Magazine KO-3

The journal for registering incoming and outgoing cash orders (form KO-3) records the primary accounting documents of cash circulation of funds.

The requirement for public sector organizations to reflect them in the registration book is enshrined in Order of the Ministry of Finance dated March 30, 2015 No. 52n. For non-public sector organizations, including non-profit organizations, it is not necessary to use the form (No. 402-FZ). But if an organization decides to use it, it is necessary to consolidate this in its accounting policies.

The form of the book was approved by Resolution of the State Statistics Committee of August 18, 1998 No. 88 and determined by the unified form code 0310003.

Magazine form

The journal for registering incoming and outgoing cash documents is an accounting book in which it is necessary to enter information and details of all documents issued by the cashier. Its unified form was approved by Resolution No. 88 of the State Statistics Committee of the Russian Federation dated August 18, 1998. It is called No. KO-3, but if desired, organizations may not use it and develop their own version. Indeed, since 2013, the use of such unified forms of primary accounting documents has been recommended. Although the remaining cash papers, in particular the same cash registers, in accordance with information from the Ministry of Finance No. PZ-10/2012, are mandatory in the approved form.

The log book is a regular consolidated accounting register, so you can develop it yourself. By virtue of Article 10 of the Federal Law of December 6, 2011 No. 402-FZ “On Accounting,” approval of accounting registers is the prerogative of the head of the organization upon the recommendation of the chief accountant. The main thing is to indicate the option used in the accounting policy. But if desired, you can use a unified form (this should also be mentioned in the accounting policy). However, this is always a book that must be numbered end-to-end and stitched. Typically, the inside of the journal form for registering incoming and outgoing orders consists of two halves of equal volume:

- For receipt orders.

- For expense orders.

They are carried out simultaneously. Information about income is usually placed on the right side of the sheet, and information about expenses is on the left. The legislation allows keeping a register not only on paper, but also in electronic form. In this case, it should be possible to print the completed form and generate it within a certain period of time. In addition, you don’t have to use paper copies if the responsible person (accountant or cashier) has a qualified electronic signature with which he can certify the records.

What to include in form KO-3

When handling primary accounting documents for cash accounting, you must follow the instructions of the Bank of Russia:

- dated 10/07/2013 No. 3073-U on the procedure for making cash payments;

- dated March 11, 2014 No. 3210-U on conducting cash transactions for accepting cash.

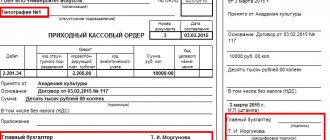

It is necessary to keep records of all “primary” documents that are drawn up when handling cash:

- cash receipt orders (PKO);

- expense cash orders (RKO).

Be sure to include the following information:

- order number;

- date;

- amount;

- notes.

How to keep a register of PKO and RKO

The cash register manager, senior cashier or an employee of the accounting department authorized to perform these actions in accordance with the order has the right to fill out the KO-3 form.

The journal records all cash transactions associated with the cash register. In particular, cash orders of various types, statements, statements and others.

Not everyone knows that the registration log of PKO and RKO can be kept both in paper and electronic form

Filling out a cash register, sample

It is allowed to keep a journal both using technical means (that is, in electronic form) and in paper form. If the journal is kept in paper form and filled out by hand, you should remember that all its pages must be numbered, stitched with thread and certified with a signature.

Let's look at how to fill out a cash register using an example.

Conventionally, the process can be divided into two parts: filling out the title page and the accounting table.

Step 1. Fill out the title page.

We indicate the name of the organization. If there are no structural divisions, a dash is added. We write code using OKPO according to statistics.

Step 2. We register the period for which records are kept. Also the position and full name of the responsible person.

Next, fill out the tabular part.

Each sheet is divided into two parts: on the left side – registration of receipt orders (RPO); on the right - expense orders (RKO). They are filled in the same way.

Step 3. Fill in the date and serial number of the receipt or expense document.

Step 4. We write down the amount indicated in the document.

Step 5. In the note we briefly indicate the information from whom the money was received or to whom the money was issued, as well as the basis for this.

IMPORTANT!

Corrections and absence of required entries are unacceptable!

Journal of registration of incoming and outgoing cash documents

Home / Cash discipline

| Table of contents: 1. Nuances of magazine design 2. Sample filling + instructions | Document: Download form KO-3 Download sample filling KO-3 |

The register of cash documents is an accounting journal in which primary documents are recorded that are subject to further transfer to the cashier for execution. These include:

- incoming and outgoing orders (PKO and RKO);

- payroll and payroll statements;

- invoices for payment;

- applications for cash withdrawal, etc.

At the same time, cash settlements issued for the payroll are registered in the journal after the actual payments are made, while other documents are recorded in the register before the receipt or issuance of money.

Nuances of magazine design

The standard form of the registration journal No. KO-3 was approved by Resolution of the State Committee on Statistics of the Russian Federation dated August 18, 1998 No. 88.

1) Since January 1, 2013, the unified forms have lost the status of mandatory documents. There is no legal requirement to use a registration journal in form No. KO-3 in accounting, nor is there any administrative responsibility for the absence of such a register. However, for organizations (IP) with a large document flow, it is advisable to register documents related to cash flow in order to avoid unlawful withdrawal of money from the cash register using counterfeit papers.

The presence of a journal allows you to reconcile the registered documents with the papers according to which the cashier issued and received cash during the working day, and compare the actual cash balance with the amounts according to the documents recorded in the register.

An entity can develop a sample register of primary cash documents independently, based on the characteristics of its economic activity, or use a standard form.

2) The function of filling out the journal is usually assigned to the financially responsible employee (accountant, cashier, etc.). The chief accountant controls the correctness of filling out the document.

3) The period of time for which the register is opened is determined by the company independently and depends on the volume of primary documentation.

4) The journal can be kept either in paper or electronic . The paper form should be numbered, stitched and certified with the personal signature of the manager (other authorized person). It is not necessary to affix a stamp. Most accounting programs generate a logbook automatically without additional time investment on the part of the responsible employee.

5) It is not advisable to make mistakes when filling out the form. If an error is made, then the incorrect information must be crossed out (the erroneous entry should be easy to read), the correct data must be entered at the top, the signature of the responsible employee and the date the correction was made.

Sample of filling out form KO-3

Title page

- In the line “Organization” the abbreviated name of the organization or individual entrepreneur is indicated (the journal is an internal consolidated register and there is no need to write the full name in accordance with the constituent documents).

- The line “Structural division” is filled in if the company has divisions.

- In the line “OKPO code” the OKPO code from the Rosstat notification is indicated.

- In the center of the title page the period for which the register is opened is indicated.

- The position and full name are filled below. the person responsible for maintaining the document.

Loose-leaf

Loose-leaf sheets are presented in the form of a table divided into two parts:

- on the left side (columns 1-4) receipt documents are registered;

- on the right side (columns 5-8) – consumables.

The table is filled in as follows:

| Column no., arrival | no ., consumption | Content |

| 1 | 5 | Date of preparation of the primary document |

| 2 | 6 | Its serial number |

| 3 | 7 | Amount of document in rubles and kopecks |

| 4 | 8 | Notes: – information about the recipient (payer); - purpose of money. |

Did you like the article? Share on social media networks:

- Related Posts

- Cash book (form KO-4)

- Sample of filling out form AO-1

- Order establishing a cash limit in 2021

- Application for the release of money for reporting

- Cash limit for LLCs and individual entrepreneurs in 2021

- Order to abolish the cash limit in 2021

- Sample of filling out form T-53

- Cash accounting book (form KO-5)

Leave a comment Cancel reply

Do you need a cash register for online cash registers?

In terms of functionality, this is the same device as before, which prints checks and stores information about them. But only now, online cash registers (including when renting an online cash register) need access to the Internet in order to transmit information about completed transactions to the tax office. There is also such a function as sending a receipt to the buyer by email.

Now, thanks to the innovative online cash register, many documents that were approved in the State Statistics Committee Resolution No. 132 dated December 25, 1998 do not need to be used. But this does not apply to documents such as:

- cash register;

- incoming and outgoing orders.

Therefore, the need to keep records in a special book at online cash registers is retained. The maintenance rules are set out in detail in the instructions of the Bank of Russia dated March 11, 2014 No. 3210-U.

Online cash registers

When asked whether a cash register is needed for online cash registers, the answer is clear - no. Transactions are recorded and receipt numbers are assigned automatically by the device’s fiscal storage device. Therefore, no additional accounting registers are provided in this situation. Before the introduction of cash register equipment with the function of online data transfer, cashiers-operators kept journals for registering receipt and expenditure orders, in which they recorded data on revenue; now this obligation has been canceled for them. The relevant explanations on this matter were given by the Russian Ministry of Finance in letter dated June 16, 2017 No. 03-01-15/37692.

Filling procedure

The basis of an account book is its title page. In addition to the name of the document itself, the following details are entered on it:

- name of the enterprise where accounting is carried out;

- OKPO (general classifier of enterprises and organizations);

- the start date of maintaining the document and the period for which it is created;

- Full name of the person responsible for filling it out, indicating the position.

Here you can find a sample document

The following sheets of the book contain the same tables to fill out. They contain eight points, 4 of them relate to expenses and another 4 to income:

- Column 1 – date of registration of the receipt order;

- Column 2 – document serial number;

- Column 3 – amount of capital received;

- Column 4 – a note in which the source of cash receipts is recorded;

- Column 5 – date of issue of the expenditure order;

- Column 6 – document serial number;

- Column 7 – amount of expenditure funds;

- Column 8 – a note indicating what the funds are spent on or for whom they are intended.

Who fills out the log book?

As a rule, the journal is filled out by the cashier or an appointed accounting employee who knows the filling rules assigned by the head of the organization. This person is financially responsible, for which an agreement is drawn up with him in advance. Illiterate maintenance, errors in the registration log of PKO and RKO, which are identified by the auditor, entail administrative liability (Article 15, paragraph 1 of the Code of Administrative Offenses of the Russian Federation).

Regulations of the Federal Law “On the Central Bank of the Russian Federation” No. 86, art. 34 of July 10, 2002 instructs the Bank of Russia to streamline cash transactions carried out by legal entities and entrepreneurs. Thus, this Federal Law establishes unified rules that are binding on the listed persons.

There is a concept of a cash limit for any enterprise. Its size is determined by the Central Bank - it is also agreed on an individual basis with the management of the organization. The amount of money exceeding the established limit must be kept in the bank.

It is worth considering in a little more detail what receipt and expense orders are that are subject to registration.

Tags: accountant, tax, expense, tool