Bill payments

Payments by bill of exchange - 2021 - 2021 are one of the forms of non-monetary payments used in the economic market.

These types of transactions are regulated by special norms of bill of exchange legislation, however, in the absence of such special norms, the general norms of the Civil Code of the Russian Federation (hereinafter referred to as the Civil Code of the Russian Federation) should be applied to them, taking into account their features (clause 1 of the resolution of December 4, 2000 of the Plenum of the Armed Forces of the Russian Federation No. 33, Plenum Supreme Arbitration Court of the Russian Federation No. 14, hereinafter referred to as Resolution No. 33/14).

Thus, the main regulatory legal acts of bill of exchange legislation are:

- Law “On promissory notes and bills of exchange” dated March 11, 1997 No. 48-FZ (hereinafter referred to as Law No. 48-FZ);

- Resolution of the Central Executive Committee of the USSR and the Council of People's Commissars of the USSR “On the implementation of the Regulations...” dated 08/07/1937 No. 104/1341 (hereinafter referred to as Regulation No. 104/1341).

The general rules in relation to transactions with bills include Art. 143, 153–181, 307–419 of the Civil Code of the Russian Federation (from 06/01/2018, Articles 815–816 of the Civil Code of the Russian Federation lost force).

Bill settlements: pros and cons

M. Kolosov, columnist for the Federal Financial Information Agency

One of the main features of any financial crisis is a noticeable lack of money in the economy. It is likely that for this reason, bills of exchange will soon begin to circulate again in settlements between counterparties, as in the good old days. Experts warn against using schemes that can no longer be “resuscitated.”

Most well-known tax consultants and experts over the past several years have characterized any complex financial schemes using taxpayers' own promissory notes or non-bank promissory notes of third parties as transactions with medium or high tax risk. The reason is that, according to tax authorities, the use of such forms of payment is almost always associated with tax evasion. At the same time, a more convenient and reliable financial instrument simply does not exist yet. It is also important that only this security is indisputably recoverable. In case of refusal to pay, a protest is made at the notary. This procedure is completed within several days following the date of payment.

In general, a bill of exchange is a simple and unconditional obligation to pay a certain amount of money. In other words, it's practically an IOU. The main document regulating the procedure for drawing up, issuing and repaying bills of exchange is the Regulations on bills of exchange and promissory notes (approved by Resolution of the Central Executive Committee of the USSR and the Council of People's Commissars of the USSR dated August 7, 1937 No. 104/1341).

According to its legal nature, a bill of exchange can be used in business activities in several capacities: as an independent item of purchase and sale, as a way to attract borrowed funds, as a means of payment.

In war as in war

In some cases, tax authorities’ claims to transactions involving bills of exchange are quite justified. Moreover, even taxpayers themselves cannot always explain the use of this financial instrument by the presence of an independent business purpose and economic feasibility. As a rule, this happens in tax disputes where there is a sale of questionable bills of exchange or participation in transactions of liquidated legal entities, or even persons whose information is not available in the Unified State Register of Legal Entities. Appealing judicial decisions with a negative result for the taxpayer is extremely difficult.

As an example, we can cite the resolution of the Federal Antimonopoly Service of the North-Western District dated December 23, 2005 No. A56-8583/2005. According to the circumstances of the case, the taxpayer purchased bills of exchange from third parties for 43 million 800 thousand rubles. These bills were sold two days after the purchase for 31 million 650 thousand rubles. For profit tax purposes, the company took into account the amount of 43 million 800 thousand rubles as non-operating expenses, and the amount of 31 million 650 thousand rubles as non-operating income, thereby receiving a loss in the amount of 12 million 150 thousand rubles. The company justified the economic justification of its actions by the fact that as a result of resale of bills at a cost less than they were purchased, it used funds, which is similar to obtaining a loan from a bank. Obtaining a loan from a bank is a more complex, time-consuming and expensive operation. However, the court considered the costs to be economically unjustified due to the fact that the taxpayer’s actions were initially and intentionally aimed at generating a loss in the transaction.

Another interesting example of a bill of exchange scheme is discussed in the resolution of the Federal Antimonopoly Service of the Ural District dated April 25, 2006 No. F09-3019/06-S7. From the circumstances of the case it is clear that the taxpayer issued, exchanged his own bills of exchange and sold them to related parties with a negative discount, including the amount of such discount in expenses. The evidence presented by the tax authority, according to the court, indicates that the taxpayer has created an artificial scheme to increase costs in order to minimize the tax base for income tax. At the same time, the servants of Themis noted that all bill transactions were unprofitable, and therefore, their economic inexpediency is obvious.

The reputation of bills of exchange has also been shaken due to their involvement in schemes related to illegal cash withdrawals. Let us immediately note that the tax service very successfully suppresses such maneuvers, since its representatives know for certain all the nuances of such operations.

"Housing problem

Separately, I would like to note the “optimization” method that was once used, as a result of which not only the budget, but also buyers of real estate lost significant amounts. Its essence boiled down to the following: persons wishing to purchase an apartment contacted a real estate agency and entered into an investment agreement for the construction of housing. In turn, settlements under the agreement were carried out, in particular, with bills purchased from organizations dependent on the real estate agency.

In the scandalous case of ZAO MIAN, the Moscow Arbitration Court recognized as legitimate the tax claims of the Federal Tax Service of Russia to the amount of about 1 billion rubles. Higher authorities upheld the court's decision, thereby making it one of the most high-profile tax cases involving the use of “bill schemes.”

As follows from the case materials, the tax authority, when conducting a repeat tax audit, in particular, found that individuals or legal entities wishing to purchase apartments applied to CJSC MIAN. The company offered to conclude an investment agreement for housing construction. Payment under the investment agreement was accepted only by bills of exchange. The bills, in turn, were purchased from organizations dependent on CJSC MIAN. Next, the investment agreement was terminated and an agreement was concluded on the assignment of the right to claim the apartments, according to which the buyers acquired the rights to receive ownership of the apartments. The arbitration court found that the bills received as payment were taken into account by the company at a price significantly lower than the nominal price. Thus, CJSC MIAN understated revenue and transferred the money received for the rights to apartments to a company that did not pay taxes on them. The rights to the apartments were also sold by a company controlled by MIAN CJSC.

Alternative to credit

At the same time, it is worth noting that in the 90s there was practically not a single financial instrument that would not have discredited itself to one degree or another. Just remember “defaulted” GKOs, “burnt” deposits, etc. Moreover, it would be unfair to say that the use of bills of exchange is always aimed only at tax evasion, and therefore, conscientious taxpayers should forget about this financial instrument. After all, in the end, with its help, companies can solve a lot of current short-term problems, such as investing free funds, when a bill of exchange acts as an independent subject of purchase and sale, as well as attracting borrowed funds. It can also act as a means of payment.

Currently, many organizations, due to the current economic situation, are experiencing a sharp shortage of working capital. Of course, no one forbids applying for a loan from a bank, but... Credit organizations now “feel” no better, and therefore put forward rather strict requirements for applicants for borrowed funds. At a minimum, they will have to provide adequate security for the loan, as well as involve guarantors in this matter, naturally, revealing almost all of their ins and outs to the credit institution.

However, this problem can be solved by issuing your own bills. This procedure does not require any permits or licenses. In addition, since a bill of exchange is not an issue-grade security (Article 2 of the Law of April 22, 1996 No. 39-FZ “On the Securities Market”), there is no need to register this operation and, accordingly, to pay state duty and remuneration to the depository. In other words, the company can produce the issue independently. True, you will still have to disclose the necessary information about the organization. Otherwise, a potential investor simply won’t take the bait. If one is already available, and moreover, he intends to invest his funds in the company’s securities, then, as they say, there is little to do.

Otherwise, you should contact special organizations that deal with the placement of bill programs. Brokers, being active participants in the bill market, can offer their existing clients to purchase these securities. In other words, a fairly wide range of potential investors participates in the “turnover”. However, reputation is most valuable, and therefore information about the company placing the bills, including the purposes for which the proceeds will be used, will be fully disclosed to interested parties.

Bill settlement

The use of bills of exchange as a means of payment allows some companies to expand the circle of buyers and increase turnover; and allows others, without stopping their activities, to receive the necessary raw materials, goods, materials, etc. from the supplier.

In the current conditions, when every client is practically worth his weight in gold, suppliers often have to defer payment for shipped goods. In turn, buyers are not always ready to pay for the purchase in full. In this case, the so-called bill of exchange comes to the rescue, which is issued as payment for goods, work or services.

In practice, working with a bill of exchange occurs as follows. If a trusting relationship has been established between business partners, then the buyer pays the supplier with his own bill of exchange. Upon expiration of the agreed period, the bill will be presented for payment, and the executor will not only return the funds, but will also receive the corresponding interest. By the way, you can also pay the supplier with a bill of exchange issued by a third-party issuer.

Just in case, fireman

But, as they say, in every barrel of honey there is a fly in the ointment. In other words, a situation cannot be ruled out when the organization that issued the bill, unable to cope with economic problems or for other reasons, will be liquidated. Will the bill holder be able to take into account the losses incurred in connection with this? The Ministry of Finance devoted a letter dated September 4, 2008 No. 03-03-05/99 to the answer to this question. Representatives of the financial department admitted that the provisions of paragraph 10 of Article 280 of the Tax Code allow companies that have received a loss from transactions with securities to take it into account when calculating income tax, including deferring it to future periods. However, as financiers noted, the procedure for accounting for damage in the form of the purchase price of securities of a liquidated company is not established by tax legislation.

Obviously, the supplier must have “insurance” against such unpleasant consequences. The problem can be solved with the help of a third party guarantee, that is, aval. The bottom line is that this very person accepts responsibility to the owner of the bill for fulfilling obligations if the drawer is unable for some reason to repay his obligation on time. Of course, in this situation the reliability of the security automatically increases.

Summary

To summarize, I would like to note once again that dubious bill of exchange transactions aimed solely at reducing the tax burden of VAT and income tax are now more than ever under the close attention of representatives of the Federal Tax Service. It is also logical that in a financial crisis it is worth discarding those optimization methods that the tax service has already noted as aimed at tax evasion. As a rule, such risky operations include methods, the use of which has become widespread, and which fall under the criteria formulated in the Concept for Planning Tax Audits, approved by Order of the Federal Tax Service of May 30, 2007 No. MM-3-06 / [email protected] ( as amended by the order of the Federal Tax Service of October 14, 2008 No. MM-3-2 / [email protected] ).

At the same time, you should not completely abandon the use of bills of exchange in business activities. After all, this financial instrument opens up a lot of opportunities for companies to free up working capital, as well as to optimize accounts receivable and payable.

Features of settlements using bills of exchange

These features include the following:

- the drawer and holder of the bill can be either a citizen or a legal entity (Article 2 of Law No. 48-FZ), including in cases established by law - an administrative-territorial unit;

- only a monetary obligation can be transferred under a bill of exchange;

- the bill of exchange can be executed exclusively on paper (Article 4 of Law No. 48-FZ, Clause 2 of Resolution No. 33/14);

- a bill of exchange can be simple (under which the drawer undertakes to pay the corresponding amount to the holder of the bill) or transferable (under which the drawer issues the bill to the holder of the bill, and payment for it is made by a third party who has assumed such an obligation by acceptance);

- the list of mandatory details of a promissory note is enshrined in clause 75 of regulation No. 104/1341, the details of a bill of exchange - in clause 1 of the said regulation.

ACCOUNTING FOR SETTLEMENTS USING BILLS [p.251]

Accounting for settlements with bills of exchange from recipients. Currently, it is recommended that accounting for settlements using bills of exchange be carried out according to a simplified scheme on those accounts that reflect settlements without the use of bills of exchange. Selection of settlements using bills of exchange is carried out in analytical accounting. i [p.252]

Accounting for settlements using bills of exchange can be carried out according to a simplified scheme. According to the current chart of accounts, debts to suppliers and contractors from the organization that issued the bill (drawer) are not written off from account 60 Settlements with suppliers and contractors, but are allocated in analytical accounting separately on a separate subaccount 2 Bills issued. Bills of exchange with overdue payment terms are allocated separately in analytical accounting. [p.175]

Accounting for settlements using bills of exchange [p.240]

A bill of exchange is a convenient form of granting and receiving a commercial loan. Under current practice, it should be taken into account by the supplier as part of the debt on other debt obligations secured by bills of exchange and reflected in accounts 94 Short-term loans and 95 Long-term loans. As with current settlements using bills of exchange, debt on short-term and long-term loans secured by issued bills of exchange is not immediately written off from the accounts of long-term and short-term loans, but is only separated in analytical accounting. [p.176]

Settlements using bills of exchange. In international payments, bills of exchange are used, issued by the exporter to the importer. Draft is a document drawn up in the form prescribed by law and containing an unconditional order from the creditor (drawee) to the borrower (drawee) to pay within a specified period of time a certain amount of money to a third party (remitee) or bearer named in the bill. D The acceptor, who is the importer or the bank, is responsible for paying the bill. The cash flows accepted by banks can easily be converted into cash through accounting. [p.62]

Accounting for settlements using commercial bills [p.336]

Accounting for settlements using commodity bills Synthetic accounting is maintained in railway stations No. 11, 15 and statement 2. [p.340]

When using bills of exchange in an organization, the auditor should first of all determine which bill of exchange the payment was made with - commodity or financial, since this is of significant importance for accounting and taxation purposes. [p.393]

Claims arising from organizations in connection with the use of bills of exchange are reflected in accounting using account 63 Calculations for claims, subaccount Claims for bills of exchange, (as amended by the letter of the Ministry of Finance of the Russian Federation dated July 16, 1996 No. 62) [p.110]

When checking settlements using various forms of non-cash payments, the presence of all supporting documents is determined, and, if necessary, counter reconciliations are carried out at the bank or with the buyer. Particular attention is paid to the correct reflection in accounting and taxation of transactions using bills of exchange. The auditor should take into account that the amount of bill interest on bills received is charged to account 80 Profit and Loss, the obligation to pay VAT to the budget arises upon receipt of funds (goods or when offsetting a counterclaim) on the bill. [p.159]

On the issue of regulating the procedure for reflecting in the accounting records of the bill holder settlements on claims in connection with non-acceptance or non-payment of bills, the Instructions for the application of the Chart of Accounts for the accounting of financial and economic activities of enterprises and the letter of the Ministry of Finance of the Russian Federation dated October 31, 1994 No. 142 come into some contradiction. Letter No. 142 of the Ministry of Finance of the Russian Federation, which defines the rules for accounting for commercial bills of exchange, prescribes in paragraph 2 that the construction of analytical accounting for accounts 62, 60, 76, etc. should ensure the receipt of the necessary data on the amounts of bills received and issued and separately interest on them in the context of issued bills of exchange, the payment period of which has not arrived; received bills of exchange, the payment period of which has not arrived; issued bills of exchange with an overdue payment period; received bills of exchange with an overdue payment period; and in paragraph 3 it establishes that claims arising from enterprises in connection with the use of bills of exchange, are reflected in the accounting records in account 63 Settlements on claims, subaccount Claims on bills of exchange. Instructions for using the Chart of Accounts state that account 63 Calculations for claims is intended to summarize information on calculations for claims presented to suppliers, contractors, transport and other organizations, as well as for fines, penalties and penalties presented to them and recognized (or awarded). So [p.139]

In accordance with these instructions, accounting for settlements between buyers and sellers for goods sold (work, services) using bills of exchange is carried out in the general manner without introducing special accounts for accounting for bills of exchange into the Chart of Accounts for accounting the financial and economic activities of enterprises. [p.33]

To secure a loan, the borrower can issue (transfer) a bill of exchange to the lender. A bill is an unconditional monetary debt obligation drawn up in the form established by law, issued by one party (the drawer) to the other party (the holder) and paid with stamp duty. A bill of exchange performs two important economic functions: a means of payment and a lending instrument. The economic essence of a bill as a security and the procedure for accounting for bills are discussed in Chapter. 21 Non-cash payments using plastic cards and bills. [p.341]

Accounts receivable for bills received arise in settlements with counterparties if the organization accepted the bill as a means of payment. This debt is accounted for on account 62 Settlements with buyers and customers, subaccount 62-3 Bills received, and in the case of acceptance of bills for non-commodity transactions - on account 76 Settlements with various debtors and creditors. Payments by bills of exchange and accounting of bills received are discussed in detail in Chapter 21 Non-cash payments using plastic cards and bills of exchange. [p.384]

Accounting by the drawer of debt on bills issued is discussed in Chapter 21 Non-cash payments using plastic cards and bills. [p.570]

The simple interest scheme is used in banking practice when calculating interest on short-term loans with a repayment period of up to one year. In this case, the indicator n is taken to be a value characterizing the share of the length of the sub-period (days, month, quarter, half-year) in the general period (year). The length of various time intervals in calculations can be rounded month - 30 days quarter - 90 days half year - 180 days year - 360 (or 365) days. Another very common short-term operation using the simple interest formula is the operation of discounting bills by a bank. In this case, use the formulas [p.147]

Settlements using bills and checks. In international payments, bills of exchange are used, issued by the exporter to the importer. Draft is a document drawn up in the form prescribed by law and containing an unconditional order from the creditor (drawee) to the borrower (drawee) to pay within a specified period of time a certain amount of money to a third party (remitee) or bearer named in the bill. The acceptor, who is the importer or the bank, is responsible for paying the bill. Drafts accepted by banks can easily be converted into cash by accounting. The form, details, conditions for issuing and paying drafts are regulated by bill of exchange legislation, which is based on the Uniform Bill of Exchange Law adopted by the Geneva Bill of Exchange Convention of 1930. The prototype of drafts was those that appeared in the 12th-13th centuries. covering letters requesting payment to the submitter (usually the merchant) of the appropriate amount in local currency. With the development of commodity-money relations and the globalization of economic relations, the bill has become a universal credit and settlement document. The use of a draft in addition to collection and letter of credit gives the right to receive credit and foreign exchange earnings. [p.227]

Q in primary accounting documents (invoices, invoices, invoices, certificates of completion of work, etc.), on the basis of which calculations are made in barter transactions, prepayment (advances), settlements using bills of exchange and offset of mutual claims. / Consequently, for the purposes of accounting for settlements with the budget for value added tax, it is necessary to fulfill the requirement to highlight the tax amount as a separate line in the primary documents drawn up when conducting mutual offset transactions (an application for offset, a statement of reconciliation of calculations, an act of offset of mutual claims, a protocol on the offset, agreement on repayment of mutual obligations). [p.203]

Financial accounting (Financial accounting) is a system for collecting, summarizing and storing information about the use of all funds and resources of the financial and economic activities of the company. It includes accounting for settlements with suppliers, customers, other organizations and individuals, as well as accounting for all financial transactions (shares and dividends, bonds and bills, loans and interest, investments). Based on financial accounting data, a financial result (company profit or loss) is identified and financial statements are drawn up: a balance sheet (balance sheet), an income statement (profit and loss statement), a statement of financial position, etc. This information is expressed by a set of formed economic indicators on which the company's financial statements are based. In turn, financial statements serve as a source of data for investors, banks, tax and statistical authorities, for regulatory authorities (auditors), for the preparation of periodic reports submitted to the shareholders of the company. [p.220]

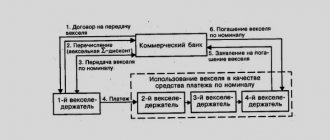

General scheme of bill payments

The scheme for settlements with bills in the general case is as follows:

- When paying with simple bills:

- the buyer of goods/recipient of services (drawer) issues a bill of exchange to the seller/service provider (drawer) as confirmation of his obligation to pay for the goods/services in the future;

- the holder of the bill fulfills his obligation to the drawer, for example, through the sale of goods or the provision of services;

- the holder of the bill presents the bill for payment;

- repayment of a promissory note directly by the drawer, i.e. fulfillment of the obligation to pay for a good or service.

- When paying with bills of exchange:

- the buyer of goods / recipient of services (drawer, drawer) sends to the debtor (drawee) a bill of exchange (draft) issued in the name of the recipient of funds (remitee), for example, the seller;

- the drawee sends the accepted bill to the drawer (if the drawee does not accept the bill, the bill of exchange is subject to notarization);

- the drawer transfers such a bill to the remitter by means of an endorsement - an endorsement (Chapter II of Regulation No. 104/1341);

- the remitter presents the bill of exchange to the drawee for payment;

- the drawee carries out the cancellation of the bill, i.e. payment. IMPORTANT! When resolving disputes related to bill settlements, the following conclusions of the law enforcement officer may be useful (see the decision of the Supreme Court of the Russian Federation dated February 15, 2018 No. 305-ES17-17027 in case No. A40-90813/2016):

- if a promissory note is not presented, the holder loses his rights in relation to persons obligated under the bill, except the drawer;

- the drawer of a promissory note is obliged in the same way as the acceptor of a transferable bill;

- the claims of the holder of the bill against the drawer arising from the promissory note are extinguished upon the expiration of three years from the date of payment.

What types of bills are there?

The Geneva Convention describes two types of bills of exchange - bills of exchange and promissory notes. We have already explained how they differ. However, over time, additional types have appeared, which depend on the type of issuer, purpose and other features:

- Personal bill and order. By name, only the person indicated in the document can claim the debt. By order, the debt must be given to the person who presents it for payment. Sometimes it is also called blank.

- Advance - issued against future work that is yet to be completed. This could be the release and sale of goods or the provision of services. Issued by the debtor upon receipt of a loan.

- Bank - issued to the person who provided the loan to the bank.

- Treasury - issued by the Central Bank on behalf of the government of the country. Usually issued for a period of no more than six months.

- Commodity - acting as security for the purchase and sale of goods. It is used in a system of relations between entrepreneurs, which excludes bank intermediation.

Bills of exchange can also be fraudulent. Sometimes there is a mention of a “bronze” bill. This is the name of a document in which the recipient of the debt is a fictitious person. Interestingly, according to bill of exchange law, such a document is valid. It is called “bronze” in the case when there is no real transaction behind it, which leads to the emergence of a debt between the drawer and the holder of the bill. Such paper is used mainly in fraudulent schemes for obtaining loans from banks, or in “sham transactions”. Despite this, it is quite difficult to prove that this document is void from a legal point of view.

The so-called “friendly” bill works in a similar way. The bottom line is that two persons issue each other counter debt obligations with the same conditions. You can then provide them to the bank for credit or pay for goods.

Circulation of bronze and friendly bills of exchange is prohibited in Russia.

What does a bill of exchange mean and why is it issued?

Payment by bills is carried out between sellers and buyers. The financial instrument provides deferred payment. The document has a strict form and filling rules. The signing involves the drawer (issuer, borrower) and the holder of the bill - creditor, recipient of the benefit.

The recipient can demand repayment of the loan from the debtor.

Characteristics of the bill:

- Indisputability. The debt is repaid in full in any situation.

- Unconditionality.

- Only monetary form.

- Appealability. Transferable without restriction from one owner to another by means of a deed of conveyance without the consent of the issuer.

- Independence and distraction from other transactions. It itself has value and legal status separately from additional conditions.

- Form of strict accountability

Main functions:

- Deferred payment for goods and services. A bill of exchange acts as security for a transaction.

- Obtaining and processing a loan. Bills of exchange are used to pay for material assets, services, repay loans, and issue loans. Lenders are comfortable with its strict form and ease of transfer, as well as the guarantee of debt repayment within the specified period.

The paper simultaneously ensures repayment of the debt and records its occurrence. The importance of this instrument is that it passes through several holders before maturity, extinguishes obligations with less money in circulation and speeds up settlements.

Who can write him out?

The right to draw up your own bill of exchange is called bill of exchange capacity. It can be produced by both companies and individuals. A person who can issue a credit ticket and be responsible for financial obligations must be an adult (over 18 years old) and mentally healthy.

Where and when can you use them?

The use of bill schemes is not limited to commodity turnover. Companies are attracting additional financial resources and restructuring accounts payable. The number of bills issued is not limited, so they are issued as an infusion of money is needed.

Types of operations:

- emission;

- sale to attract investment;

- accounting of issued and canceled forms to prevent “gray” schemes and counterfeits in the stock market;

- issuing or conducting mutual settlements;

- repayment.

Payment is possible at the end of the term or at the request of the lender. Without specifying the deadline, the receipt is considered invalid. Urgent bills require special care, since after the expiration of the term, payment of the debt is made only by agreement of the parties.

To be on the safe side before handing over the bill to the payer, I recommend making a copy of it.

When concluding a commodity transaction, the bill circulation scheme looks like this:

- After agreement, the goods are delivered to the buyer.

- The debtor's bank accepts (accepts for payment) the bill.

- The document is presented on the specified date.

- A payment order is made to the seller's account.

How to check

The issue of checking a security is especially acute if you did not receive it directly from the debtor. Banks conduct it in the presence and at the request of the client. When applying in writing, the registration of the document in the securities register is confirmed or refuted, the authenticity of the form and all marks made are verified.

To avoid being deceived, remember the following:

- The paper is considered invalid if the form prescribed by the regulations is violated.

- A document will be considered a forgery if some parts of it are falsified.

- There should be no errors or corrections in the content; information about the owner is genuine.

- The printing quality of counterfeit samples is revealed by blurry prints and excessively bright colors, glare on the main information, or poor paper quality.

The most reliable way to verify the authenticity of a debt obligation is to contact the issuer.

Is a bill of exchange a security?

Yes. According to Russian legislation, it meets this definition according to the following criteria:

- Established form of compilation and execution.

- Mandatory information about all participants.

- Contains and confirms a description of rights that are transferred only with the document and upon its presentation.

What does it look like

This is what a photo of the bill of exchange looks like. It can be downloaded online for free or purchased in the required quantity and design.

Required details

Very strict requirements are imposed on the form of the bill. It is drawn up on a regular sheet of paper or on letterhead, it depends on the drawer. The recipient of the payment may be indicated, but the document can be drawn up without this.

Required details include:

- A bill of exchange mark or designation of the type of document, such as "promissory note."

- Date and place of document preparation.

- An obligation to pay a debt amounting to a specified amount. It is indicated in numbers and words.

- Date and place of payment.

- Details of the payer and creditor. The order (to bearer) form does not indicate the recipient.

- Signature of the owner of the security (issuer).

- Details of the payer (for a bill of exchange).

It is very important to fill out the document without corrections, not to leave blank fields, and not to allow abbreviations. The receipt is invalid if errors are made in the design.

Acceptance

An accepted bill confirms the payer’s agreement to pay the debt specified in it. Until the acceptance is issued, the obligations lie with the issuer, after signing - with the drawee. This is the person indicated in the document as the payer).

The beneficiary can present a receipt for payment or transfer it to another person. For the operation, an endorsement (endorsement) on the back of the form is sufficient. The number of signatures on the transfer is not limited.

In addition to confirmation in circulation, a bill of exchange protest is often used. The act records the payer’s refusal to make the payment or indicate its exact date. Unaccepted papers go out of circulation and cannot be presented for payment or protested against non-payment.