At what rate is Belarusian VAT calculated?

When importing goods from Belarus, the Russian importer is obliged to pay import VAT, regardless of the territory of which country they were produced (this is evidenced by the letter of the Ministry of Finance of the Russian Federation dated September 8, 2010 No. 03-07-08/260). No exceptions are made for anyone: in this case, taxpayers pay VAT regardless of the chosen taxation system.

However, there is a list of goods exempt from import VAT. First of all, these are the lists given in Art. 150 of the Tax Code of the Russian Federation and the Decree of the Government of the Russian Federation dated April 30, 2009 No. 372, issued in accordance with it. The exemption under Art. 149 of the Tax Code of the Russian Federation.

For a list of cases when you do not need to pay VAT on imports from Belarus, see ConsultantPlus. Trial access to the system can be obtained for free.

For non-tax-exempt goods, the usual rates for import from Belarus are 20% or 10%, depending on the type of goods. A reduced 10% rate is provided for goods included in special lists established by the Government of the Russian Federation. In particular, for food products and children's products, such lists were approved by Decree of the Government of the Russian Federation dated December 31, 2004 No. 908. Imported products for which no benefits are established are taxed at a rate of 20%.

For shipments during the transition period (2018-2019), it was necessary to choose the VAT rate based not on the date of shipment of goods by the foreign seller, but on the date of their acceptance for registration by the Russian buyer. If the goods were shipped in 2021 and registered in 2019, the rate should be 20%.

A ready-made solution from ConsultantPlus will help you calculate VAT on imports from Belarus. You can view the material for free by obtaining demo access to the system.

When should VAT on imports from Belarus to Russia be transferred to the budget?

VAT must be paid by the 20th day of the month following the one in which the imported goods were registered.

Important! Tip from ConsultantPlus, when importing under a leasing agreement (if the transfer of ownership of the leased item is provided), pay VAT on each leasing payment no later than... For more details, see K+. This can be done for free.

KBK for payment: 182 1 0400 110.

You should pay the tax to your Federal Tax Service.

If a company has overpaid federal taxes, they may not remit import VAT at all. However, in this case, inspectors must submit a corresponding application requesting offset of the overpayment.

It should be borne in mind that, according to paragraph 4 of Art. 78 of the Tax Code of the Russian Federation, tax authorities are given 10 working days from the date of filing such an application to make a decision on the offset. And if the organization sends it without taking into account the fact that payment must be made by a certain day, it is quite likely that the inspectorate will carry out an offset when the VAT payment deadline has already passed, and then penalties will be charged.

How to pay VAT when importing goods

When importing goods from Belarus and Kazakhstan, the company must transfer import VAT to the budget (Article 3 of the Agreement between the Government of the Russian Federation, the Government of the Republic of Belarus and the Government of the Republic of Kazakhstan dated January 25, 2008 “On the principles of collecting indirect taxes when exporting and importing goods, performing work, provision of services in the Customs Union"). The tax must be paid to the tax office at the place of registration of the company (Article 2 of the Protocol of December 11, 2009 “On the procedure for collecting indirect taxes and the mechanism for monitoring their payment when exporting and importing goods in the Customs Union” (hereinafter referred to as the Protocol on the procedure for collecting indirect taxes ).

Such rules apply regardless of the country in which the imported goods are produced - in Belarus, Kazakhstan or some other state (letter of the Russian Ministry of Finance dated September 8, 2010 No. 03-07-08/260). That is, if you import Norwegian goods from the Republic of Belarus, then the rules for paying VAT within the Customs Union will apply.

Note. If your company is on the simplified regime Companies on the simplified regime, as well as on the general regime, pay the same VAT when importing goods from the Customs Union and submit a special declaration to the tax authorities. There is no difference.

At the same time, organizations must pay tax not only on the general taxation system, but also those applying special tax regimes (clause 1, article 2 of the Protocol on the procedure for collecting indirect taxes). At the same time, there is a list of products whose import into Russia is exempt from VAT. This is, for example, technological equipment. A complete list of such products is given in Article 150 of the Tax Code of the Russian Federation.

How to calculate the cost of goods

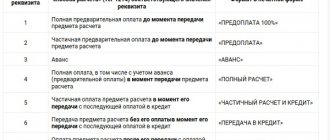

The amount of VAT must be calculated from the cost of goods that the company pays to the supplier under the terms of the contract. For excisable goods, their price must be increased by the amount of excise taxes. Expenses that, according to the terms of the contract, are not included in the cost of goods (for example, transportation) are not taken into account when calculating VAT (letter of the Ministry of Finance of Russia dated April 14, 2011 No. 03-07-14/33). The tax must be calculated on the date when the goods are registered (Clause 2, Article 2 of the Protocol on the procedure for collecting indirect taxes). The payment procedure will depend on the currency in which the contract is drawn up and in which currency the buyer pays for the goods.

Agreement and payment in rubles . The tax is calculated based on the contract value of the goods, which the supplier also indicates in the shipping documents (invoices).

Agreement and payment in foreign currency . When calculating VAT, the cost must be converted into rubles at the exchange rate on the date the goods were accepted for registration.

Agreement - in foreign currency or currency. e., payment in rubles . If the shipping documents indicate the price in foreign currency or currency. That is, then the cost must be converted into rubles at the exchange rate on the date the goods were accepted for registration. This conclusion follows from the rules for filling out an application for the import of products (clause 3 of Appendix No. 2 to the Protocol of December 11, 2009 “On the exchange of information in electronic form between the tax authorities of the member states of the Customs Union on the paid amounts of indirect taxes” (hereinafter referred to as the Protocol on exchange of information).

Under an agreement concluded in foreign currency or currency. That is, the company can transfer an advance payment to the supplier from Belarus or Kazakhstan. In this case, it is not clear on what date to recalculate the value of the goods into rubles for VAT purposes - on the date of payment of the advance or on the date of acceptance of the goods for registration. As we found out, the Russian Ministry of Finance considers the second option correct.

Since in tax accounting in such a situation the cost of goods is recalculated into rubles on the date of prepayment, the tax base for VAT and for income tax, as well as accounting, will be different.

Example 1: How to calculate import VAT when transferring an advance payment to a supplier A company purchases goods worth 50,000 euros from a Belarusian supplier. According to the agreement, the company transfers the advance in rubles at the exchange rate on the date of payment. The Bank of Russia exchange rate on the date of transfer of the advance is (conditionally) 47.5759 rubles/EUR, on the date of receipt of goods - 47.8279 rubles/EUR. In the primary version, the supplier indicated the cost in euros. The advance amount is RUB 2,378,795. (50,000 EUR x 47.5759 RUR/EUR). At this cost, the accountant reflected the goods in tax and accounting records. Import VAT is RUB 430,451.10. ((50,000 EUR x 47.8279 RUR/EUR) x 18%).

If the cost in invoices and primary documents is given in Russian rubles, then the VAT amount must be calculated from it.

At what rate is tax calculated?

Import VAT, like regular VAT, must be calculated at a rate of 18 or 10 percent, depending on the type of product (Clause 5, Article 2 of the Protocol on the procedure for collecting indirect taxes). A reduced 10 percent rate can be applied when importing goods that are included in one of the lists approved by the Government of the Russian Federation according to the All-Russian Classification of Products or the Commodity Nomenclature of Foreign Economic Activity (clause 20 of the resolution of the Plenum of the Supreme Arbitration Court of the Russian Federation dated May 30, 2014 No. 33, letter of the Ministry of Finance of Russia dated August 4, 2014 No. 03-07-07/38358). For example, for food products and products for children, refer to the lists approved by Decree of the Government of the Russian Federation of December 31, 2004 No. 908. For the import of other products, the rate of 18 percent applies.

When should taxes be transferred to the budget?

VAT must be transferred to the inspectorate no later than the 20th day of the month following the month in which imported goods were registered (Clause 7, Article 2 of the Protocol on the procedure for collecting indirect taxes). At the same time, a company that has an overpayment of federal taxes in its budget has the right not to remit import VAT (subclause 2, clause 8, article 2 of the Protocol). But then you need to submit an application to the inspectors in advance with a request to offset the overpayment. After all, inspectors have 10 working days from the date of receipt of the application to make a decision on offset (clause 4 of Article 78 of the Tax Code of the Russian Federation). If the company submits the application later, the inspectors will carry out the offset after the tax payment deadline and charge penalties.

Differences in VAT when importing goods from the Customs Union and regular imports

| What is the difference | Import from the Customs Union | Imports from countries outside the Customs Union |

| Tax base for VAT | Contract price of goods (it is not increased by additional costs for delivery, installation, etc.) | Customs value (usually the transaction price), increased by customs duty |

| Documents that need to be submitted to the Federal Tax Service to declare import tax | Declaration of indirect taxes when importing goods, application for import of goods and payment of indirect taxes, bank statement confirming payment of VAT, contract for the purchase of goods and other documents confirming import | — |

| Tax payment deadline | No later than the 20th day of the month following the month of registration of imported goods | The tax must be paid in advance at customs. Otherwise, customs officers will not release the goods into the territory of the Russian Federation |

| What documents should be registered in the purchase book in order to deduct import tax? | Application for the import of goods with inspection marks for tax payment and a payment slip for VAT payment | Customs declaration and payment invoice for transfer of import VAT |

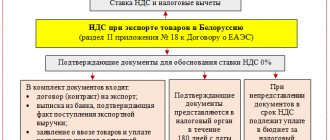

Import from Belarus to Russia: what is submitted to the tax office

For imported goods and materials, a special declaration on indirect taxes is filled out. In addition, tax officials should send a number of papers confirming the fact of import and payment of VAT to the budget.

The declaration is completed for the month in which the imported goods and materials were recorded. Moreover, if there was no fact of import, there is no need to compile it.

This declaration is sent to the inspectorate no later than the 20th day of the month following the one in which the assets were recorded. If the company had 100 or fewer employees last year, the declaration can be submitted in paper form. It should be remembered that the mandatory electronic form is provided only for regular (quarterly) VAT returns. The tax authorities themselves speak about this (letter from the Federal Tax Service of the Russian Federation for Moscow dated March 11, 2014 No. 16–15/021948).

In case of import of non-excise goods, only section 1 will be required to be completed in the declaration (in addition to the mandatory title page). In this case, the amount of import tax payable to the budget will be reflected in line 030 of section 1.

Documentation confirming import

Along with the tax declaration, it is necessary to submit a certain package of documents, or rather their certified copies (with the exception of the application for the import of goods, which is submitted in the original):

- Bank statements as confirmation of payment of import VAT (naturally, if the tax authorities decided to offset the overpayment, then it will not be needed). If we talk about how this situation works in practice, then tax officials prefer copies of payment slips with a bank mark and seal to bank statements.

- An agreement for the supply of imported goods concluded with a Belarusian counterparty. If the goods and materials were supplied through an intermediary, it is necessary to attach the corresponding intermediary agreement, as well as an information message with information about the supplier.

- Transport and accompanying papers.

- Invoices.

- Applications for the import of goods and payment of indirect taxes. It is submitted in paper form (in 4 copies), as well as in electronic form (its format is approved by order of the Federal Tax Service of the Russian Federation dated November 19, 2014 No. ММВ-7-6 / [email protected] ).

For information on the basis of which documents can be used to deduct import VAT paid by an intermediary, read the material “How to deduct VAT if an intermediary paid it at customs?”

Documents for importing goods from Belarus

Keep records of exports and imports in the Kontur.Accounting web service. Simple accounting of foreign trade activities and ruble transactions, taxes, automatic salary calculation and reporting in one service

For imported goods from the EAEU, fill out a declaration on indirect taxes in the form approved by Order of the Federal Tax Service of the Russian Federation dated September 27, 2017 No. SA-7-3 / [email protected] It includes VAT and excise taxes. If you are importing excise-free goods, enter data only on the title page and in the first section. Fill out the declaration for the month in which the imported goods are recorded.

Submit the declaration to the tax office at the place of registration before the 20th day following the month the goods were registered, and submit along with it:

- A bank statement confirming payment of VAT, or a copy of the payment order with a bank mark.

- Supply agreement with a Belarusian supplier, intermediary agreement.

- Transport and accompanying documents.

- Invoices or other documents confirming costs.

- Application for import of goods and payment of indirect taxes.

Draw up an application for the import of goods in the form approved by order of the Federal Tax Service of the Russian Federation dated November 19, 2014 No. ММВ-7-6 / [email protected] You must submit an application on paper in 4 copies and one in electronic form to the tax office, and one in electronic form, or only an electronic application certified EP.

Fill out the first section of the application and indicate your data and the supplier’s data, information about the contract and the cost of the imported goods. If you worked through an intermediary, complete the third section as well. The second section will be filled out by the tax authorities and a mark indicating the payment of VAT will be placed there.

Tax inspectors review the application within 10 working days. The tax office will keep one copy for itself, you will take one and send two to the Belarusian supplier so that he can confirm the 0% VAT rate on exports.

Application for import when importing from the Republic of Belarus

Importing companies fill out section 1 of the application, entering information about the supplier and buyer, information about the contract and the cost of imported goods and materials. Section 2 of the application is filled out by the inspectors themselves (here they also put their mark on payment of VAT). In some situations, for example, during mediation, the importer must also complete the third section.

You can download the application form on our website:

Explanations and a sample from ConsultantPlus experts will help you fill out the application, which you can view for free after receiving trial access to the system.

Inspectors review the application within 10 working days and confirm payment of VAT:

- A mark on a paper application. In this case, one copy of the application remains with the controllers, and the rest are returned to the importing company. Of these, one document is intended for the company itself, and the other 2 must be transferred to the Belarusian supplier so that he can confirm the zero export rate on his territory.

- A separate electronic document when sending an electronic application. In this case, the buyer must provide the seller with electronic or paper copies of his application and the supporting document received from the Federal Tax Service.

See also the material “When importing from Belarus, the Russian Federal Tax Service puts a mark on the application .

How is VAT deducted?

After the importer receives his copy of the application with the mark of the tax authorities, he can claim a deduction (letters of the Ministry of Finance of the Russian Federation dated 07/02/2015 No. 03-07-13/1/38180, dated 08/17/2011 No. 03-07-13/01-36) . Tax legislation (clause 2 of article 171, clause 1 of article 172 of the Tax Code of the Russian Federation) contains 3 conditions, if simultaneously met, the importer has the right to declare a VAT deduction when importing from Belarus:

- The goods were purchased for VAT-taxable transactions.

- Inventory and materials have been registered.

- Import VAT paid.

However, the rules for maintaining a purchase book, approved by Decree of the Government of the Russian Federation of December 26, 2011 No. 1137, put forward one more additional requirement: an application for the import of goods with a mark from controllers must be recorded in the purchase book indicating the number of the payment document on the basis of which VAT was paid to the budget (the date and number of the application are entered in column 3 of the book, and the details of the payment order - in column 7).

Attention! The deduction of import VAT is declared in the regular (quarterly) declaration - do not confuse it with the declaration of indirect taxes. The declared deduction amount will be reflected in line 190 of section 3 (letter of the Federal Tax Service of Russia dated October 20, 2010 No. ШС-37-3/ [email protected] ).

See also the material “What is the procedure for refunding VAT when importing goods?” .

However, there are cases when VAT paid when importing goods from the EAEU must be taken into account in their cost. Check out such cases in the Ready-made solution from ConsultantPlus for free.

Return of imports

VAT on return

Section 3 of Appendix No. 18 to the Treaty on the EAEU provides for the possibility of returning imported goods and a corresponding reduction in the amount of VAT payable in connection with the import of goods.

It is permissible to completely not reflect the import of goods in the VAT return in cases of return due to low-quality goods or non-compliance with the product configuration.

These disadvantages can be combined and present at the same time.

Failure to fill out a declaration and, accordingly, failure to pay tax according to “quality indicators” is permitted in the case of export of goods for these reasons in the same calendar month when these goods were accepted by the importer for registration. (clause 23 of section 3 of Appendix No. 18 to the Treaty on the EAEU).

It is possible that imports may not be fully or partially reflected, depending on the volume of returned goods.

Relations with tax authorities require appropriate documentation, and the exemption of the importer from VAT on returned goods is no exception.

The importer must confirm:

- Failure of the quality of the delivered goods to comply with the terms of the contract – a buyer’s claim;

- Acceptance of goods with defects by the supplier from the buyer-importer - transfer acts, transport (shipping) documents, acts of destruction of goods, etc.

In the event of a partial return of goods due to non-compliance with quality or configuration, the taxpayer-importer pays VAT on the remaining imported goods and submits the appropriate VAT return and attaches the above documents confirming the return of goods and the reasons for the return.

Let us remind you that this is how export is processed and VAT is calculated in case of return of imported goods before the expiration of the calendar month of acceptance of this goods for accounting.

Recommendation:

To document the proper processing of the return of low-quality goods, we recommend agreeing with the supplier when concluding the contract the terms and conditions and fixing them in the text:

— about the quality indicators of goods;

— on the claim procedure for resolving disputes about the quality and sequence of actions in the event of their occurrence;

— about the possibility and procedure for returning (replacing) low-quality goods;

— about the costs of returning goods;

- about document forms.

The presence in the contract of agreements on these issues will significantly reduce the time for preparing the necessary documents, eliminate controversial procedural issues, and will allow you to prepare the necessary package of documents for the tax authorities, and eliminate the possibility of requiring additional documents from the taxpayer (you can always refer to the absence of the obligation to draw up a document in the terms of the contract ).

If the goods are returned to the supplier after the expiration of the calendar month of acceptance of the goods for accounting by the importer:

- The importer is obliged to calculate and pay VAT in connection with the import of goods by the 20th day of the month following the month in which the imported goods were accepted for accounting.

- Submit the appropriate VAT tax return, which reflects the amount of VAT on all imported goods, including those that do not comply with the quality or configuration, but were not exported.

Depending on the volume of the returned goods (full or partial refund), the actions of the importer after returning the goods will differ.

Full product refund:

- The importer is required to submit an updated (additional) VAT tax return and documents (copies thereof) confirming that the goods do not comply with the quality (complete set).

- The importer DOES NOT SUBMIT an updated (in replacement of the previously submitted) application for the import of goods and payment of indirect taxes.

- The taxpayer informs the tax authority about the details of the previously submitted application for the import of goods and payment of indirect taxes, which reflected information about the fully returned goods.

These documents, together with a payment receipt for VAT when importing low-quality goods that were subsequently exported, will indicate an overpayment of VAT in connection with the import of goods.

Partial return of goods:

- The importer submits to the tax authority a revised (instead of the previously submitted) application for the import of imported goods and payment of indirect taxes without reflecting information about partially returned goods . (The actual remaining volume of imported goods is indicated)

- The importer recovers the VAT amounts previously paid when importing these goods and accepted for deduction. Reinstatement is carried out in the tax period in which the goods were returned, unless otherwise provided by the legislation of the Member State.

The VAT payment system established by Appendix No. 18 to the Treaty “On the Eurasian Economic Union” when importing goods from the territory of one state party to the treaty to the territory of another party allows, when importing goods from Belarus to Russia, to maintain the chain of VAT payers, to ensure that each payer has the opportunity to apply the state-established its location provides tax deductions, and states administer the payment of VAT.

As of October 26, 2021

Tax lawyer Gordon Andrey Eduardovich

Chamber of Lawyers of the Moscow Region

What to do with deadlines

In practice, there are often situations when VAT on imports from Belarus is paid in one quarter, and the importer receives a tax mark on the application in the next. According to officials, in this case, VAT is deducted only after the appropriate mark is made (letter of the Ministry of Finance of the Russian Federation dated July 2, 2015 No. 03-07-13/1/38180).

However, judges in such situations often take the side of taxpayers who claim a deduction during the period of actual payment of VAT to the budget, without waiting for the inspectors’ mark (Resolution of the Federal Antimonopoly Service of the Moscow District dated July 25, 2011 No. KA-A41/7408–11). However, if you don’t want to argue with the tax office, then it would be more advisable to wait for the mark.

Results

Goods imported from the EAEU countries (including from Belarus) are subject to VAT at regular rates (20 and 10%), unless they are exempt from tax. Payment of such tax is mandatory for all importers, regardless of the tax regime they apply. The deadline for payment and reporting of tax accrued on imports from the EAEU expires on the 20th day of the month following the reporting month.

The reporting is presented by an indirect tax declaration and an import statement, accompanied by copies of documents confirming the import and payment of tax. For a month in which there are no import transactions, reporting is not submitted. The paid tax, subject to the acceptance by the Federal Tax Service of the import documents, is subject to deduction.

See also our articles:

- “VAT on imports from Kazakhstan to Russia”;

- “VAT on the import of goods from Kyrgyzstan to Russia”;

- “VAT on the import of goods from Uzbekistan to Russia”;

- “Payment and restoration of VAT when importing goods from China to Russia.”

Sources:

- Tax Code of the Russian Federation

- Decree of the Government of the Russian Federation of April 30, 2009 N 372

- Decree of the Government of the Russian Federation of December 31, 2004 N 908

- Order of the Federal Tax Service of Russia dated November 19, 2014 N ММВ-7-6/ [email protected]

- Decree of the Government of the Russian Federation of December 26, 2011 N 1137

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

Payment order for VAT payment

General details

A payment order for the payment of VAT to the budget when importing from the EAEU countries is generated using the Payment order in the Bank and cash desk - Bank - Payment orders section.

In this case, it is necessary to correctly indicate the type of transaction Tax payment , then the document form takes the form for payment of payments to the budget system of the Russian Federation.

You can also quickly generate a payment order using the Tax Payment Assistant :

- through the section Main – Tasks – List of tasks;

- through the section Bank and cash desk – Payment orders using the Pay button – Accrued taxes and contributions.

Please pay attention to filling out the fields:

- Tax – VAT on goods imported into the territory of the Russian Federation , is selected from the Taxes and Contributions directory.

VAT on goods imported into the territory of the Russian Federation is predetermined in the Taxes and Contributions directory. Parameters are set for it

- corresponding KBK code;

- text template inserted into the Payment purpose ;

- tax account.

If an element is predefined in the directory, then deleting it or changing its parameters is not recommended. If necessary, BukhExpert8 advises creating a new element in the Taxes and Contributions , where you specify your settings.

- Type of liability – Tax . The choice of the type of obligation affects the BCC, which will be indicated in the payment order;

- The order of payment is 5 Other payments (including taxes and contributions) , filled in automatically, as for all tax payments to the budget paid on time (clause 2 of Article 855 of the Civil Code of the Russian Federation).

Recipient details – Federal Tax Service

Since the recipient of the VAT is the tax office with which the taxpayer is registered, it is its details that must be reflected in the Payment order .

- The recipient - the Federal Tax Service, to which the tax is paid, is selected from the Counterparties directory.

- Recipient's account – bank details of the tax authority specified in the Recipient .

Currently, in the 1C program it is possible to use the 1C: Counterparty service, which allows you to automatically fill in and monitor the relevance of the details of government bodies.

If the details are no longer relevant, the 1C:Counteragent will offer to update them in the Counterparties directly from the payment order form. PDF

- Recipient's details - TIN , KPP and Recipient's name , these are the data that are used to print the payment order. If necessary, the recipient's details can be edited in the form that opens via the link.

Filling out payment details to the budget

The accountant needs to control the data that the program fills in using the link Payment details to the budget .

In this form, you need to check that the fields are filled in:

- KBK – 18210401000011000110 “Value added tax on goods imported into the territory of the Russian Federation.” KBK is entered automatically from the Taxes and Contributions directory.

If the KBK is not known for any payment to the budget, then you can use the KBK Designer by following the link to the right of the KBK .

- OKTMO code is the code of the territory in which the Organization is registered. The value is filled in automatically from the Organization directory ;

- Payer status - 01-taxpayer (payer of fees) - legal entity ;

If a payment order for the payment of VAT is issued by an individual entrepreneur, then his payer status will be 09 - taxpayer (payer of fees, insurance premiums and other payments administered by tax authorities) - individual entrepreneur .

- UIN - 0 , because The UIN can only be specified from the information in tax notices or requests for payment of tax (penalties, fines);

- Basis of payment - TP payments of the current year , is entered when paying the tax on time;

- Tax period - MS-monthly payment , the tax period for VAT when importing from the EAEU is equal to a month, and not a quarter, as for VAT on the domestic market;

- Year – 2018 , the year for which the tax is paid;

- Month – 4 , the number of the month for which the tax is paid;

- Document number – 0 , the document on the basis of which the payment is made is a declaration, and it does not have the requisite Number ;

- Document date – 0 , payment is made before the date of signing the declaration, i.e. date is not determined (clause 4 of Appendix No. 2, approved by Order of the Ministry of Finance of the Russian Federation dated November 12, 2013 No. 107n).

Find out more about the details of payments to the budget in the article Payment order details .

- Purpose of payment – filled in automatically using a template from the Taxes and Contributions directory. The field can be edited if necessary;

You can print a payment order by clicking the Payment order . PDF