4 form?

The KM-4 journal is the official register of all cash transactions performed and recorded in the organization through cash register systems. This form should contain information about the receipt (receipt) and payment (expense) of cash.

If a business entity has several cash registers, this journal should be kept separately for each of them.

The cashier-operator's journal, compiled and filled out according to the standard KM-4 form, is a documentary register of cash transactions.

It accumulates, systematizes and displays data from the so-called Z-reports generated for each cash register device registered with a business entity (organization, individual entrepreneur) receiving/spending cash. Accordingly, KM-4 is used for permanent accounting of cash receipts/expenses.

In the practice of using cash registers, a documentary Z-report is usually called a report containing summary information about cash transactions completed and recorded by the cashier through a specific cash register device for a transaction day.

Every day, a Z-report is generated (removed) from the cash register by the responsible cashier - the cash register operator - for each fact of completion of the next work shift.

Cash reconciliation is carried out daily by the cashier-operator according to the balance recorded in the Z-report.

After this, the money is transferred directly to the administrator (chief cashier).

Using KM-4 for cash accounting, a business entity that regularly makes cash transactions through cash registers has a convenient opportunity to solve several problems at the same time.

For example, the head of an organization can easily control the amount of money passing through a cash register over a certain period of time, having received the necessary information from the cashier-operator’s journal.

In addition, the presence of a regularly filled KM-4 register at a business entity simplifies the work of tax officials who periodically check compliance with cash discipline.

The KM-4 register data is promptly verified with the corresponding figures from the cash register reading log and other reporting documentation.

At online checkouts

The use of online cash registers by business entities when making cash payments to customers makes it unnecessary to maintain the KM-4 register.

This is explained by the fact that the information previously recorded in the cashier-operator’s journal is now automatically recorded in the personal account (account) of the online cash register user on the tax service website.

This relaxation is clearly provided for in separate clarifications of the fiscal authority. Regulatory grounds - letters of the Federal Tax Service of the Russian Federation dated September 26, 2021 and the Ministry of Finance of the Russian Federation dated April 4, 2017.

Read more about maintaining the KM-4 journal at online checkouts here.

When and how to fill out the cashier-operator logbook correctly

When and how to fill out the 2020 cashier-operator logbook? We believe that organizations and individual entrepreneurs that use online cash registers and have decided to fill out the cashier-operator’s journal can independently establish rules for filling it out. In this case, you can rely on the instructions for filling it out, established by Resolution No. 132. The description for the KM-4 register states that the journal is filled out daily by the responsible employee - the cashier.

Entries in the journal should be made using a blue ballpoint/ink pen without marks. If a correction occurs, the entry made by the cashier is certified by the director and chief accountant.

Before using online cash registers, before starting to operate it, it had to be numbered, laced and registered with the Federal Tax Service. Since, as mentioned above, when using online cash registers, regulatory authorities do not feel the need for a log, then there is no need to register it with the INFS. Organizations and individual entrepreneurs can make the decision on the need to number and lace them independently based on internal rules. According to the instructions for filling out KM-4, the journal should have been filled out by the cashier immediately after the Z-report was taken. In online cash registers, when work is completed, a shift closing report is taken, the data of which can be transferred to KM-4.

For more information about where and how to fill out the cashier-operator’s log, read the article “Unified form No. KM-4 - form and sample” .

Is leading allowed or not?

According to the provisions of the above-mentioned Directive of the Central Bank of the Russian Federation No. 3210-U, the cash documents of an economic entity include only cash settlement and cash register orders, which formalize the expenditure and receipt of cash, respectively.

The cash book (CC) does not refer to cash documents, but filling it out is considered necessary.

In fact, the book is an important accounting register that records any facts of receipt and expenditure of cash.

It contains daily information from cash registers and cash registers - cash orders certifying the movement of funds from the organization and individual entrepreneurs. At the end of each day, the cash balance is displayed.

It is recommended to maintain the cash book register using the officially approved KO-4 form. However, an economic entity may develop, approve and apply any other form that contains all the necessary information.

In addition, the regulations of the Central Bank of the Russian Federation allow for maintaining a book in electronic form, which implies the use of computer equipment and suitable software for this.

In other words, a special computer program must display the electronic cash book file with the ability to regularly edit it.

The preferred form is a tabular form of data display, the structure of which most closely corresponds to the above-mentioned KO-4 standard.

The electronic form of the cash book, containing typical fields (columns), is easily filled out using the keyboard and computer mouse.

As a rule, the functionality of the program provides the ability to print saved data on paper.

The current legislation provides for filling out an electronic register at the end of each business day, if incoming or outgoing cash transactions were carried out on that day.

The result of this procedure is the generation of documentation consisting of two conventional sheets:

- a sheet containing numbers and details;

- a report sheet compiled by the cashier himself.

The cashier prints out these sheets, carefully examines their contents, and then signs these papers if there are no errors or inaccuracies in filling out. The sheets are numbered and sent to the cash desk for further storage. How to correct errors in the cash book?

By the end of the reporting year, all copies are collected and filed - a book is formed. Compiled reports are sent directly to the accounting department.

An example of filling out a cashier-operator log

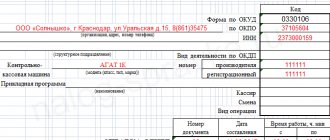

Let's take a step-by-step look at how to fill out the cashier-operator's journal. So, the cashier who passed the shift usually takes a report on the closure of the shift. The data from this document is used when filling out column 4 (report serial number), column 5 (the previous entry is duplicated here), column 6 (counter indicator) and column 10 (daily revenue). Column 9 displays data from the report taken at the end of the shift.

Columns 1–3 indicate: date, department number, cashier’s full name. In columns 7–8, 16–18, the signatures of the cashier, administrator and senior cashier are affixed, if these are 3 different people, and when combining positions, 1 signature is sufficient.

Column 11 displays the amount of cash, column 12 - the number of non-cash payments, column 13 - the non-cash amount, column 14 - the amount minus returns, column 15 - the total value of refunds from the cash register to customers.

It is very easy to check the correctness of the entered data - to do this, compare the readings from the Z-report (column 10 of the register = column 14) and the total values from columns 11–12 minus column 15.

Some more test formulas:

- column 11 = column 10 – column 13 – (column 15);

- column 14 = column 11 + column 13;

- Column 10 = Column 9 – Column 6.

Let's look at a sample of filling out a cashier-operator's book.

Filling out and maintaining a journal

Sample of filling out the cashier-operator's journal of form KM-4

The cashier's journal is kept as follows: at the beginning of a shift or working day, in columns one through three, the cashier notes the shift or date, department number and his full name.

In column 4 enter the serial number of the counter (fiscal memory report) at the end of the previous shift or working day.

The “Indications” column is filled in only when the vehicle is re-registered, checked, transferred for repair or deregistered by an employee of the technical service center or tax office. In the future, the cashier must rewrite this indicator.

Before the start of a shift or working day, the cashier records in the column the cash meter readings at the beginning of the day, which are certified in columns 7 and 8 by the signatures of the cashier and a representative of the enterprise administration, respectively.

At the end of the shift or working day, the cashier writes down the final meter readings in column 9.

In column 10 enter the amount of revenue per shift or day, which should be equal to the difference between columns 9 and 6.

Columns 11-14 contain information about what the cashier hands over to the main cash register at the end of the day:

- cash (column 11);

- number and amount of paid documents (columns 12, 13);

- the total amount deposited to the main cash register at the end of the day (column 14, equal to the sum of columns 11 and 13).

Columns 12 and 13 are filled in when paying for goods by credit card. In fact, the funds do not go to the cash desk, but to the company’s current account. However, the proceeds should still be posted through the cash register. Thus, column 12 contains data on the number of transactions on credit cards, and column 13 – revenue from them.

Column 15 contains records of the amounts that were issued for returned checks (the basis of the data is the act of returning funds to customers for unused checks to the cashier, form No. KM-3) and the number of zero checks printed per shift or working day.

At the end of the shift or day, the cashier draws up a certificate report in form No. KM-6, which is submitted along with the revenue from the cash receipt order to the senior cashier.

The entries made are confirmed by the signatures of the senior cashier, cashier-operator and administrator of the enterprise (organization) after checking the actual revenue and meter readings at the end of the shift or day. To do this, fill out columns 16-18. Orders approve specific persons who must check, accept and confirm the proceeds handed over by the cashier.

If the results of the amounts on the control tape diverge from the actual revenue, then the reasons for the discrepancy are clarified, and the identified surpluses or shortages are entered in certain columns of the cashier's journal.

No blots or erasures are permitted in this document. Corrections made are specified and certified by the signatures of the cashier, chief accountant and head of the organization.

When using several cash registers, Form No. KM-7 is additionally filled out, containing data on machine meter readings and enterprise revenue.

cashier-operator form No. KM-4

Results

Organizations and individual entrepreneurs, when making payments using online cash registers, may not fill out the cashier-operator log.

But if they decided to continue maintaining this register to fulfill internal tasks, then they are recommended to establish the procedure for maintaining it. When using online cash registers, registration of the cashier-operator's journal with the tax authorities is not required. You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

Is it necessary to lead - features of leading

The term “online cash register” defines cash register equipment, the functions of which are associated not only with printing checks and storing information about them, but also transmitting information about them in the form of electronic copies to the tax service.

Other positions of the cash register remain unchanged and differ little from previously accepted standards.

Keeping a log on the KM-4 form for the operations of the old cash register was carried out manually.

The design of the journal when putting online cash registers into operation has a great advantage over the previous form: all information on cash transactions (cash and non-cash payments) is automatically recorded in the cash register system, and then copies are sent to the tax authority.

Answering the question whether it is necessary to keep a cashier's journal when working with online cash registers, the Ministry of Finance of the Russian Federation provided clarifications in letter dated April 4, 2021 No. 03-01-15/19821.

It is reported here that the use of unified forms of primary documentation, to which the journal belongs, is not provided for in the work of the new regulations, therefore, the form is not mandatory for registration.

Using an online cash register eliminates the need for journaling.

Application of the cashier's journal

[ads-pc-3] [ads-mob-3]

The cashier-operator's journal is a special register, which is compiled according to the standard unified form KM-4, and serves to record the receipt and delivery of the company's revenue, as well as to reflect reporting benchmarks.

It is compiled for each cash register. Its maintenance is entrusted to authorized officials (cashiers), who must regularly take the relevant accounting indicators and record them in it.

The cashier's report exists in several forms. The register reflects only the total for the day or shift, which is called a z-report.

For the first time, the cashier's log of the operator at km 4 is started at the time of registration of a new cash register. This book can be purchased at a printing house. It must be numbered, laced, sealed and stamped with a supervisor’s visa. After that, it, together with the cash register card, is submitted to the tax office, where its employees mark the number they assigned on it and affix stamps and signatures.

The journal is maintained until its last line is filled. As soon as it ends, the organization must draw up a new register, while the old and subsequent ones are submitted to the inspectorate at the place of registration. Tax workers make an entry about its replacement in the KKA registration card.

The log also reflects the notes of the technical staff of the central service center, who check it in accordance with the cash service agreement.

According to the law, all KKA have EKLZ, which must be installed every year, otherwise the machine will be blocked. Its replacement must also be recorded in the cashier-operator's journal.

At the end of his shift (working day), the cashier takes a final report on the cash register and checks its data with receipt documents (if any) and cash. After this, he records the z-report readings in the journal, fills out a certificate report and hands over the daily earnings either to the senior cashier or to an authorized person, who, after checking and receiving the cash, signs in the register and returns the journal back to the cashier.

Filling procedure

Column 1: Date (change)

The date of the Z-report is set and entered into the journal. If several Z-reports were taken for this date, then they all need to be entered in a separate line, but they will all be the same date. The word “shift” in this column means that if on one date you worked two shifts and two different cashiers, you can (not necessarily) put the shift number in brackets, for example: 02/01/2013 (1).

Column 2: Department (section) number.

This column contains the numbers of the departments to which the amounts for this shift were made. You don’t have to fill out this column if you are focusing everything on one department, for example the first. Even if you break down the amounts into several departments, you may not fill out this column, especially since division by department is not provided for in the Z - reports of many cash registers.

Column 3: Last name, first name, patronymic of the cashier.

Full name is written here. cashier. If the cashier, administrator, accountant, general director are all one person, then you need to enter his (her) last name in this column.

Column 4: Serial number of the control counter (fiscal memory report) at the end of the working day (shift).

The serial number number Z of the report is written here; it can be taken from the report itself (see example).

Column 5: Serial number of the control counter (fiscal memory report), recording the number of transfers of the summing money counter readings.

The data from column 4 is copied here. This is an outdated form of the document, which assumes in the old fashioned way that the Z-report counter will be reset to zero. In modern cash registers this function has been removed.

Column 6: Readings of summing cash counters at the beginning of the working day (shift)

This column is required to be filled out. It contains the cumulative total at the beginning of the day - the sum of all the money entered on the cash register for the entire period of its existence. This amount increases with each Z-report taken. After some time after working at the cash register, this amount can reach millions, and God willing, billions of rubles. If the cash register is new, then your first savings will be equal to 1 ruble. 11 kopecks — this is the amount the tax inspector requires to enter when registering a cash register.

If the cash register is not new, then the data for this column is taken from:

- columns 9 of the previous day (the most common method)

- from the morning X-report. True, not every cash register prints savings in X reports

- the amount in this column can be recorded at the end of the day by subtracting the amount of revenue for the day (column 10) from evening savings (column 9).

Columns 7 and 8: signature of the cashier and administrator.

The cashier and administrator must sign in these boxes respectively. If this is the same person, then the signatures will be the same.

Column 9: Readings of summing cash counters at the end of the working day (shift)

This is where savings are entered ("non-zeroable total", also called "gross total") at the end of the work shift. These are the same savings that were in Column 6, but revenue for the past day has been added to them. These savings are written off from the Z - report that the cashier takes at the end of the shift (example here). For convenience, you can immediately transfer this amount to the beginning of the next shift in column 6.

Column 10: Amount of revenue per working day (shift).

This includes the amount of revenue per day. This includes all cash proceeds (column 11), non-cash (column 12), returns (column 15). This data can also be taken from Z - reports (see example).

Box 11: Delivered in cash.

Cash revenue is included here; it does not include returns and non-cash payments.

Column 12: Paid according to documents, quantity

This column contains the number of non-cash payments (payments by bank cards, traveler's checks, bank checks, etc.). That is, if you were paid by bank transfer 5 times during the day, you enter the number “5” in the column. If you cannot calculate this amount, since many cash registers do not have cashless payment counters, then you do not need to enter anything.

Column 13: Paid according to documents, amount.

The total amount of non-cash payments is entered here; it is also highlighted in the Z-report (not on all cash registers).

Some cash registers do not have a cashless payment function, so often a certain department (section) is allocated for non-cash transactions and the non-cash payment is processed there. If you are sending all non-cash funds to one of the departments, then enter in column 13 the amount of sales for this particular department .

See below for an example of filling.

Column 14: Total handed over.

The amount of non-cash and cash payments minus refunds is written here.

Column 15: Refund amount.

The total amount of returns for the shift is written here. This line is taken from the Z - report. If you did not make a refund from the cash register (since this is not necessary), then do not forget to fill out the KM-3 act and enter the amount from this form in column 15. Read more about returns here.

Column 16: cashier's signature.

After filling out the cashier-operator journal, the cashier draws up a certificate-report of the cashier-operator (form KM-6), passes it to the administrator along with the cash, and signs in this column.

Very often, the cashier, administrator and manager are one person, so one signature is placed in columns 16, 17,18.

Box 17: administrator’s signature.

Having accepted cash from the cashier, the administrator checks the accuracy of the calculations and signs in this column.

Box 18: signature of the manager.

After the shift is completed, the manager signs here.

After filling out the cashier-operator's journal, do not forget to enter the data (record cash) in the cash book.

What documents do not need to be filled out?

New legislation automatically abolished the mandatory use of a wide range of documents that were previously filled out manually. For example, journals, reference reports, acts will now be generated programmatically in electronic form. In addition, there is now no need to fill out primary documents that register the receipt of funds from customers. The group of cash documents data includes unified forms, ranging from KM-1 to KM-9.

The cashier-operator's journal (form KM-4) is the primary cash document reflecting cash flows and cash receipts. This document was approved by the State Statistics Committee 20 years ago, since then it has reflected the revenue of a retail outlet for a work shift. Until 2021, the form was mandatory for all organizations and had fairly clear requirements. The document register must be numbered, and each entry of information from the cash register must be signed not only by the cashier, but also by the chief accountant and the head of the enterprise. The importance of the document was due to the need for the Federal Tax Service to control the use of cash registers using the cashier-operator’s journal.

Now, the need to manually enter data on cash register transactions has become optional. For reporting purposes, this document is generated automatically in the cash register system, copies of checks are transmitted electronically to the tax service.

In addition, an additional benefit of using an online cash register is that customers who make purchases through online stores can receive receipts. Now this operation takes just a few minutes, and after making the payment, the buyer can find a receipt in his email that contains all the necessary details of the seller and the purchased product.

Despite the legal optionality of keeping a journal, many managers and accountants advise continuing to keep records in order to most accurately control the flow of cash through retail outlets and for the purpose of a more responsible attitude of cashiers to their work.

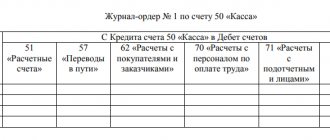

Journal warrant 6

Settlements for delivered goods and services are reflected in journal order 6 - a combined register recording the receipt of goods and services and further payments for them.

Journal order 6 (filling sample attached) is maintained according to account. 60 “Settlements with suppliers and contractors” for each counterparty.

| Provider | Check | From K/ta account. 60 in D/t accounts | From to the beginning of the month | Paid | from-to to the end of the m-tsa | ||||||

| 08 | 10 | 19 | 20 | K/t 51 | K/t 91 | ||||||

| LLC "Temp" | No. 100458 dated 01/18/2016 | 145200 | 26136 | 0 | 171336 | 0 | |||||

| OJSC "Shopping Center" | No. 000145 dated 01/05/2016 | 123000 | 0 | 0 | 123000 | ||||||