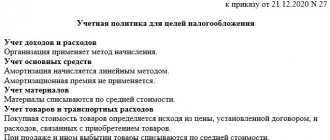

Accounting for goods in trade

A rational system of accounting for goods, combined with the efficiency of their sale, contributes to the formation of financial resources of a trading company necessary for its stable and full-fledged functioning.

Today, in conditions of an unstable economic situation, declining consumer demand, unpredictable changes in foreign exchange rates, and a tense political situation in the world, not only the rules, but also the forms of trade are changing. Mostly, forms of online trade in goods and services have recently developed. In this connection, companies began to gradually introduce the possibility of purchasing goods sold through the online store system using personal computers and various gadgets. Increased competition and excess supply of goods requires trading enterprises to adapt to new trading conditions: sell only those goods that are in demand; offer new products; create new marketing methods of promotion, etc.

Purpose of accounting for goods in trade

Due to the fact that “ the purpose of accounting for transactions for the sale of goods is to provide users with information about the results of the activities of trading organizations for decision-making, the detailing of accounts should be carried out, maximally reflecting the information system for managing the sales of goods.” Considering sales management as a methodology of market activity that determines the strategy and tactics of organizations in a competitive environment, A.O. Lebedkin and I.V. Eremina, they think it is necessary to Fr.

The activities of trade organizations, according to Yu.A. Kotlovoy “requires differentiation of accounting data for internal and external users (primarily for reporting) and increasing the efficiency of managing product sales.” This can be achieved by improving the analytical accounting system. With the help of synthetic accounts, it becomes possible to isolate from the entire income of a trading organization the income from the sale of goods and in the context of each product separately, which allows for an in-depth analysis of sales, and to decide the feasibility of purchasing and selling a particular product.

Accounting for receipt of goods in retail organizations

ACCOUNTING FOR THE RECEIPT OF GOODS AND RULES FOR ACCEPTANCE OF GOODS IN RETAIL TRADE ORGANIZATIONS

In retail trade, goods for resale come from production organizations - manufacturers of goods and wholesale trade organizations that trade from warehouses.

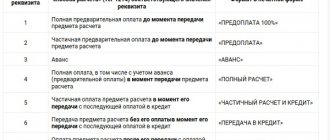

Goods entering the retail chain must have accompanying documents (invoices, waybills, delivery notes, etc.) provided for by the delivery conditions, as well as the rules for the transportation of goods. The procedure for receipt and rules for accepting goods in retail and wholesale trade are almost the same. We discussed these issues in sufficient detail in Section 2 “Wholesale Trade”, so we will not repeat ourselves, we will only note that goods are usually delivered to retail outlets from the supplier by road. In this case, the movement of goods from the supplier to the retailer is documented by a consignment note, which consists of two sections - goods and transport.